30 September 2025

Ref: DOIA-REQ-0019128

Spencer Jones

Email: [FYI request #31890 email]

Tēnā koe Spencer Jones

Thank you for your email of 4 August 2025 to the Ministry of Business, Innovation and Employment

(MBIE) requesting, under the Official Information Act 1982 (the Act), the following information:

Under the Official Information Act 1982, I request:

1. All internal MBIE briefings, Cabinet papers, Regulatory Impact Assessments, legal advice, or

memos between 1 Jan 2024 and today regarding:

- Drafting, intent, or legal rationale behind the Credit Contracts and Consumer Finance

Amendment Bill (2025);

- Any retrospective effect on litigation, especially the Banking Class Action (CIV-2021-404-119);

- Implications for consumer rights under CCCFA ss 22, 48, 99(1), and 99(1A).

2. All correspondence (emails, meeting notes, Teams chats, or memos) between MBIE staff and:

- Minister Scott Simpson or his office;

- Representatives of ANZ, ASB, NZBA, or any law firms (including Bell Gully, Russell McVeagh, or

MinterEllisonRuddWatts);

- Treasury, PCO, or the Commerce Commission concerning the class action or amendment bill.

3. Any records of:

- Stakeholder consultation prior to the bill’s drafting;

- Concerns about interference with judicial proceedings;

- Conflict-of-interest declarations by officials or advisors.

If any material is withheld, please cite the specific section of the OIA relied on.

I note you have made multiple requests on this topic, both to MBIE and to the Minister of Commerce and

Consumer Affairs, Hon Scott Simpson. I note that this response canvasses information not previously

considered in response to your previous requests.

I understand that your request relates to the retrospective provision of the Credit Contracts and

Consumer Finance Amendment Bill 2025.

In terms of your request regarding records of ‘declared conflicts of interest’, we note we hold records of

two employees involved in the policy development of these reforms were customers of one of the

defendants in the class litigation during the relevant period. This was considered a low-level perception

risk; in that they do not benefit from the decisions taken by Cabinet. We are withholding identifying

information under section 9(2)(a) of the Act - to protect the privacy of natural persons. No other

information relevant to this part of your request has been identified.

Please find attached the documentation relevant to your request.

Please note some information has been withheld under the following sections of the Act:

• 9(2)(a), to protect the privacy of natural persons;

• 9(2)(b)(ii), to protect information where the making available of the information would be likely

unreasonably to prejudice the commercial position of the person who supplied or who is the

subject of the information;

• 9(2)(ba)(i), to protect information which is subject to an obligation of confidence or which any

person has been or could be compelled to provide under the authority of any enactment, where

the making available of the information would be likely to prejudice the supply of similar

information, or information from the same source, and it is in the public interest that such

information should continue to be supplied; and

• 9(2)(h), to maintain legal professional privilege.

I do not consider that the withholding of this information is outweighed by public interest considerations

in making the information available.

If you wish to discuss any aspect of your request or this response, or if you require any further assistance,

please contact [email address].

You have the right to seek an investigation and review by the Ombudsman of this decision. Information

about how to make a complaint is available at www.ombudsman.parliament.nz or freephone 0800 802

602.

Nāku noa, nā

Glen Hildreth

Manager Consumer Policy

Commerce, Consumer and Business

Document Schedule

#

Subject/Description

Withholding grounds

1

Email Pack – Commerce Commission

9(2)(a)

9(2)(ba)(i)

9(2)(h)

2

Email Pack - Treasury

9(2)(a)

9(2)(ba)(i)

9(2)(b)(ii)

9(2)(h)

From:

Mark Atwel <Mark.Atwel @comcom.govt.nz>

Sent:

Tuesday, 1 July 2025 3:45 pm

To:

Marcus Smith

Subject:

Commerce Commission - Sections 17 & 22 enforcement outcomes

Attachments:

Commerce Commission - s17 & 22 Disclosure Cases - Prepared for MBIE July 2025

(5530437.6).pdf

Follow Up Flag:

Fol ow up

Flag Status:

Flagged

Kia ora Marcus,

In our meeting last Thursday you requested that we provide you with an update of the table we provided in

August 2024 detailing Commission enforcement outcomes and open cases for section 17 (initial disclosure)

and 22 (variation disclosure) investigations.

I attach a copy of a table detailing Commission enforcement outcomes and open investigations relating to

sections 17 and 22 for the period June 2015 to July 2025.

Please note that the table contains non-public confidential information – particularly our open investigations

and filed but not yet announced legal proceedings.

We also repeat some of the qualifications we provided in August about the completeness of the table data.

It is challenging for us to provide details of all disclosure cases because we don’t record enforcement

outcomes in our systems based on section breached in an easily retrievable way.

This means that while the attached is accurate for public enforcement outcomes (investigations

resulting in a warning or settlement outcome) the attached will significantly under record the number

of low level outcomes where s99(1A) may have been involved (i.e. compliance advice and no further

action letters).

Because there is no legal obligation to report potential breaches to the Commission, the attached

table reflects not only the level of potential breach by the lender but also the willingness of the lender

Released under the

to report errors to us.

In some cases a lender may have told us about a disclosure error but we chose not to open an

investigation.

Regards

Mark

Official Information Act 1982

Mark Atwel

Principal Adviser |Compe on, Fair Trading and Credit Branch

Commerce Commission | Te Komihana Tauhokohoko

Level 13, 55 Shortland Street | PO Box 105-222 | Auckland 1143 | New Zealand

DDI +64 (0)9 920 3492 | Mob s 9(2)(a)

| mark.atwel @comcom.govt.nz

www.comcom.govt.nz

1

This email may contain information that is confidential or legal y privileged. If you have received this email in error please

immediately notify the sender and delete the email, without using it in any way. The views presented in this email may not be

those of the Commission.

Released under the

Official Information Act 1982

2

Commerce Commission – Sections 17 and 22 disclosure breach enforcement outcomes June 2015 to July 2025 –

Contains confidential information

Public outcomes (Warnings/settlements/judgments)

Banks and finance companies

Lender name

Breach type

Breach period

Enforcement outcome

Cashinaflash.co.nz Limited

Initial disclosure (s 17)

June – October 2015

Warning 8 March 2016 (refunds involved)

(15628)

Shaw Personal Finance

Initial disclosure (s 17)

June 2015 - March 2016

Warning 5 July 2016 (refunds involved)

Limited (15830)

Adelphi Finance Limited

Initial disclosure (s 17)

June 2015 – March 2016

Warning 16 August 2016 (refunds involved)

(15821)

Aotea Finance Group

Initial disclosure (s 17)

June 2015 – February 2016

Settlement 15 July 2019 (refunds involved)

companies

Approved Finance Limited

Initial disclosure (s 17)

June 2015 – June 2016

Warning 6 April 2017

(15906)

Linsa Finance Limited (15905) Initial disclosure (s 17)

June 2015 – March 2016

Settlement August 2019 (refunds involved)

Released under the

Finance Ezi Limited t/a Ezi

Initial disclosure (s 17)

June 2015 – February 2017

Settlement May 2019 (refunds involved)

Finance (16307)

Official Information Act 1982

2

ANZ Bank New Zealand

Responsible lending (s9C) –

June 2015 – May 2016

Settlement March 2020 (refunds involved)

Limited (27686)

Incorrect information provided

in agreed variation letters

Profile Finance Limited

Initial disclosure (s 17)

June 2015 – November 2017

Settlement April 2020 (refunds involved)

(34203)

Westpac New Zealand

Initial disclosure (s 17)

May 2017 – March 2018

Settlement January 2020 (refunds involved)

Limited (40997)

Kiwibank Limited

Responsible lending (s 9C) –

June 2015 – March 2019

Settlement August 2020 (refunds involved)

arising from agreed variation

disclosure failure

Bank of New Zealand

Initial disclosure (s 17) and

June 2015 – February 2017

Warning December 2020 (refunds

Variation disclosure (s 22)

involved)

Ten or more discrete breach

circumstances (as set out in

Warning letter)

ASB Bank Limited (44141)

Responsible lending (s 9C) –

June 2015 – June 2019

Settlement February 2021 (refunds

arising from agreed variation

involved)

disclosure failure

Released under the

Two issues.

Kookmin Bank (45604)

Initial disclosure (s 17)

June 2015 – October 2021

Settlement June 2023 (refunds involved)

Official Information Act 1982

5219881.1

3

The Hongkong and Shanghai

CCCFA breaches include initial

June 2015 – October 2021

Warning June 2023 (refunds involved)

Banking Corporation Limited

disclosure (s 17) and agreed

(45870)

variation disclosure (s 22)

Investment Bureau Limited

CCCFA breaches include initial

June 2018 – February 2021

Warning November 2023 (refunds

(45990)

disclosure (s17)

involved)

Southland Building Society

Agreed variation disclosure

March 2014 – November

Warning June 2024 (refunds involved)

t/a Southland Bank (46240)

(s 22)

2021

Dolbak Finance Limited

Agreed variation disclosure

December 2021 – November

Warning February 2024 (refunds involved)

(46178)

(s 22)

2022

El Cheapo Cars Limited t/a

Agreed variation

June 2015 – November 2021

Judgment 20 May 2025 (Link to be added to

Ezybid Finance (47455)

disclosure (s 22)

Commission website soon. Criminal

proceedings. Fined $115,000. Ordered to

pay statutory damages to affected

borrowers)

High cost lenders

Lender name

Breach type

Breach period

Enforcement outcome

Acorn Finance Limited

CCCFA breaches include initial

1 and 27 May 2020

Warning February 2022 (refunds involved)

(45104)

disclosure (s 17)

Released under the

Hippo Holdings Limited

CCCFA breaches include initial

May – June 2020

Warning and Enforceable Undertakings

(45101)

disclosure (s 17)

December 2022 (refunds involved)

Tiny Loans Limited (45401)

CCCFA breaches include initial

June 2020 – August 2021

Warning February 2023 (refunds involved)

disclosure (s 17)

Eagle M.A.N. Group Limited

Alleged CCCFA breaches

June 2015 – August 2022

Judgment October 2024 (declaration of

include initial disclosure (s 17)

breach of s17, no refunds involved. Civil

Official Information Act 1982

pecuniary penalty for breach of high cost

5219881.1

4

rules)

Local Authorities

Lender name

Breach type

Breach period

Enforcement outcome

Auckland Council (44827)

CCCFA breaches include initial

June 2015 – February 2020

Warning February 2021 (refunds involved)

disclosure (s 17)

Canterbury Regional Council

CCCFA breaches include initial

August 2018 – March 2021

Warning August 2023 (refunds involved)

t/a Environment Canterbury

disclosure (s 17)

(45299)

Mobile traders [NB: typically don’t charge interest but s99(1A) results in waiving or refunding of credit and default fees]

Ace Marketing Limited

Breaches included s17

June 2013 – November 2015

Judgment (fine and ancillary order for costs

of borrowing)

Bestdeals 4 You Limited

Initial disclosure breach (s 17)

June 2015 – April 2016

Judgment (fine and ancillary order for COB)

Best Buy Limited

Breaches included s17

June 2015 – April 2016

Judgment (fine and ancillary order for COB)

Appenture Marketing Limited Breaches included s17

June 2015 – April 2016

Judgment (fine and ancillary order for COB)

Budget Warehouse Limited

Initial disclosure breach (s 17)

June 2015 – May 2016

Judgment (fine and ancillary order for COB)

Released under the

Macful International Limited

Breaches included s17

April 2015 – November 2015

Judgment (fine and ancillary order for COB)

Mobile Shop Limited

Breaches included s17

October 2015 – September

Judgment (fine and ancillary order for

2016

statutory damages)

Greenfield Global Limited t/a

Breaches included s17

June 2015 – April 2016

Warning (refunds involved)

KiwiOwn

Official Information Act 1982

5219881.1

5

Non-public enforcement outcomes – (Compliance advice letters and litigation)

Banks and finance companies

s 9(2)(ba)(i)

Released under the

Official Information Act 1982

5219881.1

6

Non-public open investigations – No enforcement outcome as at 1 July 2025

Banks and finance companies

s 9(2)(ba)(i)

Released under the

Official Information Act 1982

5219881.1

From:

Mark Atwel <Mark.Atwel @comcom.govt.nz>

Sent:

Monday, 12 August 2024 3:41 pm

To:

Marcus Smith

Cc:

Sarah Bartlett; Jil Pitches; Crystal Euden; Brett Carter; Cathrine McIntosh; Linn

McManamon

Subject:

FW: For feedback by 12pm Thurs - Draft Cabinet paper on Financial Services

Reforms policy decisions [IN-CONF DENCE: RELEASE-EXTERNAL]

Attachments:

Commerce Commission - s99(1A) Disclosure Cases - Prepared for

MBIE(5219881.2).pdf

Follow Up Flag:

Fol ow up

Flag Status:

Flagged

Kia ora Marcus,

I attach a document setting out enforcement outcomes for potential breaches of initial disclosure (s17) and

agreed variation disclosure (s22) obligations. Note that the attached contains confidential information.

For a number of reasons it is challenging for us to provide the information you have requested.

The primary reason is that we don’t record enforcement outcomes in our systems based on section breached

in an easily retrievable way.

This means that while the attached is accurate for public enforcement outcomes (investigations resulting in a

warning or settlement outcome) the attached will significantly under record the number of low level outcomes

where s99(1A) was involved (i.e. compliance advice and no further action letters).

There are also a number of other qualifications to the data provided or challenges with replying to your

request:

It is not clear what a “distinct event” is for the purposes of your question – some lender errors will

a ect multiple products (e.g. home loans, credit cards, and personal loans) and sometimes there

are minor variations on the same error.

The attached does not include investigations where we have concluded that there is a likely breach

Released under the

of ss17 or 22 but where we concluded that ss99(1A) was not triggered in a way that required refunds

(which investigations still require significant resource for the Commission and lenders).

Because there is no legal obligation to report potential breaches to the Commission, the attached

table reflects not only the level of potential breach by the lender but also the willingness of the

lender to report errors to us (and the biggest banks are significantly more likely to do this – e.g. ANZ

reports errors to us on a quarterly cadence).

In some cases a lender may have told us about a disclosure error but we chose not to open an

investigation.

Official Information Act 1982

Regards

Mark

Mark Atwell

Principal Adviser | Credit Branch

Commerce Commission | Te Komihana Tauhokohoko

Level 13, 55 Shortland Street | PO Box 105-222 | Auckland 1143 | New Zealand

DDI +64 (0)9 920 3492 | Mob s 9(2)(a)

| mark.atwel @comcom.govt.nz

1

www.comcom.govt.nz

From: Marcus Smith <[email address]>

Sent: Thursday, August 8, 2024 11:42 AM

To: Mark Atwel <Mark.Atwel @comcom.govt.nz>

Subject: RE: For feedback by 12pm Thurs - Draft Cabinet paper on Financial Services Reforms policy decisions [IN-

CONF DENCE: RELEASE-EXTERNAL]

Thanks for ge ng us these comments Mark. Helpful as always.

One further request if it’s not too much trouble:

To provide a sense of scale with s99(1A), would you be able to give me an idea of the number of a) disclosure

failures (as in dis nct events giving rise to s99(1A) liability) and b) lenders responsible for them that the Commission

is aware of or has se led both:

Pre-December 2019

Post-December 2019?

I’l make sure I caveat it / express loosely if it’s hard to be precise. But would be useful if you can provide something

on this.

Thanks

Marcus

From: Mark Atwel <Mark.Atwel @comcom.govt.nz>

Sent: Wednesday, August 7, 2024 4:09 PM

To: Marcus Smith <[email address]>

Cc: Sal y Whineray Groom <Sal [email address]>; Michel e Schulz <Michel [email address]>;

Manon Roehrig <[email address]>; Chris Cuthbertson <[email address]>; Bil

Busfield <Bil .[email address]>; Nelson Curry <[email address]>; Alice Jackson

<[email address]>; Caitlin Melhuish <[email address]>; Linn McManamon

<[email address]>; Crystal Euden <[email address]>; Sarah Bartlett

<[email address]>; Cathrine McIntosh <[email address]>; Brett Carter

<[email address]>; Jil Pitches <Jil .[email address]>; Andrew Palmer

<[email address]>

Subject: RE: For feedback by 12pm Thurs - Draft Cabinet paper on Financial Services Reforms policy decisions [IN-

Released under the

CONF DENCE: RELEASE-EXTERNAL]

Kia ora Marcus,

Thank you for the opportunity to comment on the draft RIS.

I attach the consumer credit RIS with comments from Commission sta .

We have no comment on the conduct RIS.

Official Information Act 1982

Regards

Mark

Mark Atwell

Principal Adviser | Credit Branch

Commerce Commission | Te Komihana Tauhokohoko

Level 13, 55 Shortland Street | PO Box 105-222 | Auckland 1143 | New Zealand

DDI +64 (0)9 920 3492 | Mob s 9(2)(a)

| mark.atwel @comcom.govt.nz

2

www.comcom.govt.nz

From: Marcus Smith <[email address]>

Sent: Wednesday, July 31, 2024 12:28 PM

To: Caitlin Melhuish <[email address]>; Elena Obolonkina [TSY

<[email address]>; Linn McManamon <[email address]>; Nelson Curry

<[email address]>; Daryl.Col [email address]; Louis Campbel <Louis.Campbel [email address]>; Alice

Jackson <[email address]>; [email address]; [email address]; Edwin Mitson

<[email address]>; Victoria Learmonth <[email address]>; Crystal Euden

<[email address]>; Mark Atwel <Mark.Atwel @comcom.govt.nz>; Sarah Bartlett

<[email address]>; Karla Reynolds <[email address]>; Cathrine McIntosh

<[email address]>; James Sergeant <[email address]>; Louise Unger

<[email address]>; Lachlan Cartwright <[email address]>; Debbie McLean

<[email address]>; Disee Anorpong [TSY <[email address]>; Mark Holden

<[email address]>; Brett Carter <[email address]>; Cathie Jenkins

<[email address]>; mary.l ewel [email address]; Michael Sherwood [TSY]

<[email address]>

Cc: Sal y Whineray Groom <Sal [email address]>; Stephanie Zhang <[email address]>;

Michel e Schulz <Michel [email address]>; Manon Roehrig <[email address]>; Emma Moore

<[email address]>; Daniel Meech <[email address]>; El iot Clark

<El [email address]>; Chris Cuthbertson <[email address]>; Bil Busfield

<Bil .[email address]>; Richard Clough <[email address]>; Katrina Melvil e

<Katrina.Melvil [email address]>; Iris Henderson <[email address]>; Andrew Palmer

<[email address]>

Subject: RE: For feedback by 12pm Thurs - Draft Cabinet paper on Financial Services Reforms policy decisions [IN-

CONF DENCE: RELEASE-EXTERNAL]

Kia ora anō,

We also invite your feedback on the a ached regulatory impact statements for consumer credit and conduct

reforms (for anyone who doesn’t already have the la er), which are currently before our internal QA panels. You’re

welcome to let us know if you spot anything problema c before Ministerial consulta on (same deadline as below

sorry), but we would like to take the me during Ministerial consulta on to work through parts of our analysis with

you – par cularly for the consumer credit RIS (see some comments/queries embedded).

Released under the

Please get us your comments on either document / both by COP next Wednesday 7 August, so we have me to

make changes before our panels sign off final versions that then go to the Minister’s office.

We’l be in touch separately with the FMA and Commission staff about a me early next week (when Chris is back)

to discuss some of the consumer credit op ons. Others are welcome to join us too: just let me know if you’re

interested.

Thanks as always for your help.

Official Information Act 1982

Ngā mihi

MBIE

From: Caitlin Melhuish <[email address]>

Sent: Tuesday, July 30, 2024 1:53 PM

To: Elena Obolonkina [TSY <[email address]>; Linn McManamon

<[email address]>; Nelson Curry <[email address]>; Daryl.Col [email address];

Louis Campbel <Louis.Campbel [email address]>; Alice Jackson <[email address]>;

3

[email address]; [email address]; Edwin Mitson <[email address]>; Victoria

Learmonth <[email address]>; [email address]; Mark.Atwel @comcom.govt.nz;

[email address]; [email address]; [email address]; James

Sergeant <[email address]>; Louise Unger <[email address]>;

[email address]; Debbie McLean <[email address]>; Disee Anorpong [TSY

<[email address]>; Mark Holden <[email address]>; Brett Carter

<[email address]>; Cathie Jenkins <[email address]>; mary.l ewel yn-

[email address]; Michael Sherwood [TSY] <[email address]>

Cc: Sal y Whineray Groom <Sal [email address]>; Stephanie Zhang <[email address]>;

Michel e Schulz <Michel [email address]>; Marcus Smith <[email address]>; Manon Roehrig

<[email address]>; Emma Moore <[email address]>; Daniel Meech

<[email address]>; El iot Clark <El [email address]>; Chris Cuthbertson

<[email address]>; Bil Busfield <Bil .[email address]>; Richard Clough

<[email address]>; Katrina Melvil e <Katrina.Melvil [email address]>; Iris Henderson

<[email address]>; Andrew Palmer <[email address]>

Subject: For feedback by 12pm Thurs - Draft Cabinet paper on Financial Services Reforms policy decisions [IN-

CONF DENCE: RELEASE-EXTERNAL]

Kia ora koutou

Please find a ached the dra Financial Services reforms policy decisions Cabinet paper for feedback. Can you please

let us know of any significant showstoppers in the paper by 12pm Thursday. There wil be another opportunity for

you to feedback during Ministerial consulta on. I’ve provided next steps below on what we are aiming for.

There are a few gaps – eg dispute resolu on schemes. We are working on this sec on fol owing Minister decisions

yesterday and can circulate an updated paper tomorrow. However for now we would appreciate your feedback on

the CoFI and CCCFA elements of the paper.

We are consul ng separately on decisions needed for the Commission to FMA transfer, but these wil go in this

paper.

Please note this version is also s l subject to legal review par cularly of the recommenda ons.

Next steps

Friday 2 August – paper goes to MO

8-12 August Ministerial consulta on

15 August lodge paper for ECO

21 August ECO Released under the

26 August Cabinet

Real y appreciate your me and please let us know if you’d like to discuss anything in the paper.

Ngā mihi nui

Caitlin Melhuish (she/her)

Senior Policy Advisor | Financial Markets

Commerce, Consumer and Business | Building, Resources and Markets

Official Information Act 1982

Hīkina Whakatutuki | Ministry of Business, Innova on & Employment (MBIE)

Email: [email address] | Telephone: 04 831 9633

4

This email may contain information that is confidential or legally privileged. If you have received this email in error please

immediately notify the sender and delete the email, without using it in any way. The views presented in this email may not

be those of the Commission.

Released under the

Official Information Act 1982

5

Commerce Commission – Sections 17 and 22 disclosure breach enforcement outcomes June 2015 to August 2024 –

Section 99(1A) – Contains confidential information

Public outcomes (warnings/settlements)

Banks and finance companies

Lender name

Breach type

Breach period

Enforcement outcome

s

Cashinaflash.co.nz Limited

Initial disclosure (s 17)

June – October 2015

Warning 8 March 2016 (refunds involved)

9

(15628)

(

2

Shaw Personal Finance

Initial disclosure (s 17)

June 2015 - March 2016

Warning 5 July 2016 (refunds involved)

Limited (15830)

Adelphi Finance Limited

Initial disclosure (s 17)

June 2015 – March 2016

Warning 16 August 2016 (refunds involved)

(15821)

Aotea Finance Group

Initial disclosure (s 17)

June 2015 – February 2016

Settlement 15 July 2019 (refunds involved)

companies

Approved Finance Limited

Initial disclosure (s 17)

June 2015 – June 2016

Warning 6 April 2017

(15906)

Linsa Finance Limited (15905) Initial disclosure (s 17)

June 2015 – March 2016

Settlement August 2019 (refunds involved)

Released under the

Finance Ezi Limited t/a Ezi

Initial disclosure (s 17)

June 2015 – February 2017

Settlement May 2019 (refunds involved)

Finance (16307)

Official Information Act 1982

2

ANZ Bank New Zealand

Responsible lending (s9C) –

June 2015 – May 2016

Settlement March 2020 (refunds involved)

Limited (27686)

Incorrect information provided

in agreed variation letters

Profile Finance Limited

Initial disclosure (s 17)

June 2015 – November 2017

Settlement April 2020 (refunds involved)

(34203)

Westpac New Zealand

Initial disclosure (s 17)

May 2017 – March 2018

Settlement January 2020 (refunds involved)

Limited (40997)

Kiwibank Limited

Responsible lending (s 9C) –

June 2015 – March 2019

Settlement August 2020 (refunds involved)

arising from agreed variation

disclosure failure

Bank of New Zealand

Initial disclosure (s 17) and

June 2015 – February 2017

Warning December 2020 (refunds

Variation disclosure (s 22)

involved)

Ten or more discrete breach

circumstances (as set out in

Warning letter)

ASB Bank Limited (44141)

Responsible lending (s 9C) –

June 2015 – June 2019

Settlement February 2021 (refunds

arising from agreed variation

involved)

disclosure failure

Released under the

Two issues.

Kookmin Bank (45604)

Initial disclosure (s 17)

June 2015 – October 2021

Settlement June 2023 (refunds involved)

Official Information Act 1982

5219881.1

3

The Hongkong and Shanghai

CCCFA breaches include initial

June 2015 – October 2021

Warning June 2023 (refunds involved)

Banking Corporation Limited

disclosure (s 17) and agreed

(45870)

variation disclosure (s 22)

Investment Bureau Limited

CCCFA breaches include initial

June 2018 – February 2021

Warning November 2023 (refunds

(45990)

disclosure (s17)

involved)

Southland Building Society

Agreed variation disclosure

March 2014 – November

Warning June 2024 (refunds involved)

t/a Southland Bank (46240)

(s 22)

2021

Dolbak Finance Limited

Agreed variation disclosure

December 2021 – November

Warning February 2024 (refunds involved)

(46178)

(s 22)

2022

High cost lenders

Lender name

Breach type

Breach period

Enforcement outcome

Acorn Finance Limited

CCCFA breaches include initial

1 and 27 May 2020

Warning February 2022 (refunds involved)

(45104)

disclosure (s 17)

Hippo Holdings Limited

CCCFA breaches include initial

May – June 2020

Warning and Enforceable Undertakings

disclosure (s 17)

December 2022 (refunds involved)

Tiny Loans Limited (45401)

CCCFA breaches include initial

June 2020 – August 2021

Warning February 2023 (refunds involved)

disclosure (s 17)

Released under the

Eagle M.A.N. Group Limited

Alleged CCCFA breaches

June 2015 – August 2022

Civil proceedings filed

include initial disclosure (s 17)

Official Information Act 1982

5219881.1

4

Local Authorities

Lender name

Breach type

Breach period

Enforcement outcome

Auckland Council (44827)

CCCFA breaches include initial

June 2015 – February 2020

Warning February 2021 (refunds involved)

disclosure (s 17)

Canterbury Regional Council

CCCFA breaches include initial

August 2018 – March 2021

Warning August 2023 (refunds involved)

t/a Environment Canterbury

disclosure (s 17)

(45299)

Mobile traders [NB: typically don’t charge interest but s99(1A) results in waiving or refunding of credit and default fees]

Ace Marketing Limited

Breaches included s17

June 2013 – November 2015

Judgment (fine and ancillary order for COB)

Bestdeals 4 You Limited

Initial disclosure breach (s 17)

June 2015 – April 2016

Judgment (fine and ancillary order for COB)

Best Buy Limited

Breaches included s17

June 2015 – April 2016

Judgment (fine and ancillary order for COB)

Appenture Marketing Limited Breaches included s17

June 2015 – April 2016

Judgment (fine and ancillary order for COB)

Budget Warehouse Limited

Initial disclosure breach (s 17)

June 2015 – May 2016

Judgment (fine and ancillary order for COB)

Macful International Limited Breaches included s17

April 2015 – November 2015

Judgment (fine and ancillary order for COB)

Mobile Shop Limited

Breaches included s17

October 2015 – September

Judgment (fine and ancillary order for

Released under the

2016

statutory damages)

Greenfield Global Limited t/a Breaches included s17

June 2015 – April 2016

Warning (refunds involved)

KiwiOwn

Official Information Act 1982

5219881.1

5

Non-public enforcement outcomes – (Compliance Advice Letters and No Further Action)

s 9(2)(ba)(i)

Open investigations – No enforcement outcome

Released under the

s 9(2)(ba)(i)

Official Information Act 1982

5219881.1

s 9(2)(ba)(i)

Released under the

Official Information Act 1982

5219881.1

From:

Marcus Smith

Sent:

Tuesday, 25 February 2025 3:26 pm

To:

Mark Atwel

Subject:

RE: Credit - Retrospective change

Looks like the statement of claim does distinguish between existing and ‘post amendment’ loans, and only

claims section 99(1A) applies to the latter. Will be interesting to see how they argue section 99(1) applies to

the former…

Marcus

From: Mark Atwel <Mark.Atwel @comcom.govt.nz>

Sent: Tuesday, 25 February 2025 1:14 pm

To: Marcus Smith <[email address]>

Subject: Credit - Retrospective change

Hi Marcus,

Following on from this morning I think we also have a potential concern around the retrospective change

drafting.

It’s probably easiest to talk through. Let me know when you are free for a quick chat.

Cheers

Mark

Mark Atwel

Principal Adviser |Compe on, Fair Trading and Credit Branch

Commerce Commission | Te Komihana Tauhokohoko

Level 13, 55 Shortland Street | PO Box 105-222| Auckland 1143 | New Zealand

DDI +64 (0)9 920 3492 | Mob s 9(2)(a)

| mark.atwel @comcom.govt.nz

www.comcom.govt.nz

Released under the

This email may contain information that is confidential or legal y privileged. If you have received this email in error please

immediately notify the sender and delete the email, without using it in any way. The views presented in this email may not be

those of the Commission.

Official Information Act 1982

1

From:

Mark Atwel <Mark.Atwel @comcom.govt.nz>

Sent:

Tuesday, 18 February 2025 12:51 pm

To:

Marcus Smith

Cc:

Katrina Melvil e

Subject:

RE: Draft RIS for review: backdating 2019 reforms to section 99(1A) of the CCCFA

Kia ora Marcus,

I wanted to confirm that we are no longer seeking the CLO legal opinion and that MBIE can cease any work

progressing this.

This is on the basis that the savings provision in the CCCF Amendment Bill (assuming we are comfortable with

the final form) lessens the need for us to understand what the potential e ects of retrospective legislation

might be.

Thanks for your initial work in investigating the release of the opinion.

Regards

Mark

Mark Atwel

Principal Adviser |Compe on, Fair Trading and Credit Branch

Commerce Commission | Te Komihana Tauhokohoko

Level 13, 55 Shortland Street | PO Box 105-222 | Auckland 1143 | New Zealand

DDI +64 (0)9 920 3492 | Mob s 9(2)(a)

| mark.atwel @comcom.govt.nz

www.comcom.govt.nz

From: Marcus Smith <[email address]>

Released under the

Sent: Wednesday, 5 February 2025 4:19 pm

To: Mark Atwel <Mark.Atwel @comcom.govt.nz>

Cc: Katrina Melvil e <Katrina.Melvil [email address]>

Subject: RE: Draft RIS for review: backdating 2019 reforms to section 99(1A) of the CCCFA

Kia ora Mark,

We may need to consider this further on Monday. (I’m away Friday and so is Glen.) Not sure the CLO advice

we’ve got would actually help the Commission with the below, but there’s some prospect of us getting more

Official Information Act 1982

direct advice on whether a savings provision may be necessary if we can swing that in time. In any case, we’re

certainly committed to working with the Commission to resolve its concern about past settlements.

Please contact Katrina if you need anything in the meantime.

Ngā mihi

Marcus

1

From: Mark Atwel <Mark.Atwel @comcom.govt.nz>

Sent: Wednesday, 5 February 2025 1:28 pm

To: Marcus Smith <[email address]>

Cc: Katrina Melvil e <Katrina.Melvil [email address]>

Subject: RE: Draft RIS for review: backdating 2019 reforms to section 99(1A) of the CCCFA

Kia ora Marcus,

Retrospective application of legislation is highly unusual in New Zealand and, given this, it would be helpful for

us to understand CLO’s view s 9(2)(h)

Given

the CLO’s greater experience in considering matters such as this it may also provide us with a degree of

comfort that we have considered the various facets of the potential implications.

Regards

Mark

Mark Atwel

Principal Adviser |Compe on, Fair Trading and Credit Branch

Commerce Commission | Te Komihana Tauhokohoko

Level 13, 55 Shortland Street | PO Box 105-222 | Auckland 1143 | New Zealand

DDI +64 (0)9 920 3492 | Mob s 9(2)(a)

| mark.atwel @comcom.govt.nz

www.comcom.govt.nz

From: Marcus Smith <[email address]>

Sent: Monday, 3 February 2025 1:58 pm

To: Mark Atwel <Mark.Atwel @comcom.govt.nz>

Cc: Katrina Melvil e <Katrina.Melvil [email address]>

Subject: RE: Draft RIS for review: backdating 2019 reforms to section 99(1A) of the CCCFA

Kia ora Mark,

We’re finding it a bit di icult to articulate the case to the CLO for sharing the legal advice based on how the

proposal might a ect the Commission. We’re thinking it may help if you’re able to share with us your specific

concerns, based on the legal advice you said you were getting. At least that way we could work out the nature

of your concerns and to what extent the CLO advice might be relevant to them (as well as how the

Released under the

amendments might need to accommodate them – noting we’re running short on time to reconsider the

drafting).

How does that sound to you?

Thanks

Marcus

Official Information Act 1982

From: Marcus Smith

Sent: Friday, 31 January 2025 12:23 pm

To: Mark Atwel <Mark.Atwel @comcom.govt.nz>

Subject: RE: Draft RIS for review: backdating 2019 reforms to section 99(1A) of the CCCFA

We’re sending them our paperwork today, but no idea how quickly we’l have an answer sorry Mark.

From: Mark Atwel <Mark.Atwel @comcom.govt.nz>

Sent: Friday, January 31, 2025 12:15 PM

2

To: Marcus Smith <[email address]>

Subject: RE: Draft RIS for review: backdating 2019 reforms to section 99(1A) of the CCCFA

Thanks Marcus. Appreciate your e orts. Yes, if you could ask Katrina that would be great.

From: Marcus Smith <[email address]>

Sent: Friday, 31 January 2025 12:06 pm

To: Mark Atwel <Mark.Atwel @comcom.govt.nz>

Subject: RE: Draft RIS for review: backdating 2019 reforms to section 99(1A) of the CCCFA

Kia ora Mark. You wouldn’t believe the process required to get legal privilege waived by CL. We’re quite far along in

trying for you though. Shal I ask Katrina for an indica on of when we might know?

Marcus

From: Mark Atwel <Mark.Atwel @comcom.govt.nz>

Sent: Friday, January 31, 2025 11:19 AM

To: Marcus Smith <[email address]>

Subject: RE: Draft RIS for review: backdating 2019 reforms to section 99(1A) of the CCCFA

Morena Marcus,

Just following up on whether MBIE has any further thoughts on whether the Commission is able to see a copy

of the Crown Law opinion.

Regards

Mark

Mark Atwel

Principal Adviser |Compe on, Fair Trading and Credit Branch

Commerce Commission | Te Komihana Tauhokohoko

Level 13, 55 Shortland Street | PO Box 105-222 | Auckland 1143 | New Zealand

DDI +64 (0)9 920 3492 | Mob s 9(2)(a)

| mark.atwel @comcom.govt.nz

www.comcom.govt.nz

Released under the

From: Marcus Smith <[email address]>

Sent: Monday, 23 December 2024 1:09 pm

To: Mark Atwel <Mark.Atwel @comcom.govt.nz>

Cc: Katrina Melvil e <Katrina.Melvil [email address]>; Glen Hildreth <[email address]>; Michel e Schulz

<Michel [email address]>; Nelson Curry <[email address]>; [email address]; Alice

Jackson <[email address]>; Sarah Bartlett <[email address]>; Lachlan Cartwright

<[email address]>; Jil Pitches <Jil .[email address]>; Caroline Andic

<[email address]>

Official Information Act 1982

Subject: RE: Draft RIS for review: backdating 2019 reforms to section 99(1A) of the CCCFA

Kia ora Mark,

Many thanks for ge ng us these comments so smartly. A ached are some responses to show what I’m proposing to

do with them. There wil likely be more opportuni es to adjust details through January and February where we need

to.

3

When Katrina’s back next year, I’l find out whether there is any prospect of Crown Law waiving legal privilege for

Crown en es. It may be worth us discussing what value that would add to your input, but I’l come back to you on

this.

Ngā mihi nui

Marcus

From: Mark Atwel <Mark.Atwel @comcom.govt.nz>

Sent: Friday, December 20, 2024 1:51 PM

To: Marcus Smith <[email address]>

Cc: Katrina Melvil e <Katrina.Melvil [email address]>; Glen Hildreth <[email address]>; Michel e Schulz

<Michel [email address]>; Nelson Curry <[email address]>; [email address]; Alice

Jackson <[email address]>; Sarah Bartlett <[email address]>; Lachlan Cartwright

<[email address]>; Jil Pitches <Jil .[email address]>; Caroline Andic

<[email address]>

Subject: RE: Draft RIS for review: backdating 2019 reforms to section 99(1A) of the CCCFA

Kia ora Marcus,

Thank you for the opportunity to comment on the latest draft of the s99(1A) RIS.

I attach the RIS with Commission comments.

A couple of key points to highlight from our perspective:

Paragraph 61 – We request that the sentence referring to the Commission informing parties a ected

by the proposal be deleted. We do not see that the Commission has a role here.

Paragraph 62 – The last sentence provides “We wil work with the Commission to manage any impact of

the policy change on these se lements”. We request that the words “on these se lements” be deleted in

order not to create the impression that exis ng se lements are affected more than we believe they are. On

that note, in order to help us consider the impact of any proposed change on the Commission as well as

supporting us to provide more well-informed comments on the RIS it would assist if we could see a

copy of the legal advice MBIE has obtained from the Crown Law Office s 9(2)(h)

Finally, we note that the bullet point comments in our cover email providing feedback to MBIE on an earlier

Released under the

draft of the RIS continue remain relevant (further copy of email 29 October 2024 attached).

Regards

Mark

Mark Atwel

Principal Adviser |Compe on, Fair Trading and Credit Branch

Official Information Act 1982

Commerce Commission | Te Komihana Tauhokohoko

Level 13, 55 Shortland Street | PO Box 105-222 | Auckland 1143 | New Zealand

DDI +64 (0)9 920 3492 | Mob s 9(2)(a)

| mark.atwel @comcom.govt.nz

www.comcom.govt.nz

From: Marcus Smith <[email address]>

Sent: Wednesday, 11 December 2024 10:32 am

To: Nelson Curry <[email address]>; [email address]; Alice Jackson

<[email address]>; Sarah Bartlett <[email address]>; Lachlan Cartwright

4

<[email address]>; Jil Pitches <Jil .[email address]>; Mark Atwel

<Mark.Atwel @comcom.govt.nz>; [email address]; Mark Holden <[email address]>

Cc: Katrina Melvil e <Katrina.Melvil [email address]>; Glen Hildreth <[email address]>; Michel e Schulz

<Michel [email address]>

Subject: Draft RIS for review: backdating 2019 reforms to section 99(1A) of the CCCFA

Kia ora koutou,

As foreshadowed, I’m seeking feedback on the latest dra of our RIS proposing retrospec ve legisla ve change to

provide the courts with discre on over the effect of sec on 99(1A). Accep ng there wil be people coming and going

over the next few weeks, I’m not proposing a specific deadline for comment. I’l let you know once I have a date

confirmed for review by an MBIE RIS panel, but I’d say I’m unlikely to submit it this year. (I’m back at work on 6

January.) Comments before them would of course be welcome! FYI, I’m also ge ng more comments internal y.

I understand the Minister wil very shortly be seeking the A orney-General’s agreement to have this amendment

dra ed in advance of Cabinet approval (and agreed instead when the Bil proposed for introduc on is before

Cabinet). Failing that, the proposal would s l likely go to Cabinet early next year (and added to the Bil later).

A reminder this ma er is market sensi ve. Please handle with care.

Some things to note in terms of what has changed since the last dra :

Approach to defining the problem

My approach to defining the problem is a bit more limited than others have suggested. This reflects that:

The problem relates to a law that has since changed (i.e. been addressed by the 2019 reforms, in that ful

forfeiture can be avoided where it would be unjust/inequitable). Normal y the point of regulatory change is to

influence how regulated par es behave. Retrospec ve legisla on general y can’t do that. In this case, it’s not

clear how the historical law could influence how lenders make decisions about lending in the present unless it

changes their financial posi on (or they are so worried it wil that they act as if it has).

o Not a perfect analogy, but to try and capture what I’m proposing to ignore: Say there used to be site

hazard present in a building that has since been renovated and brought up to standard. The fact that

hazard used to exist shouldn’t affect (ra onal) wil ingness to enter the building. It’s a historical

wrong. If to regret an old policy (in this case da ng back to 2015) were a good enough reason to

erase it from legal history, retrospec ve legisla on would be commonplace.

The situa on we’re concerned about is where the court finds in the li ga on against ANZ and ASB that it is

bound to require ful forfeiture to affected customers. The reasons we’re concerned with it should be

Released under the

informed by the purposes of the CCCFA. If the losses to ANZ and ASB, or subsequently to any other lenders,

don’t have any implica ons for the future supply of credit or the interests of consumers, then they are not

problema c from a public policy perspec ve. They would just cons tute a transfer from the banks to their

customers (and transfers within an economy are neutral). So I’m focussing on the poten al indirect

consequences of that transfer in terms of impact on the market/consumers.

The indirect consequences of such a transfer depend on how large it is and how many lenders it could involve. For

the purposes of trying to quan fy it, I’m focussing on the poten al liability of ANZ and ASB, given the RBNZ

model ing is based on the facts applying to them. RBNZ advice is that smal er, domes c banks with greater reliance

Official Information Act 1982

on income from consumer lending would be worse affected by comparable liability. I emphasise this in our problem

defini on, but it does rely on having some sense for what scale of losses are possible in the event ful forfeiture is

required (to a subset of customers rela ng to a disclosure breach covering 1 – 4 years), and more is known about

what that would look like for ANZ and ASB.

We’re s l unsure (and therefore keen to test) whether ‘bank runs’ is a plausible consequence of the ful -forfeiture

scenario. I don’t see this as essen al to our problem defini on, but it would perhaps add some weight if it were a

plausible concern.

5

Choice of criteria

We’ve made some adjustments to these to ensure they work for the historical nature of the problem we’re trying to

address. For example, the concept of compliance costs is not par cularly meaningful here. We also con nue to think

it’s important the criteria enable us to analyse op ons against the legal conven ons/principles relevant to

retrospec ve legisla on (as strongly recommended by the LDAC guidelines and lawyers involved).

s 9(2)(h)

I’m happy to discuss any of this. Thanks in advance for your feedback.

Ngā mihi nui

Marcus

This email may contain information that is confidential or legally privileged. If you have received this email in error please

immediately notify the sender and delete the email, without using it in any way. The views presented in this email may not

be those of the Commission.

Released under the

Official Information Act 1982

6

From:

Mark Atwel <Mark.Atwel @comcom.govt.nz>

Sent:

Monday, 3 February 2025 4:53 pm

To:

Marcus Smith

Cc:

Sarah Bartlett; Jil Pitches; Cathrine McIntosh; Katrina Melvil e; Glen Hildreth

Subject:

CCCF Amendment Bil - Retrospective change - savings provision

Follow Up Flag:

Fol ow up

Flag Status:

Flagged

Kia ora Marcus

We have been considering the issue of whether the CCCF Amendment Bill needs to include some sort of

savings provision stating that the retrospective change to the e ect of s99(1A) doesn’t impact on existing

Commission settlements or enforceable undertakings. You raised this with us recently and we have come to

the view that it would be preferable for the Bill to contain a savings provision of this kind.

Our reasons include that not all the Commission settlements and enforceable undertakings are stated to be in

full and final settlement, and while they do contain provisions that reserve our rights and other protections

against breach by the lender, there is a risk that a lender could seek to challenge a settlement or enforceable

undertaking once retrospective application of ss95A and 95B comes into force. Our preference is to guard

against this risk.

We are happy to discuss these thoughts with you.

Regards

Mark

Mark Atwel

Principal Adviser |Compe on, Fair Trading and Credit Branch

Commerce Commission | Te Komihana Tauhokohoko

Level 13, 55 Shortland Street | PO Box 105-222 | Auckland 1143 | New Zealand

DDI +64 (0)9 920 3492 | Mob s 9(2)(a)

| mark.atwel @comcom.govt.nz

www.comcom.govt.nz

Released under the

This email may contain information that is confidential or legal y privileged. If you have received this email in error please

immediately notify the sender and delete the email, without using it in any way. The views presented in this email may not be

those of the Commission.

Official Information Act 1982

1

From:

Mark Atwel <Mark.Atwel @comcom.govt.nz>

Sent:

Monday, 3 February 2025 11:14 am

To:

Marcus Smith

Subject:

FW: Able to clarify?

Attachments:

2024-12-10 RIS for proposal to make discretion over effect of s99(1A) retrospective

- draft for Crown entities (5366966.2) - Marcus replies.docx

Follow Up Flag:

Fol ow up

Flag Status:

Flagged

Morena Marcus,

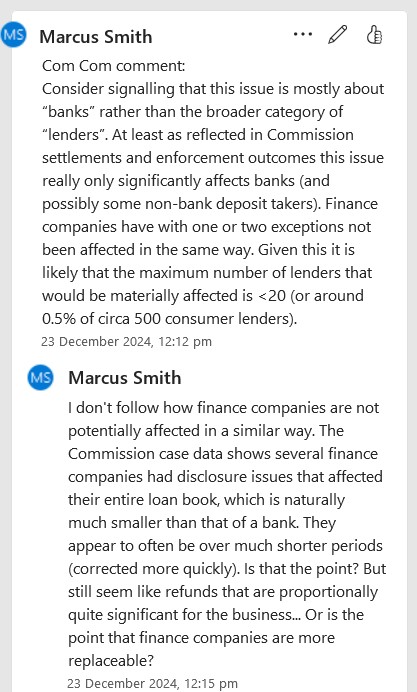

While both banks and finance companies are potentially impacted by section 99(1A) the Commission’s

experience is that a greater number of issues have arisen with banks as compared to finance companies.

The Commission has taken enforcement action against (settlements, warnings etc) or is currently

investigating s 9(2)(ba)(i)

In contrast, the Commission has taken enforcement action against 10 finance companies in relation

to disclosure errors out of a total population of more than 500 finance companies

Nearly all of the major banks have been investigated for agreed variation disclosure errors (s22)

whereas only one of the finance company enforcement outcomes relates to agreed variation (with the

other nine relating to s17 initial disclosure)

Some of the di erence in enforcement outcomes between banks and finance companies likely

reflects an increase willingness of banks as compared to finance companies to self-report errors to

the Commission but di erences in business models are likely relevant here also. Finance companies

often have a much smaller range of loan products and distribution channels (often just one) any

typically won’t do as many agreed variations (eg car loans are often one and done as compared to

home loans) making compliance more straight forward. Banks have a greater range of products,

methods of loan origination and variation, and are more likely to agree to loan variations (particularly

with home loans) making disclosure compliance more complicated and in the Commission’s

experience leading to an increased incidences of disclosure errors.

Regards

Released under the

Mark

Mark Atwel

Principal Adviser |Compe on, Fair Trading and Credit Branch

Commerce Commission | Te Komihana Tauhokohoko

Level 13, 55 Shortland Street | PO Box 105-222 | Auckland 1143 | New Zealand

DDI +64 (0)9 920 3492 | Mob s 9(2)(a)

| mark.atwel @comcom.govt.nz

Official Information Act 1982

www.comcom.govt.nz

From: Marcus Smith <[email address]>

Sent: Friday, 31 January 2025 2:33 pm

1

To: Mark Atwel <Mark.Atwel @comcom.govt.nz>

Subject: Able to clarify?

Kia ora anō Mark,

I’m s l fixing up the RIS (fol owing feedback through our internal RIA review panel process). Looking back at the

Commission comment below, are you able to help me understand what was meant?

Thanks

Marcus

Released under the

Official Information Act 1982

This email may contain information that is confidential or legally privileged. If you have received this email in error please

immediately notify the sender and delete the email, without using it in any way. The views presented in this email may not

be those of the Commission.

2

From:

Mark Atwel <Mark.Atwel @comcom.govt.nz>

Sent:

Friday, 24 January 2025 10:10 am

To:

Marcus Smith

Subject:

RE: Financial Services Reforms: draft RIS for comment - proposal to make discretion

over the effect of section 99(1A) retrospective [IN-CONF DENCE: RELEASE-

EXTERNAL]

Follow Up Flag:

Fol ow up

Flag Status:

Completed

Kia ora Marcus,

No problems - I’m happy to chat with you about this.

I have a meeting 11:00-12pm but otherwise I am free all day.

Cheers

Mark

Mark Atwel

Principal Adviser |Compe on, Fair Trading and Credit Branch

Commerce Commission | Te Komihana Tauhokohoko

Level 13, 55 Shortland Street | PO Box 105-222 | Auckland 1143 | New Zealand

DDI +64 (0)9 920 3492 | Mob s 9(2)(a)

| mark.atwel @comcom.govt.nz

www.comcom.govt.nz

From: Marcus Smith <[email address]>

Sent: Thursday, 23 January 2025 2:47 pm

To: Sarah Bartlett <[email address]>; Mark Atwel <Mark.Atwel @comcom.govt.nz>

Subject: RE: Financial Services Reforms: draft RIS for comment - proposal to make discretion over the effect of

section 99(1A) retrospective [IN-CONF DENCE: RELEASE-EXTERNAL]

Released under the

Kia ora kōrua,

Would it be possible to chat with one or more of you about the concern highlighted below? Hoping to be er

understand what it might mean for dra ing, ideal y in the next couple of days. Just when you can next spare 15 mins

or so please.

Thanks

Marcus

Official Information Act 1982

From: Sarah Bartlett <[email address]>

Sent: Tuesday, October 29, 2024 2:27 PM

To: Sal y Whineray Groom <Sal [email address]>; Andrew Royle <[email address]>;

Gwen Rashbrooke <[email address]>; Elena Obolonkina [TSY

<[email address]>; Owen McManamon <[email address]>;

Daryl.Col [email address]; Louis Campbel <Louis.Campbel [email address]>; Alice Jackson

<[email address]>; [email address]; Edwin Mitson <[email address]>; Victoria

Learmonth <[email address]>; Mark Atwel <Mark.Atwel @comcom.govt.nz>; James Sergeant

1

<[email address]>; Lachlan Cartwright <[email address]>; Debbie McLean

<[email address]>; Disee Anorpong [TSY <[email address]>; Mark Holden

<[email address]>; mary.l ewel [email address]; Michael Sherwood [TSY]

<[email address]>; Nelson Curry <[email address]>; Jil Pitches

<Jil .[email address]>; Kama Khairuzin [TSY] <[email address]>;

[email address]

Cc: Andrew Palmer <[email address]>; Katrina Melvil e <Katrina.Melvil [email address]>; Richard

Clough <[email address]>; Glen Hildreth <[email address]>; Tom Simcock

<[email address]>; Caroline Andic <[email address]>

Subject: RE: Financial Services Reforms: draft RIS for comment - proposal to make discretion over the effect of

section 99(1A) retrospective [IN-CONF DENCE: RELEASE-EXTERNAL]

Kia ora Sally

Thank you for the opportunity to comment on the draft RIS.

Jill has collated the Commission’s comments and included those in the attached version of the document. I

am just back from leave today so have also added in a few comments.

The key points from our perspective are the same as those included in our feedback on the draft briefing (the

team’s email of 8 October 2024):

Should retrospectivity be implemented, then it is important that any retrospective law change makes

clear that it does not undo or otherwise impact on any Commission settlements or other Commission

enforcement actions for disclosure failures covering the period June 2015 to December 2019, including

those where other banks (e.g. Kookmin, BNZ) made full repayment of costs of borrowing for disclosure

breaches.

We note the very real problem that any retrospective law change would effectively create a situation

where two different laws apply or have applied to lenders that may have engaged in the same or similar

conduct over similar periods, with one group of lenders who have relied on and complied with, or been

subject to enforcement outcomes consistent with, the current legislation, and others, who have not

complied but have not yet been subject to enforcement outcomes, who would be subject to the

proposed retrospective legislation, despite the harm to consumers being consistent across the

different periods. The retrospective effect would specifically advantage this second group of lenders

and disadvantage that group of consumers. We have a number of open investigations into lenders

following self-reports to the Commission of initial and agreed variation disclosure errors covering the

period June 2015 to December 2019 relating to tens of thousands of customers. We are working

Released under the

through these investigations and take a measured view of lender liability arising from disclosure

failures during this period. The announcement of potential retrospective law change would create real

uncertainty and could significantly complicate the timely progression and resolution of our

investigations and potential future remediation payments to consumers. Lenders may be less

incentivised to work with the Commission and agree an appropriate quantum. The issues will need to

be fully addressed by MBIE so as not to create problems for the Commission.

We stress again that the Commission is keen for the transfer of the enforcement function for the

CCCFA from the Commission to the FMA (and associated transfer of staffing and funding) to occur as

Official Information Act 1982

soon as possible. We would have concerns if the legislative time-frame for any retrospective change to

s95A meant a delay to the coming into effect of amendment legislation transferring the CCCFA

enforcement function.

Kind regards

Sarah

2

Sarah Bartle (she/her)

Director Credit

Compe on, Fair Trading and Credit

Commerce Commission | Te Komihana Tauhokohoko

44 The Terrace | PO Box 2351 | Wel ington 6140 | New Zealand

Mob s 9(2)(a)

| sarah.bartle @comcom.govt.nz

www.comcom.govt.nz

From: Sal y Whineray Groom <Sal [email address]>

Sent: Tuesday, 22 October 2024 5:31 pm

To: Andrew Royle <[email address]>; Gwen Rashbrooke <[email address]>;

Elena Obolonkina [TSY <[email address]>; Owen McManamon

<[email address]>; Daryl.Col [email address]; Louis Campbel

<Louis.Campbel [email address]>; Alice Jackson <[email address]>; [email address]; Edwin

Mitson <[email address]>; Victoria Learmonth <[email address]>; Mark Atwel

<Mark.Atwel @comcom.govt.nz>; Sarah Bartlett <[email address]>; Karla Reynolds

<[email address]>; James Sergeant <[email address]>; Lachlan Cartwright

<[email address]>; Debbie McLean <[email address]>; Disee Anorpong [TSY

<[email address]>; Mark Holden <[email address]>; Cathie Jenkins

<[email address]>; mary.l ewel [email address]; Michael Sherwood [TSY]

<[email address]>; Nelson Curry <[email address]>; Jil Pitches

<Jil .[email address]>; Kama Khairuzin [TSY] <[email address]>;

[email address]

Cc: Andrew Palmer <[email address]>; Katrina Melvil e <Katrina.Melvil [email address]>; Richard

Clough <[email address]>; Glen Hildreth <[email address]>; Tom Simcock

<[email address]>

Subject: Financial Services Reforms: draft RIS for comment - proposal to make discretion over the effect of section

99(1A) retrospective [IN-CONFIDENCE: RELEASE-EXTERNAL]

Kia ora koutou ComCom, FMA, RB, Treasury and Ministry of Regulation folk,

Please see attached a draft RIS for comment on options to give the courts explicit discretion over the effect

of section 99(1A) for the 2015-2019 period. This draft RIS is shared in strict confidence.

The Minister of Commerce and Consumer Affairs has not yet made a decision on the briefing that we sent

up on 10 October, but we are preparing this draft RIS in the event that he does decide he would like to

Released under the

seek a Cabinet decision.

We are not able to share legal advice that we have received that has informed the RIS as it’s subject to

legal professional privilege – you wil see that where this is referred to in the RIS that it has been deleted.

Please get your feedback back to me by COP Tuesday 29 October. I am available to discuss the draft RIS

tomorrow (Wednesday) and Thursday. I am on annual leave Friday and Tuesday.

Treasury – s 9(2)(ba)(i)

. Therefore, we haven’t included this

Official Information Act 1982

in the RIS yet.

I also want to try and get the RIS down to 10 pages or less…. so always keen for suggestions of where I

can condense content.

Ngā mihi,

Sal y Whineray Groom

Principal Policy Advisor, Consumer Policy Team

Building Resources and Markets Group

3

Ministry of Business, Innova on & Employment

sal [email address]

Waea/Telephone: +64 4 901 6191

Level 5, 15 Stout Street, Wel ington 6011

NZBN 9429000106078

This email may contain information that is confidential or legal y privileged. If you have received this email in error please

immediately notify the sender and delete the email, without using it in any way. The views presented in this email may not be

those of the Commission.

Released under the

Official Information Act 1982

4

From:

Mark Atwel <Mark.Atwel @comcom.govt.nz>

Sent:

Tuesday, 8 October 2024 4:35 pm

To:

Marcus Smith

Cc:

Katrina Melvil e; Glen Hildreth; Michel e Schulz; Sal y Whineray Groom;

[email address]; Alice Jackson; [email address];

[email address]; [email address];

[email address]; Sarah Bartlett; Karla Reynolds; James Sergeant;

Lachlan Cartwright; [email address];

[email address]; [email address]; mary.l ewel yn-

[email address]; Michael Sherwood [TSY]; [email address]; Jil

Pitches; James Barnett [TSY]; [email address]; Caroline Andic;

Andy Luck

Subject:

RE: For comment: Draft advice on historical problem with section 99(1A) of the

CCCFA

Attachments:

20241002 Briefing on s99(1A) historical issue - draft for agency feedback

(5287100.3).docx

Follow Up Flag:

Fol ow up

Flag Status:

Completed

Kia ora Marcus,

Thank you for the opportunity to comment on the draft briefing.

We attach Commission comments.

Key points from our perspective are:

The Commission has undertaken investigations into disclosure failures covering the period June 2015

to December 2019 and entered into settlements and/or enforceable undertakings with lenders or

arrived at other enforcement outcomes (e.g. judgments, warnings) based on the laws that applied

during that period. It is important that any retrospective law change makes clear that it does not undo

or otherwise impact on any Commission settlements or other Commission enforcement actions.

Released under the

Even where s99(1A) is not referenced in the relevant settlement, we consider that it has likely informed

both parties’ view of the appropriate quantum. Any retrospective law change would effectively create a

situation where two different laws apply or have applied to lenders that may have engaged in the same

or similar conduct over similar periods. Put another way, there would be one group of lenders who

have relied on and complied with, or been subject to enforcement outcomes consistent with, the

current legislation. Others, who have not complied but have not yet been subject to enforcement

outcomes, would be subject to the proposed retrospective legislation. The retrospective effect would

specifically advantage this second group. We have a number of open investigations into lenders

following self-reports to the Commission of initial and agreed variation disclosure errors covering the

Official Information Act 1982

period June 2015 to December 2019 relating to tens of thousands of customers. We are working

through these investigations and take a measured view of lender liability arising from disclosure

failures during this period. The announcement of potential retrospective law change would create real

uncertainty and could significantly complicate the timely progression and resolution of our

investigations and potential future remediation payments to consumers.

The Commission is keen for the transfer of the enforcement function for the CCCFA from the

Commission to the FMA (and associated transfer of staffing and funding) to occur as soon as possible.

We would have concerns if the legislative time-frame for any retrospective change to s95A meant a

1

delay to the coming into effect of amendment legislation transferring the CCCFA enforcement

function.

Regards

Mark

Mark Atwel

Principal Adviser |Compe on, Fair Trading and Credit Branch

Commerce Commission | Te Komihana Tauhokohoko

Level 13, 55 Shortland Street | PO Box 105-222 | Auckland 1143 | New Zealand

DDI +64 (0)9 920 3492 | Mob s 9(2)(a)

| mark.atwel @comcom.govt.nz

www.comcom.govt.nz

From: Marcus Smith <[email address]>

Sent: Thursday, October 3, 2024 9:29 AM

To: [email address]; Owen McManamon <[email address]>;

Daryl.Col [email address]; Alice Jackson <[email address]>; [email address];

[email address]; [email address]; [email address]; Mark Atwel

<Mark.Atwel @comcom.govt.nz>; Sarah Bartlett <[email address]>; Karla Reynolds

<[email address]>; Cathrine McIntosh <[email address]>; James Sergeant

<[email address]>; Lachlan Cartwright <[email address]>;

[email address]; [email address]; [email address]; Cathie Jenkins

<[email address]>; mary.l ewel [email address]; Michael Sherwood [TSY]

<[email address]>; [email address]; Jil Pitches <Jil .[email address]>;

James Barnett [TSY] <[email address]>; [email address]

Cc: Katrina Melvil e <Katrina.Melvil [email address]>; Glen Hildreth <[email address]>; Michel e Schulz

<Michel [email address]>; Sal y Whineray Groom <Sal [email address]>

Subject: For comment: Draft advice on historical problem with section 99(1A) of the CCCFA

Kia ora koutou,

As we’ve communicated in our regular updates, RBNZ has been doing model ing on the potential impacts of a class

action against ANZ and ASB and we’ve been aiming to get advice on this delivered to Minister Bayly next

Released under the

Wednesday, and forwarded to the Minister of Finance.

Please find a draft of this briefing attached for comment by 10am Tuesday 8 October. Please handle with care.

Explanation for timing: We are trying to get this considered while there is stil a prospect of having a proposal

included in the Cabinet paper currently planned for ECO on 6 November. But this is a complex issue, and we want to

ensure agencies have time to contribute expertise and perspectives. Please let me know if you think this balance off

and we can discuss with our Minister’s office.

Official Information Act 1982

RBNZ model ing: The briefing attempts to summarise the conclusions from RBNZ’s model ing (for your feedback

please RBNZ). I’l leave RBNZ to forward on their paper to others as appropriate.

Nature of input we’re seeking: You’l see a number of questions we’d appreciate CoFR agencies’ help with, but of

course welcome any other feedback/views. This is stil a relatively early draft, and we may end up with less

background in the briefing we deliver. So your time is best spent focussing on the substance of the advice and

analysis, rather than structure or presentation. If you’re comfortable looping in other recipients when providing

comments, that might assist with overal visibility. I see this as one for CoFR agencies to col aborate on. I’d also be

open to arranging a time for us on to discuss on Monday next week.

2

Any concerns or questions, please let me know.

With thanks in advance for your thoughts,

nāku noa, nā

Marcus

This email may contain information that is confidential or legal y privileged. If you have received this email in error please

immediately notify the sender and delete the email, without using it in any way. The views presented in this email may not be

those of the Commission.

Released under the

Official Information Act 1982

3

From:

James Barnett [TSY] <[email address]>

Sent:

Thursday, 7 November 2024 1:50 pm

To:

Sal y Whineray Groom; Kama Khairuzin [TSY]; Disee Anorpong [TSY]; Marcus Smith

Subject:

RE: Financial Services Reforms: draft RIS for comment - proposal to make discretion

over the effect of section 99(1A) retrospective [IN-CONFIDENCE: RELEASE-

EXTERNAL] [IN-CONF D

s ENCE]

Follow Up Flag:

Fol ow up

Flag Status:

Completed

Hi Sal y,

We checked in with the office and MoF only received it last night. If it makes the weekend bag, then you may hear

early next week, but as you say she is very busy.

We can’t do much more than ask the office as above, sorry! If you don’t hear back by say Tuesday/Wednesday next

week let me know and I can ask again.

Thanks,

James

From: Sal y Whineray Groom <Sal [email address]>

Sent: Thursday, November 7, 2024 9:30 AM

To: Kama Khairuzin [TSY] <[email address]>; Disee Anorpong [TSY]

<[email address]>; Marcus Smith <[email address]>

Cc: James Barnett [TSY] <[email address]>

Subject: RE: Financial Services Reforms: draft RIS for comment - proposal to make discretion over the effect of

section 99(1A) retrospective [IN-CONFIDENCE: RELEASE-EXTERNAL] [IN-CONF DENCE]

Thank you Kama, we have heard MOF is stil considering this. Is there any way Treasury could help move

this up her list of things to look at? Appreciate she is very busy…

Given she’s stil considering this, we haven’t sent the RIS to the panel. My col eague Marcus wil consider

Released under the

your comments.

Regards, Sal y

From: Kama Khairuzin [TSY] <[email address]>

Sent: Tuesday, October 29, 2024 5:01 PM

To: Sal y Whineray Groom <Sal [email address]>; Disee Anorpong [TSY]

<[email address]>

Cc: James Barnett [TSY] <[email address]>

Official Information Act 1982

Subject: RE: Financial Services Reforms: draft RIS for comment - proposal to make discretion over the effect of

section 99(1A) retrospective [IN-CONF DENCE: RELEASE-EXTERNAL] [IN-CONF DENCE]

[IN-CONF DENCE]

Kia ora Sal y,

Thank you for sending through the dra RIS.

1

We an cipate that MBIE wil consult both Crown Law and LDAC on the proposal, par cularly as op on 2 (which wil

interfere with ac ve li ga on) is stated to be the preferred op on. We note that certain legal advice has been

redacted from the paper under the “Legal principles” heading (currently at para 55) – so am uncertain whether such

consulta on has already taken place. We are sure MBIE’s Legisla on team are al over it in any event.

Do let us know if you have any updates from your private sec regarding Min Bayly’s mee ng with MoF and if you

have s 9(2)(ba)(i)

We also agree with Sarah’s comment on ensuring this doesn’t distract from the transi on from ComCom to FMA –

as that’d get very messy (financial y) very quickly!

On the distribu on list – Elena Obolonkina, Mary Llewel yn-Fowler, and Michael Sherwood does not need to be on

the list anymore.

Many thanks,

Kama

From: Sarah Bartlett <[email address]>

Sent: Tuesday, October 29, 2024 2:27 PM

To: Sal y Whineray <Sal [email address]>; ^Regulation: Andrew Royle

<[email address]>; Gwen Rashbrooke <[email address]>; Elena

Obolonkina [TSY] <[email address]>; Owen McManamon

<[email address]>; Daryl Col ins <Daryl.Col [email address]>; Louis Campbel

<Louis.Campbel [email address]>; Alice Jackson <[email address]>; [email address]; Edwin

Mitson <[email address]>; ^RB: Victoria Learmonth <[email address]>; Mark Atwel

<Mark.Atwel @comcom.govt.nz>; James Sergeant <[email address]>; Lachlan Cartwright

<[email address]>; Debbie McLean <[email address]>; Disee Anorpong [TSY]

<[email address]>; Mark Holden <[email address]>; Mary Llewel yn-Fowler [TSY]

<Mary.Llewel [email address]>; Michael Sherwood [TSY] <[email address]>;

Nelson Curry <[email address]>; Jil Pitches <Jil .[email address]>; Kama Khairuzin [TSY]

<[email address]>; Ben Temple <[email address]>

Cc: Andrew Palmer <[email address]>; Katrina Melvil e <Katrina.Melvil [email address]>; Richard

Clough <[email address]>; Glen Hildreth <[email address]>; Tom Simcock

<[email address]>; Caroline Andic <[email address]>

Subject: RE: Financial Services Reforms: draft RIS for comment - proposal to make discretion over the effect of

section 99(1A) retrospective [IN-CONF DENCE: RELEASE-EXTERNAL]

Released under the

Kia ora Sally

Thank you for the opportunity to comment on the draft RIS.

Jill has collated the Commission’s comments and included those in the attached version of the document. I

am just back from leave today so have also added in a few comments.

The key points from our perspective are the same as those included in our feedback on the draft briefing (the

Official Information Act 1982

team’s email of 8 October 2024):

Should retrospectivity be implemented, then it is important that any retrospective law change makes

clear that it does not undo or otherwise impact on any Commission settlements or other Commission

enforcement actions for disclosure failures covering the period June 2015 to December 2019, including

those where other banks (e.g. Kookmin, BNZ) made full repayment of costs of borrowing for disclosure

breaches.

We note the very real problem that any retrospective law change would effectively create a situation

where two different laws apply or have applied to lenders that may have engaged in the same or similar

2

conduct over similar periods, with one group of lenders who have relied on and complied with, or been

subject to enforcement outcomes consistent with, the current legislation, and others, who have not

complied but have not yet been subject to enforcement outcomes, who would be subject to the

proposed retrospective legislation, despite the harm to consumers being consistent across the

different periods. The retrospective effect would specifically advantage this second group of lenders

and disadvantage that group of consumers. We have a number of open investigations into lenders

following self-reports to the Commission of initial and agreed variation disclosure errors covering the

period June 2015 to December 2019 relating to tens of thousands of customers. We are working

through these investigations and take a measured view of lender liability arising from disclosure

failures during this period. The announcement of potential retrospective law change would create real