Report on possible government measures to encourage

the uptake of electric vehicles

Contents

Report on possible government measures to encourage

the uptake of electric vehicles

Contents

Purpose of report ................................................................................................................................ 2

Useful terms ........................................................................................................................................ 2

Transport greenhouse gas emissions in New Zealand ....................................................................... 3

Percentage fuel used on the roads in New Zealand (2013)................................................................ 3

The New Zealand vehicle fleet: challenges to growing the market for electric vehicles ..................... 4

Electric vehicles in New Zealand – policies and uptake ..................................................................... 5

Current projections for electric vehicle uptake .................................................................................... 6

What are the opportunities and barriers for electric vehicles? ............................................................ 7

Criteria used to assess potential measures ........................................................................................ 9

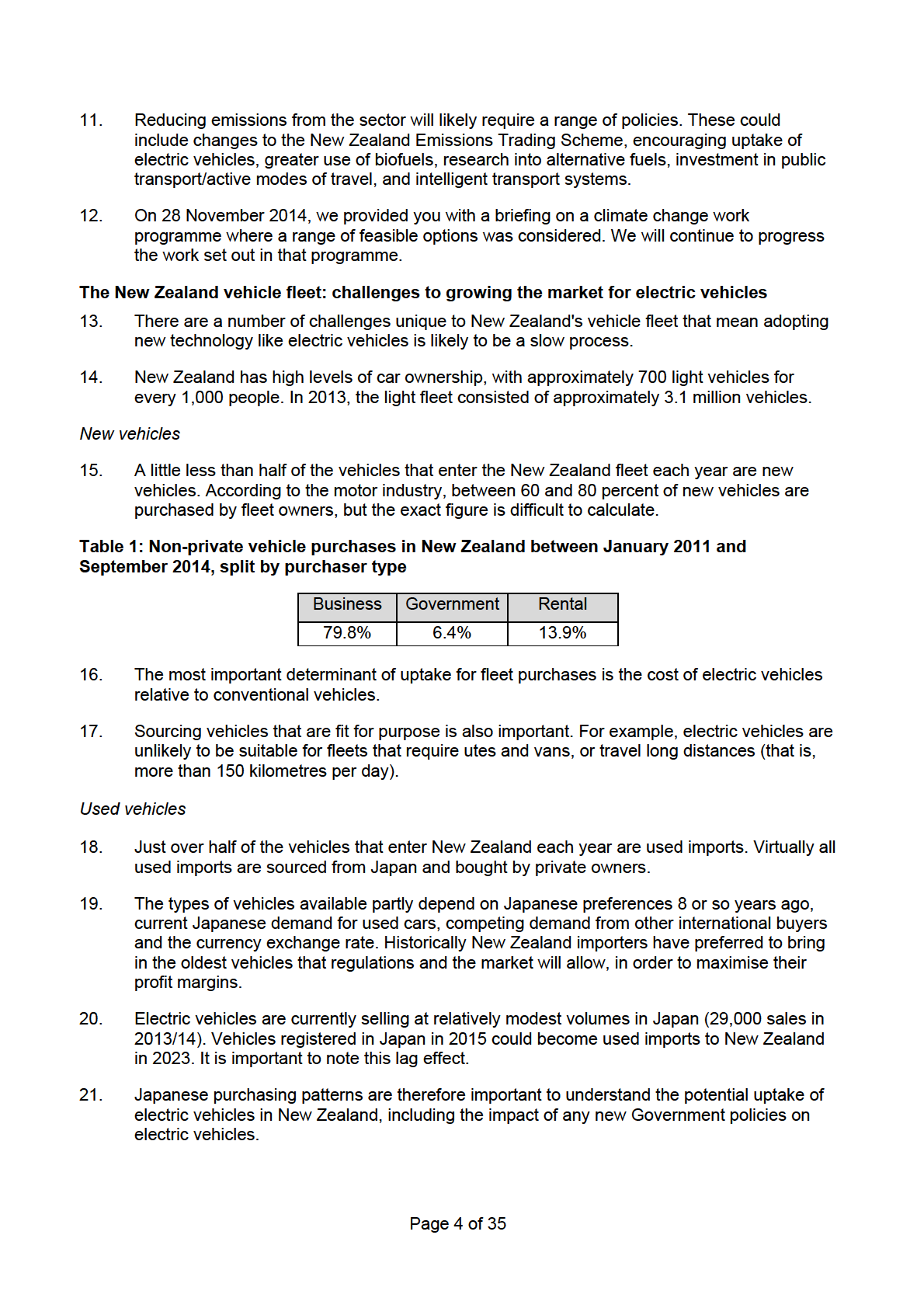

Measures that we recommend be investigated further for inclusion in a package ........................... 10

Measure 1: Energy Efficiency and Conservation Authority (EECA) information and promotion

campaign ....................................................................................................................................... 10

Measure 2: Government support for charging infrastructure ......................................................... 12

Measure 3: Government fleet procurement of electric vehicles .................................................... 14

Measures that could be investigated further ..................................................................................... 17

Measure 4: An electric vehicle programme to co-fund initiatives with other parties ...................... 17

Measure 5: Electric vehicles in bus and transit lanes.................................................................... 19

Measure 6: Road User Charges (RUC) exemptions and discounts for electric vehicles .............. 22

Measure 7: Fringe benefit tax on electric and hybrid vehicles ...................................................... 26

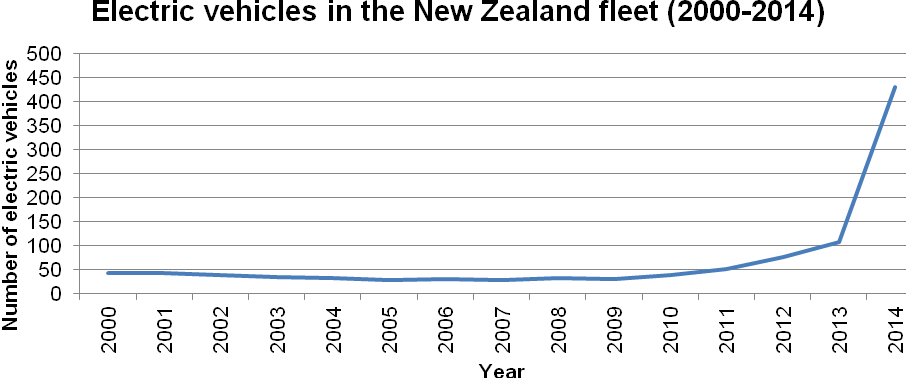

Measure 8: Tax depreciation rates for electric vehicles ................................................................ 28

Measures to be progressed outside of the package ......................................................................... 29

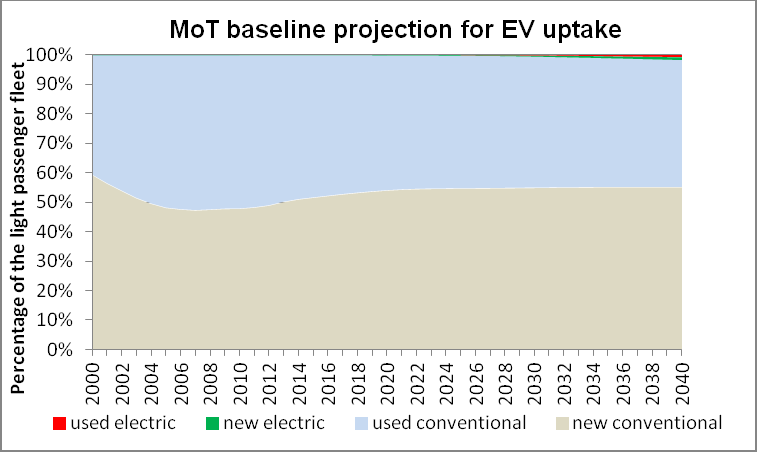

Measure 9: Amending ACC levies for plug-in hybrid electric vehicles (PHEVs) ........................... 29

Measure 10: A Road User Charges (RUC) rate for plug-in hybrid electric vehicles (PHEVs) ....... 31

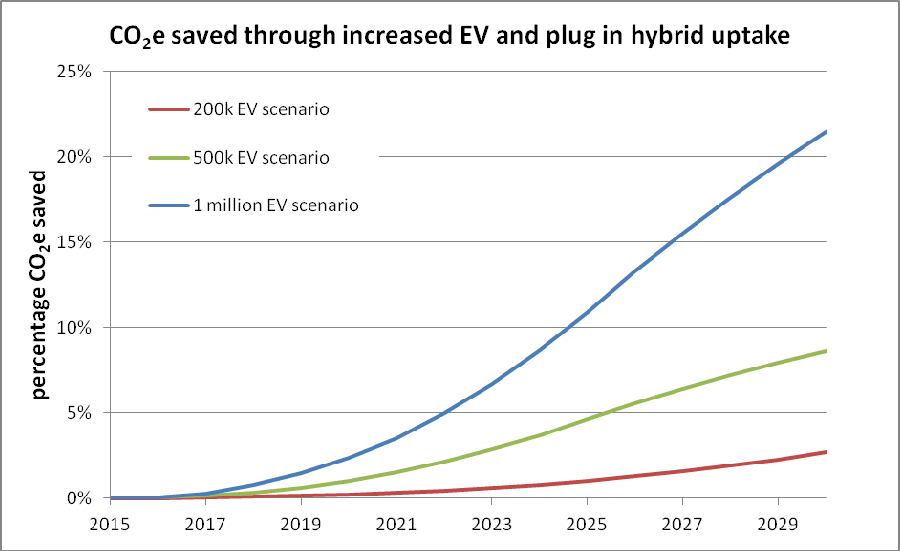

Measure 11: Removing battery import duties................................................................................ 32

Measure 12: A feebate scheme to encourage purchase of low emission vehicles ....................... 33

Measure 13: Recognition of alternative low emission vehicle designs .......................................... 34

Measures that were not considered worth progressing .................................................................... 35

Measure 14: Lower registration and annual vehicle licensing fees for electric vehicles ............... 35

Measure 15: GST exemption for second hand electric vehicles ................................................... 35

Page 1 of 35

Purpose of report

Purpose of report

1.

This report outlines the potential role of electric vehicles in helping New Zealand reduce its

greenhouse gas (GHG) emissions from transport.

2.

It provides you with advice on a range of measures that could form a package to encourage

the uptake of electric vehicles in New Zealand.

3.

Our advice is divided into four categories of potential measures that:

3.1.

we recommend be investigated further for possible inclusion in a package

3.2.

could be investigated further for possible inclusion in a package

3.3.

should be progressed outside of the package

3.4.

were not considered worth progressing.

Useful terms

4.

Pure electric vehicle – a vehicle powered solely by electric batteries charged from an

external source.

5.

Plug-in hybrid vehicle (PHEV) – a vehicle that operates on a combination of batteries that

are charged externally, along with petrol or diesel motors.

6.

Electric vehicle – either a pure electric vehicle or a PHEV.

7.

Hybrid vehicle – a vehicle that has an internal battery but cannot be directly plugged in, and

must have petrol or diesel to run.

8.

Light vehicle – a vehicle with a maximum gross mass of 3.5 tonnes or less.

Page 2 of 35

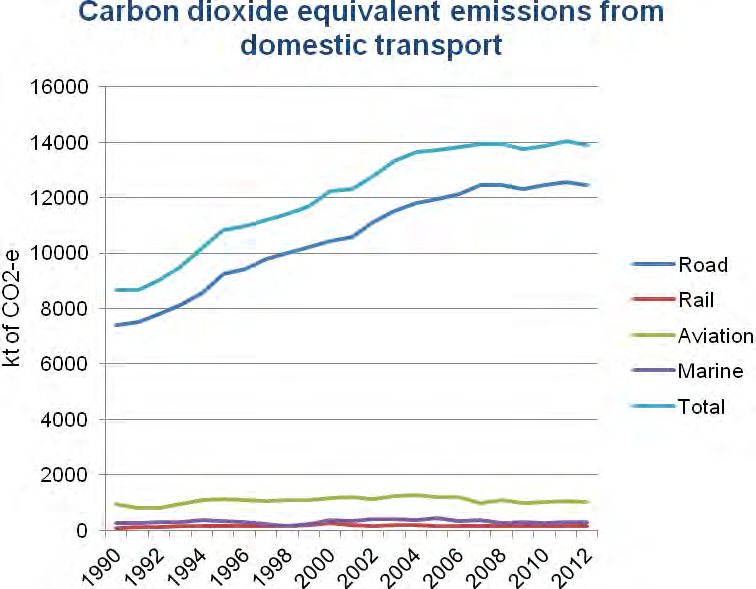

Transport greenhouse gas emissions in New Zealand

Transport greenhouse gas emissions in New Zealand

9.

In 2012, the transport sector accounted for 18 percent of New Zealand’s emissions. Of this,

89 percent was from road transport and the remainder from domestic aviation, marine and

rail.

10.

Light passenger vehicles emit the majority of road transport GHG emissions. While making

up only 4 percent of the vehicle fleet, heavy vehicles use almost 21 percent of the total fuel

used in New Zealand.

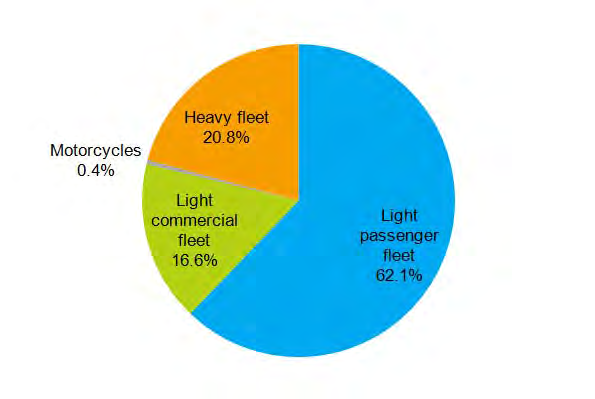

Percentage fuel used on the roads in New Zealand (2013)

Page 3 of 35

Turnover of the fleet

Turnover of the fleet

22.

The speed at which the make-up of the light vehicle fleet can be changed is driven by the

fleet turnover. This is difficult to predict accurately, but on average over the last decade 7.1

percent of light vehicles enter the fleet each year. New Zealand has an aging fleet by

Organisation for Economic Co-operation and Development (OECD) standards. In New

Zealand, the average lifespan of a car is 20 years, and about 5.5 percent of the light fleet is

scrapped annually.

Electric vehicles in New Zealand – policies and uptake

23.

In New Zealand, measures have already been implemented to promote the uptake of low

emission vehicles generally, which have an impact on the uptake of electric vehicles. These

include:

23.1. the New Zealand Emissions Trading Scheme, which establishes a price on emissions

that flows through to the cost of petrol (the current price signal is weak)

23.2. the fuel economy labelling scheme

23.3. electric vehicles being exempt from road user charges (RUC) until 2020.

24.

Recent data indicates that the average emissions performance of light vehicles entering the

fleet is improving. In 2013 it was 183 grams of carbon dioxide (CO2) per kilometre, down

from 220 grams per kilometre in 2005.

25.

However, these initiatives have had limited impact on uptake of low emission vehicles to

date. While the numbers of electric and hybrid vehicles are increasing, they currently make

up 0.32 percent of the total vehicle fleet (electric vehicles only make up 0.02 percent of our

total fleet).

Page 5 of 35

Current projections for electric vehicle uptake

Current projections for electric vehicle uptake

26.

There are serious challenges in providing accurate projections for electric vehicle uptake in

New Zealand given the high level of uncertainty around a number of factors that will

influence uptake. Uncertainties include:

26.1. the rate that the prices of electric vehicles will fall

26.2. the extent to which battery prices will fall

26.3. trends in the cost of other energy sources

26.4. trends in the price imposed on carbon emissions

26.5. the future of the RUC exemption

26.6. the availability of used electric vehicles into the New Zealand market (half of light

vehicle registrations in New Zealand are used vehicles).

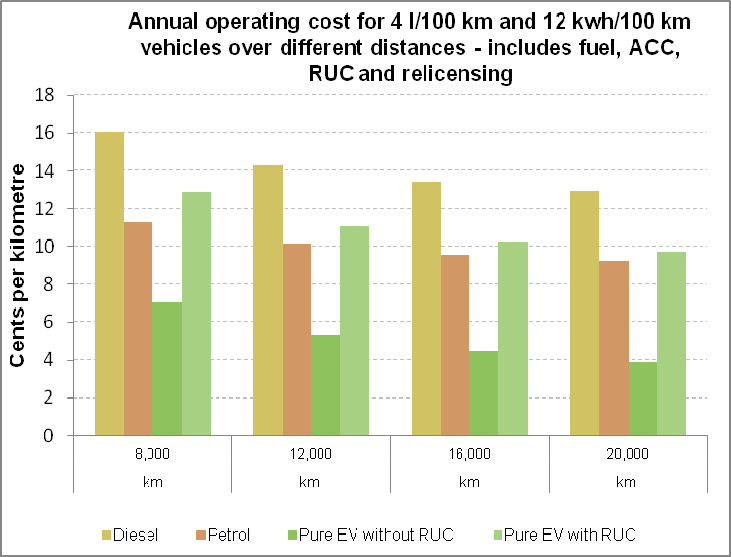

27.

The Ministry of Transport ran one baseline projection of electric vehicle uptake (below). This

forecasts that electric vehicles will account for 1 percent of the vehicle fleet by 2035 and 2

percent by 2040. This baseline scenario is based on electric vehicle uptake trends to date. It

assumes no significant changes in policy, the price of electric vehicles, or any relevant

external shocks.

28.

We have not been able to analyse how the measures identified in this report could affect the

Ministry of Transport’s baseline projection. We have instead provided a qualitative analysis

of the impact we expect each measure could have on addressing market failures and

regulatory barriers to uptake (Appendix B to the cover briefing).

Other modelling work

29.

We have also undertaken some modelling work for the Ministry for the Environment, in

response to a query by the Minister for Climate Change Issues, asking what impact 1 million

electric vehicles in fleets have on reducing CO2 emissions.

30.

We assumed a range of scenarios where electric vehicles made up approximately 200,000,

500,000, and 1 million vehicles in the fleet and modelled the corresponding effect on carbon

emissions (see the graph below).

Page 6 of 35

31.

The scenarios depicted below were not based on any specific assumptions about changes in

policy or the cost of electric vehicles. No analysis was undertaken to identify the conditions

or policy pathways that would be needed for these scenarios to be realised.

32.

Ministers may also be aware of some electric vehicle scenario work undertaken by the

Ministry of Business, Innovation and Employment (MBIE) as part of the Smart Grid Forum.

MBIE assumed a scenario where electric vehicles saturate the market by 2028. This was

done exclusively to test what impact this level of uptake would have on the distribution

network. This scenario was not based on a likely scenario for electric vehicle uptake, or a

particular policy pathway. The scenario would be extremely unlikely to occur given the

constraints on used imports discussed above.

What are the opportunities and barriers for electric vehicles?

The opportunity

33.

As well as reducing emissions, increased uptake of electric vehicles can bring other benefits

such as reducing our reliance on imported fossil fuels, and enhancing the efficiency of

renewable electricity networks.

34.

New Zealand is well positioned to benefit from electric vehicles because:

34.1. we have high levels of renewable electricity generation (currently 78 percent), with

capacity to increase the energy demand on renewables via electric vehicle uptake

34.2. 95 percent of daily travel demand is for distances less than 120 kilometres, which is

within the range of electric vehicle batteries (currently approximately 150 kilometres

per charge)

34.3. we do not need major investment in infrastructure – domestic power supply is

suitable for charging at home, and 80 percent of homes have off-street parking.

Page 7 of 35

35.

We previously advised that any policies dependent on the turnover of the vehicle fleet may

be effective at reducing emissions over a very long-term, but are unlikely to make a

significant contribution to New Zealand’s 2020–2030 emissions reduction target.1 Therefore

adopting a package of measures to achieve higher electric vehicle uptake represents an

investment for the long-term, and may assist in the achievement of longer-term emissions

targets.

Barriers to uptake

36.

High upfront costs – although some models are becoming cost-competitive, the average

upfront costs of electric vehicles are generally higher than conventional vehicles, and

consumers are not recognising their additional associated value.

37.

Limited range – pure electric vehicles are not suited to long journeys (over 150 kilometres)

without stops to recharge the vehicle. There is a strong body of research that private citizens

highly value the ability to travel long distances, even if very occasionally.

38.

Few electric models are available in New Zealand – only a small range of models are offered

in the New Zealand market currently.

39.

Supply of used electric vehicles is likely to be constrained in the foreseeable future – uptake

of electric vehicles in Japan is expected to be low in the foreseeable future. Further,

Japanese policies mean electric vehicles do not depreciate as quickly as conventional

vehicles so they are not on-sold into the second-hand market as quickly. These factors may

consequently limit the supply of used electric vehicles in New Zealand in the future.

Government’s role in overcoming these barriers

40.

Government is limited in what it can directly do to address the barriers above. In some cases

intervention may not be required as existing barriers may reduce themselves through cost

reductions and improved battery technology over time.

41.

There is a clearer role for government intervention to address market failures affecting

uptake, such as in helping to resolve:

41.1. coordination problems, for example, addressing any issues to ensure that the

necessary infrastructure is in place ahead of demand in order to encourage uptake

41.2. information problems, for example, lack of awareness and misconceptions about

electric vehicles, and uncertainty about the total cost of ownership (including

maintenance costs, battery life and residual values)

41.3. trade barriers, for example, the removal of import duties on a broad range of

environmental goods (which could include electric vehicles and batteries) in the

context of the negotiations towards a global Environmental Goods Agreement in the

World Trade Organization (WTO).

42.

As well, we have identified several instances of possible regulatory failure (for example, ACC

levies and road user changes for PHEVs). Left unaddressed, these regulatory failures may

‘nudge’ motorists away from choosing electric vehicles.

1 Our modelling indicates that doubling the uptake rate of electric and hybrid vehicles over the next 25 years (compared to

business-as-usual baseline) could result in emissions reductions of 7 percent in the transport sector by 2040.

Page 8 of 35

Criteria used to assess potential measures

Criteria used to assess potential measures

43.

A set of standard criteria was used to assess the merits of potential measures in accelerating

the uptake of electric vehicles as a means to reduce transport GHG emissions.

43.1. Effective – the measure will achieve a reduction in transport GHG emissions. This

includes securing a reduction that is sustained long-term.

43.2. Efficient – the measure will take account of:

43.2.1. purchase, implementation, and maintenance costs for individuals, businesses

and government

43.2.2. compliance costs and government administration costs.

43.3. Equitable – the measure addresses distributional impacts between high income

households and low income households, and maintains the principle that system use

and costs imposed determine who pays and at what level.

43.4. The measure maximises co-benefits (for example, increasing air quality) and

minimises co-costs (for example, increasing the pressure on freshwater ecosystems).

43.5. The measure encourages private sector activity and investment with government

intervention only occurring where there is an identified market or regulatory failure.

43.6. The measure helps New Zealand transition to a long-term low-emissions transport

sector.

Page 9 of 35

Measures that we recommend be investigated further for inclusion in a package

Measures that we recommend be investigated further for inclusion in a package

44.

Listed below are the measures that we recommend are prioritised for further investigation.

Our initial analysis suggests these measures are the most viable for inclusion in a package

to encourage the uptake of electric vehicles.

Measure 1: Energy Efficiency and Conservation Authority (EECA) information and promotion

campaign

We recommend any package includes an information and promotion campaign as a central

component. A campaign would help address information barriers and enhance the visibility of other

measures to address barriers to uptake of electric vehicles. Given that vehicle fleet turnover is a

long-term option for reducing GHG emissions, we recommend pursuing a campaign that seeks

long-term change (this would require funding of approximately $1.7 million per year, for 5 years).

45.

Many motorists are either unaware of, or hold misconceptions about electric vehicles and

their operation. Electric vehicles are a relatively new technology that is not well understood

or accepted by potential buyers.

46.

The Sustainable Business Council has also cited a “lack of awareness of electric vehicles by

corporate fleet managers and staff that have vehicles as part of their salary package” as a

barrier to uptake. We are undertaking research with EECA to better understand the

information barriers that exist among fleet buyers.2

47.

We consider an ideal information and promotion campaign is one that supports the long-term

change in perceptions and understanding of electric vehicles, which is necessary to

maximise GHG reductions from uptake.

48.

Such a campaign would need to target the market segments most likely to respond to

information and promotion in the first instance (for example, fleet owners, lease companies,

large businesses, and government agencies). Public information would focus on dispelling

misconceptions.3 Building long-term relationships with business and local government would

provide opportunities to develop joint measures and share learnings between stakeholders.

This level of commitment would send a strong signal to business and local government

about the Government’s long-term support for electric vehicles.

49.

EECA has the mandate and capability to deliver this kind of information and promotion

campaign. EECA has identified the elements of a comprehensive campaign that seeks long-

term consumer change and addresses barriers to uptake. The campaign would run for 5

years and cost $1.7 million per year. This could require a new budget initiative. The funding

would enable EECA to:

49.1. run a high profile media and advertising campaign

2 EECA has engaged with a number of major light vehicle fleet owners (including Downer, Opus and Fonterra) to better

understand barriers to the uptake of electric vehicles from a fleet buyer’s perspective. A key barrier is a lack of information

on the total cost of ownership. In response to this, EECA is working on a “total cost of ownership” tool to help fleet

managers compare the total costs of owning and operating an electric vehicle with an equivalent petrol or diesel vehicle,

so that fuel and maintenance savings can be readily taken into account.

3 For example, EECA’s engagement with fleet managers (and the public) has identified misconceptions about the

environmental performance of electric vehicles as a barrier to uptake. To this end, EECA is engaging a consultant to

undertake a lifecycle analysis of electric vehicles in the New Zealand context, to provide authoritative information that can

be easily communicated.

Page 10 of 35

49.2. directly market to, and build long-term partnerships with, corporate fleet managers

49.3. undertake joint measures with private sector companies and local government.

50.

This campaign is scalable and could be delivered with a more limited reach over a shorter

time frame (for example, 2 years) for a cost of $1.2 million per year.

51.

Any campaign would also be used to inform consumers of other measures within the

package that address barriers to uptake (for example, the RUC exemption for light electric

vehicles).

52.

We recommend any package to support the uptake of electric vehicles should involve an

information and promotion campaign. We consider a longer-term and more comprehensive

campaign is best suited to the dynamics of the New Zealand vehicle market, particularly as

the majority of new vehicles are purchased for fleets before entering the second-hand

market 3 to 5 years later.

53.

We consider the smaller, lower cost campaigns would still have merit, but would also have

fewer benefits over the long-term. The signal sent to industry would also be weaker.

Page 11 of 35

Measure 2: Government support for charging infrastructure

Measure 2: Government support for charging infrastructure

We recommend that the Government supports the private sector to establish a cohesive network of

fast-charging stations by:

offering branding and promotional support to facilitate a cohesive network

providing independent advice to local government and other independent investors about

appropriate recharging infrastructure

potentially funding, or co-funding the installation of fast-charging stations in locations where

it is not commercially viable for the market to do so.

A new budget bid would be required to request Crown funding for this option. Alternatively, should

you progress measures 1 and 4, funding for charging infrastructure (promotion and installation)

could be drawn from the proposed EECA promotional campaign and electric vehicle programme.

54.

As in other countries, the majority of electric vehicles are likely to be charged during

overnight parking, predominantly in homes. In addition, 95 percent of all journeys in

New Zealand are less than 120 kilometres, well within the range of electric vehicles. We

anticipate that range will improve with battery technology over the coming years.

55.

Nevertheless, charging infrastructure will still be required to offset range anxiety and

enhance the versatility of electric vehicles.

56.

Evidence from jurisdictions such as Oregon (USA) suggests that public charging

infrastructure increases the utility, and therefore value, of electric vehicles. Without a

charging infrastructure network, electric vehicles are only useful within a radius of 50 percent

of their range. A network of fast-charging facilities means that electric vehicles can travel

further if required. This makes them appealing to a larger segment of the car-buying

population.

57.

The Electricity Networks Association has announced plans to study if a ‘renewable highway’

providing a nationwide infrastructure for charging is possible.

58.

On 12 February 2015, officials met with Mighty River Power (MRP) and the Sustainable

Business Council. [Commercial in-confidence] MRP advised us that it plans to partner with

other electricity industry players to invest in a ‘renewable highway’. The ‘renewable highway’

is a network of fast-charging stations that will form a network from which other charging

infrastructure could expand. We understand that MRP considers that this measure can be

entirely funded by industry. MRP intends to establish these charging stations at locations

where motorists would logically stop on a long journey (for example, shopping areas, tourist

attractions).

59.

Other parties (such as JuicePoint and the private equity group behind Charge.net.nz) are

also looking to provide more charging infrastructure. This does not require Crown funds.

60.

There may be a role for government in ensuring the network is cohesive. For example, there

may be locations where charging infrastructure is not commercially viable to install, but

necessary to complete a cohesive network. Easy identification of charging stations and the

standardisation of various systems may also be an issue if multiple businesses are installing

fast-charging stations.

Page 12 of 35

61.

We understand that a number of local councils and other players that are looking to install

charging infrastructure are seeking independent advice about what charging facilities they

should install. There would be value in government filling this gap.

62.

We considered the following options for government support for charging infrastructure.

Option 2.1 – government branding and information support for charging infrastructure.

Option 2.2 – inclusion of charging infrastructure in large State highway projects.

Option 2.3 – government providing funding for charging infrastructure to fill gaps in the

network.

Assessment of the options

63.

Option 2.1 is preferred. Under this option, the market decides the most appropriate locations

for fast-charging infrastructure. The cost of providing branding and information support could

be covered by EECA as part of the information and promotion campaign (see page 10 of this

report). If set up as a stand-alone programme, a budget bid may be required to request

Crown funds.

64.

EECA could potentially play an advisory and coordination role in supporting these

independent players. The NZ Transport Agency advises that it could assist by providing

access to Crown land and transport planning advice.

65.

Option 2.2 is not preferred because motorists are unlikely to consider it desirable or safe to

charge their vehicles on the roadside (for example, motorists would prefer to do something

productive during charging times). The cost of creating a safe area for motorists to charge

their vehicles along State highways would be much higher than installing charging

infrastructure at existing parking facilities.

66.

Option 2.3 would be more effective once we have an indication of where the gaps in the

network are that cannot be filled by the market. The Government could fund (or co-fund)

charging infrastructure under the proposed electric vehicle programme (see page 17).

Page 13 of 35

72.3. Electric vehicles remain unattractive to many fleet managers for practical reasons,

such as the need to ensure pool cars are charged for the next user, ensuring that

electric vehicles have sufficient range for employees’ day-to-day activities, and that

employees have access to charging facilities.

73.

The current AoG contract is due to expire on 30 June 2015 and the new contract has the

potential to be in place for the next 10 years. The criteria for vehicle inclusion in the

catalogue are expected to stay much the same, and as a result electric vehicles are highly

unlikely to be included in the catalogue under the status quo.4

Options considered

74.

Potential options to facilitate the uptake of electric and other low emission vehicles into the

government fleet include the following.

Option 3.1 – the Government funding a trial of electric vehicles within government agency

fleets. An indicative cost for such a trial would be around $500,000 (and potentially cost

neutral over time). This level of funding would cover the additional purchase costs for around

24 electric vehicles or PHEVs in four government fleet locations around New Zealand. It

would also cover the risk to fleet managers of any lower residual value at on-sale, the cost of

installing charging facilities, and costs associated with project management, research and

monitoring.

Option 3.2 - requiring MBIE to include a specific class in the AoG catalogue for electric and

hybrid vehicles.

Option 3.3 – providing greater information in government fleet managers’ guidelines

regarding electric vehicles.

Option 3.4 – amending government procurement guidelines to require a set percentage of all

vehicles purchased by government fleets to be electric.

Option 3.5 – the Government guaranteeing agencies a residual value on the resale of all

electric vehicles purchased through the AoG vehicle catalogue. Government would

guarantee an on-sale price that would make electric vehicles competitive with other vehicles

vying for inclusion in the catalogue.

Option 3.6 – choosing electric vehicles for some or all Crown limousine replacements and

ministerial self-drive cars.

Assessment of the options

75.

Option 3.1 is the preferred option. A trial could fill information gaps around the whole-of-life

cost associated with electric vehicles, and demonstrate their functionality in New Zealand

fleets. This information would help to inform government and corporate fleet purchasers

about key uncertainties, such as likely resale value, and maintenance and replacement

costs, and therefore reduce risk. The visibility of a trial by government could complement a

government information campaign by normalising electric vehicles and dispelling myths

associated with electric vehicles.

76.

MBIE and EECA have expressed their willingness to support the development of a trial

scheme, in terms of developing parameters, providing comparative cost data, and identifying

willing government agencies to participate.

4 Inclusion in the catalogue is determined by an expert procurement panel.

Page 15 of 35

77.

Further discussions would be needed to determine who would administer and manage this

trial. MBIE would also work with the AoG contracted suppliers on the supply of electric

vehicles. While some contracted suppliers are manufacturing electric vehicles globally, these

are not being imported into New Zealand due to the current low demand for these types of

vehicles.

78.

There is some risk associated with this option. The unknown costs around electric vehicles

(that is, on-sale value, maintenance and replacement costs), which this trial is trying to

identify, also risk increasing (or decreasing) the costs of this trial.

79.

Option 3.2 (including a specific class for electric and hybrid vehicles in the catalogue) is also

recommended. This would make electric and hybrid vehicles more visible to government

fleet managers and nudge them to consider them as a viable option. It would ensure that

manufacturers that sell electric vehicles are included in the AoG contract so that lower prices

for electric vehicles can be negotiated. This measure would place some cost on MBIE, which

may have to run an additional tender process for this specific class.

80.

Option 3.3 would provide a low cost way of encouraging uptake of electric vehicles in the

government fleet. However, without information relating to the whole-of-life costs (that option

3.1 will seek to generate), this would have limited effect.

81.

Option 3.4 is potentially viable but it is a higher risk option. We do not know how government

agencies use their vehicles so a prescribed level of uptake risks burdening agencies with

vehicles that do not fit their needs (that is, typical driving distance or pooling arrangements).

This approach could also present a financial risk to agencies and government given the

unknowns around the supply of affordable electric vehicles, the on-sale value of these cars,

and maintenance costs (all unknowns that a trial would seek to inform). This option would

require adjustments to the AoG solution, but MBIE advises that the new contract scheduled

from 1 July 2015 will be flexible enough to allow for any such change.

82.

Option 3.5 could be effective for incentivising wider uptake of electric vehicles in the

government fleet. It could also offer a simplified approach to financing option 3.4. It removes

the risk for government fleet purchasers of on-sale value being unknown, and provides

useful information about whole-of-life cost for private fleet purchasers. However, this option

presents a financial risk to government and similar information about electric vehicle on-sale

value could be gained from a lower risk trial (option 3.1).

83.

Option 3.6 would not be viable at this time as MBIE has already begun the tender process

for Crown limousine replacements. We understand that the tender document includes the

following wording to encourage the inclusion of electric vehicles in the tender process:

“If it

meets all the requirements electric vehicles would be welcomed.”

Page 16 of 35

Measures that could be investigated further

Measures that could be investigated further

84.

The measures below could be initiated in the short-term (next 2 years). You may wish to

consider which, if any, of these options should be progressed as part of a package to

encourage the uptake of electric vehicles.

Measure 4: An electric vehicle programme to co-fund initiatives with other parties

We could investigate the establishment of an electric vehicle programme that would co-fund projects

that encourage the uptake of electric vehicles. This option would encourage businesses and local

communities to develop projects to address the market failures/barriers that are limiting the uptake

of electric vehicles. This would require a new budget bid.

85.

In addition to government, there are other parties that have an interest in encouraging

uptake of electric vehicles, including the electricity sector, manufacturers of electric vehicles,

businesses seeking to reduce their fuel costs and GHG emissions, and local government.

86.

An electric vehicle programme could be used to bring together the efforts of these parties

over a focused period of time. The programme could be used to ensure that the sum of

efforts to encourage uptake of electric vehicles is maximised by having a greater degree of

visibility and coherence. This programme would be distinct from the EECA promotional

campaign.

87.

Under this option, local government and private sector organisations would be incentivised to

develop and implement their own projects aimed at increasing the uptake and use of electric

vehicles. They would apply to have their project co-funded and an investment group would

assess the projects against a set of agreed criteria. The investment group would be

responsible for ensuring that the projects represent value for money and contribute to the

objective of lowering GHG emissions through the uptake of electric vehicles.

88.

The advantage of this approach is that it encourages innovation by giving local government

and private sector organisations the flexibility to determine the types of projects that are most

appropriate for particular market conditions and/or their local communities.

89.

The co-funding approach encourages partnership by giving both parties the incentive to

ensure that projects are value for money, and achieve the desired outcomes of encouraging

uptake of electric vehicles and reducing GHG emissions.

90.

Examples of the type of projects that could be funded by an electric vehicle programme

include:

90.1. trials of electric buses on urban public transport routes

90.2. installation of public fast-charging infrastructure at locations where it is not

commercially viable for the market to do so, but is necessary to form a cohesive

network

90.3. creation and promotion of branded tourism routes (for example, where tourists can

hire electric vehicles, and preferentially park and charge the electric vehicle at tourist

attractions, cafes and accommodation along the route)

90.4. demonstrations of vehicle types not currently offered in New Zealand (for example,

electric vans for use by trade employees in business fleets).

Page 17 of 35

91.

Auckland Transport’s recent announcement of a Request for Proposal from car share

operators to launch an electric vehicle scheme in Auckland is also an example of the type of

project that could be co-funded through an electric vehicle programme.

Details that would need to be considered

92.

Details of an electric vehicle programme that would need to be determined include the

following:

92.1. The level of funding made available, and over what period – the level of funding could

vary significantly depending on the level of ambition assigned to the programme. As

an example, a programme in the order of $2 million over 2 years could be used to co-

fund 8 to 10 trials, demonstrations or small infrastructure projects (for example,

charging stations).

92.2. Co-funding rates for projects – we consider that a maximum co-funding rate of 50

percent would give both parties the appropriate incentive to ensure that the projects

were effective and value for money.

92.3. Which government department or agency is primarily responsible for administering

the fund.

92.4. Composition of the investment group – the group would ideally be comprised of

representatives of central and local government, industry and users.

92.5. Eligibility and criteria for funding – these would be decided by ministers.

92.6. Appropriate level of oversight for allocation decisions – this would depend on the

level of funding for the programme and the potential cost of individual projects.

93.

Our recommendation is to consider this option. The Ministry of Transport, NZ Transport

Agency, and EECA have experience in dealing with similar programmes, and can assist in

the development and administration of an electric vehicle programme.

Page 18 of 35

Measure 5: Electric vehicles in bus and transit lanes

Measure 5: Electric vehicles in bus and transit lanes

Consideration could be given to investigating the removal of regulatory barriers preventing road

controlling authorities from allowing electric vehicles in bus and transit lanes.

94.

Allowing electric vehicles access to bus and transit lanes is a relatively low cost incentive to

encourage uptake of electric vehicles and bring forward GHG emission reductions. This

particular measure is perceived by drivers to be of high value relative to other common

electric vehicle incentives. In Norway this incentive was a key part of changing consumer

opinion about electric vehicles.5

95.

In New Zealand, priority vehicle lanes exist in two main forms: as transit lanes (for example,

T2 and T3 lanes), which prioritise private vehicles carrying multiple passengers; and as bus

lanes, which primarily prioritise public buses.

96.

Priority lanes run along congested arterial roads in urban areas and are intended to reward

forms of travel that make a stronger contribution to network efficiency. Priority lanes offer

time savings, which provide strong incentives for travel behaviour change.

97.

Under the Land Transport (Road User) Rule 2004 (the Road User Rule), road controlling

authorities (RCAs) are restricted from granting electric vehicles access to priority lanes. This

incentive is therefore not currently possible without changes to the Road User Rule and

related provisions in Land Transport Rule: Traffic Control Devices 2004.

Background

98.

At present, transit lanes only exist in Auckland. They operate in two forms.

98.1. As ‘priority lanes’ at on-ramps onto the motorways, where vehicles with two or more

people can bypass the on-ramp signal lights during congested periods and enter the

motorway ahead of other traffic.

98.2. As ‘T2 or T3 lanes’. These operate on arterial roads during peak hours and are

reserved for cars with two to three or more people.

99.

Bus lanes exist along main arterial roads in most of New Zealand's main urban centres.

100. The NZ Transport Agency is a RCA and manages priority lanes on the Auckland motorway.

RCAs, like Auckland Transport and Greater Wellington Regional Council, have responsibility

for determining bus lane location and identifying vehicles that can and cannot use the lanes.

101. Providing electric vehicles access to priority lanes would likely provide an incentive for

ownership. However, there is limited data available to identify what time savings are

necessary to influence electric vehicle uptake. In the USA, there is evidence that policies

allowing access to transit lanes have positively influenced the uptake of electric and hybrid

vehicles.6 NZ Transport Agency research shows a fairly strong relationship between travel

5 Sourced from a 2014 presentation by Norwegian Transportokinomisk Institutt, on ‘Electrification of road transport in

Norway’, slide 9.

6 See two USA studies: (2014)

Evaluation of State-level U.S. Electric Vehicle Incentives, The International Council on

Clean Transportation, p.26; and (2008)

Impact of High Occupancy Vehicle (HOV) Lane incentives for Hybrids in Virginia,

Journal of Public Transportation, vol. 11, no.4, p.52.

Page 19 of 35

time savings offered by bus and car pool lanes and a shift from car to buses or high

occupancy vehicles.7

102. Allowing electric vehicles to access priority lanes will inevitably have some impact on other

transport objectives. Priority lanes are typically implemented for network efficiency purposes,

and the inclusion of electric vehicles in such lanes is likely to impact on public transport

reliability and general congestion as electric vehicle numbers grow. However, without RCAs

modelling specific corridors, it is not possible to know the precise effects of this incentive,

either for electric vehicle uptake or on other transport objectives.

103. In Auckland, the Onewa Road T3 lane offers a travel time saving of around 20 minutes (this

resulted in a 120 percent increase in the share of high occupancy vehicles). The priority

lanes on on-ramps offer time savings between 2 and 5 minutes and have resulted in only a

small increase in high occupancy vehicles.8

104. Many bus lanes in New Zealand may not offer a real time saving to car drivers, given the

stop-start nature of buses operating in them. The NZ Transport Agency has also advised that

the four main corridors with bus lanes in Auckland are expected to be congested within 1 to

3 years. This suggests there are limited opportunities to provide electric vehicle drivers with

real time savings via bus lanes. Nevertheless access to bus lanes is likely to remain an

incentive for electric vehicle uptake as it provides the perception of priority access.

Options

105. The options considered were:

option 5.1 – amending existing legislation to allow electric vehicles automatic right of access

to all bus and transit lanes

option 5.2 – amending existing legislation to enable RCAs to determine which bus and transit

lanes electric vehicles can access.

Assessment of the options

106. If this measure is pursued, option 5.2 is preferred. Under this option the Ministry of Transport

would consider options for amending legislation to give RCAs the power to allow electric

vehicle access to specific bus and transit lanes. RCAs would retain the power to exclude

electric vehicles from bus and transit lanes should they choose to do so.

107. This option provides RCAs with the flexibility to choose which bus and transit lanes electric

vehicles can access. This flexibility would allow RCAs to manage conflicting transport

priorities along a corridor, including electric vehicle promotion and network efficiency.

108. There is a risk that this option would not result in electric vehicles having access to bus and

transit lanes. It is the NZ Transport Agency’s expectation that RCAs are unlikely to be

interested in granting electric vehicles access to bus and transit lanes. The NZ Transport

Agency expects RCAs will share its reservations about the potentially negative impact of

having electric vehicles in bus and transit lanes on network efficiency (that is, vehicle

congestion and bus reliability). For this reason, it would be important to discuss this measure

with RCAs prior to any announcement or decision.

7 http://www.nzta.govt.nz/resources/research/reports/557/docs/557.pdf , p.23.

8 Ibid, p.22, 23.

Page 20 of 35

109. This risk could be mitigated through consultation with RCAs. Matters relating to

implementation of the option will need to be tested with RCAs to consider how they could be

managed.

110. This incentive would result in minor costs for RCAs. There would be costs involved in

altering signage to identify electric vehicle accessible lanes, and also to make it clear the

lanes that do not afford electric vehicles access.

111. The NZ Transport Agency advises that changes to systems to enable identification of electric

vehicles for enforcement purposes could range between $60,000 and $200,000 to enable.

However, this work may be able to ‘piggyback’ on other projects.

112. Option 5.1 would be the simplest way to ensure this policy is implemented. However, it

would reduce the flexibility RCAs have to manage their networks. Should electric vehicle

numbers grow, and impede the flow of other traffic in a priority lane, RCAs would have no

recourse to mitigate this. A mandatory policy would also mean electric vehicle access could

not be revoked until the regulation expired or was amended.

Page 21 of 35

Measure 6: Road user charges (RUC) exemptions and discounts for electric vehicles

Measure 6: Road user charges (RUC) exemptions and discounts for electric vehicles

Consideration could be given to introducing a RUC exemption for light electric vehicles from the

date each vehicle is registered in New Zealand, for a finite period of time (for example, 5 years).

This option would require a change to the Road User Charges Act 2012.

113. The New Zealand land transport system is largely funded on a user pays basis. Anyone

using New Zealand’s roads contributes towards the operation and development of the land

transport system. Vehicle operators pay for their road use through either fuel excise duty

(FED) or road user charges (RUC), and through a portion of the annual vehicle licensing fee.

114. The Road User Charges Act 2012 (the RUC Act) requires that all vehicles that do not pay

FED through tax on fuel purchases9 (that is, including electric and diesel vehicles) be subject

to RUC, unless exempted.

115. The scope for exemptions is defined in section 37 of the RUC Act. It allows the Governor-

General to, by Order in Council, specify the period during which road user charges are not

payable in respect of light electric vehicles. An Order in Council made under section 37 of

the RUC Act must specify the date on which the exemption expires, and may, from time to

time, be amended to provide for a later date.

116. The Road User Charges (Exemption Period for Light Electric RUC Vehicles) Order 2012

makes light electric vehicles exempt from RUC until 30 June 2020.The definition of electric

light vehicle in the RUC Act includes all vehicles with “motive power wholly or partly derived

from an external source of electricity”. In practice, the exemption includes pure electric

vehicles and PHEVs.

Previous Cabinet decisions

117. In May 2009, the Cabinet Economic Growth and Infrastructure Committee:

117.1. agreed that the Road User Charges Act 1977 and Road User Charges Regulations

1978 be amended to exempt light electric vehicles from paying road user charges

117.2. agreed that a road user charges exemption (that is intended to apply until 1 percent

of the light vehicle fleet is electric) will apply until 2013, with the ability to reassess the

percentage of light electric vehicles in the fleet and extend the exemption [EGI Min

(09) 10/7 refers].

118. In April 2012, Cabinet agreed to extend the existing exemption from RUC for light electric

vehicles until 30 June 2020 [EGI Min (12) 6/6]. This decision reflected a slower than

anticipated rate of uptake of light electric vehicles.

Benefits of the RUC exemption for light electric vehicles

119. The RUC exemption does not address information or coordination problems. It is a financial

incentive that is designed to encourage electric vehicle uptake by reducing their operating

costs.

120. We have not formally evaluated the RUC exemption, so we do not know exactly how

effective the RUC exemption is at incentivising the uptake of electric vehicles in practice.

This includes knowing the extent to which consumers are aware of the RUC exemptions,

9 Note that FED is also charged on CNG and LPG.

Page 22 of 35

and its potential value. For instance, motorists who have previously driven light petrol

vehicles are unlikely to consider the saving on RUC as distinct from overall fuel costs.

121. Stakeholders, such as the Sustainable Business Council and Fleet Management

Association, have said that their members consider the RUC exemption to be an important

consideration when making fleet purchase decisions.

122. We undertook analysis of whether electric vehicles would be reliant on the RUC exemption

for an economic advantage over conventional vehicles based on current costs. We found

that, based on current vehicle and fuel prices, the RUC exemption is an important factor in

determining whether the total cost of ownership for electric vehicles is competitive with

comparable petrol and hybrid vehicles. The RUC exemption therefore plays an important

role in determining whether it makes economic sense for fleet buyers to purchase electric

vehicles in the short to medium-term.

123. The analysis compared the per kilometre operating cost of different vehicle types, based on:

123.1. fuel cost (2015 prices)

123.2. ACC costs

123.3. annual vehicle licensing

123.4. RUC (where applicable)

124. The analysis did not cover capital (that is, purchase price), maintenance costs or

depreciation.

125. The following breakdown shows the costs for both petrol and diesel vehicles using 4 litres

per 100 kilometre and electric vehicles using 12 kilowatt-hours per 100 kilometres.10 It shows

that efficient petrol vehicles have similar operating costs to electric vehicles paying RUC.

10 Conventional Toyota Prius hybrids use 4 to 4.5 litres per 100 kilometres of petrol in the real word, and Nissan Leaf

electric vehicles achieve around 13 kilowatt-hours per 100 kilometres.

Page 23 of 35

126. The analysis shows that if there was no RUC exemption, a solely financial analysis would

exclude electric vehicles from any rational business decisions (unless there was a significant

rise in the price of petrol or major drop in electric vehicle purchase prices).

Cost of RUC exemption

127. Currently, electric vehicles make up just 0.02 percent of the fleet. Based on our modelling of

projected uptake, we would expect to see 30,000 electric vehicles (or about 1 percent of the

fleet) in the New Zealand fleet by 2033 under a ‘status quo’ scenario. The financial

sustainability of the RUC exemption would need to be addressed at this point.

128. The cost of exempting 1 percent of light electric vehicles from RUC is approximately $22

million per year (2015) from the approximately $3 billion which goes into the national land

transport fund annually. Forgoing this revenue means that:

128.1. less funding is available for delivering roading improvements, which could require that

delivery is spread over a slightly longer time frame

128.2. more of the revenue burden is carried by a decreasing proportion of road users,

which could require proportionate increases in FED and RUC to achieve the same

level of funding.

Options considered

129. The following option is consistent with existing government policy, and can be implemented

under the RUC Act.

Option 6.1 – extend the blanket RUC exemption for light electric vehicles to a date beyond

30 June 2020.

130. The following amendments to RUC for electric vehicles would require amendment of the

RUC Act.

Option 6.2 – introduce RUC exemption for light electric vehicles from the date individual

vehicles are first registered in New Zealand, for a finite period of time.

Option 6.3 – introduce a lifetime exemption from RUC for all the light electric vehicles first

registered in New Zealand before a specified date.

Option 6.4 – extend the RUC exemption to include heavy electric vehicles.

Option 6.5 – provide a discounted rate of RUC for heavy electric vehicles.

Option 6.6 – provide a discounted rate of RUC for heavy passenger electric vehicles.

131. Note that no amendment to the RUC Act is proposed for this year’s legislative programme.

Assessment of the options

132. If this measure is pursued, option 6.2 is preferred. A RUC exemption for light electric

vehicles from the date they are first registered, for a finite period of time, would help manage

the cost of foregone revenue (within the 1 percent limit already agreed by Cabinet). It is also

more equitable than the current exemption because owners of electric vehicles would begin

paying their fair share towards the land transport system after the finite period ended. We

would need to do more work to determine an appropriate exemption period. A risk of this

option is that it could be politically difficult for a future government to close off the exemption.

Page 24 of 35

133. If you do not want to pursue an amendment to the RUC Act, you could consider option 6.1.

Based on our preliminary assessment, the RUC exemption for light electric vehicles could be

extended to 2025 without exceeding the 1 percent limit already agreed by Cabinet, even with

a boost in uptake levels as a result of a government package.11

134. We do not recommend that option 6.3 be pursued. While this option would incentivise early

uptake, it could create some unwanted market distortions (for example, a ‘bubble’ of electric

vehicles registered prior to the exemption close off). Such distortions would substantially

increase the amount of revenue foregone and would further exacerbate the inequity of the

RUC exemption.

135. We do not recommend exempting or discounting heavy electric vehicles from RUC. Heavy

vehicles do significantly more damage to the roads, and therefore have a greater impact on

maintenance costs. It would also be a further deviation from the user pays model, and is

likely to face political resistance.

136. Currently, there are very few electric heavy vehicles on the road. Nationally, there is 1 fully

electric truck, 3 hybrid trucks, and 80 electric trolley buses in Wellington.

137. If pursued further, we would need to consult with industry to consider their views on the

matter, and get a better indication of likely rates of uptake. This would inform the projected

costs of the exemption. We would also suggest limiting the scope of the changes to reduce

the risk of higher-than-expected revenue losses (for example, option 6.6 – a discount for

heavy passenger electric vehicles).

138. A risk with all the options above is that the overall cost cannot be defined accurately

(essentially it will be demand driven). Also, there could be perceptions of unfairness from

manufacturers or users of other low emission technologies, such as hydrogen vehicles.

139. If a change to the RUC Act is required following ministerial decisions on the RUC exemption,

the Ministry of Transport could explore whether the exemption should also apply to other low

emission vehicles.

11 If we assume that a package of measures to encourage the uptake of electric vehicles doubles the baseline rate of

uptake, we could see 30,000 electric vehicles in the New Zealand fleet by 2029. However, it is very difficult to project

future uptake of electric vehicles off the current low base (approximately 400 vehicles). Actual uptake in 10 years’ time

may vary significantly from current projections.

Page 25 of 35

Measure 7: Fringe benefit tax on electric and hybrid vehicles

Measure 7: Fringe benefit tax on electric and hybrid vehicles

We recommend that a review be conducted within the next 2 years of the basis for calculating the

taxable value of the fringe benefit for electric and hybrid vehicles. This review would ensure that the

lower running costs of these vehicles are adequately recognised.

140. Fringe benefit tax is a tax on non-cash benefits provided in connection with employment. The

tax is intended to leave an employee neutral between receiving a fringe benefit and receiving

the equivalent monetary remuneration. Consequently, fringe benefit tax should not distort

choice, unless it results in overtaxing the benefit, such as through an overvaluation of the

benefit provided.

141. Electric and hybrid vehicles attract a higher amount of fringe benefit tax as their purchase

prices are higher than those of equivalent conventional vehicles. The Sustainable Business

Council and Business are of the view that reducing the fringe benefit tax on electric vehicles

would have a significant nudge effect on the purchase decisions of fleet managers.

142. For the purposes of fringe benefit tax, the annual taxable value of an employee’s vehicle

benefit is calculated as either 20 percent of a vehicle’s cost price, or 36 percent of its book

value. These proportions are proxy estimates of the fixed and running costs that the

employee would bear if they owned the car themselves. Fringe benefit tax applies to these

estimates.

143. Little is known about the extent to which fleet purchase decisions are being influenced by

fringe benefit tax. In our view, however, it is more likely that other barriers, such as the

limited (travel) range of pure electric vehicles, are playing a far greater role in company

decisions not to purchase electric vehicles for their fleets. Also, many employees use motor

vehicles solely for work purposes rather than as a non-cash employment benefit, and would

be unaffected by changes to fringe benefit tax rules.

144. Nevertheless, a potential issue with the fringe benefit tax regime could be the method for

calculating the taxable value of the fringe benefit. The regime assumes that the calculation

used to value the fringe benefit of a conventional vehicle correctly values the benefit of an

electric/hybrid vehicle. However, although the purchase price is higher, the running costs of

electric/hybrid vehicles tend to be lower than for conventional vehicles. By using the same

proportion of cost price (or book value), the calculation ignores these key differences.

145. Despite the expectation that the purchase price of electric vehicles will continue to fall over

time, it is unlikely that it will fall below that of conventional vehicles. This means that in the

future the potential for the tax calculation to overvalue the fringe benefit of electric/hybrid

vehicles will remain.

146. Where the tax regime overtaxes the fringe benefit of electric vehicles, this would have the

potential to distort vehicle choice in favour of conventional vehicles and away from

electric/hybrid vehicles. This brings a risk that the tax calculation will continue to potentially

overvalue and overtax the fringe benefit of electric/hybrid vehicles.

147. The options looked at to address this concern were:

option 7.1 – exempt electric vehicles from fringe benefit tax

option 7.2 – allow the fringe benefit tax on an electric vehicle to be calculated on the basis of

the cost price/book value of an equivalent conventional vehicle

Page 26 of 35

option 7.3 – review the basis for calculating the taxable value of the vehicle benefit for

electric/hybrid vehicles within the next 2 years.

Assessment of the options

148. If this measure is pursued, option 7.3 is preferred. This would remove any perception that

the fringe benefit tax regime is influencing companies to favour conventional vehicles over

electric/hybrid vehicles. It would also preserve and strengthen the existing policy settings of

the fringe benefit tax regime.

149. Tax officials note that this review work would have to be prioritised against other items on the

Government’s tax policy work programme. The timing of any review should also take into

account the likelihood of continued large variations in the cost structure of electric vehicles,

to ensure any amendment would appropriately reflect the benefit provided, over a longer

term.

150. Option 7.1 is not preferred as it would be inconsistent with New Zealand’s broad based tax

settings. It would also compromise equity goals by affording a tax advantage to those

companies and employees where an electric/hybrid company car is made available for

private use.

151. Option 7.2 is not preferred because it would also, although to a lesser extent, be inconsistent

with the current broad based tax settings and would compromise equity goals within the

current framework. Such a change would create a discrepancy between the effective

taxation of a fringe benefit vehicle and the equivalent cash remuneration.

Page 27 of 35

Measure 8: Tax depreciation rates for electric vehicles

Measure 8: Tax depreciation rates for electric vehicles

We recommend that you consider inviting relevant industry groups (for example, Drive Electric,

electric vehicle manufacturers) to discuss with tax policy officials the case for having higher

depreciation rates for electric vehicles. It would be expected that the industry would prepare an

economic case and support its arguments for a higher rate of depreciation for income tax purposes.

152. MRP and Zero Emission Vehicles Limited have suggested that government could consider

accelerated depreciation rates for electric vehicles. Currently electric vehicles are

depreciated at the same rate as passenger vehicles (30 percent (diminishing value) or 21

percent (straight line) over 5 years). Residual value for passenger vehicles is estimated at 25

percent of cost price.

153. We understand companies that calculate residual vehicle values are making low estimates

for electric vehicles (from $5,000 to $15,000) even though their original purchase price is

higher than similar conventional vehicles. This is likely to be because electric vehicles are

new to the market so there is a lack of information about their resale value and there is

uncertainty about durability, potential technological developments and battery life.

154. Lower than average residual values act as a further disincentive to fleet buyers by increasing

their overall fleet’s vehicle costs. The standard tax depreciation rate for passenger vehicles

is thus perceived as unfair, in part because they receive a poor return on investment. They

perceive that the total cost of ownership over a 5-year period will be higher for electric

vehicles, but they are unable to deduct the tax on the additional cost from their taxable

earnings annually. An accelerated tax depreciation rate for electric vehicles would therefore

help make them more cost-effective and competitive with conventional vehicles.

155. The impact identified by relevant industry groups is a question about the timing and value of

tax depreciation deductions rather than a permanent tax effect. When the asset is disposed

of, the Income Tax Act 2007 requires a wash-up to calculate if the relevant tax depreciation

rate has correctly spread the cost of the asset over its economic life.

156. Tax policy officials advise that proposals for accelerated depreciation would be inconsistent

with the Government’s revenue strategy, which supports a broad-base low-rate tax system

and generally avoids tax concessions. Keeping the tax bases as broad as practical

minimises the distortionary impact taxes can have on decision-making in terms of consumer

choice and decisions to produce goods and services. The primary function of the tax system

is to raise revenue to finance government expenditure in a fair and efficient way; its function

is not to encourage particular types of economic activity. If the Government wishes to

encourage a particular economic activity it is preferable for this to be done in a transparent

way by direct funding rather than through the tax system.

157. That said, the policy principle behind tax depreciation is that the deduction should match the

economic life of the asset. Within these parameters, and keeping in mind the principles of

New Zealand’s broad-base low-rate tax system, there may be a case to consider whether

the current tax depreciation rate that applies to the entire New Zealand passenger vehicle

fleet is appropriate for electric passenger vehicles.

158. Relevant industry groups (for example, Drive Electric, electric vehicle manufacturers) can

discuss their concerns with Inland Revenue directly. Industry would be required to make an

economic case for change, including a clear indication of the fiscal costs.

159. Depreciation rates for electric passenger vehicles are not administratively determined by

Inland Revenue and any work on this issue would need to be prioritised against other items

on the Government’s tax policy work programme.

Page 28 of 35

Measures to be progressed outside of the package

Measures to be progressed outside of the package

160. We have assessed the following measures as having merit, but being more suitable for

progression over the medium-term as part of wider reviews within the relevant departments

or agencies.

Measure 9: Amending ACC levies for plug-in hybrid electric vehicles (PHEVs)

We recommend that this issue be deferred until there is a wider review of the NZ Transport

Agency’s annual vehicle licensing classification system.

161. The owners of PHEVs pay more in ACC levies than equivalent diesel or electric vehicle

owners. This is considered to be inequitable and a disincentive to ownership.

162. This anomaly results from the way in which ACC levies are collected as well as the way in

which PHEVs are classified by the NZ Transport Agency and ACC.

163. ACC levies are collected from vehicle owners either exclusively through annual vehicle

licensing (as is the case for electric and diesel vehicles), or through a combination of annual

vehicle licensing and the ACC motor vehicle levy placed on petrol. Under this system a

petrol driven vehicle pays a lower ACC levy as part of their annual vehicle licence compared

to a non-petrol driven vehicle (for example, pure electric and diesel vehicles), as they are

also charged an ACC levy at the petrol pump.

164. PHEVs are overcharged because they are classified as ‘non-petrol driven’ vehicles. Non-

petrol driven vehicles are charged a higher ACC levy as part of their annual vehicle licence

as it is assumed they do not pay a levy on petrol. However, as PHEVs may use petrol for

approximately 40 percent of their travel, they end up making additional ACC levy payments.

165. We estimate that (under the new ACC levy rates on petrol from July 2015) PHEV owners will

pay, on average, an additional $15 to $40 per annum in ACC levies beyond what other non-

petrol vehicle owners are paying.

166. This additional levy equates to a net cost to consumers of approximately $4,000 per annum

(assuming the 2014 level of PHEV ownership: 220 vehicles in the fleet).

167. Our preliminary modelling suggests PHEV numbers may increase to 2,600 or 0.07 percent of

the vehicle fleet in 2020. In this scenario, the cumulative cost of the additional ACC levy

would reach approximately $159,200 by 2020 (assuming 2015 prices and no increase in the

ACC levy rate on petrol or change in PHEV fuel economy).

Options

168. The options considered to address this anomaly were:

option 10.1 – defer this issue until there is a wider review of the NZ Transport Agency’s

annual vehicle licensing classification system

option 10.2 – undertake a review of the levy rate charged on PHEVs by ACC and amend if

necessary.

Page 29 of 35

Assessment of the options

Assessment of the options

169. Option 10.1 is preferred. While there is an equity issue related to the overpayment by PHEV

owners, the cost involved in removing this anomaly is considerably greater than the

expected net benefit to consumers. ACC estimates that the one-off cost of changing the levy

rate charged as part of the annual licensing of PHEVs would be between $0.5 million and

$1.2 million. The NZ Transport Agency estimates that reclassifying PHEVs in the Motor

Vehicle Register would cost between $60,000 and $200,000.

170. The additional cost of the ACC payment to the individual PHEV owners is also unlikely to be

a disincentive to purchasing these vehicles as it is hidden within annual vehicle licensing

costs.

171. Should you wish to pursue option 10.2, the following steps would need to be taken.

171.1. You would need to write to the ACC Minister to request that ACC undertakes a

review of the PHEV levy rate.

171.2. Should ACC consider it appropriate to amend the rate charged on PHEVs, both ACC

and the NZ Transport Agency would need to collaborate to design an operational

policy to identify, classify, and charge PHEVs with a new levy.

171.3. You would need to write to the NZ Transport Agency Board requesting that they

direct the Agency to collaborate with ACC in this process.

172. Note that ACC and the NZ Transport Agency would need to develop this operational policy

prior to June 2015. ACC need to consult on levy changes before seeking Cabinet approval

and the next cycle of consultation is set for August 2015. Missing this deadline would delay

consultation until the 2017 consultation cycle, or necessitate an out-of-cycle consultation,

which would in turn increase the cost of this process.

Page 30 of 35

Measure 10: A road user charges (RUC) rate for plug-in hybrid electric vehicles (PHEVs)

Measure 10: A road user charges (RUC) rate for plug-in hybrid electric vehicles (PHEVs)

We recommend that officials investigate setting a RUC rate for PHEVs shortly before any RUC

exemption is due to end.

173. When the RUC exemption ends, PHEVs will have to pay RUC as well as FED on any petrol

used. They could apply for a refund of FED, but the burden of doing so may be a

disincentive for uptake of PHEVs, and increase the NZ Transport Agency’s administrative

costs. We can investigate setting a RUC rate for PHEVs shortly before any RUC exemption

is due to end.

Page 31 of 35

Measure 11: Removing battery import duties

Measure 11: Removing battery import duties

We recommend that this issue be considered in the context of New Zealand’s participation in the

Environmental Goods Agreement negotiations at the World Trade Organization. We will continue to

work with the Ministry of Foreign Affairs and Trade (MFAT), MBIE and the New Zealand Customs

Service to establish the impact of any future changes to the tariffs on electric vehicle batteries

174. New Zealand has joined 17 other World Trade Organization members (including China, the

European Union, Japan and the USA) in negotiations towards an Environmental Goods

Agreement in the World Trade Organization context.

175. The possible inclusion of electric vehicles in any final Environmental Goods Agreement

outcome may have a noticeable impact on the global uptake of electric vehicles through

faster and deeper cost reductions, for not only electric vehicles but also associated

technology including batteries and charging infrastructure.

176. Replacement batteries for electric and hybrid vehicles are subject to a 5 percent import duty,

which may add to battery replacement costs for owners. This duty represents a relatively

small component of the cost of replacing a battery, but any reduction in battery replacement

cost would ‘nudge’ consumers to consider electric vehicles as an affordable option.

177. The 5 percent import duty is in place to assist New Zealand manufacturers of batteries.

Though such domestic manufacturers appear to no longer exist, Cabinet has agreed that the

rate remains in place until 30 June 2017.

178. MFAT advises that import duties on replacement batteries for electric vehicles continue to

play an important role as negotiating coin in the context of trade negotiations, particularly the

negotiations towards an Environmental Goods Agreement.

179. MFAT is opposed to any unilateral action to reduce import duties on replacement batteries.

Import duties on a range of environmentally friendly technologies, including electric vehicles

and replacement batteries, may be reduced in accordance with an eventual Environmental

Goods Agreement outcome, assuming that these technologies are part of the final package.

180. Further analysis is required on the impact of tariff duty on imports of replacement batteries

for electric vehicles, noting that in 2014, 98 percent of the $12.8 million trade in lithium-ion

batteries entered free of tariff duty.

181. We will continue to work with MFAT, MBIE, and the New Zealand Customs Service to

establish the impact of any future changes to the tariffs on electric vehicle batteries.

182. We consider this the preferred way forward. Given the removal of duties requires Cabinet

approval, it would be preferable to have the input and support of relevant departments and

ministers.

183. MBIE advises that if the recommendation is to put in place a new tariff concession scheme,

this process would take approximately 4 months (this includes the policy development

process).

Page 32 of 35

Measure 12: A feebate scheme to encourage purchase of low emission vehicles

Measure 12: A feebate scheme to encourage purchase of low emission vehicles

We recommend that feebates not be pursued as a measure for encouraging the uptake of electric

vehicles. We recommend that feebates should be further investigated as a mechanism for reducing

GHG emissions across the vehicle fleet as a whole.

184. Feebate schemes reward purchasers of low emission vehicles with a rebate on the purchase

cost while vehicles with higher emissions are charged a fee.12 We previously advised that

feebates could be a way to provide a subsidy to purchasers of electric vehicles without

imposing a cost on government, as the fees charged to higher emissions vehicles can fund

the rebates to lower emissions vehicles.

185. Feebates reward the consumer ‘up front’ for future cost savings and related long-term

societal benefits of reduced GHG emissions. Feebates aim to improve vehicle emissions

performance across the vehicle market rather than incentivising electric vehicles

per se.

186. Feebates have been implemented in France, and feebate-like systems are in place in other

areas such as the Netherlands and California. Evidence suggests the French and Dutch

systems have been effective in achieving reductions in GHG emissions from new vehicles,

but the impact on the uptake of electric vehicles is less clear. In France, uptake of electric

(both pure electric and PHEVs) and hybrid vehicles is low (3.4 percent of the new vehicle

market in 2013). In comparison, in other markets the uptake of the three classes is higher

(for example, Japan with 21 percent of all new vehicles in 2013, Norway with 12.8 percent,

the Netherlands with 11.3 percent, and California with 10.3 percent).

187. After further analysis we conclude that feebate systems are unsuitable solely as a

mechanism to encourage the uptake of electric vehicles. International studies have found the

major impact of feebates is to incentivise improved emissions performance of existing

vehicle models, rather than achieving a shift in the models purchased. Increased uptake of

electric vehicles may be an indirect effect of feebates. However, the costs of establishing a

feebates scheme solely to encourage electric vehicle uptake would outweigh the benefits (if