LOWER NORTH ISLAND LONGER-DISTANCE

ROLLING STOCK BUSINESS CASE

PREPARED FOR GREATER WELLINGTON REGIONAL COUNCIL

26 September 2019

1987

under LGOIMA,

Released

link to page 2

All redactions are made under

s 7(2)(i) of the LGOIMA, 1987

QUALITY STATEMENT

PROJECT MANAGER

PROJECT TECHNICAL LEAD

Doug Weir

Doug Weir

PREPARED BY

Doug Weir, Andrew Liese

………………………………...............

26/09/19

CHECKED BY

Jamie Whittaker, Doug Weir, Deepa Seares ………………………………...............

26/09/19

1987

REVIEWED BY

Jamie Whittaker, Phil Peet

………………………………...............

26/09/19

APPROVED FOR ISSUE BY

Doug Weir

………………………………...............

26/09/19

LGOIMA,

WELLINGTON

Level 13, 80 The Terrace, Wel ington 6011

PO Box 13-052, Armagh, Christchurch 8141

TEL +64 4 381 6700

under

REVISION SCHEDULE

Authorisation

Rev

No.

Date

Description

Prepared

Checked

Reviewed Approved

by

by

by

by

Released

1

27/07/18 First Draft Final

DW, AL

JW

JW

DW

2

24/10/18 Updated First Draft Final

DW

JW

JW

DW

3

05/08/19 Revised Draft Final (Sustainable

Transport Committee)

DW

DW

PP

DW

3

20/08/19 Updated Revised Draft Final

DW

DS

PP

DW

4

26/09/19 Amended Draft Final

DW

DW

PP

DW

Stantec │ Lower North Island Longer-Distance Rolling Stock Business Case │ 26 September 2019

Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rol ing Stock Business Case -

Amended Draft Final.docx

Executive Summary

Introduction This business case has been prepared by Stantec New Zealand and Greater Wellington Regional Council

(GWRC), with input from key stakeholders including KiwiRail, Transdev, Horizons Regional Council and the

NZ Transport Agency (NZTA), and economic peer review by Transport Futures Limited. It assesses the case

for replacing the rol ing stock fleets that provide longer-distance rail passenger services on the Wairarapa

and Manawatu lines, and using the replacement fleet to improve service levels and increase the overal

capacity of GWRC’s Metlink rail network to address serious and urgent capacity constraints. It follows a

2017 business case that assessed the case for continued short-term public investment in the Palmerston

North-Wellington rail passenger service, and two 2017 infrastructure-focused business cases that assessed

the case for catch-up track renewals and capacity and resilience enhancements on the Wel ington metro

rail network, which includes the Wairarapa Line and the southern end of the Manawatu Line. These will

be supported by and incorporated into a new Wellington Regional Rail Plan (WRRP), which is currently

under development.

Background

1987

The Wairarapa and Manawatu lines are an established, integral and wel -utilised component of the lower

North Island transport system. They serve areas that are experiencing significant ongoing population

growth, which is forecast to continue in the future, and the longer-distance services that operate on the

lines fulfil very important transport system access and capacity roles.

The Wairarapa Line links Masterton and Wellington. It is one of only two transport links between the

Wairarapa sub-region and the rest of the Wel ington region, and it has a critical role connecting Wairarapa

residents to many employment, educational and other opportunities and services that are not available

locally. Its direct route under the Remutaka Range is safer, more efficient and more resilient than paral el

State Highway 2, which crosses the range via a steep, winding and narrow route that is very busy at peak

times and has a high crash risk, low average speed and susceptibility to weather-related closure. Rail

LGOIMA,

passenger services on the line consequently have an important road substitute role and a high mode

share of commuting trips, including a very high 60% share of trips to the Wellington CBD, which is around

half of the journey to work trips between Wairarapa and the entire Wel ington region. This provides

consequent congestion, parking and environmental benefits in the Hutt Val ey and Wel ington city.

Wairarapa Line services also provide access and vital extra capacity to supplement the electrified metro

rail services in the Hutt Val ey, where they are an integral part of the rail service offering.

under

The Wairarapa Line is operated as part of the Metlink public transport network. It is currently served by

three peak direction services in each weekday peak, two weekday off-peak services in each direction, an

additional service in each direction on Friday nights, and two in each direction on weekend days. These

carried approximately 625,000 peak passengers and 154,000 off-peak passengers in the 2019 financial

year. Peak services are close to capacity, and changes were made to carriage allocation to provide

short term relief on the most-crowded afternoon service in April 2019. Further options to improve asset

utilisation are being investigated but are limited.

Wairarapa Line services are provided by a mixed fleet of conventional locomotive-hauled rolling stock

consisting of two types of rebuilt ex-British Rail carriages that date from the 1970s. GWRC is about to

Released

commence a light mid-life refurbishment of both types, which wil extend the carriages’ life to the mid-

2020s. This could be expanded to al ow the fleets to remain in service for a longer period if required. All

carriages will be life-expired and require replacement by 2032.

The Manawatu Line links Palmerston North and Wellington. It serves a large catchment in the northwest of

the Wellington region and south of the Horizons region, and connects residents to many employment,

educational and other opportunities and services that are not available elsewhere on the corridor.

Services also provide vital extra capacity to supplement the electrified metro rail services south of

Waikanae. The line parallels State Highway 1 for much of its length, which carries large traffic volumes and

is geographical y constrained, making it vulnerable to congestion and resilience events. The road is

currently being upgraded to expressway to north of Otaki, which is expected to both al eviate these

problems along some of the corridor in the short to medium term and increase population and general

transport demand on the corridor.

The Manawatu Line is currently served by the Capital Connection, a weekday commuter train operated

by KiwiRail, which runs a single peak direction service in each weekday peak. This carried approximately

Stantec │ Lower North Island Longer-Distance Rolling Stock Business Case │ 26 September 2019

Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rol ing Stock Business Case -

Amended Draft Final.docx │ Page i

134,000 passengers in the 2019 financial year and is increasingly operating at capacity on some days of

the week. Capacity is constrained by rol ing stock availability and cannot be increased.

Manawatu Line services are provided by a fleet of conventional locomotive-hauled rolling stock, similarly

to the Wairarapa Line. Although the Manawatu Line carriages were rebuilt from the same 1970’s-era ex

British Rail carriage source as the Wairarapa Line carriages, they differ from and are incompatible with

them. Critical y, the carriages are close to the end of their service life and require either extensive

refurbishment or replacement prior to mid-2021 to enable continued operation of services after that point.

A decision on whether to proceed with refurbishment wil be required within six months.

Regional and National Context Investment in longer-distance rail passenger rol ing stock, and reliability, capacity, frequency and journey

time improvements is foreshadowed and supported by Wel ington and Horizons transport plans and

supported by spatial planning and regional economic development programmes in both regions.

Regional Land Transport Plans (RLTPs) are especial y relevant as they provide the strategic context and

investment programme for land transport (including public transport) in each region. Both RLTPs prioritise

investment in the improvements noted in this business case. Both RLTPs are also due for review, which is

timely as this business case can be used to confirm the investment programme for rail long distance rail in

both regions.

1987

Regional Public Transport Plans (RPTPs) are also integral to this discussion. The existing Wellington RPTP sets

out the key elements of the existing WRRP, including Rail Scenario 1 with a focus on unlocking capacity

across the network. This business case builds on current initiatives and foreshadows longer term ideas and

plans to increase supply. As with the reviews of RLTPs, the current review of the WRRP and upcoming

reviews of both RPTPs provide an ideal opportunity to set out the key delivery components of this business

case in much greater detail.

Investment in improvements is consistent with the NZTA’s strategic view and investment priorities for each

corridor in both regions, where the rail modal option is seen as being an important component of the multi-

modal transport mix. It is also consistent with the Government’s higher-level land transport priorities as

LGOIMA,

expressed in the Government Policy Statement on Land Transport, addressing objectives associated with

the key ‘Access’ strategic priority, which commits to increased investment in urban and inter-regional

public transport in both peak and off-peak periods, and the supporting ‘Environment’ strategic priority,

which commits to increased investment in lower emission modes of transport such as public transport.

Investment in longer-distance rol ing stock and services achieves these objectives by enhancing

connectivity, capacity, reliability and resilience at several critical points on the network, on existing

commuter rail services that support housing and employment and, in the case of the Wairarapa Line, are

under

close to capacity. Investment in rail services that are at capacity or support housing and employment is a

specific GPS focus.

Investment in improvements is also likely to meet al key requirements for the Provincial Growth Fund (PGF),

including sustainable economic development, social inclusion and participation, climate change and

environmental sustainability, and resilience objectives. The Horizons Region and Wairarapa and Kapiti

areas of the Wel ington Region are eligible for PGF funding.

Problem Definition A stakeholder assessment at an October 2017 workshop found that there are three clear problems

Released

associated with the existing longer-distance rail rol ing stock fleet, which need to be addressed with some

urgency. These relate to train condition, fleet capacity, and operational (in)efficiencies.

Train Condition

All existing longer-distance rail rol ing stock dates from either the early 1970s (carriages) or late 1970s

(luggage / generator vans). Although al have been subsequently rebuilt to varying degrees and are

equipped to current amenity and safety standards, the bulk of the fleet is now approaching 50 years in

age and nearing the end of its service life.

The Manawatu Line carriages are of most concern. These have been in continuous post-rebuild service for

nearly 20 years and increasing age-related maintenance costs are reflected in a current

mil ion short-

term funding gap. The carriages wil either require full refurbishment at an estimated cost of

million,

replacement, or withdrawal from service prior to mid-2021. This timeframe places some urgency on an

investment decision and subsequent implementation of the chosen option.

The Wairarapa Line carriages are less of an immediate concern. However, they are looking increasingly

tired due to their heavy use, are increasingly unable to cope with demand, and several components are

Stantec │ Lower North Island Longer-Distance Rolling Stock Business Case │ 26 September 2019

Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rol ing Stock Business Case -

Amended Draft Final.docx │ Page ii

link to page 5

approaching end of life. GWRC is about to commence a light mid-life refurbishment, which wil enable

them to continue operating until the mid-2020s as previously noted, but a more extensive refurbishment to

enable them to operate until 2032 wil be avoided if they are replaced at that point.

Fleet Capacity

Wairarapa Line patronage has grown substantial y over the last decade, increasing by 15% to 780,000

boardings in the decade ending in the 2019 financial year. Peak patronage increased by 24% over the

same period, and it has been close to or greater than seated capacity over much of the decade, despite

the introduction of additional capacity in 2013.

Figure 1-1 shows that peak services are again

approaching seated capacity and indicates that crowding can be expected to become an increasing

problem unless significant capacity improvements are made to cater for future demand, particularly if the

recent four-year average annual peak growth rate of 3.3% is sustained. This rate is well above the current

forecast.

Current

Seated Capacity

Forecast

Population (1.3%)

Recent (3.3%)

2,400

1987

nage

2,200

atro

2,000

1,800

eak P

1,600

ing P

rn

1,400

1,200

1,000

LGOIMA,

ge Daily Mo

800

vera

600

400

pa Line A

ra

200

under

aira

0

W

09

14

19

24

29

34

39

Jun-

Jun-

Jun-

Jun-

Jun-

Jun-

Jun-

Figure 1-1: Wairarapa Line morning peak patronage and projected demand

Manawatu Line patronage fluctuated over the decade ending in the 2019 financial year, reflecting the

Released

impact of electrification of the Paraparaumu-Waikanae section of the Kapiti Line in early 2011, the existing

service’s low frequency, worn rol ing stock and uncertain future, and fare increases necessitated by its

commercial nature. However, traffic congestion and increased urban development and population

growth are again driving strong patronage growth, resulting a recent four-year average annual growth

rate of 3.1%. The existing service carried 136,000 passengers in the 2019 financial year and is increasingly

operating at capacity on some days.

Patronage on the electrified Hutt, Johnsonvil e and Kapiti Lines has grown substantial y over the last

decade, similarly to the Wairarapa Line, increasing by 21% to 13.5 mil ion boardings in the 2019 financial

year. This growth reflects population growth on the corridors that the lines serve, and investment in

improvements in infrastructure, rol ing stock and services that have improved service quality, frequency

and reliability, including the complete replacement of the previous obsolete electric fleet by the new

Matangi fleet between 2010 and 2016.

Electrified area patronage growth has been most significant at the peak, with Hutt Line, Johnsonvil e Line,

and Kapiti Line average daily morning peak patronage increasing by 16%, 11% and 29% respectively

Stantec │ Lower North Island Longer-Distance Rolling Stock Business Case │ 26 September 2019

Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rol ing Stock Business Case -

Amended Draft Final.docx │ Page iii

link to page 6 link to page 7

between mid-2009 and mid-2019.

Figure 1-2 shows that the peak period increase has been most acute

since mid-2015, reflecting similar trends to the Wairarapa and Manawatu lines since that point, and it

indicates that capacity improvements are likely to be required to cater for future demand, particularly if

recent the recent four-year average annual peak growth rate of 5.5% is sustained. This rate is well above

forecast.

Current

Seated Capacity

Forecast (with LGWM)

Population (1.0%)

Recent (5.5%)

45,000

nage 40,000

atro 35,000

eak P

30,000

ing P

orn 25,000

1987

20,000

ge Daily M 15,000

vera

a A 10,000

5,000

LGOIMA,

0

Electrified Are

09

14

19

24

29

34

39

Jun-

Jun-

Jun-

Jun-

Jun-

Jun-

Jun-

Figure 1-2: Electrified area morning peak patronage and projected demand

under

Figure 1-3 shows that the capacity issue is particularly acute between 7:30 and 8:30, where ideal capacity

could be exceeded by 2024, and standing capacity by 2029, if there are no further initiatives beyond

proposed RS1 timetable changes, which wil maximise utilisation of the Matangi fleet once associated

infrastructure is in place. This wil require additional peak capacity if crowding and mode shift away from

public transport is to be avoided.

Rolling stock lead times place urgency on resolution of this problem, but a small metro EMU order is

expected to be unattractive to rol ing stock manufacturers. However, there is an opportunity to address

this capacity issue efficiently and promptly through resolution of the longer-distance capacity issue, since

Released

longer-distance services are an integral part of the metro service offering and are already used to provide

much needed capacity within the electrified area.

Stantec │ Lower North Island Longer-Distance Rol ing Stock Business Case │ 26 September 2019

Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rol ing Stock Business Case -

Amended Draft Final.docx │ Page iv

link to page 7

Seated Capacity

Ideal Capacity

Standing Capacity

Forecast (with LGWM)

Current - All (5.7%)

Current - Peak (7.3%)

18,000

30 16,000

o 8:

30 t 14,000

12,000

eekdays 7: 10,000

als -W 8,000

rriv 6,000

n A

Change

4,000

able

1987

et

im

2,000

gton Statio

1 T

RS

ellin

0

W

19

24

29

34

39

Jun-

Jun-

Jun-

Jun-

Jun-

Figure 1-3: Projected Wel ington Station morning peak hour demand and capacity (al Metlink lines)

LGOIMA,

Operational Efficiencies

The Wairarapa and Manawatu lines are run as separate operations, which is inflexible and inefficient.

There is no ability to manage operations between the two lines, nor is there the ability to manage rol ing

stock fleet al ocation and maintenance in an effective way. Maintenance is further complicated by a

complex set of contractual relationships. under

The mixed rolling stock fleet of three different and incompatible carriage types across the two lines is also

an issue. This limits interoperability and does not provide the economies of scale that might be available if

the fleet was composed of a single type.

Existing services on both lines are locomotive hauled and consequently expensive to operate. The

locomotives require special safety features that limits the pool that are available run services, which in turn

necessitates extras to provide redundancy to cover failures, increasing fleet requirements. The locomotive

hire cost is consequently a sizeable proportion of the cost of running services on both lines and the cost of

providing additional services is therefore high.

Released

Locomotive-hauled trains are also very operational y limiting. They require long turnaround times that are a

considerable constraint, particularly in Wellington where there is conflict with other services that limits the

efficient operation of al services at peak times, and they are consequently a barrier to frequency

enhancements that might otherwise help to address capacity issues. The locomotive turning requirement

also necessitates that two locomotives must be used instead of one when a train runs for only part of a

line’s length, which has consequent cost impacts.

Benefits of Investment A stakeholder assessment found that investing to address the problems is expected to provide four major

benefits: enhanced regional connectivity, improved rail service quality, a more resilient transport network,

and investment value for money. These benefits link closely to the objectives of key central and local

government strategies and plans, and provide strategic justification for investing in a rolling stock solution,

as summarised in

Table 1-1. Table 1-1: Links between investment benefits and relevant strategies and plans

Stantec │ Lower North Island Longer-Distance Rolling Stock Business Case │ 26 September 2019

Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rol ing Stock Business Case -

Amended Draft Final.docx │ Page v

link to page 9 link to page 7

Enhanced

Improved

More

Value for

Regional

Rail Service

Resilient

Money

Connectivity Quality

Transport

Network

Wellington Regional Rail Plan

Wel ington Regional Public Transport Plan

Wel ington Regional Land Transport Plan

Wairarapa Economic Development Strat

Horizons Regional Public Transport Plan

Horizons Regional Land Transport Plan

Horizons Accelerate25 Growth Programme

NZTA Long Term Strategic View

1987

NZTA Investment Proposal

Govt Policy Statement on Land Transport

Provincial Growth Fund

Enhanced Regional Connectivity

Investment wil maintain existing connectivity into the future and then further strengthen it if used to

improve capacity and service levels in the growth areas served by the two lines. This wil improve liveability

LGOIMA,

and quality of life and help to drive local economic activity and growth in the areas served by them, as

identified in the regional economic development plans. Additional capacity wil also strengthen the

capacity of Metlink’s core electrified rail corridors by providing additional capacity and travel options at

key stations, helping to manage connectivity on those lines as demand increases.

Improved Rail Service Quality

Investment wil ensure that the services remain running and running reliably into the future, that they can

under

cope with current and ongoing growth, and that they remain attractive to and a preferred choice for

users, the majority of whom spend two to four hours a day travelling by train.

More Resilient Transport Network

Investment wil offer transport system-level resilience benefits by providing a modal and route alternative to

the road network, and public transport network-level resilience benefits by utilising a different power

source from the electrified network if the chosen option does not solely rely on an overhead power source.

This benefit wil be enhanced if the fleet can be managed between the two lines to al ow resilience-

related capacity issues to be managed.

Released

Value for Money

Direct value for money benefits from investment are likely to come from the elimination of some impending

heavy maintenance, maintenance and operational economies of scale, and if chosen in an option, from

replacement of locomotive haulage with a more-efficient motive power source. These would al ow the

same level of service to be provided at lower cost, or more service to be provided at the same level of

investment, with either scenario providing better value for money than at present.

Value for money will also be provided at the public transport network level, by al owing patronage growth

to be accommodated without requiring other additional capacity, and transport system level, by al owing

transport system growth to be accommodated without additional road capacity.

Figure 1-4 shows how

investment in an expanded longer-distance rol ing stock fleet and associated services might address the

morning peak hour capacity issue shown in

Figure 1-3, delaying the requirement for additional EMU

capacity until the Matangi fleet is replaced and so offering network level value for money.

Stantec │ Lower North Island Longer-Distance Rolling Stock Business Case │ 26 September 2019

Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rol ing Stock Business Case -

Amended Draft Final.docx │ Page vi

link to page 10

Seated Capacity (with LD)

Ideal Capacity (with LD)

Standing Capacity (with LD)

Forecast (with LGWM)

Current - All (5.7%)

Current - Peak (7.3%)

30 18,000

o 8: 16,000

30 t

14,000

eekdays 7: 12,000

10,000

als -W

pact

rriv

8,000

n A

6,000

Change

1987

4,000

able

et

gton Statio

im

2,000

ellin

1 T

ling stock capacity im

W

RS

Ro

0

19

24

29

34

39

Jun-

Jun-

Jun-

Jun-

Jun-

LGOIMA,

Figure 1-4: Projected Wel ington Station morning peak hour demand and extra capacity (al Metlink lines)

Finally, value for money may be gained from joint procurement of a replacement fleet with other regions

and/or the ability the use a new Wellington fleet to run trials in other parts of the country.

Option Selection

under

Six investment options have been identified from a long list of sixteen potential mode/fleet and nine

potential service level responses by stakeholders. These are:

•

Option 1: maintain the existing Wairarapa Line fleet and services and al ow Manawatu Line services to

cease operating (the do-minimum option);

•

Option 2: improve the Wairarapa Line fleet and service levels by purchasing additional used rol ing

stock and maintain the existing Manawatu Line fleet and service levels (the enhanced status quo

option);

•

Option 3: electrify to Featherston and Otaki, extend electric multiple unit (EMU) operations to those

Released

points and improve service levels, with bus connections from outer points;

•

Option 4: replace existing fleets with a diesel multiple unit (DMU) fleet at the earliest opportunity and

improve service levels;

•

Option 5: replace existing fleets with a dual-mode multiple unit (DMMU) fleet at the earliest opportunity

and improve service levels; and

•

Option 6: electrify to Masterton and Palmerston North, extend EMU operations to those points at

earliest opportunity and improve service levels.

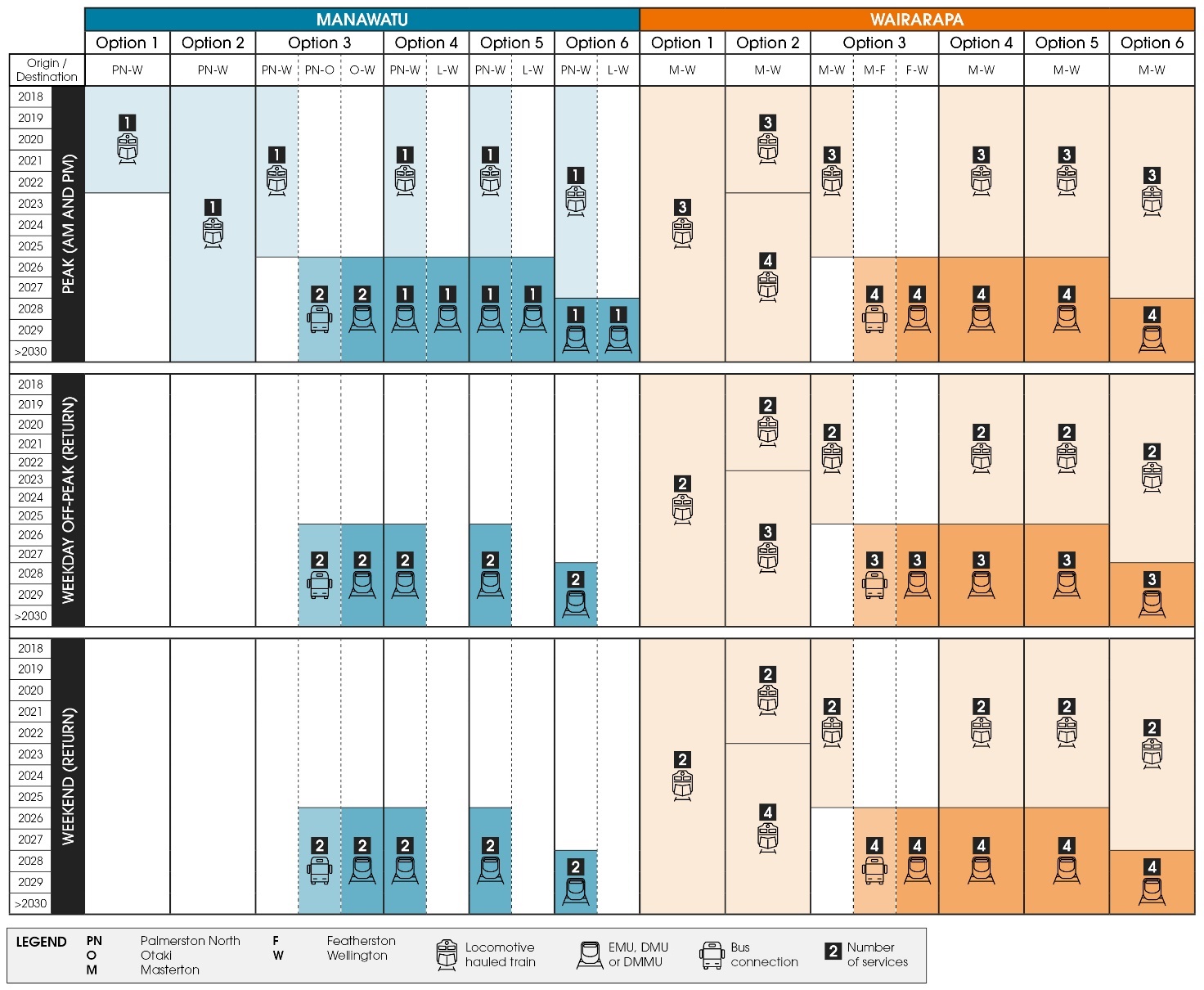

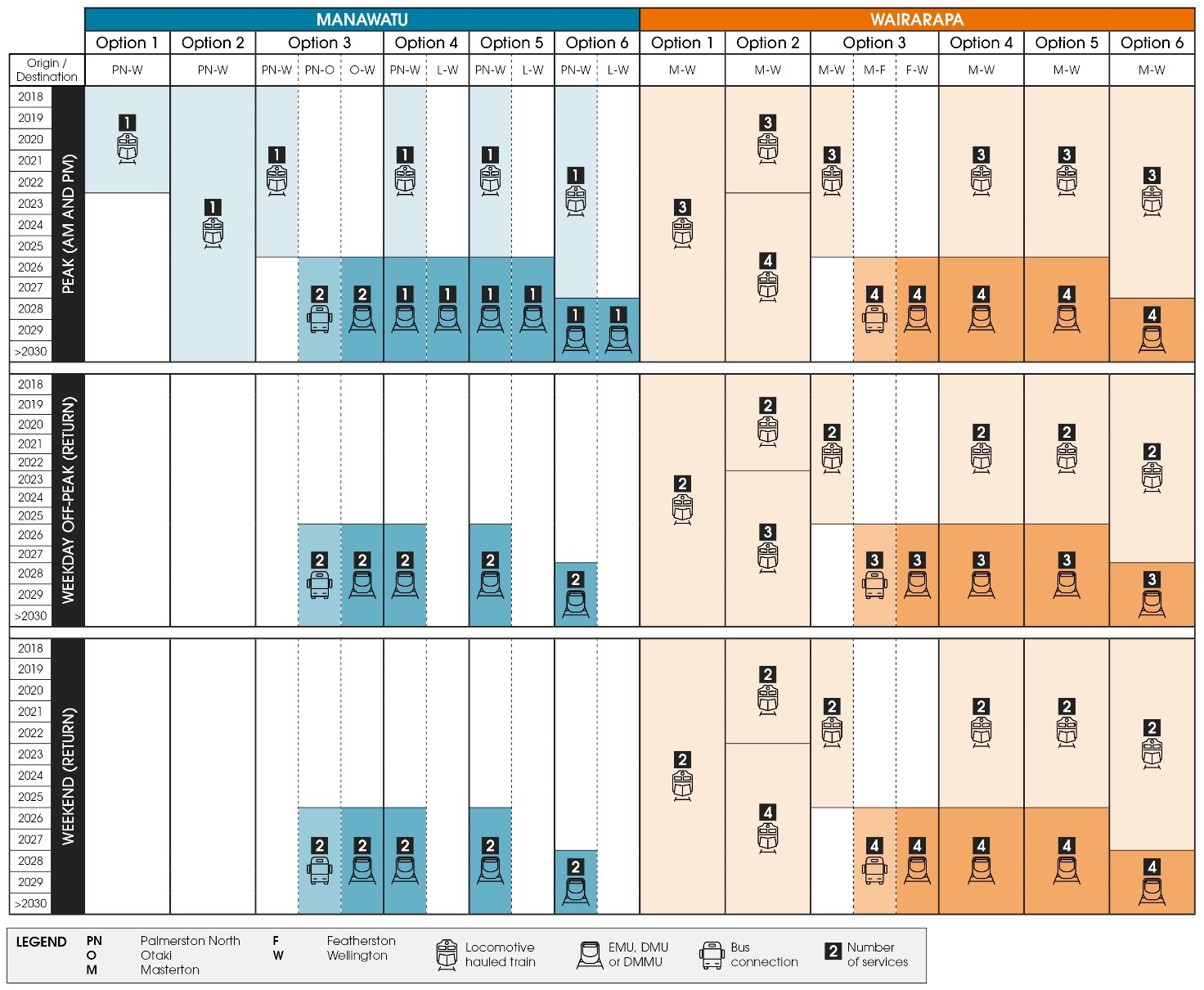

Figure 1-5 summarises and compares the timing (financial year) and level of service provided by the

operational elements of the options.

Stantec │ Lower North Island Longer-Distance Rolling Stock Business Case │ 26 September 2019

Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rol ing Stock Business Case -

Amended Draft Final.docx │ Page vii

link to page 11

1987

LGOIMA,

under

Figure 1-5: Summary of the timing and level of service provided by each option at key periods

The options have been assessed against the assessment framework shown i

n Table 1-2, which consists of:

•

Four investment objectives identified by stakeholders, which show the options’ likely response to the

problems and benefits, relating to service capacity, customer satisfaction, operational flexibility (which

includes resilience) and whole of life costs;

•

Seven critical success factors identified by stakeholders, which are essential to the successful

implementation of any option, relating to strategic alignment, affordability – capital costs, affordability

– operational costs, technical achievability, resilience, environmental sustainability, and public

Released

acceptability (which includes timeframe and environment); and

•

Four option characteristics, which al ow the options to be compared further, relating to indicative cost,

indicative economics, implementation timeframe, and key risks.

The DMU and DMMU options have been found to be best performing across al three aspects of the

assessment. The DMU option is more affordable and provides a slightly better economic return, but the

DMMU option best meets the scored assessment criteria, with better scores against the investment

objectives and crucial Strategic Alignment critical success factor. The DMMU option is consequently

ranked ahead of DMU, although both options are viable.

Stantec │ Lower North Island Longer-Distance Rolling Stock Business Case │ 26 September 2019

Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rol ing Stock Business Case -

Amended Draft Final.docx │ Page viii

link to page 11 link to page 11 link to page 11

Table 1-2: Option assessment summary

t

st

t

et

ts

Flee

t

Flee

Boo e

e

g

a

U Fle

1: n

le

U Fleet

ap

2: in & F

3:

M

MMU

U Fle

htin

g

l EM

ig

D

D

tion ntai rar

tion inta tin

tion

tion 4:

tion 5:

tion 6: EM

p ai ai

p a

p rtia

p ew

ew

p

We

O M W

O M Exis

O Pa

O N

Op N

O Full

Investment Objectives

Increase service capacity

25%

L

M

M

H

H

H

Improve customer

15%

satisfaction

L

L

L

H

H

H

Maximise operational

10%

flexibility

L

L

L

M-H

H

M

Minimise whole of life costs

10%

1987

per passenger

H

M

M-H

H

H

L

1

Critical Success Factors

Strategic alignment

10%

L

L-M

M

M-H

H

M-H

Affordability - capital

5%

H

M

M

M

M

L

Affordability - operational

5%

H

L-M

M-H

M

M

M

Technical achievability

5%

H

H

H

H

M-H

H

Resilience

5%

L

M

M-H

H

H

M-H

LGOIMA,

Environmental sustainability

5%

L

L

M

L-M

M-H

H

Public acceptability

5%

L

L-M

L

M

M-H

M

Characteristics2

Indicative 30-year net cost

$200 -

$176 -

$202 -

$454 -

under

over do-minimum (2018 $m)

-

$227 -

$386

$364

$343

$381

$754

Indicative 30-year BCR over

do-minimum

3

-

0.9 - 2.2

0.9 - 2.2

1.2 - 3.3

1.1 - 2.9

0.5 - 1.2

Indicative 60-year BCR over

do-minimum

-

1.1 - 3.1

1.1 - 3.3

1.4 - 5.0

1.3 - 4.2

0.7 - 2.0

Indicative implementation

timeframe

13 years

3 years

7 years

7 years

7 years

9 years

Key Risks

t

t

t

Released en e en

ty

en

gy

ture

er

e er xi e er

lo

m th

m th

le

p

m th

ironm ilienc to

ironm ilienc to

ilienc to

ironm

hno

t struc

us ow

us ow

om

us ow

os

Env Res C Gr

Env Res C Gr

C Res C Gr

Env

Tec

C Infra

MCA score

100%

2.0

2.3

2.7

4.4

4.7

3.9

Overal Ranking

6

5

4

2

1

3

1 Based on the discounted net cost per passenger over a 60-year assessment period.

2 Costs, benefits and BCR ranges are based on 80% of the model ed costs and high patronage and revenue growth

(see Section 5.4.1), 120% of costs and low growth, and a 4% discount rate.

3 BCRs are indicative high-level ‘first cut’ BCRs, which were used to test the options at the option selection stage. They

differ from those that support the recommended option, which were the result of detailed analysis of benefits and costs.

Stantec │ Lower North Island Longer-Distance Rolling Stock Business Case │ 26 September 2019

Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rol ing Stock Business Case -

Amended Draft Final.docx │ Page ix

Recommended Option The investment proposal entails the replacement of al existing longer-distance rail rol ing stock with a fleet

of 15 four-car DMUs or DMMUs, which wil be owned by GWRC and enter service in the 2025 financial year.

The new rolling stock will operate all services on the Wairarapa and Manawatu lines, which wil run at

improved frequencies to provide better access and capacity between Masterton/Palmerston North and

Wellington, including much needed additional capacity at key stations within the electrified area.

Supporting improvements wil be made to maintenance facilities, stations and network infrastructure.

Existing rolling stock will be maintained in acceptable operating condition until the introduction of the new

rol ing stock and then be retired.

The DMMU option is the primary preferred and recommended option due to its better alignment with the

investment objectives and key success factors. A detailed assessment has found that this has:

•

medium growth 30-year discounted benefits of $551.7m compared to costs at the same level of

$291.2m, and a projected BCR range of 1.3 to 2.6 (compared to a DMU BCR range of 1.5 to 3.0); and

•

a higher BCR range of 2.2 to 4.1 (compared to a DMU BCR range of 2.5 to 5.1) if the cost of network

infrastructure, which is required to restore infrastructure that was previously removed and catch up for

past underinvestment, is excluded.

1987

Assessment against the NZTA’s 2018-21 Investment Assessment Framework gives a recommended results

alignment rating of Very High and a BCR rating of Low, which give both options a priority order rating of 1,

the highest priority for NLTP funding. The Very High rating relates to the ongoing improvement in access

that the investment proposal enables for large numbers of passengers on the Wellington region’s main

northern corridors.

GWRC would lead implementation and be responsible for procuring the new DMMU rol ing stock fleet and

station-related infrastructure improvements, along with overal programme management. GWRC would also

be responsible for long-term operation of services on both lines, including Manawatu Line services, which

would be incorporated into its existing rail contract and operated on behalf of HRC north of the regional

LGOIMA,

boundary. KiwiRail would be responsible for network-related infrastructure improvements in accordance with

the Metropolitan Rail Operating Model. Key risks around timeframe, funding, KiwiRail’s commercial interests,

costs and revenue would be managed through the project management process and contractual

mechanisms.

The investment proposal includes expected project capital expenditure of $415.3m, with a

confidence

under

estimate of $449.2m. It is proposed that network infrastructure wil be funded by the NZTA at a

FAR,

rol ing stock, maintenance facility and station improvements receiving a special

FAR, and ongoing

maintenance and operations receiving a standard

FAR. Cost and revenue wil be shared between

GWRC and HRC based on the share of vehicle service km in each region. An urgent funding decision is

required to enable the specification and procurement process to commence in mid-2020 and ensure that

sufficient capacity is in place when required to meet projected demand pressures, given the long lead times

for rol ing stock and supporting infrastructure.

In conclusion, the investment proposal has been shown to clearly respond to significant problems and offer

significant benefits to the lower North Island. These link closely with national transport and economic

development priorities and provide a strong case for investment. It is therefore recommended that

Released

investment decision makers:

•

approve this proposal to replace existing Wel ington longer-distance rail rol ing stock with a fleet of 15

four-car dual-mode DMMU units, and associated infrastructure and service enhancements;

•

approve funding through appropriate channels at appropriate FAR rates by June 2020; and

•

prioritise these approvals, to al ow project planning to commence and enable the new rol ing stock to

be brought into service in the 2025 financial year and service improvements to be implemented the

fol owing financial year.

Decision Sought •

Agree that Option 5 - replace existing fleets with a dual-mode multiple unit fleet at the earliest

opportunity and improving service levels once the fleet is in place is the best outcome for this business

case;

Stantec │ Lower North Island Longer-Distance Rolling Stock Business Case │ 26 September 2019

Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rol ing Stock Business Case -

Amended Draft Final.docx │ Page x

•

Agree funding of the preferred option’s capital investment of $415.3m (or the

confidence

estimate of $449.2m), ful y or partial y co-funded through the NLTP at a full FAR (network infrastructure)

and special FAR rate (other capital investment), or potential y through another source such as the PGF,

subject to funding approval;

•

Agree that GWRC procure and deliver the new DMMU rol ing stock fleet and above-track

infrastructure, along with overal programme management; and

•

Agree that KiwiRail to procure and deliver network infrastructure-related improvements

•

Confirm funding arrangements by June 2020, to enable specification, design and procurement

processes to commence immediately and ensure that the rol ing stock is in place when required to

help manage demand.

1987

LGOIMA,

under

Released

Stantec │ Lower North Island Longer-Distance Rolling Stock Business Case │ 26 September 2019

Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rol ing Stock Business Case -

Amended Draft Final.docx │ Page xi

Abbreviations

DMMU

Dual Mode Multiple Unit

DMU

Diesel Multiple Unit

EDMU

Electro-Diesel Multiple Unit

EEM

Economic Evaluation Manual

EMU

Electric Multiple Unit

FAR

Funding Assistance Rate

FY

Financial Year

GPS

Government Policy Statement on Land Transport

1987

GWRC

Greater Wellington Regional Council

HRC

Horizons Regional Council

LGWM

Let’s Get Wellington Moving

LTMA

Land Transport Management Act

LGOIMA,

MOT

Ministry of Transport

NLTF

National Land Transport Fund

NLTP

National Land Transport Programme

NZRP

New Zealand Rail Plan

under

NZTA

New Zealand Transport Agency

PGF

Provincial Growth Fund

RGF

Regional Growth Framework

RIC

Rail Infrastructure Consultants

RLTP

Regional Land Transport Plan

Released

RPTP

Regional Public Transport Plan

RNIP

Rail Network Investment Plan

RS1

Rail Scenario 1

TAIP

Transport Agency Investment Proposal

WMUP

Wel ington Metro Upgrade Programme

WRRP

Wellington Regional Rail Plan

Stantec │ Lower North Island Longer-Distance Rol ing Stock Business Case │ 26 September 2019

Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rol ing Stock Business Case - Amended

Draft Final.docx │ Page xi

link to page 7 link to page 11 link to page 29 link to page 30

Greater Wellington Regional Council

Lower North Island Longer-Distance Rolling Stock Business Case

CONTENTS

Executive Summary ........................................................................................................................................................ i

Abbreviations ............................................................................................................................................................... xii

1.

Introduction ...................................................................................................................................................... 1

2.

Strategic Context ............................................................................................................................................ 2

2.1

Background ...................................................................................................................................................... 2

2.2

Regional Context ............................................................................................................................................. 7

2.3

National Context............................................................................................................................................ 11

1987

2.4

Conclusion ...................................................................................................................................................... 14

3.

Strategic Assessment .................................................................................................................................... 16

3.1

Problem Definition ......................................................................................................................................... 16

3.2

Benefits of Investment ................................................................................................................................... 24

3.3

Investment Objectives .................................................................................................................................. 26

3.4

Conclusion ...................................................................................................................................................... 27

LGOIMA,

4.

Option Selection ............................................................................................................................................ 29

4.1

Options Development ................................................................................................................................... 29

4.2

Options Description ....................................................................................................................................... 29

4.3

Option Assessment ........................................................................................................................................ 42

under

4.4

Conclusion ...................................................................................................................................................... 47

5.

Recommended Option ................................................................................................................................ 48

5.1

Description ...................................................................................................................................................... 48

5.2

Benefits ............................................................................................................................................................ 53

5.3

Costs ................................................................................................................................................................ 55

5.4

Economic Analysis ......................................................................................................................................... 58

5.5

Assessment Profile .......................................................................................................................................... 62

Released

5.6

Commercial Case .......................................................................................................................................... 64

5.7

Financial Case ................................................................................................................................................ 68

5.8

Management Case ....................................................................................................................................... 70

5.9

Conclusion and Final Recommendation ................................................................................................... 71

LIST OF TABLES

Table 1-1: Links between investment benefits and relevant strategies and plans .............................................. v

Table 1-2: Option assessment summary ..................................................................................................................... ix

Table 2-1: Relevant activity class investment priorities and opportunities .......................................................... 12

Table 2-2: GPS access and environment strategic priorities, objectives and applicable results .................... 13

Stantec │ Lower North Island Longer-Distance Rol ing Stock Business Case │ 26 September 2019

Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rol ing Stock Business Case - Amended

Draft Final.docx

link to page 45 link to page 46 link to page 47 link to page 48 link to page 50 link to page 52 link to page 54 link to page 56 link to page 58 link to page 59 link to page 60 link to page 63 link to page 68 link to page 69 link to page 70 link to page 73 link to page 74 link to page 75 link to page 77 link to page 77 link to page 78 link to page 78 link to page 79 link to page 80 link to page 83 link to page 85 link to page 86 link to page 86 link to page 87 link to page 88 link to page 5 link to page 6 link to page 7 link to page 9 link to page 10 link to page 19 link to page 21 link to page 22

Table 3-1: Links between the investment benefits and relevant strategies and plans ..................................... 28

Table 4-1: Potential options ........................................................................................................................................ 29

Table 4-2: Option 1 operational and fleet and infrastructure requirements ...................................................... 30

Table 4-3: Option 2 operational and fleet and infrastructure requirements ...................................................... 31

Table 4-4: Option 3 operational and fleet and infrastructure requirements ...................................................... 33

Table 4-5: Option 4 operational and fleet and infrastructure requirements ...................................................... 35

Table 4-6: Option 5 operational and fleet and infrastructure requirements ...................................................... 37

Table 4-7: Option 6 operational and fleet and infrastructure requirements ...................................................... 39

Table 4-8: Summary of the fleet and infrastructure requirements and completion financial year................. 41

Table 4-9: Assessment framework scoring system ................................................................................................... 42

Table 4-10: Option assessment summary ................................................................................................................. 43

Table 4-11: Mid-range and incremental BCRs ......................................................................................................... 46

Table 5-1: Current and proposed service levels - Wairarapa Line ....................................................................... 51

1987

Table 5-2: Current and proposed service levels - Manawatu Line ...................................................................... 52

Table 5-3: Links between the problem response, and investment benefits and objectives ............................ 53

Table 5-4: 30-year discounted cost of DMU cost elements over the do-minimum ........................................... 56

Table 5-5: 30-year discounted cost of DMMU cost elements over the do-minimum ........................................ 57

Table 5-6: Cost confidence ........................................................................................................................................ 58

Table 5-7: Results of DMU cost benefit appraisal .................................................................................................... 60

Table 5-8: Results of DMMU cost benefit appraisal ................................................................................................. 60

LGOIMA,

Table 5-9: Results of cost sensitivity testing with network infrastructure cost included ..................................... 61

Table 5-10: Results of cost sensitivity testing with network infrastructure cost excluded .................................. 61

Table 5-11: Results of benefit sensitivity testing ....................................................................................................... 62

Table 5-12: GPS results alignment .............................................................................................................................. 63

under

Table 5-13: Key risks ...................................................................................................................................................... 66

Table 5-14: Capital investment components without and with additional contingency ................................ 68

Table 5-15: DMMU capital investment cash flow .................................................................................................... 69

Table 5-16: DMMU loan repayment cashflow and funding split .......................................................................... 69

Table 5-17: DMMU change in operational costs (revenue, operating/maintenance/renewal costs)........... 70

Table 5-18: Key milestones .......................................................................................................................................... 71

Released

LIST OF FIGURES

Figure 1-1: Wairarapa Line morning peak patronage and projected demand.................................................. iii

Figure 1-2: Electrified area morning peak patronage and projected demand ..................................................iv

Figure 1-3: Projected Wel ington Station morning peak hour demand and capacity (al Metlink lines) ......... v

Figure 1-4: Projected Wel ington Station morning peak hour demand and extra capacity (al Metlink lines)vii

Figure 1-5: Summary of the timing and level of service provided by each option at key periods ................. viii

Figure 2-1: Wel ington longer-distance rail lines - Wairarapa (red) and Manawatu (blue) ............................... 2

Figure 2-2: SW carriage type ........................................................................................................................................ 4

Figure 2-3: SE carriage type.......................................................................................................................................... 5

Stantec │ Lower North Island Longer-Distance Rol ing Stock Business Case │ 26 September 2019

Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rol ing Stock Business Case - Amended

Draft Final.docx

link to page 23 link to page 34 link to page 35 link to page 36 link to page 37 link to page 38 link to page 39 link to page 39 link to page 43 link to page 43 link to page 57 link to page 65 link to page 66

Figure 2-4: S carriage type (source: nzrailphotos.co.nz) .......................................................................................... 6

Figure 3-1: Wairarapa Line morning peak patronage and seated capacity .................................................... 17

Figure 3-2: Wairarapa Line morning peak patronage and projected demand................................................ 18

Figure 3-3: Manawatu Line morning peak patronage and seated capacity ................................................... 19

Figure 3-4: Manawatu Line morning peak patronage and projected demand ............................................... 20

Figure 3-5: Electrified area morning peak patronage .......................................................................................... 21

Figure 3-6: Electrified area morning peak patronage and projected demand ................................................ 22

Figure 3-7: Projected Wel ington Station morning peak hour demand and capacity (al Metlink lines) ....... 22

Figure 3-8: Projected Wel ington Station morning peak hour demand and extra capacity (al Metlink lines)

26

Figure 4-1: Summary of the timing and level of service provided by each option at key periods ................. 40

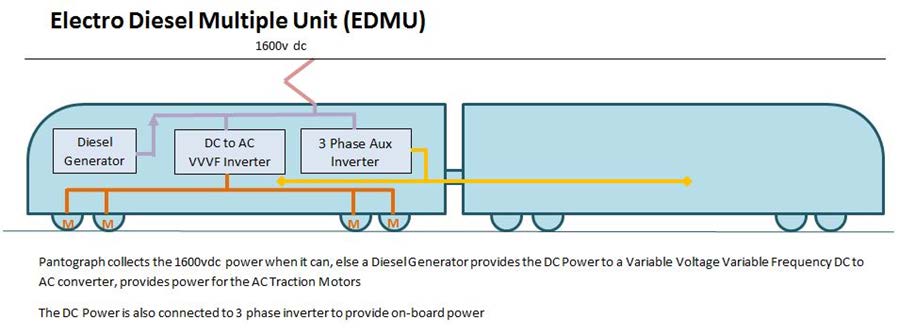

Figure 5-1: Characteristics of a DMU with diesel-hydraulic transmission ............................................................. 48

Figure 5-2: Characteristics of an EDMU .................................................................................................................... 49

1987

APPENDICES

Appendix A Investment Logic Map

Appendix B Benefits Realisation Plan

Appendix C Summary of Long List Options

Appendix D Investment Cash Flow

LGOIMA,

under

Released

Stantec │ Lower North Island Longer-Distance Rol ing Stock Business Case │ 26 September 2019

Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rol ing Stock Business Case - Amended

Draft Final.docx

link to page 19 link to page 33 link to page 46 link to page 65

1.

Introduction

This business case has been prepared by Stantec New Zealand and Greater Wellington Regional Council

(GWRC), with economic peer review by Transport Futures Limited. It assesses the case for replacing the

rol ing stock fleets that provide longer-distance rail passenger services on the Wairarapa and Manawatu

lines, which are nearing end of life, and using the replacement fleet to improve service levels and increase

the overall capacity of GWRC’s Metlink rail network to address serious and urgent capacity constraints. It

fol ows a 2017 business case that assessed the case for continued short-term public investment in the

Palmerston North-Wellington rail passenger service, and two 2017 infrastructure-focused business cases

that assessed the case for catch-up track renewals and capacity and resilience enhancements on the

Wel ington metro rail network, which includes the Wairarapa Line and the southern end of the Manawatu

Line. These wil be supported by and incorporated into a new under-development Wellington Regional

Rail Plan (WRRP), which wil provide a future investment pathway for the Metlink network.

The business case takes the form of a single-stage business case fol owing the NZ Transport Agency (NZTA)

Business Case Approach. It therefore combines elements of the activity Strategic, Indicative and Detailed

business cases into a single document, which has the fol owing structure:

•

Chapter

2 describes the strategic context;

1987

•

Chapter

3 presents the strategic assessment, which combines with the strategic context to form the

Strategic Case;

•

Chapter

4 assesses the option selection process that forms the basis of the Indicative Case; and

•

Chapter

5 details the recommended option, completing the overal Detailed Case for investment.

The business case has been developed col aboratively by stakeholders. These include GWRC, which has a

key interest as the organisation that is responsible for planning and funding public transport in the

Wellington Region, Horizons Regional Council (HRC), which is responsible for planning and funding public

transport in the Horizons Region (Manawatu-Whanganui), and the NZTA, which has an interest both as the

LGOIMA,

Government’s transport investor and as the state highway network operator. Input has also been provided

by Transdev, the Wellington rail passenger service operator, KiwiRail, the network operator and operator of

the existing Palmerston North-Wellington service, and local councils on both corridors, al of whom

participated in one or more of the previous business cases. Additional input has been sought from other

parties as required.

under

Released

26 September 2019 │ Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rolling Stock

Business Case - Amended Draft Final.docx

Page 1

link to page 19 link to page 19 link to page 19

2.

Strategic Context

2.1

Background

The lower North Island is served by an extensive network of public transport services, which include

Wel ington urban area bus, rail and ferry services, Wairarapa bus services, Palmerston North bus services,

and longer-distance rail services. The latter extend Wel ington’s core public transport corridors beyond the

Wel ington electrified area rail termini of Upper Hutt and Waikanae, to link Masterton on the Wairarapa

Line, and Palmerston North on the Manawatu Line, with Wel ington. Both lines have had continuous rail

passenger service since they were completed in the 1880s and are consequently an established and

integral part of the transport system in the communities that they serve, and the services that operate on

them are well-patronised.

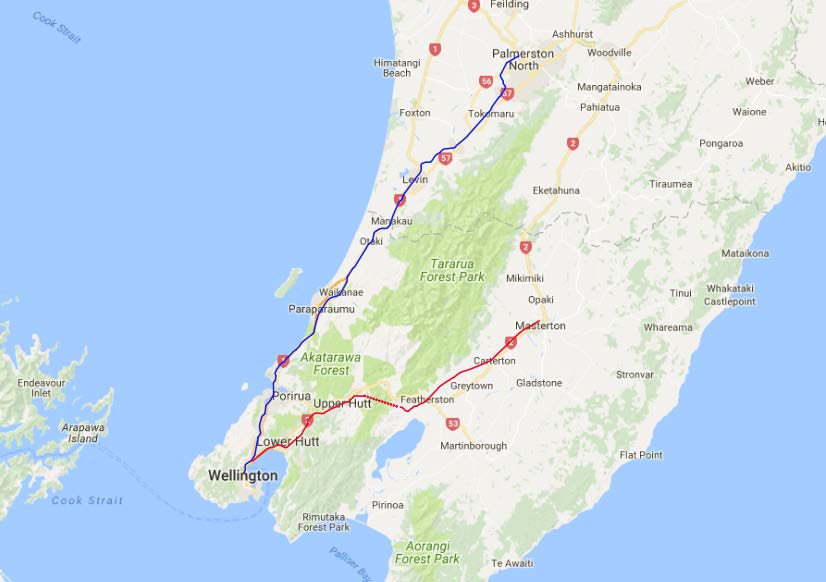

The two lines are shown i

n Figure 2-1 and are described further in the following sections.

1987

LGOIMA,

under

Released

Figure 2-1: Wel ington longer-distance rail lines - Wairarapa (red) and Manawatu (blue)

2.1.1 Wairarapa Line

The Wairarapa Line is located on the eastern side of and entirely within the Wellington Region, and

primarily serves the Wairarapa sub-region, which is a predominantly rural area that encompasses 73% of

the region’s land area. Its population of 45,500

4 (approximately 9% of the region’s population) is

experiencing significant ongoing growth, which is forecast to continue in the future. The line links

Masterton (three stations), Carterton, Matarawa, Woodside (Greytown), and Featherston (with connecting

bus services from Martinborough), and surrounding areas of the Masterton, Carterton and South Wairarapa

districts, with each other and Wellington. Services also cal at Maymorn (where they are the only form of

public transport), Upper Hutt, Waterloo and Petone in the Hutt Val ey, to provide access to local

destinations and vital extra capacity to supplement the electrified metro rail services that serve the

population of 149,6

004 there, and are an integral part of the rail service offering.

4 Statistics New Zealand subnational population estimate as at 30 June 2018.

26 September 2019 │ Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rolling Stock

Business Case - Amended Draft Final.docx

Page 2

link to page 21 link to page 22 link to page 20 link to page 20 link to page 20 link to page 20 link to page 20 link to page 20

The link is very important to Wairarapa residents, given that the Hutt Val ey and Wellington provide many

employment, educational and other opportunities and services that are not available locally.

Approximately one quarter of Wairarapa residents commute to other parts of the region for work.

The Wairarapa Line has a critical role as one of only two transport links between the Wairarapa and the

rest of the Wellington region. Its direct route under the Remutaka Range via the 8.8 km Remutaka Tunnel is

safer, more efficient and more resilient than paral el State Highway 2, which crosses the range via a steep,

winding and narrow route over a 555-metre summit. This road is very busy at peak times and has a high

crash risk

5, low average speed

6 and susceptibility to weather-related closure

7. Rail passenger services on

the line consequently have an important road substitute role, which is exemplified by the high rail mode

share of commuting trips, including a very high 60% share of trips to the Wellington CBD

8, which is around

half of the journey to work trips between Wairarapa and the entire Wel ington region. This provides

consequent congestion, parking demand and environmental benefits in the Hutt Valley and Wel ington

city.

The Wairarapa Line is currently served by three peak direction services in each weekday peak, two

weekday off-peak services in each direction, an additional service in each direction on Friday nights, and

two in each direction on weekend days. Each takes between 1 hour and 40 minutes and 1 hour and 50

minutes to travel the 90.96 km between the line’s end points, which is competitive with the car alternative.

In total, they carried approximately 625,000 peak passengers and 154,000 off-peak passengers in the 2019

1987

financial year

9 (FY), which equated to an average of around 420 peak passengers and 100 off-peak

passengers per trip. Peak services are close to capacity, and changes were made to carriage al ocation

to provide short term relief on the most crowded afternoon service in April 2019. Further options to improve

asset utilisation are being investigated but are limited.

Wairarapa Line services are currently operated as part of the Metlink public transport network by Transdev,

under contract to GWRC, using a mixed fleet of GWRC-owned

10 conventional locomotive-hauled rolling

stock. Hyundai Rotem provides rol ing stock maintenance as a subcontractor to Transdev through an

Operator Maintenance Partnering Contract. KiwiRail provides locomotives and locomotive crews through

a hook and tow arrangement.

The rolling stock fleet is made up of the fol owing carriage types:

LGOIMA,

•

The SW type, il ustrated in

Figure 2-2, which were remanufactured specifical y for Wairarapa Line

service from ex-British Rail Mark 2 carriages dating from the early 1970s prior to entering New Zealand

service in 2007. The carriages can be identified by their large windows and modern seating and

interiors, and they feature a mix of airline style and table seating, at-seat power outlets, air

conditioning, automatic doors and a public-address system. The type consists of:

under

12 SW class carriages, which have 64 seats and a single toilet;

3 SWS class carriages, which have 37 seats, a servery (unused), a wheelchair hoist on each side, an audio

induction loop system and an accessible toilet; and

3 SWG class carriages, which have 37 seats, a luggage compartment and a diesel generator to power the

carriages.

•

The SE type, il ustrated in

Figure 2-3, which were refurbished from ex-British Rail Mark 2 carriages dating

from the early 1970s prior to entering New Zealand service in 2009, although much less extensively than

the SW type. Further modifications were made prior to their introduction on Wairarapa Line services in

Released

2013. The carriages can be identified by their original smal windows and British Rail-based seating and

interiors, and they feature general y similar amenities to the SW carriages, although they were initial y

5 New Zealand Road Assessment Programme KiwiRAP) collective and personal risk scores for this section of road have

varied between Medium High and High over the last decade. Both scores are at the high end of the five-point risk

scale.

6 The 2016 NZ Transport Agency SH2 Te Marua to Masterton Programme Business Case notes that this section of State

Highway 2, which has a nominal 100 km/h speed limit, has an average speed of 58 km/h.

7 The 2016 NZ Transport Agency SH2 Te Marua to Masterton Programme Business Case notes that State Highway 2 had

19 closures due to unplanned natural events (snow/ice, wind, slip) in the prior five-year period. Each closure had an

average duration of 36 hours, indicating that the road is closed for an average of 5.7 days a year (i.e. nearly a week)

due to weather related events.

8 This compares to between 44% and 50% in Kapiti, Hutt Val ey and Porirua. Based on Statistics New Zealand journey to

work data from the 2013 Census.

9 Financial years in this document denote the 12-month period ending on 30 June of the year stated, so the 2019

financial year refers to the period between 1 July 2018 and 30 June 2019.

10 The carriages are owned by Greater Wellington Rail Ltd, which is a subsidiary of Greater Wel ington Regional Council.

26 September 2019 │ Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rolling Stock

Business Case - Amended Draft Final.docx

Page 3

used to provide additional capacity in the electrified area and have a higher-density seating

arrangement. The type consists of:

4 SE class carriages, which have 75 seats and a single toilet;

1 SES class carriage, which has 63 seats, a wheelchair hoist on each side, an audio induction loop system

and an accessible toilet; and

1 SEG class carriage, which has 44 seats, a luggage compartment and a diesel generator to power the

carriages.

•

A single AG type luggage / generator van, which dates from the late 1970s and is used to supplement

or replace the SWG or SEG carriages on an as needed basis.

1987

LGOIMA,

under

Figure 2-2: SW carriage type

Released

Trains typically operate with between five and nine carriages, providing a seated capacity of between

266 and 599 passengers per train. Each consist requires a SWS/SES and SWG/SEG, with the balance of

SW/SE types. The largest consists are al ocated to the most heavily used peak services, which depart

Masterton at 6:20 and Wel ington at 16:25. Two SWs, one SWS and one SWG are typical y held as spares to

facilitate maintenance.

The SW and SE types are based on the same source carriage but were previously incompatible due to

differences in suspension systems (bogies), electrical connections and brake systems. Trains therefore had

to operate in al -SW type or all-SE type sets, which limited flexibility and consequently capacity on some

trains, particularly when SE type carriages were removed from service for maintenance. Compatibility

modifications, which were completed in early-2019, have addressed this issue, al owing the introduction of

the nine car consist.

GWRC is about to commence a light mid-life refurbishment of the SW and SE fleets, which wil take

eighteen months to complete and extend the carriages’ life to the mid-2020s. The scope of the overhaul

26 September 2019 │ Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rolling Stock

Business Case - Amended Draft Final.docx

Page 4

link to page 25 link to page 22 link to page 22

could be expanded if this business case determines that the fleets need to remain in operation for a longer

period. All carriages will be life-expired require replacement by 2032.

1987

LGOIMA,

Figure 2-3: SE carriage type

2.1.2 Manawatu Line

The Manawatu Line is located on the western side of the Wel ington Region and extends beyond the

regional boundary into the Horizons Region. It primarily serves the Kapiti Coast and southern Manawatu

under

areas, which together have a catchment population of approximately 174,900

11 (75% of which lies north of

Waikanae), which is experiencing significant ongoing growth that is forecast to continue in the future. The

line links Palmerston North, Shannon, Levin, Otaki, Waikanae and Paraparaumu, and surrounding areas of

the Palmerston North city and Horowhenua and Kapiti Coast districts with each other and Wellington, and

services provides vital extra capacity to supplement the electrified metro rail services south of Waikanae.

The link is important to residents, since it provides access to many employment, educational and other

opportunities and services that are not available elsewhere on the corridor.

The Manawatu Line paral els State Highway 57 north of Levin and State Highway 1 south of that point.

State Highway 1 carries large traffic volumes south of Levin, and geographical constraints restrict it to a

single lane and limit road alternatives for much of its length, which makes it vulnerable to congestion and

Released

resilience events. State Highway 1 is currently being upgraded (see Sectio

n 2.2.2).

The Manawatu Line is currently served by the Capital Connection, a weekday commuter train operated

by KiwiRail, which runs a single peak direction service in each weekday peak. It is the only rail passenger

service on this corridor north of Waikanae

12, and currently the only long-distance commuter train that

crosses a regional boundary in New Zealand. The train takes 2 hours and 5 minutes to travel the 136.23 km

between the line’s end points, which is competitive with the car alternative. It carried approximately

134,000 passengers in the 2019 FY, which equated to an average of around 280 passengers per trip. It is

increasingly operating at capacity on some days of the week, reflecting day to day patronage variations

associated with long-distance commuting, but its capacity is constrained by rolling stock availability and

cannot be increased.

11 Statistics New Zealand subnational population estimate as at 30 June 2018.

12 KiwiRail also runs the tourism-focused thrice-weekly Auckland-Wel ington Northern Explorer on the corridor, which runs

in the opposite direction to peak commuter requirements and stops at Palmerston North and Wel ington only.

26 September 2019 │ Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rolling Stock

Business Case - Amended Draft Final.docx

Page 5

link to page 23 link to page 33 link to page 26

The Capital Connection uses KiwiRail-owned conventional locomotive-hauled rolling stock, with

locomotives and locomotive crews being provided through an intra-company hook and tow

arrangement. The rolling stock fleet is made up of:

•

The S type, il ustrated in

Figure 2-4, which were rebuilt from ex-British Rail Mark 2 carriages dating from

the early 1970s prior to entering New Zealand service in 1999, although differently from the SW and SE

cars, which they are not compatible with. The carriages can be identified by their original smal

windows and upgraded seating and interiors, and they feature general y similar amenities to the SW

and SE carriages. The type consists of:

7 standard S class carriages, which have 60 seats and a single toilet; and

1 S class servery carriage, which has 28 seats and a toilet.

•

A single AG type luggage / generator van, which dates from the late 1970s and is equipped with a

wheelchair hoist.

The train currently operates in an eight-car configuration between Friday afternoon and Tuesday morning,

with six standard cars, the servery car, and luggage / generator van, to provide a seated capacity of 388.

It operates with one less standard car at other times to al ow for maintenance, providing a seated

capacity of 328. One standard car is inoperable due to significant structural issues. No spares are held, so

1987

the train operates at reduced capacity when additional maintenance is required.

The S type carriages are close to the end of their service life, and either require extensive refurbishment or

replacement prior to mid-2021 to enable continued operation of services after that point. A decision on

whether to proceed with refurbishment wil be required within six months (see Sectio

n 3.1.1).

The Capital Connection is classified as an exempt service under the Land Transport Management Act 2003

(LTMA) (see Sectio

n 2.2.3) and operates as a stand-alone service with a separate fare structure. It

operated without public subsidy between its introduction in 1991 and July 2015.

LGOIMA,

under

Released

Figure 2-4: S carriage type (source: nzrailphotos.co.nz)

26 September 2019 │ Status: Draft │ Project No.: 310200204 │ Our ref: 310200204 190926 Lower North Island Longer-Distance Rolling Stock

Business Case - Amended Draft Final.docx

Page 6

link to page 26 link to page 22

2.2

Regional Context

2.2.1 Regional Rail Investment

2.2.1.1

Existing

GWRC’s rail investment plans are detailed in the Wellington Regional Rail Plan, which supplements the

Regional Public Transport Plan and Regional Land Transport Plan (see Sectio

n 2.2.3). The most recent 2013

update of the plan updated the preferred growth pathway known as Rail Scenario 1 (RS1), although it

focused on upgrades to the electrified network that were underway at that time and future infrastructure

upgrades that would enable frequency increases. The 2013 WRRP noted ongoing patronage increases on

the Wairarapa Line but did not propose frequency or capacity increases beyond the electrified area

termini in the short or medium term. In the longer-term, it envisaged reduced journey times on al lines

under Rail Scenario A and network extensions in the form of shuttle or non-electrified interlined services on

both the Wairarapa and Manawatu lines under Rail Scenario B. The WRRP also determined that

electrification beyond Upper Hutt and Waikanae would not be warranted.

Recent planning has revolved around three separate business cases. The first is the Palmerston North-

Wel ington Rail Passenger Business Case, which was completed in October 2017. This assessed the case for

continued public investment in a Palmerston North-Wellington rail passenger service beyond June 2018

1987

when the existing arrangement was due to expire, making it a key supporting reference for this business

case. It considered six options: withdrawal of the train at that point, continued operation of a

conventional locomotive-hauled through train, replacement with a Diesel Multiple Unit (DMU) through

train, replacement with a DMU through train with improved service levels, replacement with a connecting

DMU service north of Waikanae, and replacement with a connecting coach (bus) north of Waikanae. It

determined that the best return on investment would be achieved by retaining through rail services and

improving them in the medium term, by replacing existing rol ing stock with DMUs and improving service

levels. The business case recommended that $6.2 mil ion in Crown funding be sought to enable continued

operation of the existing train until the 2022 financial year (when rol ing stock refurbishment and

replacement is required as noted in Sectio

n 2.1.2) and al ow sufficient time for the longer-term solution to