Purpose of report

Purpose of report

1.

The purpose of this briefing is to respond to a range of issues that you raised about the

proposed government-industry electric vehicle (EV) package at your meeting with Ministry of

Transport (Ministry) officials on 2 November 2015. These issues include:

1.1.

the scope of a potential information campaign for EVs by the Energy Efficiency and

Conservation Authority (EECA)

1.2.

whether the Electricity Levy can be used to fund the contestable fund or other

measures proposed in the draft EV package

1.3.

the potential role that the New Zealand Transport Agency (NZ Transport Agency)

could play in establishing EV charging infrastructure – we have divided this into:

1.3.1. within existing Government Policy Statement (GPS) settings, and

1.3.2. options for funding charging infrastructure from the National Land Transport

Fund (NLTF)

1.4.

information about public investment in charging infrastructure in other countries

1.5.

the link between the exemption from road user charges (RUC) for light EVs and the

proposed targets for EV uptake

1.6.

the potential to extend the RUC exemption to heavy EVs

1.7.

the scope of the proposed contestable fund, and its link to EV procurement options

1.8.

the actual numbers of EVs that business fleets have already purchased, or have

committed to purchasing.

2.

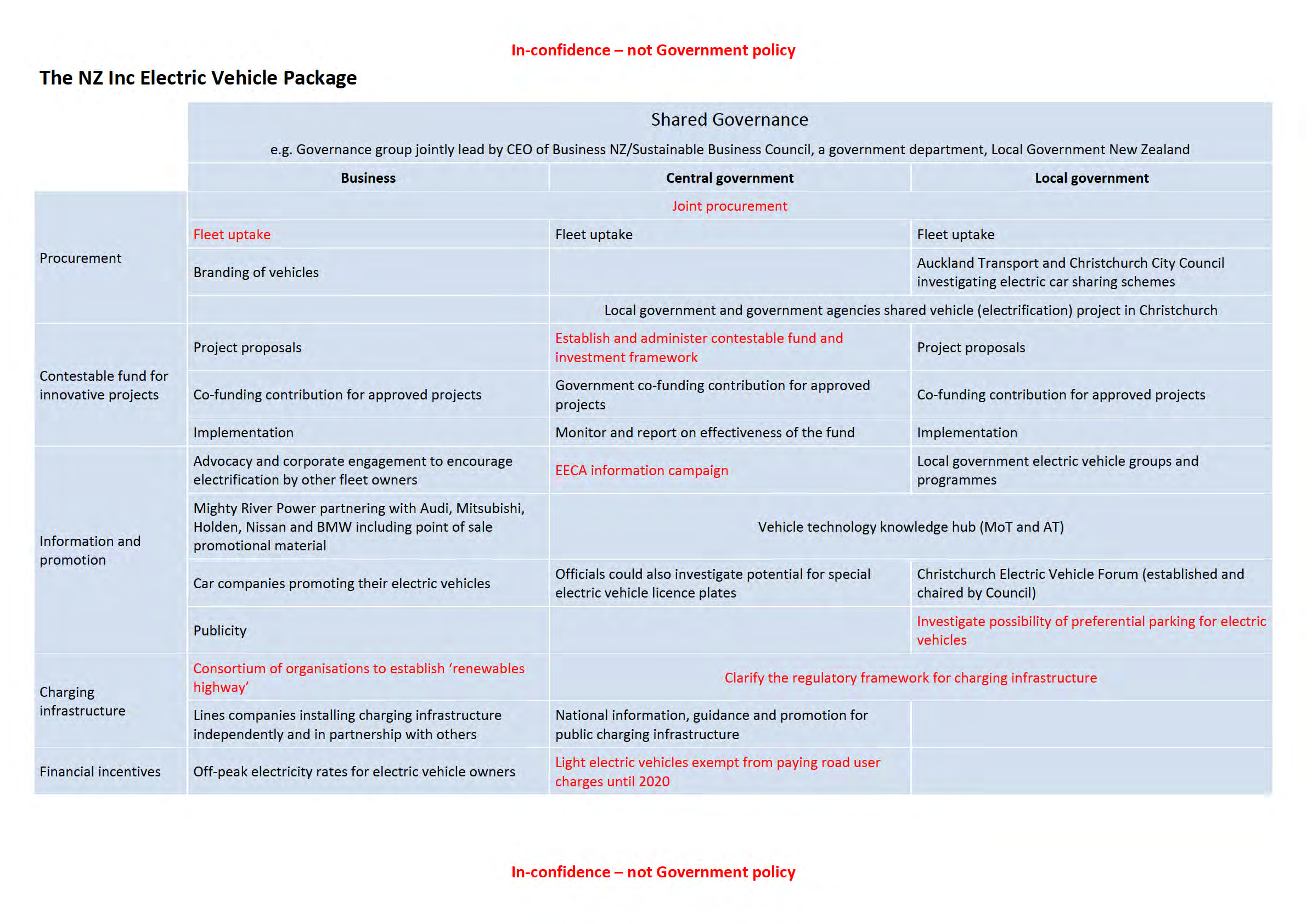

We have updated the A3 overview of the government-industry package in accordance with

your direction. The revised A3 is attached.

3.

The Sustainable Business Council Advisory Board met on 5 November 2015 to consider the

proposed package. Feedback from that meeting is in paragraph 84.

4.

You also raised tax issues related to EVs at your meeting with Ministry officials. On 9

November 2015, we will provide your office with a briefing on these issues for your meeting

with the Minister for Revenue, Hon Todd McClay.

An EECA information campaign would target business fleets and assist with industry

coordination

5.

The information and promotion campaign would have two components:

5.1.

a campaign targeted at business fleets (estimated at $400,000 per year)

5.2.

industry engagement and coordination (estimated at $450,000 per year).

Page 2 of 14

Business fleets campaign

Business fleets campaign

6.

An EECA information campaign would target businesses because most new cars come into

New Zealand through fleet purchases, so business fleets are a key market to influence. In

addition, overseas experience indicates that employees who experience an EV at work are

more likely to consider an EV for their own private vehicle.

7.

Barriers to uptake include misconceptions and nervousness about adopting new technology.

As EECA has already conducted market research into business fleets, it would be possible

to roll out a targeted information campaign quickly.

8.

Through the campaign, EECA would aim to persuade business fleet operators to include

EVs in their fleet purchases by:

8.1.

enabling easy cost comparisons via online tools1

8.2.

overcoming information barriers through workshops and other events

8.3.

providing opportunities to trial EVs first-hand

8.4.

showcasing high profile businesses that have already successfully adopted EVs.

Industry engagement and coordination

9.

EECA would provide a point of coordination for the range of businesses and industry bodies

involved in the EV market, to avoid duplication of effort or public confusion. EECA would

engage with all relevant parties to ensure that projects such as fast-charging networks or EV

charging brands are coordinated, promoted in a cohesive way, and are accessible to all

market entrants.

10.

Identifying and mitigating emerging risks to the EV programme would be part of this

workstream. For example, EECA has already started a gap analysis to identify information

and capability needs for EVs (e.g. ensuring that the relevant parties are taking steps to

develop appropriate capacity for effective emergency response in the event of a crash

involving an EV).

Using the Electricity Levy to promote EV uptake and associated infrastructure

11.

On 2 November 2015, you asked us whether the Electricity Levy could be used to fund

measures in the proposed EV package. We have discussed this matter with EECA.

However, we understand that your office has subsequently asked the Ministry of Business,

Innovation and Employment (MBIE) for similar information by Tuesday 10 November 2015.

12.

Given that MBIE administers the legislation under which the Electricity Levy is collected, it

will lead the response to you on this issue. We are happy to provide further advice on your

direction.

1 In October 2015, EECA launched its Total Cost of Ownership tool online.

Page 3 of 14

The NZ Transport Agency’s potential role in establishing EV charging infrastructure within

The NZ Transport Agency’s potential role in establishing EV charging infrastructure within

existing GPS settings

13.

The NZ Transport Agency advises that it has already begun work to enable the faster uptake

of EVs in New Zealand. This work includes:

13.1. collaborating with the Ministry and local government to understand how it can support

charging infrastructure

13.2. co-leading work on electric vehicles in the Auckland Transport Alignment Project

13.3. undertaking environmental scanning with partners to better understand the drivers of

change in this area.

14.

The NZ Transport Agency could, without changing the current investment settings in the

GPS, undertake activities as part of the following measures in the government-industry EV

package:

14.1. clarify the regulatory framework for charging infrastructure

14.2. provide national information, guidance and promotion for public charging

infrastructure.

15.

Specifically, the NZ Transport Agency advises that it could explore a variety of initiatives,

such as:

15.1. continuing to collaborate with local government partners to develop a set of shared

standards and knowledge base on the best placement of charging infrastructure and

minimum infrastructure requirements

15.2. providing traffic pattern data to aid with the planning of charging infrastructure

placement

15.3. developing standards for signage to indicate charging infrastructure or a special

vehicle designation to ensure on-street charging infrastructure is reserved for electric

vehicles

15.4. supporting a shared procurement process for charging infrastructure to maximise

economies of scale

15.5. investigating the potential to include charging infrastructure at State highway rest

stops that are managed by the NZ Transport Agency

15.6. investigating whether it owns any unused land that could serve as a charging site

15.7. funding or co-funding enabling research

15.8. aligning the deployment of charging infrastructure installation and scheduled road

works

15.9. streamlining the process to apply for access to the State highway corridor to install

charging infrastructure

Page 4 of 14

15.10. adding charging infrastructure locations to the journey information it already provides

to customers.

Options for funding charging infrastructure from the NLTF

16.

As set out in our advice of 24 August 2015 (OC033342), we advise against funding public EV

charging infrastructure from the NLTF in the next 2 years. Nevertheless there are three ways

the NLTF can be used to fund EV charging infrastructure.

Option 1: Amend the GPS to include a new activity class to fund EV charging infrastructure

17.

The GPS would be amended to include a new activity class from which EV charging

infrastructure can be funded. This option would give greater certainty that charging

infrastructure would be funded and built than option 2 or the status quo.

18.

EV charging infrastructure projects would not have to compete with a wide range of other

land transport projects, however they would compete amongst themselves. For example, an

EV charging infrastructure project in Auckland would compete for funding against a similar

project in Christchurch. To meet value for money criteria the funding would be demand

driven and this may result in some projects not receiving funding.

19.

While you can amend the GPS, the addition of a small level of funding is contrary to the

rationalisation of activity classes smaller than $15 million annually, which was undertaken for

the current GPS. That in itself does not render this option unworkable.

20.

Option 1 would require at least a 49 percent contribution to the cost from councils’ local

share. You could issue criteria to the NZ Transport Agency to set an enhanced funding

assistance rate, which would lower the required contribution from local authorities.

21.

A new activity class may be subject to increased scrutiny and trigger a requirement to

engage with key land transport stakeholders on a variation to the GPS. If a new activity class

is included, the activity class should be enabling to ensure funding is not limited to a specific

type of project. Economic growth and productivity, road safety and/or value for money, are

specific result areas in the GPS, so there would need to be a clear line of sight between a

new activity class and these priorities.

Option 2: Amend the GPS to provide funding for EV charging infrastructure from an existing activity

class

22.

The GPS would be amended to provide funding for EV charging infrastructure from an

existing activity class, e.g. ‘local road improvements’.

23.

EV charging infrastructure projects would need to compete for funding with other projects in

the activity class and be signalled as sufficiently high priority to compete with existing

priorities. Under this option there is no guarantee that EV infrastructure projects would be

funded, or that they would meet the value for money assessment by the NZ Transport

Agency.

24.

EV charging infrastructure projects would be assessed for both their national priority by the

NZ Transport Agency and regional priority by Regional Transport Committees against other

2 A package including the briefings referred to in this paper has been separately provided to your office, so we

have not attached the documents to this briefing.

Page 5 of 14

existing priorities such as congestion relief, efficient freight links and road safety. There is a

risk that EV charging infrastructure has insufficient relative priority to be funded.

25.

However, this risk could be addressed by including strong signals and direction within the

GPS to give EV charging infrastructure priority over the existing GPS results for economic

growth and productivity and road safety. This would require a specific result area being set

within an activity class.

26.

As with option 1 a local share would be required.

Option 3: Fund EV charging infrastructure from the NLTF but outside of the GPS

27.

Section 9 of the Land Transport Management Act (LTMA) 2003 allows the Crown to utilise

land transport revenue to fund specific activities without the activities needing to participate

in the contestable funding process run by the NZ Transport Agency.

28.

Under this option, section 9 would be amended so funding for EV charging infrastructure

would be from the NLTF but be outside of the GPS. This would effectively reduce funding for

the NLTF. A small number of activities are funded in this way, such as Search and Rescue.

29.

The current specified activities have a strong user-pays link to the NLTF. For instance,

boaties pay fuel excise duty and receive the benefit of search and rescue services.

30.

EV owners, currently, do not have a strong user-pays link to the NLTF (i.e. light EVs are

exempt from paying RUC until 2020, and plug-in hybrids use less petrol and therefore pay

less fuel excise duty than conventional petrol vehicles). Nevertheless, a portion of the

registration costs for EVs do fall into the NLTF.

31.

If option 3 is progressed it may create an unhelpful precedent for other activities to be

treated in a similar manner.

General risks with funding EV infrastructure through the NLTF

32.

As value for money is a GPS priority, a cost benefit analysis would need to be completed for

EV charging infrastructure projects under all of the options. The cost benefit ratio would need

to be greater than 1 for such infrastructure to be considered for funding. This may be difficult

to achieve given the current low uptake of EVs in New Zealand, however it may improve in

the future.

33.

A broader value for money assessment would also need to be undertaken, including

assessing the policy alignment with the strategic direction of the GPS.

34.

Given EV owners currently do not have a strong user-pays link to the NLTF, there may be

equity concerns between EV owners and other vehicle owners that pay RUC and fuel excise

duties.

35.

Local government have finalised their financial commitments towards the 2015-18 National

Land Transport Programme (NLTP) and their land transport planning for the Regional Land

Transport Plans that feed into the NLTP, as required by the LTMA. Any call for a new activity

and additional local share at this time may not be accommodated without triggering

individual councils’ significance policies and require re-consultation on a variation to local

and regional financial and transport plans.

36.

The NZ Transport Agency implemented fundamental changes to the funding assistance rate

system for the 2015-18 NLTP. This simplified the funding assistance system with a single

rate for each council instead of having different rates for different activities. The NZ

Transport Agency has retained the ability to use targeted enhanced rates but sees this being

Page 6 of 14

used only in exceptional circumstances. The setting of funding assistance rates is an

independent function of the NZ Transport Agency under criteria that the Minister of Transport

may issue.

Ownership of EV charging infrastructure

37.

If the Government decided to fund charging infrastructure ownership issues would need to

be worked through, as the NZ Transport Agency requires that property and infrastructure for

which it provides public funding assistance will be in public ownership.

38.

The NZ Transport Agency would consider funding of infrastructure not in public ownership

for transport purposes but would do so only on the condition that the use of the facility for

transport purposes will endure.

Other considerations for government investment in EV charging infrastructure

39.

Our advice in March 2015 (OC02885) recommended Government support the private sector

by potentially funding, or co-funding the installation of charging infrastructure in locations

where it is not commercially viable for the market to do so.

40.

Currently, it is difficult to know when Government would intervene, and how it would be

established that a site was not commercially viable for the market to implement charging

infrastructure. This makes it difficult to estimate what level of funding would be required from

Government.

41.

The role of Government in owning EV charging infrastructure would need to be clarified.

There will be a need to set out the business case for this investment to clarify who will be

maintaining and monitoring sites. This may raise comment regarding whether it is

Government’s business to invest in infrastructure that is equivalent to a privately owned

petrol station.

The Ministry’s preferred option

42.

The Ministry considers the funding for EV charging infrastructure from the GPS or NLTF

should be included as part of the GPS 2018 developments. This will provide sufficient time

for respective policies to be developed and for any identified regulatory barriers to be

assessed.

43.

This would also provide opportunity to consider whether other EV activities should be

included within a broader EV activity or technology class in the NLTF or GPS.

44.

The biggest risk will be whether EV charging infrastructure can meet the threshold for a cost

benefit analysis or the value for money assessment against other GPS priorities that would

result in funding.

45.

The local authorities we have engaged with on the EV package do not see a need for

government to invest directly in public EV charging infrastructure. Local authorities are

already being approached by private businesses seeking consents and support to establish

charging infrastructure. At least one of the main cities is looking to encourage businesses to,

as far as possible, establish charging infrastructure off-street (i.e. shopping car parks,

parking buildings).

Page 7 of 14

Investment in infrastructure: international approaches

Japan

Investment in infrastructure: international approaches

Japan

46.

The Japanese Government has made available up to US$500 million dollars over 2 years to

support the installation of public EV charging infrastructure (both 200 volt AC chargers and

SC fast chargers). Over 10,000 chargers are already in place.

47.

Development of public EV charging infrastructure is based on ‘Deployment Plans’ set by

local authorities. The Government subsidises two-thirds of the purchase cost and a fixed

amount of the installation cost.

48.

For multi-unit dwellings (e.g. apartment blocks) the Government subsidises half the purchase

cost and a fixed amount of the installation cost.

49.

Japan operates on a 110 volt power supply3 and a high proportion of its urban populations

live in multi-unit dwellings. This increases the need for public investment in charging

infrastructure.

Norway

50.

For households in Norway, the Government offers a sales tax exemption for EVs chargers if

purchased with the vehicle itself.

51.

There are national and regional subsidies for fast chargers. These fund a percentage of the

purchase cost. The market (applicant) decides where to install the charger, and to be eligible

for the subsidy the operator must charge a fee for use.

52.

There are national, regional and local subsidies for normal EV charging infrastructure. Up to

the full cost is subsidised (around €1,250 or about NZD$2050).

United Kingdom (UK)

53.

The 2009 Plugged-in Places programme offered matched funding to a consortia of

businesses and public sector partners to support installation of EV charging infrastructure in

six local areas. The programme has since been expanded to eight new areas.

54.

Government grants are available to home owners, local authorities, and train operating

companies to install EV charging points.

55.

In 2011 the Government also published a nationwide recharging infrastructure strategy.

California

56.

The California Energy Commission provides funding for EV charging points. The Electric

Vehicle Charging Station Financing Program provides loans for the design, development,

purchase, and installation of EV charging stations at small business locations.

57.

To support home charging, new building regulations have been amended to make homes

‘EV-ready’, i.e. to encourage new homes to include charging points. This is important

because, like Japan, the US domestic power supply is low (120 volts).

3 In New Zealand domestic power supply is 230 volts.

Page 8 of 14

The link between the RUC exemption for light EVs and the targets in the proposed EV

The link between the RUC exemption for light EVs and the targets in the proposed EV

package

58.

The RUC exemption for light EVs applies until 30 June 2020. When the Government agreed

to the exemption, it was intended that the exemption would apply until 1 percent of the light

vehicle fleet was electric (approximately 30,000 vehicles). At this 1 percent threshold, the

foregone revenue from the RUC exemption would be $20 million per year.

59.

On 12 October 2015, targets for EV uptake were developed at a government-industry

workshop on the EV package. It is intended that these would be ‘NZ Inc’ targets, with central

government, local government and business sharing responsibility for achieving them.

60.

The table below sets out the targets developed with stakeholders, and estimates how much

RUC revenue is foregone due to the exemption for light EVs.

Table 1: Annual RUC revenue foregone if EV uptake targets are met (targets set at 12 October

2015 government-industry workshop)

2016

2017

2018

2019

2020

Target – annual

1,000

5,000

-

25,000

-

registrations of EVs

Projected cumulative

total EVs (if targets

1,950

6,950

14,287

39,287

58,084

met)

EVs as a % of the

0.07

0.2

0.5

1.3

1.9

vehicle fleet

Foregone RUC

1.17

4.17

8.57

23.57

36.85

revenue (in million $)

61.

Under these targets, EVs make up about 1 percent of the vehicle fleet by 2019, and almost 2

percent in 2020. This would mean a higher level of foregone revenue than was envisaged by

the Government when it agreed to the RUC exemption. The practical impact is that:

61.1. other road users would face greater increases to fuel excise duty and RUC over this

period to offset the foregone revenue, and/or

61.2. desirable transport investment may need to be reduced or delayed.

62.

On 2 November 2015, we discussed the achievability of the targets with key stakeholders.

There was general agreement that the targets developed at the 12 October workshop were

too much of a stretch to be credible beyond 2016, so two alternative sets of targets have

been proposed. These targets and their associated impact on foregone RUC revenue are set

out in Tables 2 and 3.

Page 9 of 14

Table 2: Annual RUC revenue foregone if EV uptake targets are met (doubling the number of EV

Table 2: Annual RUC revenue foregone if EV uptake targets are met (doubling the number of EV

registrations each year)

2016

2017

2018

2019

2020

Target – annual

1,000

2,000

4,000

8,000

16,000

registrations of EVs

Projected cumulative

total EVs (if targets

1,950

3,950

7,950

15,950

31,950

met)

EVs as a % of the

0.07

0.13

0.27

0.53

1.06

vehicle fleet

Foregone RUC

1.17

2.37

4.77

9.57

19.17

revenue (in million $)

63.

Under the targets set out in Table 2, EVs make up about 1 percent of the vehicle fleet by

2020 and foregone RUC revenue is within the tolerance intended by the Government when it

originally agreed to the RUC exemption.

Table 3: Annual RUC revenue foregone if EV uptake targets are met (option 3: targets as a

percentage of annual vehicle registrations)

2016

2017

2018

2019

2020

5% of

10-15% of

Target – annual

registrations

registrations

1,000

-

-

registrations of EVs

(about 12,000

(about 24,000 –

vehicles)

36,000 vehicles)

Projected cumulative

total EVs (if targets

1,950

3,709

15,709

29,863

53,863 – 65,863

met)

EVs as a percentage of

0.07

0.12

0.52

1.00

1.80 – 2.20

the vehicle fleet (%)

Foregone RUC

1.17

2.23

9.43

17.92

32.32 – 39.52

revenue (in million $)

64.

The targets in Table 3 would result in a higher level of foregone revenue than was envisaged

by the Government when it agreed to the RUC exemption.

65.

Under all the proposed targets, EVs make up 1 percent of the light vehicle fleet or more by

2020. Presently, business is most comfortable with the targets in Table 2 which, if achieved,

would keep foregone RUC revenue within expectations.

66.

If Government and industry achieved the targets in Table 1 or 3, EVs numbers would exceed

the threshold set by Government for the RUC exemption. The Government would have to

consider its options for managing the higher than anticipated revenue losses that would

occur.

The Ministry’s preferred option

67.

We favour the targets set out in Table 2 as they send a signal that Government is supportive

of a visible increase in the number of EVs in the fleet, are achievable within current

projections and have support from stakeholders.

68.

There are benefits of the percentage approach taken in Table 3, in that a target range allows

for fluctuations in the annual number of EVs available on the market. However, the exact

percentage values were not agreed by all stakeholders and would require further discussion.

Page 10 of 14

Extending the RUC exemption to heavy EVs

Extending the RUC exemption to heavy EVs

69.

In March 2015, we provided you with advice on extending the RUC exemption to include

heavy EVs (OC02885 refers). We advised against extending the RUC exemption to heavy

EVs because:

69.1. it would further compromise the user-pays basis of the transport system and mean

that the cost burden of building and maintaining the road networks would fall on a

smaller proportion of road users. This would raise equity issues, particularly among

low-income road users who are less able to afford newer, more fuel-efficient vehicle

technologies

69.2. it would exacerbate revenue pressures and consequently limit or delay desirable

transport investment because heavy vehicles do significantly more damage to the

roads, and therefore have a greater impact on road maintenance costs

69.3. the benefits of this option would be limited to operators who can reasonably adopt EV

technology, thus raising further equity concerns. With the present state of EV

technology, this is only an option for a small proportion of operators, such as urban

buses, waste collection vehicles, and some construction vehicles.

70.

Any extension of the RUC exemption to heavy EVs would require a change to the Road User

Charges Act 2012, because the power to exempt electric vehicles from paying RUC is

specifically limited to

light EVs.

71.

If the RUC exemption were extended to heavy EVs, the 80 trolley buses used in Wellington

would no longer pay RUC. This is a issue given that the Greater Wellington Regional Council

has already decided to phase these buses out based on existing policy settings.

72.

If pursued further, we would need to consult with councils and industry to consider their

views on the matter, and get a better indication of likely rates of uptake. This would inform

the projected costs of the exemption. We would also suggest limiting the scope of the

changes to reduce the risk of higher-than-expected revenue losses (for example, limiting

introducing a RUC discount for heavy passenger EVs). This would help mitigate the risks

noted above.

The proposed contestable fund and its link to EV procurement options

73.

Stakeholders agree that the price differential between EVs and equivalent conventional

vehicles is a key barrier to the uptake of EVs. From a business perspective, even when

considered on a total cost of ownership basis the lower running costs of EVs do not offset

the higher purchase price.

74.

At the 12 October 2015 government-industry workshop, the joint procurement and

contestable fund were proposed by business representatives as interrelated initiatives to

bridge the price differential.

75.

Through the joint procurement initiative, aggregated volume of demand would be leveraged

to achieve lower prices. The remaining price differential would then be ‘shared’ on a like-for-

like basis between the purchaser (industry or local/central government) and government via

a fund established for this purpose. The expectation was that these options would work

together to assist industry and government to make a better business case, based on total

cost of ownership, for the purchase or lease of EVs. Further discussion of the proposed fund

broadened it to a contestable fund, which could be accessed to fund other innovative

projects involving EVs.

Page 11 of 14

76.

Under the scenario proposed by business, the fund would act in part as a subsidy (albeit on

a cost sharing basis) for the purchase of EVs. We expect it would be likely to be

oversubscribed. Given your earlier direction on the issue of subsidies we would need to

discuss the operation of a contestable fund with you further, should you choose to progress

this option.

77.

The Government already provides a financial incentive or ‘tax break’ for EVs through the

existing RUC exemption, which is worth around $600 per vehicle per annum until 2020. It

appears the RUC exemption, which is factored into the total cost of ownership analysis, is

not sufficient on its own to bridge the price differential.

78.

The risk under this approach is that it could be difficult to justify an additional financial

incentive purely to fund the purchase or lease of a private asset, particularly if that incentive

was not available to the public at large. Another option, which could address the price

differential, is a government guarantee of residual value, which would require further analysis

if it was to be progressed further.

Numbers of EVs that fleets have already purchased, or have committed to purchasing

79.

The Sustainable Business Council has provided the information in Table 4 about uptake of

EVs by its members:

Table 4: EV uptake by some Sustainable Business Council members

Organisation

Number of EVs

Air NZ

Subject to Request for Proposal (80 vehicles – to be

confirmed)

Auckland Airport

1 EV

2 EVs; 1 EV on order and a business case is being

Auckland Council

developed that could see up to 45 purchased

Contact

18 EV

Downer

5 EVs

Kapiti Coast District Council

1 electric rubbish truck

15 EVs (plan to transition 70 percent of its fleet to

Mighty River Power

EVs by 2018. Its fleet size is about 100 vehicles)

NZ Post

14 fully electric specialist vehicles (postal delivery)

Vector

3 EVs

Total

60 EVs

80.

In addition, Wellington Electricity Lines has five EVs, Nelson-Marlborough District Health

Board has one, Northpower has six, and Christchurch City Council has three (a total of 15

between them). There may be other fleets with EVs, but we are not aware of any that have a

significant number (e.g. more than five).

81.

Christchurch City Council is currently working with four public sector organisations to scope

a shared fleet project which could potentially be a public car share scheme. Based on work

to date, Christchurch City Council estimates that it would need 100 EVs if the scheme went

ahead.

82.

[Commercial in-confidence] Auckland Transport is currently working to finalise the details for

a car share scheme using electric vehicles. The following update on progress with the

scheme has been provided by AT on a highly confidential basis:

Page 12 of 14

82.1. A provider has been selected and is planning to launch the scheme in May or June

2016, with 100 EVs. This is seen as a starting point, and if it goes well further EVs will

be added to the scheme. The cars will be able to be used by Auckland Transport and

Auckland Council staff for business and private use, as well as by members of the car

share scheme. Auckland Transport is able to source the vehicles it requires but has

not yet settled on a manufacturer.

Feedback from the Sustainable Business Council Advisory Board Meeting

83.

At its 5 November 2015 meeting, the Sustainable Business Council Advisory Board

considered the attached A3 and the targets set out in Tables 1-3 above. It:

83.1. endorsed the targets that saw annual registrations of EVs double each year to 2020

(see Table 2 above)

83.2. encouraged Government to be bold in its approach

83.3. encouraged innovative thinking on funding models, and would like to see a

comprehensive contestable fund that complemented joint procurement, and assisted

in bridging the cost gap between EVs and internal combustion equivalents

83.4. endorsed the collaborative approach between officials and business and are

supportive of continuing this.

Page 13 of 14