link to page 2 link to page 16 link to page 26 link to page 28 link to page 28 link to page 45 link to page 45

Table of Contents

1.

The Income Tax and Transfer System

1

2.

Negative Income Tax Systems

15

3.

Modelling a Cost-Neutral Guaranteed Minimum Income (GMI) Scheme

25

4.

The Treasury’s position on income adequacy and poverty: previous advice and

27

potential directions

5.

The Treasury’s position on income adequacy and poverty: previous advice and

44

potential directions - Slide Pack

20180164 TOIA Binder New

Doc 1

Page 1 of 62

DRAFT – FOR OFFICIAL USE ONLY

IN-CONFIDENCE

The income tax and transfer system: issues and

options

This note is intended to be an internal resource for officials to support the analysis of tax and

transfer settings. It is not government policy or advice.

The scope of this report is the personal income tax system and the transfer payments (benefits,

supplementary assistance and tax credits) received by working-age individuals and families. This

report discusses the broad structure of the tax and transfer interface and does not evaluate each

individual transfer payment. Retirement income policy is not within scope.

Deleted - Not Relevant to Request

1. Deleted - Not Relevant to Request

2.

3. The nature of work is changing, which poses challenges for the tax and transfer system.

There is greater diversity of working arrangements than in the past and there may be

greater use of the social safety net in the future to support workers as they transition

between occupations. Some argue that a universal basic income (UBI) should be introduced

to reduce job insecurity in this environment. However, there is not a strong case for a UBI in

New Zealand as it would reduce the effectiveness of the welfare system in reducing poverty,

although overseas pilot studies should be monitored for their outcomes.

Deleted - Not Relevant to Request

4. Deleted - Not Relevant to Request

5.

6.

7.

1

20180164 TOIA Binder New

Doc 1

Page 2 of 62

DRAFT – FOR OFFICIAL USE ONLY

IN-CONFIDENCE

Deleted - Not Relevant to Request

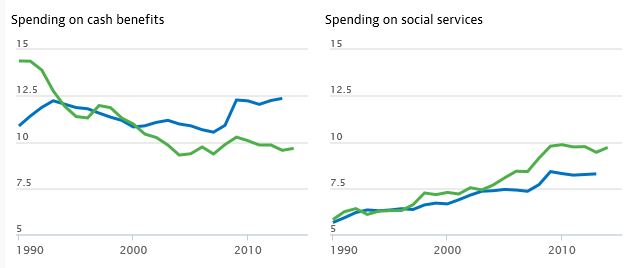

Cash transfers are one component of overall social spending. New Zealand’s social spending is

approximately equally split between cash transfers and social services (around 10% of GDP is spent

on each). For the working-age population, two-thirds of social spending is through in-kind support

and one-third is in cash transfers.

2

20180164 TOIA Binder New

Doc 1

Page 3 of 62

DRAFT – FOR OFFICIAL USE ONLY

IN-CONFIDENCE

FIGURE 1 - SPENDING ON CASH BENEFITS AND SOCIAL SERVICES

OECD

New Zealand

New Zealand

OECD

Source: OECD

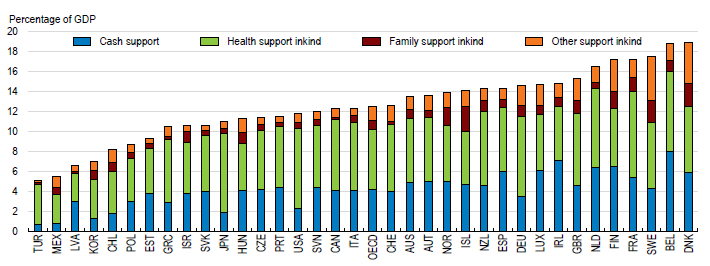

FIGURE 2 - PUBLIC SOCIAL SPENDING ON THE WORKING-AGE POPULATION

Source: OECD

Deleted - Not Relevant to Request

3

20180164 TOIA Binder New

Doc 1

Page 4 of 62

DRAFT – FOR OFFICIAL USE ONLY

IN-CONFIDENCE

Deleted - Not Relevant to Request

4

20180164 TOIA Binder New

Doc 1

Page 5 of 62

DRAFT – FOR OFFICIAL USE ONLY

IN-CONFIDENCE

Deleted - Not Relevant to Request

y

5

20180164 TOIA Binder New

Doc 1

Page 6 of 62

DRAFT – FOR OFFICIAL USE ONLY

IN-CONFIDENCE

Deleted - Not Relevant to Request

There are two fundamental types of structures for income transfers: 1) a universal basic income or

2) means-tested benefits. Both can achieve a poverty alleviation goal and create a progressive

effective tax rate structure. However, there will be different properties in terms of average and

marginal tax rates. Related to this is the concept of target efficiency. A universal basic income is

simple but is also received by the whole population, which means that some receive a transfer that

is not necessary to alleviate poverty. It is typically associated with a high average tax rate to fund the

universal transfer payment. Means-tested benefits generally have greater target efficiency but are

associated with potentially higher effective marginal tax rates for recipients as benefits are abated.

Deleted - Not Relevant to Request

6

Pages 7-25 Deleted - Not Relevant to Request

20180164 TOIA Binder New

Doc 1

Page 7 of 62

DRAFT – FOR OFFICIAL USE ONLY

IN-CONFIDENCE

FIGURE 21 – SOCIAL EXPENDITURE BY AGE OF CHILD IN NEW ZEALAND

$ (PPP per capital USD)

Cash benefits

Childcare

Other benefits in kind

Education

14,000

12,000

10,000

8,000

6,000

4,000

2,000

0

atal

0

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

21

22

23

24

25

26

27

28

29

en

Pr

Age of child

Source: OECD. Note: Data is for 2011, but pattern would be expected to be similar in 2017.

Deleted - Not Relevant to Request

26

Pages 27-31 Deleted - Not Relevant to Request

20180164 TOIA Binder New

Doc 1

Page 8 of 62

DRAFT – FOR OFFICIAL USE ONLY

IN-CONFIDENCE

Part 2: Options

The options that are considered will depend on objectives. We discuss the general issues relating to

addressing barriers to employment and income adequacy.

Options to addressing barriers to employment

Deleted - Not Relevant to Request

A universal basic income avoids the question of varying incomes from wages or salaries, since - by

definition – this kind of payment is not conditional on earned income. In a highly targeted transfer

system, however, state income support is withdrawn as income from wages and salaries increases.

This can have the perverse impact of discouraging people from taking up more employment. Income

taxes combine with abatement of transfers create high effective marginal tax rates.

Deleted - Not Relevant to Request

32

Pages 33-47 Deleted - Not Relevant to Request

20180164 TOIA Binder New

Doc 1

Page 9 of 62

DRAFT – FOR OFFICIAL USE ONLY

IN-CONFIDENCE

Deleted - Not Relevant to Request

Universal basic income

A universal basic income (UBI) is a type of tax and transfer policy that provides a guaranteed

minimum income to all households, irrespective of income, work-status or other criteria.

It is an old idea, but has received renewed attention. Its key advantage is its simplicity. Economic

changes mean that workers may have greater job insecurity, technological disruption and different

types of working arrangements (eg, the ‘gig economy’) than in the past. A UBI may support greater

income security in this type of economic conditions.

The disadvantages of a UBI is that it will likely increase poverty rates, in the absence of large

increases in tax revenues. Spreading existing working age benefits to the entire working age

population will materially reduce the level of payment to those who already receive benefits. At

current spending levels, a UBI would be substantially below the poverty line in most OECD

economies (OECD, 2017). This is particularly the case for New Zealand, given New Zealand’s existing

transfer payments are highly targeted. To illustrate, New Zealand spends around 10% of GDP on

working age benefits, which is around $8,500 a year per working age person. A sole parent jobseeker

currently receives around $17,000 a year.

While concerns around impact on poverty rates could be addressed with a higher payment rate, this

could not be budget neutral. It would require a significant increase in tax revenues, and therefore

average tax rates would rise. This could materially weaken work incentives and reduce employment

levels.

There are a number of pilot studies planned for UBIs in certain municipalities, including in Canada,

the Netherlands and Finland. It is too early to evaluate the effects of these pilot studies, but they

should be monitored for their results.

Deleted - Not Relevant to Request

Deleted - Not Relevant to Request

48

Pages 49-57 Deleted - Not Relevant to Request

20180164 TOIA Binder New

Doc 1

Page 10 of 62

DRAFT – FOR OFFICIAL USE ONLY

IN-CONFIDENCE

Deleted - Not Relevant to Request

The nature of work is changing, which poses challenges for the tax and transfer system. There is

greater diversity of working arrangements than in the past and there may be greater use of the

social safety net in the future to support workers as they transition between occupations. Some

argue that a universal basic income (UBI) should be introduced to reduce job insecurity in this

environment. However, there is not a strong case for a UBI in New Zealand as it would reduce the

effectiveness of the welfare system in reducing poverty, although overseas pilot studies should be

monitored for their outcomes.

Deleted - Not Relevant to Request

Deleted - Not Relevant to Request

58

20180164 TOIA Binder New

Doc 1

Page 11 of 62

DRAFT – FOR OFFICIAL USE ONLY

IN-CONFIDENCE

References

Kleven, Henrik Jacobsen. 2014. "How Can Scandinavians Tax So Much?"

Journal of Economic

Perspectives, 28(4): 77-98.

OECD (2011),

Taxation and Employment, OECD Publishing, Paris.

http://dx.doi.org/10.1787/9789264120808-en

John Creedy and Penny Mok (2015) “Labour Supply in New Zealand and the 2010 Tax and Transfer

Changes”. Treasury Working Paper 15/13.

John Creedy & Penny Mok, 2017. "The Marginal Welfare Cost of Personal Income Taxation in New

Zealand," Treasury Working Paper Series 17/01, New Zealand Treasury.

Penny Mok and Joseph Mercante (2014) “Working for Families changes: The effect on labour supply

in New Zealand” New Zealand Treasury Working Paper 14/18.

John Creedy, 2010. "Tax-and-Transfer Tensions: Designing Direct Tax Structures," Australian

Economic Review, The University of Melbourne, Melbourne Institute of Applied Economic and Social

Research, vol. 43(2), pages 103-113.

Carey, D. (2017), "Adapting to the changing labour market in New Zealand", OECD Economics

Department Working Papers, No. 1420, OECD Publishing, Paris.

http://dx.doi.org/10.1787/e6ced642-en

Veronica Jacobsen, Nicholas Mays, Ron Crawford, Barbara Annesley, Paul Christoffel, Grant Johnston

and Sid Durbin (2002) "Investing in Well-being: An Analytical Framework" New Zealand Treasury

Working Paper 02/23 December, 2002.

IMF,

Fiscal Monitor, October 2017

OECD 2012, “Income inequality and growth: The role of taxes and transfers”, OECD Economics

Department Policy Notes, No. 9. January 2012.

OECD (2016), “Enhancing Child Well-Being to Promote Inclusive Growth”

http://www.oecd.org/officialdocuments/publicdisplaydocumentpdf/?cote=DELSA/ELSA(2016)7/REV

1&doclanguage=en

Layard, R., A. Clark, F. Cornaglia, N. Powdthavee and J. Vernoit (2014), “What predicts a successful

life? A life-course model of well-being”,

The Economic Journal, Vol. 124, Issue 580, pp. F720-F738.

Emmanuel Saez (2002) “Optimal income transfer programs: intensive versus extensive labor supply

responses”

The Quarterly Journal of Economics, August 2002.

Robert W. R. Price & Thai-Thanh Dang & Jarmila Botev, 2015. "Adjusting fiscal balances for the

business cycle: New tax and expenditure elasticity estimates for OECD countries," OECD Economics

Department Working Papers 1275, OECD Publishing.

59

20180164 TOIA Binder New

Doc 1

Page 12 of 62

DRAFT – FOR OFFICIAL USE ONLY

IN-CONFIDENCE

Blanchard, Olivier, Dell'ariccia, Giovanni and Mauro, Paolo, (2010), Rethinking Macroeconomic

Policy

, Journal of Money, Credit and Banking, 42, issue s1, p. 199-215.

Jonathan Boston & Simon Chapple (2014)

Child poverty in New Zealand.

Jason Raven (2015) "Financial Incentives to Work"

Policy Quarterly – Volume 11, Issue 4 – November

2015

60

Pages 61-72 Deleted - Not Relevant to Request

20180164 TOIA Binder New

Doc 1

Page 13 of 62

IN-CONFIDENCE

Summary of modelling capabilities in terms of potential

options

Deleted - Not Relevant to Request

Universal

Basic Income

(UBI)

Potential

HES

data sources

Taxwell

Such a

significant

change to the

system means

that any

results based

on a static

analysis may

be too

removed from

the actual

impacts.

Taxwell B

No

27

http://www.stats.govt.nz/browse_for_stats/people_and_communities/Children/ChildcareSurv

ey_HOTP2009revised/Commentary.aspx

Treasury:3788507v1

IN-CONFIDENCE

73

20180164 TOIA Binder New

Doc 1

Page 14 of 62

IN-CONFIDENCE

Deleted - Not Relevant to Request

MSD – MSIM Only for MSD

clients

IR

No –

insufficient

data as does

not include

people with

no income

Treasury:3788507v1

IN-CONFIDENCE

74

20180164 TOIA Binder New

Doc 2

Page 15 of 62

Draft 1

NEGATIVE INCOME TAX SYSTEMS

Ewen McCann1

6 September 2000

Prepared for a Working Group on Financial Incentives to Work

1 I have had useful conversations with Martin Neylan while preparing this paper.

C:\NRPortbl\iManage\SHENK\92754_1.doc

20180164 TOIA Binder New

Doc 2

Page 16 of 62

Summary

1.

The negative income tax system of delivering welfare benefits consists

of,

• A lump sum transfer payment clear of tax.

• A tax on market income.

2.

Al welfare delivery systems are compromises between the conflicting

objectives of,

• Decent living standards.

• Low levels of break-even income.

• Low rates of the abatement-tax

3.

A negative income tax with wide coverage would,

• Be administratively cheap and transparent to beneficiaries.

• Preserve horizontal equity.

• Offer similar work incentives for al .

4.

Effective marginal tax rates are high under the existing welfare system.

A negative income tax system requiring high tax rates is therefore not

necessarily disadvantaged in comparison with the present welfare payment

system. One issue is what tax schedule would be required to finance a

negative income tax system.

5.

Negative income tax methods of welfare delivery could be

particularised to specific groups.

6.

The issue with all welfare delivery systems in promoting incentives to

work is the low rates of response of the labour supply to after tax incentives.

This has been demonstrated for welfare payments generally and also in

experiments with negative income tax systems.

7.

New Zealand unkowingly has an extensive system of negative income

tax welfare payments.

8.

One part of this is the family tax credit. It is a cash grant of $15080 p.a.

after which each dollar of income is taxed at 100% until the lump sum is paid

back. Education and health services are lump sums paid in kind. Families

receiving them pay income tax on market income. The services thereby meet

the two requirements for a negative income tax. Present welfare payments

can be shown to be equivalent to a complicated system of selective or

earmarked negative income taxes.

9.

The negative income tax framework is a useful way of conceptualising

the current New Zealand welfare payment system and thinking about reforms

to it. There is a diagrammatic representation of the scheme in the Appendix.

C:\NRPortbl\iManage\SHENK\92754_1.doc

20180164 TOIA Binder New

Doc 2

Page 17 of 62

1. Introduction

10.

A comprehensive negative income tax fully integrates the tax and

welfare payment systems and is the only way of doing so. It consolidates the

two systems.

11.

A negative income tax system requires just two things: a lump sum

transfer from the Government to a person and a tax on market income.

12.

The term is a mite confusing. Positive income tax is paid by people to

the Government. Negative income tax is paid by the Government to the

people. The receipt of money from the Government is the negative tax as far

as the household is concerned because tax money usually flows in the other

direction. Think of it as a poll tax in reverse. Instead of paying it a person

receives it from the Government.

13.

The negative income tax provides a single type of benefit that is a lump

sum payment made at, say, the beginning of the period though in practice

probably at intervals through it. That is the end of the benefit side of the

tax/welfare system. Thereafter, all is tax. Tax is applied only on what is

subsequently earned. There may or may not be a single tax schedule for all.

14.

The system can be seamless between transfers to and from the

Government. Threshold problems need not emerge. There is no point in

falsifying welfare claims if there is universal entitlement. Tax fraud remains

profitable.

15.

A negative income tax need not be as comprehensive as this and it can

be piecemeal, earmarked or in kind as we will see.

16.

A negative income tax system would not impose marginal tax rates

above 100% the way the existing tax/abatement regime occasionally does.

17.

Beneficiaries apparently see at present just the total of the welfare

payments that they receive without distinguishing the component benefits.

There need be no separate benefits in the lump sum of the negative income

tax.

18.

The conflicting requirements of a decent living standard, low breakeven

income (the level of earned income where benefits are clawed back in tax or

benefit abatement), low tax or abatement rates, and low budgetary cost apply

to al welfare payment systems.

19.

There is a diagrammatic representation of the scheme in the Appendix

where design and important issues around incentives to work are discussed.

2. Features of the System

C:\NRPortbl\iManage\SHENK\92754_1.doc

20180164 TOIA Binder New

Doc 2

Page 18 of 62

20.

The advantages of the negative income tax method of poor relief are

that,

• It is administratively cheap and transparent to beneficiaries.

• Horizontal equity is preserved.

• Work incentives are the same for al .

21.

The negative income tax system is distinguished from earmarked

welfare payments which have effects that are the opposite of these.

Earmarked welfare payments provide sub-groups with individualised welfare

benefits. High effective tax rates of the abatement regimes can be a

consequence of beneficiaries receiving more than one earmarked benefit, a

core benefit and a supplementary benefit. Labour market inefficiencies result.

22.

If the negative income tax reached a significant portion of or even all

the population, it would be expensive and marginal tax rates have therefore to

be high for at least some taxpayers in order to finance it or recoup it. There

would then be significant work disincentives with it, as there are with the

extant earmarked benefits.

3. Marginal Tax Rates

23.

The relatively high marginal rates of income tax that would accompany

a negative income tax system with broad coverage is

not a particularly

important objection to it. This is because the system of earmarked benefits

that we have at present is widespread and is accompanied by high effective

tax rates.

24.

An extensive negative income tax system would probably involve high

marginal tax rates because of the Government’s budget imperative. In its pure

form a negative income tax system would have the same tax schedule

applying to everyone’s market income. The difference between this and the

high effective marginal tax rate system is that the present skyscraper skyline

diagram of effective marginal tax rates need not accompany the negative

income tax system. Labour market distortions should be less under the

negative income tax system than under the present system of supporting the

poor.

25.

The proper question is, given the broad coverage and high EMTRs of

the present benefit system, what income tax schedule would be required to

finance a parallel negative income tax system?

4. Earmarked Negative Income Taxes 26.

Half way houses seem possible, like applying the negative income tax

system to earmarked groups. The trick to cost containment would be to sort

groups by non-economic criteria that are not readily under the control of

individuals, or that are costly for them to meet.

C:\NRPortbl\iManage\SHENK\92754_1.doc

20180164 TOIA Binder New

Doc 2

Page 19 of 62

27.

The privileged status of one group causes others to try to join it. Their

success in joining would raise the budgetary cost of a programme and the

new members may not be work responsive. Any social assistance scheme

contains an incentive to move from work to welfare in some degree. This may

make their effects on the distribution of income ambiguous. Take the case

where sizeable numbers went from work to welfare, accepting an income

reduction. This increases the income inequality that the programmes are

designed to reduce.

28.

Demographic characteristics are the obvious selection criteria for a

restricted system of negative income tax. Age, gender, congenital

abnormalities and dependents are either impossible or costly to modify.

Excluded groups cannot readily join in. Earmarked groups could be taken off

their present benefits and become a part of the restricted negative income tax

system.

29.

For example, all or some DPB beneficiaries could be given a suitable

weekly lump sum, usually expressed as a fraction of the average wage. Then,

whatever they earned above this

could be taxed at the income tax rates

applying to non-beneficiaries. The high EMTRs inherent in the current benefit

abatement and income tax regimes are removed for them as a result. Work

incentives improve for this earmarked group. This is an earmarked negative

income tax system.

30.

In a pure form of negative income tax the same lump sum is paid to all

though this need not be the case. Lump sums could rise with family size or

other circumstances. Administration costs would rise with them.

31.

It is not necessary for its operation that the beneficiaries of the negative

income tax face the same income tax schedule as other taxpayers. There are,

however, clear administrative and labour market efficiency advantages a

single tax schedule.

5. Responsiveness

32.

Groups with the higher labour supply elasticities are the ones that are

the better candidates for an earmarked negative income tax rate, as long as

their memberships can be circumscribed for budgetary reasons, perhaps by

demographic criteria.

33.

The rates of response of work effort to changes in after tax wages are

typically low. Deadweight losses are probably low because of it. From this

point of view beneficiaries’ present high effective marginal tax rates involve

little social cost in the economic sense of the term because their labour

supplies are probably inelastic.

34.

It is hard to see why the high EMTRs receive the attention in policy

discussion that they do when their economic welfare costs are likely to be

small.

C:\NRPortbl\iManage\SHENK\92754_1.doc

20180164 TOIA Binder New

Doc 2

Page 20 of 62

35.

Just as the present welfare system appears to do little to get people

working, not too much should be expected of a negative income tax either,

and for the same reasons

viz, the supposedly low labour supply elasticities.

36.

This expectation has been confirmed by experiments with the negative

income tax. There were tests of this welfare delivery method in the 1970’s in

New Jersy, Gary Indianna, Seattle, Denver and in Manitoba. The Denver

experiment lasted eight years.

37.

The designers of the negative income tax have problems with al of the

experiments because,

• The lump sums were set at too high a level.

• It did not replace other benefits but was in addition to them.

It is for these reasons that one of them (Milton Friedman) publicly opposed

President Nixon’s variation of the scheme2.

38.

There have been a number of studies of the work incentives in the Aid

to Families with Dependent Children programme in the USA. This is not a

negative income tax but nevertheless,

Changing benefits formulas to increase work incentives are likely to generate

minimal increases in the labour supply3

6. New Zealand Case

39.

A negative income tax requires just two things: an untaxed lump sum

and a tax on market income.

40.

Without realising it, New Zealand presently operates an extensive

though complicated negative income tax. There are three parts to the New

Zealand negative income tax (

i.e. welfare) system. One is through Family Tax

Credit scheme and some similar practices, another is through benefits in kind

and the other is the current general welfare payment system. We treat them in

turn.

41.

The Family Tax Credit is a negative income tax. It applies to a

restricted group of people who receive a cash grant of $15080 p.a. Each

dollar of market income reduces the $15080 by one dollar4. The two

requirements of a negative income tax are therefore met by this welfare

benefit. These are the lump sum grant and the taxation of market income. In

this case the lump sum grant from the Government is not of a gross amount,

though it can be converted to one, and the tax-abatement rate is 100%. This

along with other tax credits is the first of New Zealand’s negative income

taxes.

2 Parker, Hermione (1989).

Instead of the Dole. Routledge, London. p 144.

3 Hoynes, H.W.(1996)

Work Welfare and Family Structure: What have We Learned? National

Bureau of Economic Research, Cambridge MA. Working Paper 5644 p 34.

4 This dollar reduction is composed first of income tax and then of the abatement tax.

C:\NRPortbl\iManage\SHENK\92754_1.doc

20180164 TOIA Binder New

Doc 2

Page 21 of 62

42.

The second negative income tax system is of payments in kind. Health

and education goods are transfer payments in kind that the Government

provides to families. These do not abate, they are lump sum transfers in kind

and are unrelated to income, just like a full scale negative income tax would

be. Education and health recipients pay tax on their market income at the

standard income tax schedule. They are on a negative income tax system for

health and education goods.

43.

Negative income tax types of transfers in kind could be extended. Food

stamps and rent subsidies are obvious extensions. Payments in kind are not

optimal for the recipients because they will be better off, by their own lights,

upon the receipt of a benefit to the same value in cash.

44.

We do not hear these optimality arguments mounted to replace

negative income taxes in kind by cash transfers. This is because taxpayers

want to know what the transfers are being spent on.

45.

A voucher system of welfare payments preserves the specified good

characteristic of the transfer and would also be a negative income tax in kind

that is supposedly more economically efficient than state produced goods.

The accommodation supplement is similar to a voucher inasmuch as the

recipient can spend it on any supplier of a specified good.

46.

The current cash welfare payments are the third component of New

Zealand’s negative income tax system. The current system of the payment of

cash benefits is a complicated negative income tax system though it is not

seen as such because of the way that the abatement regimes are interpreted.

47.

We see abatement as reducing the amount of the benefit in the hand

as income increases. And we see income tax as reducing income in the hand

as income increases. These viewpoints probably arise because of the

separate functions of the Department of Work and Income and the Inland

Revenue Department. We will look at them a little differently.

48.

It will be helpful to imagine that the “first” division of the Department of

Work and Income decides on an applicant’s gross benefit entitlement and that

the “second” division applies the abatement regime.

49.

Let us focus on the second division’s activity. A beneficiary would see

no economic distinction between a reduction in a welfare cheque determined

by the second division and the same reduction in take-home market income

determined by the Inland Revenue Department. The person’s disposable

income is reduced by the same amount and has the same smaller total in

each case. Income tax and abatement have the same effect on the

beneficiary, as long as the penalties are equal. The reason for this is that is

that abatement and income tax are both determined by the amount of market

income.

C:\NRPortbl\iManage\SHENK\92754_1.doc

20180164 TOIA Binder New

Doc 2

Page 22 of 62

50.

An abatement at 70 cents in the dollar is entirely equivalent to an

income tax at the same rate as far as the income-taxpaying-beneficiary is

concerned.

51.

To a beneficiary, a particular abated benefit plus an after tax market

income is therefore equivalent to a lump sum benefit plus a gross market

income that is taxed at a rate suitably greater than is specified by the statutory

income tax schedule. A welfare payment under the current system has been

shown to meet the two requirements of a negative income tax, the lump sum

transfer and a tax on market income.

52.

This proves our point. The incentive effects of the benefit-abatement-

income–tax regimes are the same as a specific and highly structured negative

income tax system as far as beneficiaries are concerned.

53.

We can, and we perhaps should, view the present tax and benefit

systems as complicated negative income tax regimes. This would provide a

framework for welfare payment reform, if reform is necessary.

C:\NRPortbl\iManage\SHENK\92754_1.doc

20180164 TOIA Binder New

Doc 2

Page 23 of 62

APPENDIX

54.

The diagram for a person under a negative income tax is,

Negative Income Tax

Disposable

Income C

B Disposable Income

D A

$10,000

45O

Before Tax Market Income

55.

The solid line shows the person’s disposable income. The lump sum

transfer from the Government is $10,000 at point D. As the person earns

income in the market place tax is paid just on that income. The slope of DB

reflects that first rate of income tax. At point A the tax paid equals the lump

sum transfer payment. At point B the tax rate reduces and at C it increases.

The negative income tax is $10,000 because that is what the Government

gives the person.

56.

The characteristics of the disposable income line reflects the incentives

to work that are designed into the negative income tax system. The flatter is a

segment the higher is the tax rate. Different designs shift the disposable

income line and alter the slopes of the segments,

i.e. the tax rates.

57.

The slope of DB reflects a relatively high first tax rate to clawback the

transfer. Point A is the clawback point, where tax paid equals the transfer

received, and is always at a market income of the lump sum divided by the

first tax rate, $10,000/(tax rate) in this case. A lower first income tax rate

moves point A north-east and increases the fiscal cost of the scheme. Points

A and B could coincide.

58.

The type of tax schedule reflected in the diagram carries the problem

that the taxpayer-beneficiary can be trapped on segment DB. Schedules that

bend the other way can also leave them stuck - at a kink such as C.

59.

These sorts of problems apply to most tax schedules and they are not

peculiar to the negative income tax system. Their importance is that they

show that transfers, wages and taxes are only half of the incentive story.

60.

The full picture involves the individual’s personal evaluations.

The

incentive to work is not the after tax and transfer wage. The incentive is

the difference between this amount and the individual’s personal valuation of

an hour’s work times a constant. When this difference is positive a person will

increase the amount of work that they do.

C:\NRPortbl\iManage\SHENK\92754_1.doc

20180164 TOIA Binder New

Doc 2

Page 24 of 62

C:\NRPortbl\iManage\SHENK\92754_1.doc

20180164 TOIA Binder New

Doc 3

Page 25 of 62

IN-CONFIDENCE

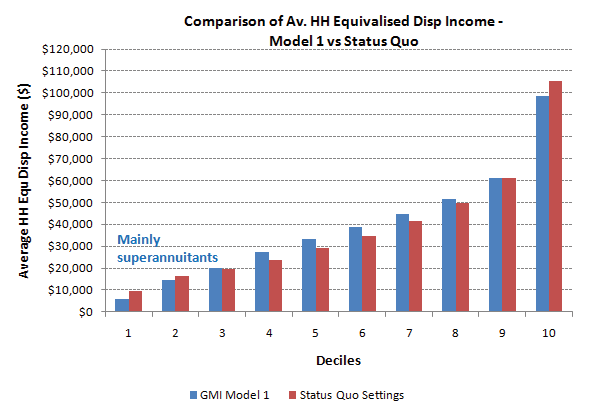

Modelling a Cost-Neutral Guaranteed Minimum Income (GMI) Scheme – Welfare Working Group 2010

STATUS QUO – Summary of fiscal costs and measures under

Model 1 – GMI with NZ Superannuation

Model 1 Contd.

settings for the 2011/12 tax year

Model specifications

Winners and Losers – Model 1 compared to status quo settings

The status quo model incorporates the personal tax structure as

Benefit system abolished

from 1 October 2010:

Status quo settings for NZ Superannuation retained

Families

Working for Families retained – payments for dependants aged 16

(total across

# Families

% Families

population)

Income

Rate

– 18 set to zero

$0 – 14,000

10.5%

Winners

1,485,353

65.86%

GMI scheme - payment of $300 per week for each person

$14,001 - $48,000

17.5%

Losers

769,433

34.12%

between the ages of 16 and 64 inclusive - people aged over 64

$48,001 - $70,000

30.0%

No Change

-

-

who do not receive NZ Superannuation are eligible for GMI

Over $70,000

33.0%

Total

All other settings and assumptions as per BEFU 2010

(approx.)

2,255,260

Mainly super

GST set at 15%

annuitants and high

Rates for core benefits, Working for Families and NZ

Fiscal Cost of GMI

Households

income earners

(total across

# HH

% HH

Superannuation and income projections are based on

population)

assumptions and settings from the

Budget Economic and Fiscal

Winners

1,004,174

60.51%

Update (BEFU), 2010

Weekly payment for GMI

$300

Total population

4,344,921

Losers

655,357

39.49%

# People eligible for GMI

2,839,284

No Change

-

-

Total

Total

1,659,531

($ millions)

Fiscal cost of GMI ($ millions)

$44,463

Financial Assistance

Equality and Poverty Measures

Invalid Benefit

$ 1,457.3

Estimating a flat tax for GMI

Sickness Benefit

$ 884.3

Domestic Purposes Benefit

$ 1,614.3

Total

Equality

Widows Benefit

$ 264.9

($ millions)

Measures

Unemployment Benefit

$ 1,082.1

Financial Assistance

Gini Coefficient

0.349

NZ Super and Veterans Pension

$ 8,246.3

General Minimum Income (GMI)

$ 44,463

80 / 20 Ratio

3.491

Under Age Non-Qualified Partner

$ 184.1

Working for Families

$ 2,813

Supplementary Assistance

$ 748.0

NZ Super and Veterans Pension

$ 8,262

Poverty Reference Line

Median HH disposable income

Other Benefits

$ 518.4

Social Transfers Total

$ 55,537

(equivalised)

Student Allowance

$ 319.9

Relative Reference

$36,009

Working for Families Tax Credit Total

$ 2,848.2

Taxation

Social Transfers Total

$ 17,983.7

Taxable income

$ 122,380

Poverty line: % of relative reference line

% HH below poverty line

Tax NZ Super

$ 969

50% relative

22.2%

Taxation

Total Tax payable

$ 23,801

60% relative

27.4%

Tax on Benefits

$ 584.5

70% relative

32.3%

Tax on Super

$ 967.2

Net Benefit Cost (Tax Payable – Total

Other income tax

$ 22,939.0

Social Welfare)

-$ 31,736

Individual Rebates

$ 18.9

The redistributive effect of GMI with NZ Superannuation

Tax Payable

$ 24,471.8

For cost-neutrality (

whereby social assistance payments are fully

funded by personal tax revenue), tax payable needs to be $

Better off compared to SQ - households in deciles 3 to 8

Equality

55,537 million

Worse off - mainly superannuitants who are in deciles 1 and 2 and high

Measures

Revenue from personal taxes under 1 October 2010 settings is

income earners (mainly decile10) whose higher tax contribution exceeds

Gini Coefficient

0.355

estimated at $ 23,801 million

the GMI payment

80 / 20 Ratio

3.010

Additional amount to raise from personal tax to fund GMI $ 31,736

million

Poverty Reference Line

Median HH disposable income

(equivalised)

The tax rate that raises this additional amount is ($55,537 /

Relative Reference

$31,671

$122,380) ≈

45.4% (this is the flat tax rate for cost-neutrality)

Poverty line: % of relative reference line

% households below poverty line

Taxwell simulation with a flat tax of 45.4%

50% relative

13.4%

60% relative

23.7%

Total

70% relative

32.1%

($ millions)

Financial Assistance

Notes:

General inimum Income (GMI)

$ 44,463

Increase

This analysis is based on Statistics New Zealand’s ‘

Household

Working for Families

$ 2,946

mainly due to

MFTC

and Economic Survey’ (HES) 2008/09 – results are subject to

NZ Super and Veterans Pension

$ 4,596

sampling error

Social Transfers Total

$ 52,005

Fiscal cost estimates detailed here are generated using

Taxation

Broadly cost-

Treasury’s static micro-simulation model ‘Taxwel ’ – these may

Taxable income

$ 118,716

neutral

differ from official Inland Revenue Department (IRD) and Ministry of

Tax NZ Super

$ 2,081

Social Development (MSD) forecasts

Total Tax payable

$ 53,843

IN-CONFIDENCE

1

20180164 TOIA Binder New

Doc 3

Page 26 of 62

IN-CONFIDENCE

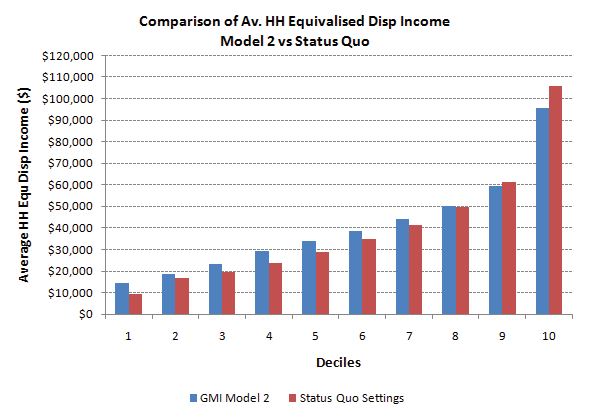

Modelling a Cost-Neutral Guaranteed Minimum Income (GMI) Scheme – Welfare Working Group 2010

Model 2 – GMI without NZ Superannuation

Model 2 Contd.

Model 2A – Model 2 without Working for Families

Model specifications

Winners and Losers - Model 2 compared to status quo settings

Model specifications

Benefit system abolished

Families

# Families

% Families

As for model 2 but with Working for Families abolished and

NZ Superannuation abolished

(total across

replaced with a payment of $86 per child per week (assuming

population)

Working for Families retained – payments for dependants aged 16

Winners

1, 466,69

65.03%

child is aged 0 to 15)

– 18 set to zero

Losers

788,094

34.94%

GMI scheme - payment of $300 per week for each person aged

No Change

-

-

Fiscal Cost

16 years and older.

Total

2,255,260

All other settings and assumptions as per BEFU 2010

(approx.)

Weekly payment for GMI

$300

Fiscal Cost of GMI

Households

# HH

% HH

Total population

4,344,921

(total across

# People eligible for GMI

3,361,325

population)

# Children eligible for weekly

983,596

Winners

1,039,695

62.65%

Weekly payment for GMI

$300

payment

Losers

619,836

37.35%

Total population

4,344,921

No Change

-

-

# People eligible for GMI

3,361,325

Total

1,659,531

Fiscal cost of GMI ($ millions)

$52,638

Total

($ millions)

Financial Assistance

Total

Equality and Poverty Measures

General Minimum Income (GMI)

$ 52,638

($ millions)

Weekly child payment

$ 4,416

Financial Assistance

Equality

Social Transfers Total

$ 57,054

General Minimum Income (GMI)

$ 52,638

Measures

Working for Families

$ 2,819

Gini Coefficient

0.294

Taxation

Social Transfers Total

$ 55,458

80 / 20 Ratio

2.622

Taxable income

$ 114,127

Total Tax payable

$ 22,581

Taxation

Poverty Reference Line

Median HH disposable income

Taxable income

$ 114,127

(equivalised)

Net Benefit Cost (Tax Payable – Total

-$ 34,473

Total Tax payable

$ 22,581

Relative Reference

$36,381

Social Welfare)

Net Benefit Cost (Tax Payable – Total

-$ 32,876

Poverty line: % of relative reference line

% HH below poverty line

Tax rate that funds this scheme

50%

Social Welfare)

50% relative

14.1%

60% relative

22.7%

Taxwell simulation with a flat tax of 50%

For cost-neutrality (

whereby social assistance payments are fully

70% relative

29.0%

funded by personal tax revenue), tax payable needs to be

Total

$55,458 mil ion

The redistributive effect of GMI without NZ Superannuation

($ million )

Revenue from personal taxes under 1 October 2010 tax settings

Social Transfers Total

$ 57,054

is estimated at $22,581 mil ion

Better off compared to SQ - mainly households in deciles 1 to 7

Additional amount to raise from personal taxes to fund GMI

Worse off – households in deciles 9 and 10

Taxation

Taxable income

$ 114,127

$32,876 million

Total Tax payable

$ 57,042

The tax rate that raises this additional amount is ($55,458 /

$114,127) ≈

48.6% (this is the flat tax rate for cost-neutrality)

Equality and Poverty Measures

Taxwell simulation with a flat tax of 48.6%

Equality

Measures

Total

Gini Coefficient

0.292

($ million )

80 / 20 Ratio

2.646

Financial Assistance

General Minimum Income (GMI)

$ 52,638

Poverty Reference Line

Median HH disposable income

Working for Families

$ 2,993

(equivalised)

Social Transfers Total

$ 55,631

Relative Reference

$36,644

Taxation

Broadly cost-

Taxable income

$ 114,127

Other poverty measures similar to those for model 2

neutral

Total Tax payable

$ 55,444

Contacts for further information:

A flat tax of ≈

49% (that broadly allows cost-neutrality) converts

Gerald Minnee s9(2)(k)

Omar A. Aziz s9(2)(k)

the tax less transfers deficit to a surplus

IN-CONFIDENCE

2

Manager - Economic, Research

Analyst - Economic Research and

and Analysis Unit

Analysis Unit

20180164 TOIA Binder New

Doc 4

Page 27 of 62

IN-CONFIDENCE

The Treasury’s position on income adequacy and

poverty: previous advice and potential directions

Barbara Annesley

7 April 2017

1

20180164 TOIA Binder New

Doc 4

Page 28 of 62

IN-CONFIDENCE

Executive Summary

This report reviews previous Treasury advice on policy settings that directly influence income

adequacy: taxes and transfers, wages and other work incentives. It considers this advice in relation

to data about the adequacy of current benefits and wages, evidence on the effectiveness of different

levers for addressing poverty, and wider social and labour market changes.

Deleted - Not Relevant to Request

2

20180164 TOIA Binder New

Doc 4

Page 29 of 62

IN-CONFIDENCE

Current and emerging labour market trends in New Zealand and overseas point to risks associated

with low work intensity and precarious employment. These risks may contribute to reduced income

adequacy, security, mobility and smoothing over the life-course. In response to such trends there

have been calls for a shift from highly targeted to universal forms of income support, and from re-

distributive mechanisms (such as tax credits) to approaches that ensure earned income is sufficient

to meet basic needs (such as ‘living wage’ proposals).

While previous Treasury advice is high quality, analytically sound and reflective of the agencies wider

economic and fiscal interests, there is scope to strengthen it further. Suggested areas of focus for

future work include: clarifying the application of the Living Standards Framework and investment

approach to some income adequacy policy settings; better articulation of the respective roles and

application of targeted and universal approaches; additional analysis and modelling of the universal

basic income or similar concepts; the provision of advice on opportunities to improve the integrity

and coherence of the tax and transfer system; and a deep-dive analysis of trends and determinants

of wage levels at the lower end of the income distribution.

3

20180164 TOIA Binder New

Doc 4

Page 30 of 62

IN-CONFIDENCE

Introduction

1. This report reviews previous Treasury advice related to income adequacy, considers relevant

New Zealand and overseas trends and developments, and identifies potential areas of focus and

opportunities to strengthen future Treasury advice.

2. Deleted - Not Relevant to Request

3.

4. This report is accompanied by a slide pack that provides visual and summary information on the

key points.

4

Pages 5-17 Deleted - Not Relevant to Request

20180164 TOIA Binder New

Doc 4

Page 31 of 62

IN-CONFIDENCE

Deleted - Not Relevant to Request

•

Treasury advice on directions for change in existing policy

se

(slide 17)

44. Deleted - Not Relevant to Request

45.

46. A consistent message in Treasury advice is that universal benefits, and changes to tax settings

and wage levels (e.g. minimum wage increases, a ‘living wage’) are ineffective mechanisms for

addressing poverty and material hardship. Advice notes that they are costly and poorly targeted,

with the potential to create significant labour market and economic distortions.

47. Deleted - Not Relevant to Request

18

Pages 19-25 Deleted - Not Relevant to Request

20180164 TOIA Binder New

Doc 4

Page 32 of 62

IN-CONFIDENCE

Deleted - Not Relevant to Request

78.

79.

Emerging challenges to targeted approaches to income support

and social investment

(slide 24)

80. Central to Treasury’s advice on income adequacy and the social investment approach is an

emphasis on closely targeting assistance to those who stand to benefit the most, including using

administrative data to identify risk propensity.

12 The OECD defines activation strategies as aiming to

“bring more people into the effective labour force, to counteract the

potential effects of unemployment and related benefits on work incentives by enforcing their conditionality on active job

search and participation in measures to improve employability, and to manage employment services and other measures so

that they effectively promote and assist the return to work” (Martin, 2014, Pg 3)

26

20180164 TOIA Binder New

Doc 4

Page 33 of 62

IN-CONFIDENCE

81. Standing in stark contrast to this is the growing political momentum and popular support for

more universal and broad-based approaches to poverty reduction, such as through the provision

of universal child benefits or a universal basic income (UBI) to replace existing means-tested and

work-tested income support.

Universal basic income (slide 25)

82. The idea of a Universal Basic Income has a long history, and has recently re-emerged in response

to a range of social and economic changes. These include increased inequality of income and

wealth, the changing nature of work (particularly the rise of precarious and part-time

employment), lack of recognition and value attached to unpaid family responsibilities and

voluntary work, and concerns about some of the downsides of narrowly targeted income support

(e.g. their stigmatising nature, poverty traps and work disincentives, and administrative

complexity).

83. The general idea of a UBI is to provide everyone in the population (or a subsection thereof) with

a minimum level of income, generally with no work obligations or means-testing. It’s important

to note, however that there is not one version of UBI – specific versions can include abatements

and targeted additional support.

84. Proponents of a UBI suggest that it is likely to have multiple and varied benefits, including

reduced bureaucracy as a result of its administrative simplicity, reduced family stress, improved

incentives to develop skills and be entrepreneurial, better skills matching and labour market

efficiency (as people will be able to be more selective about the employment they undertake)

and increased household savings and spending, contributing to economic growth.

85. Many of these suggested benefits are purely speculative, and the lack of a robust evidence base

makes it difficult to ascertain the extent to which they would be realised. Many commentators

and policymakers have drawn attention to the significant costs associated with implementing a

UBI, along with other issues such as negative effects on work incentives, reduced returns to skills,

potential for employers to reduce wages and exploit vulnerable workers; regressive

redistribution of government transfers to middle income earners.

86. For these reasons, even many of those who support the UBI concept in principle advocate a

cautious approach to its adoption, such as small-scale trials to its effectiveness in delivering

expected outcomes. Current and proposed overseas examples of such trials include:

•

Finland: 2000 randomly selected unemployed people will receive a basic income instead of a

benefit for 2 years

•

Netherlands: 250 beneficiaries in Utrecht will receive a flat sum guaranteed income for 2

years

•

Italy: 200 families in Livorno have received a basic monthly income, with plans to expand this

further

•

Ontario, Canada: the provincial government is currently consulting on details of a potential

pilot project to test UBI in three sites

•

Glasgow, Scotland: the city’s council is partnering with the Royal Society of Arts to research

the design of a pilot UBI project

27

20180164 TOIA Binder New

Doc 4

Page 34 of 62

IN-CONFIDENCE

•

USA: Professor Greg Duncan (an economist at the University of California) and colleagues

from a number of other major American universities have completed a pilot study looking at

the impact of UBI receipt on children’s brain development, and are planning a larger study

involving 1000 low-income mothers and their children.

87. Closer to home, several political parties have indicated support, to a greater or lesser extent, for

a UBI. The Green Party has said that they support debate and experimentation; the Labour Party

has signalled that it would consider a limited trial of a UBI, while its ‘Future of Work’ discussion

document suggests combining a lower UBI with targeted supplemental support. The newly

established ‘The Opportunities Party’, has released a detailed proposal outlining a progressive

approach to introducing an Unconditional Basic Income, starting with $200 per week to all

families with children aged under 3 (replacing paid parental leave) and for all people aged over

65 (replacing New Zealand Superannuation, but accompanied by a means-tested top-up). This

would be augmented by an additional non-work tested payment of $72 per week to all low

income families with dependent children (replacing the current In-Work Tax Credit) and free full-

time childcare for the under 3 year olds from families with low income parents engaged in any

paid work.

88. While Treasury hasn’t undertaken a general analysis of UBI, in 2010 it undertook ‘preliminary’

modelling for the Welfare Working Group (WWG) on a specific UBI proposal involving a universal

and unconditional payment of $300 per week to all individuals aged 16 and over, with an extra

payment to families with children. This modelling highlighted a range of issues and negative

consequences, not least of which is the considerable fiscal cost. The following table summarises

the Treasury’s conclusions about the GMI scheme, and this appears to stands as Treasury’s

advice on UBIs to date

(slide 26).

Table 4: UBI Benefits and Costs identified by the Treasury, 2010

Benefits

Costs

• More equal distribution of income

• Poverty is either increased across all relative levels as

• Removes disincentive for beneficiaries

Superannuitants have their payment decreased by

to undertake part-time work

44% on average*, or is increased when measured at

• Poverty is reduced but only at the 60

the 50 percent relative level*.

and 70 percent relative levels*

• Horizontal equity problems due to differential

• May improve labour market outcomes in

treatment of one and two parent families

some areas: more employee flexibility;

• Many current beneficiaries (e.g. sole parents, the

encourages unpaid work; additional

disabled and carers) will be financially worse off

employee bargaining power; encourages

under the scheme

entrepreneurial activity; and reduces the

• Reduces the supply of labour: decreases hours

opportunity cost of full time training or

worked; increases migration of skilled workers;

education.

discourages people from taking entry level jobs;

• Lowers administrative, management and

discourages further education and training; and the

operating costs

EMTRs for families with children are very high

discouraging further work, MFTC*.

* These specific effects relate to one or more of

• High personal income taxes have negative

the three versions of the GMI that were modelled

implications for saving, investment and productivity

by Treasury. Fuller information is contained in

the Treasury report

• Lowers economic growth (estimated at 2.8

percentage points per year)

• Non-alignment causes integrity and coherence issues

for the tax system

(GMI - A Preliminary Assessment of the Tax and Equity Implications:1909076) .

28

20180164 TOIA Binder New

Doc 4

Page 35 of 62

IN-CONFIDENCE

89. A core assumption in Treasury’s 2010 modelling was that the GMI scheme would be funded by

increased personal income tax, although it was noted that it may be possible to fund part of the

GMI by increasing other taxes, by base broadening, or by reducing government expenditure in

other areas.

90. In developing advice for the incoming government, Treasury should consider providing well-

considered advice on the risks and benefits of a UBI-type approach to income support, key design

considerations, and options for meeting the costs associated with such a policy. This is likely to

require new modelling to reflect different assumptions. Treasury could also consider presenting

alternative options that could achieve similar objectives to a UBI, with fewer downsides.

91. More generally, the UBI debate highlights the perceived binary nature of targeted and universal

approaches to improving income adequacy and distribution. In reality, all systems have a

combination of both approaches. Even within an investment approach, there will continue to be

a core set of universal provisions (e.g. in health and education), with explicit decisions needed

about the balance between these and more targeted interventions.

92. There may be value in Treasury better articulating the respective roles of targeted vs universal

support and services. A report by Gugushvili and Hirsch (2014) reviews the effectiveness of

universal and targeted social spending in reducing poverty, against the background of

longstanding debate and emerging evidence in this area. They note that the universal vs. means-

tested debate is far from resolved, but that more recent studies have challenged the previously

established correlation between universal systems, higher redistribution and improved poverty

reduction. Sen (2009) whose work on capabilities has strongly influenced Treasury’s Living

Standards Framework, has also written on the political economy of targeting.

Deleted - Not Relevant to Request

29

20180164 TOIA Binder New

Doc 4

Page 36 of 62

IN-CONFIDENCE

Deleted - Not Relevant to Request

30

20180164 TOIA Binder New

Doc 4

Page 37 of 62

IN-CONFIDENCE

Deleted - Not Relevant to Request

31

20180164 TOIA Binder New

Doc 4

Page 38 of 62

IN-CONFIDENCE

Suggested areas of focus for future Treasury advice

Deleted - Not Relevant to Request

32

20180164 TOIA Binder New

Doc 4

Page 39 of 62

IN-CONFIDENCE

Deleted - Not Relevant to Request

• Clarifying its policy position and strengthening advice on the roles and respective uses of

targeted vs universal support and services, and the balance between them.

105.

With regard to welfare settings, Treasury could

(slide 31):

• Deleted - Not Relevant to Request

• Refresh modelling and analysis in relation to the universal basic income concept, to take

account of current international developments and New Zealand proposals (though not

costing specific political party policies);

• Deleted - Not Relevant to Request

•

106.

•

•

•

Deleted - Not Relevant to Request

33

Pages 34-42 Deleted - Not Relevant to Request

20180164 TOIA Binder New

Doc 4

Page 40 of 62

IN-CONFIDENCE

References

Anon (2009) Design of the Income Tax / Transfer System: Background Paper for the Tax

Working Group. 24 July 2009.

Australian Government Productivity Commission (2015) Tax and Transfer Incidence in

Australia. Commission Working Paper, Canberra. October 2015

Burton, Tony, Louise Butler, Melissa Piscetek, Caroline Reid, Paul Rodway and Robert

Templeton (2016) The benefits of improved social sector performance. Background paper for

He Tirohanga Mokopuna: 2016 Statement on the Long-Term Fiscal Position. New Zealand

Treasury. November 2016

Cleland, Alice, Amapola Generosa, Ben Wallace, Dan Harvey and Holly Norton (2016) The

workforce, workplace and the nature of work: A snapshot of key trends. Ministry of Business,

Innovation and Employment.

Conway, Paul, Lisa Meehan & Dean Parham (2015) Who benefits from productivity growth? –

The labour income share in New Zealand, New Zealand Productivity Commission Working

Paper 2015/1. Wellington: Productivity Commission.

Design of the Income Tax/Transfer System: Background paper for the Tax Working Group

(http://www.victoria.ac.nz/sacl/cagtr/twg/Publications/taxes_transfers.pdf)

Eichhorst, Werner (2017) Labour market institutions and the future of work: Good jobs for all?

IZA Institute of Labour Economics Policy Paper Series. IZA Policy Paper No. 122. January 2017

Fletcher, Michael (2015) The structure and generosity of financial assistance for beneficiaries:

How New Zealand compares with other OECD countries. March 2015. Retrieved from the

New Zealand Ministry of Social Development website

(https://www.msd.govt.nz/documents/about-msd-and-our-work/publications-

resources/research/social-assistance-international-comparisons/social-assistance-

international-comparisons-publication-version.docx

Gregg, Paul (2012) Pre-distribution opens up a new set of policy tools but also a key constraint.

www.blogs.lse.ac.uk

Gugushvili, Dimitri and Donald Hirsch (2014) Means-tested and universal approaches to

poverty: international evidence and how the UK compares. Centre for Research in Social Policy

Working Paper 640. Loughborough University. August 2014

Hirsch, Donald (2013) Paying for children: the state’s changing role and income adequacy.

Journal of Social Policy. Volume 42, Number 3, Pgs 495-512

Hurnard, Roger (2012) The assessment of retirement income system options. A paper for the

external panel on the Treasury’s long-term fiscal statement. October 2012

43

20180164 TOIA Binder New

Doc 4

Page 41 of 62

IN-CONFIDENCE

Johnson, Jennifer and Kristie Carter (2015) Increasing Equity Background Paper. Treasury’s

Living Standards Framework Papers. The New Zealand Treasury. December 2015

Leoni, Thomas (2015) The social investment perspective as guiding principle for welfare state

adjustment. WIFO (the Austrian Institute for Economic Research). May 2015

Maloney, Tim and Amanda Gilbertson (2013) A literature review on the effects of Living Wage

policies. Auckland Council technical report TR2013/034

Martin, John (2014) Activation and active labour market policies in OECD countries: stylised

facts and evidence on their effectiveness. IZA Policy Paper No 84. June 2014

Nolan, Patrick (2017) Family and work tax credits in five liberal welfare states. Presentation to

Australasian Tax Teachers Association Conference. January 2017

Nolan, Patrick (2007) Lifting families’ incomes. Policy Quarterly. Volume 3, Issue 2, Pgs 22-29

Nolan, Patrick (undated) When work and marriage do not pay: poverty traps and marriage

penalties in New Zealand’s tax-benefit system. New Zealand Institute for Economic Research.

OECD (2016) Benefits and Wages Indicators. Printed on 22/03/2017 from

www.oecd.org/ols/social/workincentives

Pacheco, Gail, Philip S Morrison, Bill Cochrane, Stephen Blumenfeld and Bill Rosenberg

(undated) Understanding insecure work. New Zealand Work Research Institute and Victoria

University of Wellington Centre for Labour, Employment and Work.

Perry, Bryan (2016) Household incomes in New Zealand: Trends in indicators of inequality and

hardship 1982 to 2015. Ministry of Social Development, Wellington. August 2016

Raven, Jason (2015) Financial incentives to work: the size of the margin between benefits and

in-work incomes. Policy Quarterly. Volume 11, Issue 4, November 2015, Pgs 26-33

Rosenberg, Bill (2014) New Zealand’s wages system is buggered. Briefing papers.

www.briefingpapers.co.nz

Sen, Amartya (1995) The political economy of targeting. In: Van de Walle, D and Nead K (eds)

Public Spending and the Poor: Theory and Evidence. John Hopkins University Press. Baltimore

The Treasury (2010) A guaranteed minimum income for New Zealand: A preliminary

assessment of the tax and equity implications. Welfare Working Group Options for Reform.

October 2010

Victoria University of Wellington Tax Working Group (2010) A Tax System for New Zealand’s

Future. Report of the Victoria University of Wellington Tax Working Group. January 2010

44

20180164 TOIA Binder New

Doc 4

Page 42 of 62

IN-CONFIDENCE

Other source documents

Adema, Willem (2011) Setting the scene: the mix of family policy objectives and packages

across the OECD. Children and Youth Services Review, Vol 34 (2012) Pgs 487-498.

Aziz, Omar, Norman Gemmell and Atheme Laws (2013) The distribution of income and fiscal

incidence by age and gender: Some evidence from New Zealand. Victoria University of

Wellington, Working Papers in Public Finance. Working Paper 10/2013

Broadway, Barbara, Guyonne Kalb, Duncan McVicar and Bill Martin (2016) The impact of paid

parental leave on labour supply and employment outcomes. Melbourne Institute Working

Paper Series. Working Paper No. 9/16. University of Melbourne Faculty of Business and

Economics. March 2016

www.basicincome.org – articles on basic income pilots being undertaken in various

jurisdictions around the world

Colombino, Ugo (2015) Is unconditional basic income a viable alternative to other social

welfare measures? IZA World of Labour 2015: 128. February 2015 www.wol.iza.org

Crampton, Eric (2016) I love the idea of a Universal Basic Income. But here’s the problem. 31

March 2016. www.thespinoff.co.nz

Creedy, John (undated) Designing tax and transfer schemes: some basic principles.

Fletcher, Michael (2016) A Universal Basic Income may be a good idea but we will still need

social security that works. 30 March, 2016. www.briefingpapers.co.nz

NZIER (2016) Defining social investment, Kiwi-style. NZIER pubic discussion paper. Working

Paper 2016/5. December 2016

Perry, Bryn (2016) The material wellbeing of New Zealand households: trends and relativities

using non-income measures, with international comparisons. Ministry of Social Development.

August 2016

Rankin, Keith (2016) Universal Basic Income and Income Tax Reform. 22 March 2016.

www.briefingpapers.co.nz

Statistics New Zealand (2016) Household living-cost price indexes: Background. October 2016

www.statistics.govt.nz

Stewart, Miranda, Andre Moor, Peter Whiteford and R Quentin Grafton (2015) A stocktake of

the tax system and directions for reform: five years after the Henry Review. Tax and Transfer

Policy Institute, Crawford School of Public Policy. Australian National University. February

2015

Social Policy Evaluation and Research Unit (2015) Perceptions of income adequacy by low

income families. SUPERU, January 2015

The Opportunities Party: UBI and Thriving Families. www.top.org.nz

45

20180164 TOIA Binder New

Doc 4

Page 43 of 62

IN-CONFIDENCE

Van Der Linden, Bruno (2016) Do in-work benefits work for low-skilled workers? IZA World of

Labour 2016: 246. March 2016 www.wol.iza.org

Whiteford, Peter (undated presentation) adequacy of social security benefits for working age

households: a comparative assessment. Crawford School of Public Policy, Australian National

University

http://www.google.co.nz/url?sa=t&rct=j&q=&esrc=s&source=web&cd=1&cad=rja&uact=8&ve

d=0ahUKEwij2IPYsP3SAhVilVQKHTdPAfcQFggYMAA&url=http%3A%2F%2Frsss.anu.edu.au%2Fs

ites%2Fdefault%2Ffiles%2FPeterWhiteford.pdf&usg=AFQjCNF_lCVAns-XDZpdU0rxjWx90iqQiQ

46

20180164 TOIA Binder New

Doc 4-1

Page 44 of 62

The Treasury’s position on

income adequacy and poverty:

Previous advice and

possible future d

irections

Barbara Annesley

7 April 2017

20180164 TOIA Binder New

Doc 4-1

Page 45 of 62

Purpose and scope

This work:

Identifies policy levers and reviews policy advice

Discusses emerging trends and issues

Makes suggestions for areas for further work and focus

It doesn’t:

Provide an exhaustive review of advice, da ta and evidence

Include a detailed discussion of definitional and measurement issues

Consider the distribution of income (inequality)

Propose specific policy changes

2

20180164 TOIA Binder New

Doc 4-1

Page 46 of 62

Setting the scene:

Measures, data and policy levers

Pages 4-12 Deleted - Not Relevant to Request

3

20180164 TOIA Binder New

Doc 4-1

Page 47 of 62

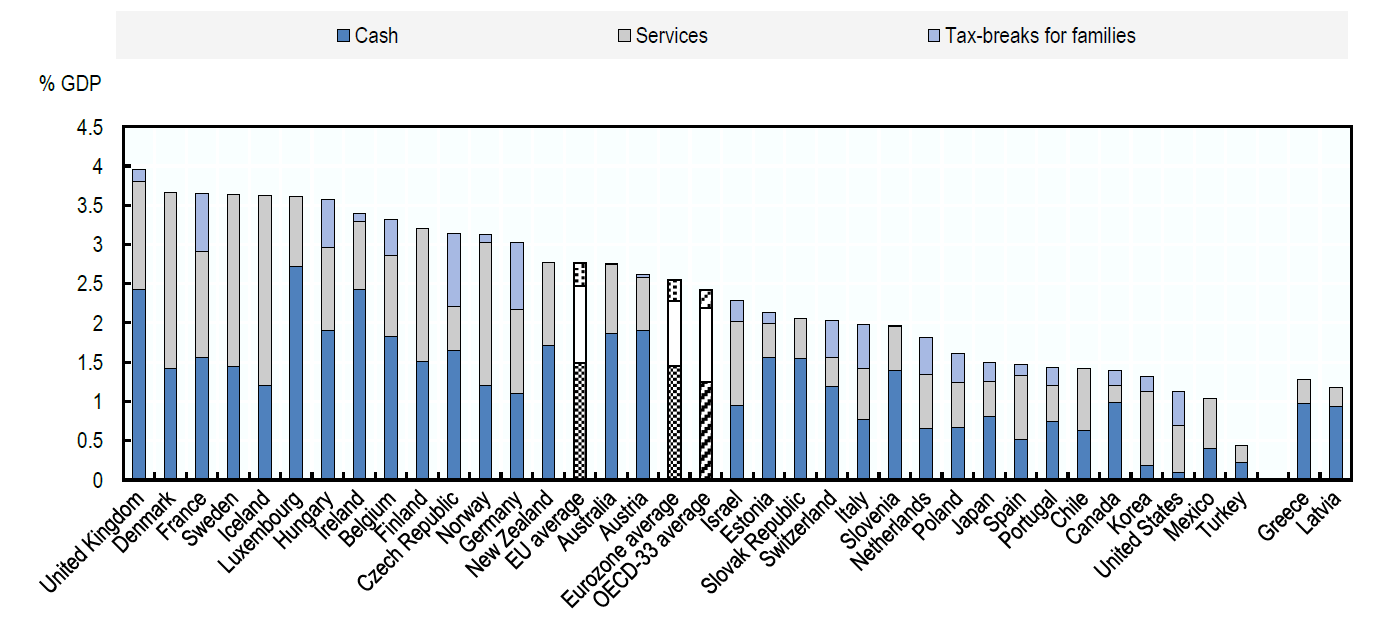

NZ has a mix of measures (noting difficulty of cross-

country comparisons)

Public spending on family benefits in cash, in-kind and through tax measures (percentage of GDP, 2013)

Source: OECD Benefits and Wage Indicators Database

13

20180164 TOIA Binder New

Doc 4-1

Page 48 of 62

Previous Treasury advice:

Frameworks used, issues identified and proposed

directions for change

14

20180164 TOIA Binder New

Doc 4-1

Page 49 of 62

Deleted - Not Relevant to Request

15

20180164 TOIA Binder New

Doc 4-1

Page 50 of 62

Deleted - Not Relevant to Request

16

20180164 TOIA Binder New

Doc 4-1

Page 51 of 62

Suggested areas for change identified in Treasury

advice (mainly 2013-15)

Deleted - Not Relevant to Request

Universal benefits and changes to personal tax settings and wage levels are not supported as ways to lift

incomes (high cost, poorly targeted, potential distortionary economic and labour market effects)

Deleted - Not Relevant to Request

Pages 18-21 Deleted - Not Relevant to Request

17

20180164 TOIA Binder New

Doc 4-1

Page 52 of 62

New and emerging considerations:

The nature and quality of employment; challenges

to current paradigms

22

20180164 TOIA Binder New

Doc 4-1

Page 53 of 62

Deleted - Not Relevant to Request

23

20180164 TOIA Binder New

Doc 4-1

Page 54 of 62

Challenges to existing paradigms, settings and

advice

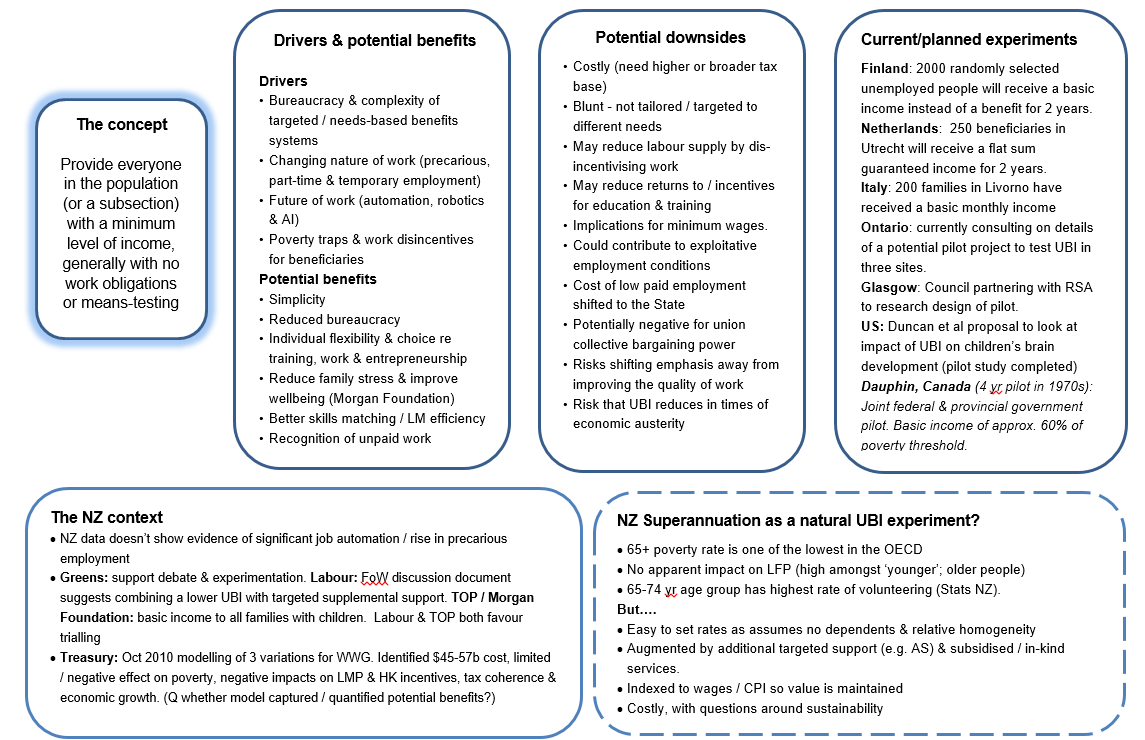

Universal vs. targeted approaches to addressing poverty:

UBI the most obvious example (a response to increased targeting, ‘new social risks’

and changing nature of work)

In reality universal vs. targeted approaches are binary – there’s a place for both

Treasury’s 2010 modelling based on specific set of features and assumptions. Worth

re-visiting and doing modelling a few options

24

20180164 TOIA Binder New

Doc 4-1

Page 55 of 62

Universal Basic Income

25

20180164 TOIA Binder New

Doc 4-1

Page 56 of 62

Previous Treasury advice on UBI

Benefits

Costs

More equal distribution of income

Poverty is either increased across all relative levels as Superannuitants

Removes disincentive for beneficiaries to

have their payment decreased by 44% on average*, or is increased

undertake part-time work

when measured at the 50 percent relative level*.

Poverty is reduced but only at the 60 and 70

Horizontal equity problems due to differential treatment of one and

percent relative levels*

two parent families

May improve labour market outcomes in

Many current beneficiaries (e.g. sole parents, the disabled and carers)

some areas: more employee flexibility;

will be financially worse off under the scheme

encourages unpaid work; additional employee

Reduces the supply of labour: decreases hours worked; increases

bargaining power; encourages entrepreneurial

migration of skilled workers; discourages people from taking entry level

activity; and reduces the opportunity cost of

jobs; discourages further education and training; and the EMTRs for

full time training or education.

families wit

h children are very high discouraging further work, MFTC*.

Lowers administrative, management and

High personal income taxes have negative implications for saving,

operating costs

investment and productivity

Lowers economic growth (estimated at 2.8 percentage points per year)

Non-alignment causes integrity and coherence issues for the tax system

* These specific effects relate to one or more of the three versions

of the GMI that were modelled by Treasury.

26

20180164 TOIA Binder New

Doc 4-1

Page 57 of 62

Deleted - Not Relevant to Request

27

20180164 TOIA Binder New

Doc 4-1

Page 58 of 62

Deleted - Not Relevant to Request

28

20180164 TOIA Binder New

Doc 4-1

Page 59 of 62

Potential areas of f ocus for future

Treasury advice

29

20180164 TOIA Binder New

Doc 4-1

Page 60 of 62

At a strategic level, Treasury could:

Deleted - Not Relevant to Request

Clarify its policy position and strengthen advice on the roles and respective uses

of targeted vs universal support and services, and the balance between them

30

20180164 TOIA Binder New

Doc 4-1

Page 61 of 62

Deleted - Not Relevant to Request

31

20180164 TOIA Binder New

Doc 4-1

Page 62 of 62

Deleted - Not Relevant to Request

32

Document Outline