Document 1

Tertiary Education Report: Student allowances for mature students:

further advice

Date:

22 February 2013

Priority:

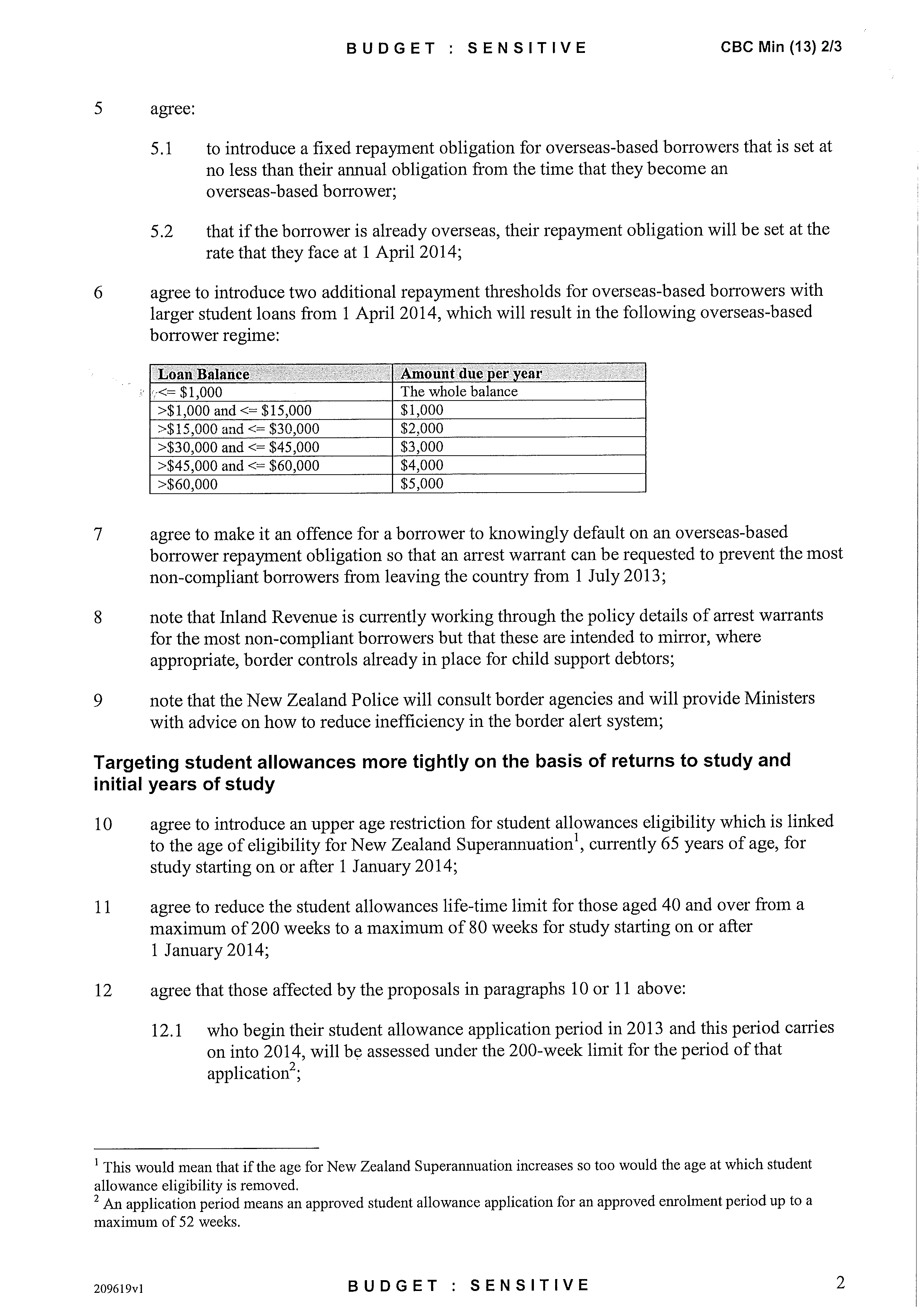

High

1982

Security Level:

Budget Sensitive

METIS No: 752339

Action Sought

Act

Addressee

Actions sought

Deadline

Minister for Tertiary

note further advice on possible student allowance directions

Education, Skills and

forward this paper to the Minister for Social Development

26 February

Employment

and her Associate Minister responsible for student allowance 2013

administration, Hon Chester Borrows.

Enclosure: No

Round Robin: No

Contact for Telephone Discussion (if required)

Information

Name

Position

Telephone

1st Contact

Julie Keenan

Senior Policy Manager

463 8093

027 504 6210

Penny Pender

Drafter

463 8032

The following departments/agencies have seen this report:

Official

MBIE

IR

MoE

Treasury

MoH

MSI

MSD

NZQA

NZTE

OAG

Stats

TEC

TPK

Other

the

Minister to Complete (please circle)

1 = very poor

2 = poor

3 = acceptable

4 = good

5 = very good

Minister’s Office to Complete:

Approved

Declined

Noted

Needs change

under Seen

Overtaken by Events

See Minister’s Notes

Withdrawn

Comments:

Released

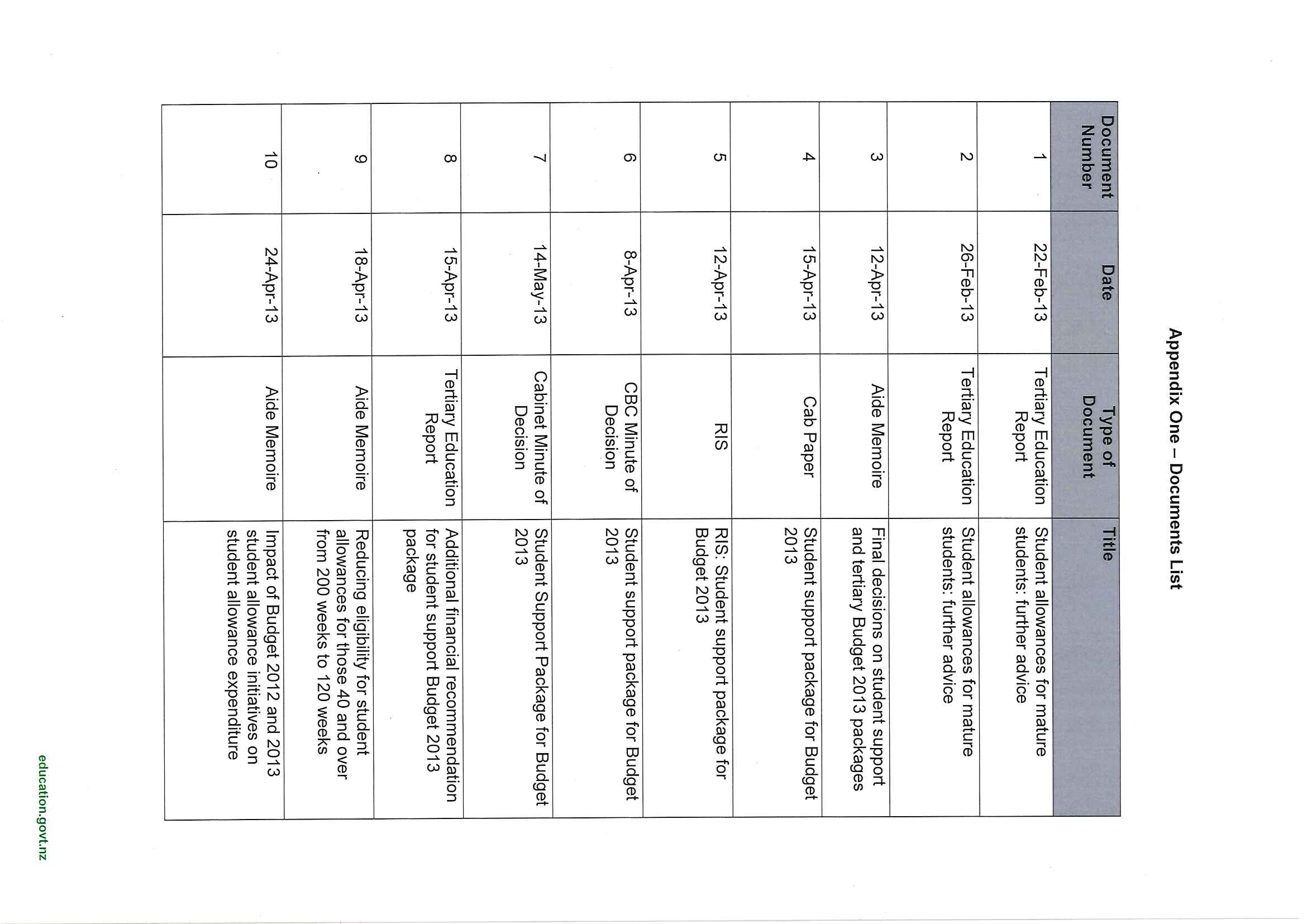

Tertiary Group – TEP

1

Tertiary Education Report: Student allowances for mature students:

further advice

Executive summary

This paper provides advice on the risks and benefits associated with reducing the student

1982

allowances lifetime entitlement from people over the age of 40, down to 80 weeks. This

report provides analysis and initial estimates of the above option and considers how this

might complement other options to target student allowances more closely based on age.

Budget 2013 decisions will be made in the context of changes needed to achieve Better

Act

Public Services targets, and before the impacts of Budget 2012 student allowance changes

are seen. We therefore recommend an incremental approach, to improve alignment with

government objectives.

We recommend you consider forwarding this paper to the Minister for Social Development

and her Associate Minister, Hon Chester Borrows, who is responsible for student allowance

administration.

Recommended actions

We recommend that the Minister for Tertiary Education, Skills and Employment:

Information

1

note the

advice on the implications of reducing the student allowances lifetime

entitlement from people over the age of 40, down to 80 weeks

2

indicate which, if any, of the options officials should develop towards Budget 2013:

Options

Reduce eligibility for those aged

Reduce eligibility for those over (X) age

Official

Y/N

Y/N

over

by lowering the 200 week lifetime cap to

40

Y/N

80 weeks

Y/N

45

Y/N

120 weeks

Y/N

the

50

Y/N

160 weeks

Y/N

55

Y/N

Y/N

60

Y/N

Y/N

65

Y/N

Y/N

AND/OR Remove eligibility from those aged over

under

55

Y/N

65 (Recommended)

Y/N

Released

2

3

forward this paper to the Minister for Social Development and her Associate Minister

responsible for student allowance administration, Hon Chester Borrows.

YES/NO

Dr Andrea Schöllmann

Group Manager

Tertiary Education

1982

Act

Hon Steven Joyce

Minister for Tertiary Education, Skills and Employment

__ __/__ __/__ __

Information

Official

the

under

Released

3

Tertiary Education Report: Student allowances for mature students:

further advice

Purpose of report

1. This paper provides advice on the implications of reducing the student allowances

lifetime entitlement from people over the age of 40, down to 80 weeks. It also provides

analysis and initial estimates of the above option and considers how this might form part

1982

of a package of other options to target student allowances more closely based on age.

Background

Act

2. On 15 February 2013 you were provided with advice on potential options for a student

allowances package for Budget 2013 (METIS 743597). This advice contained options to

target student allowances more closely based on age, and residential status, with

variants provided on age limits and lifetime entitlements.

3. On 19 February officials provided you with indicative initial estimates on the option of

reducing the student allowances lifetime entitlement from people over the age of 40,

down to 80 weeks. Subsequent work suggests this remains a reasonable estimate. This

option is likely to have the following indicative impact:

Indicative impact (annual)

Operating

Offset operating costs

Overall

Numbers affected

Information

savings ($m)

($m)

savings

Student

Student Loans

Accommodation

($m)

Allowances

Supplement

(12)

2

3

(7)

1,800

(NB: doesn’t include grand-parenting costs or administration costs/savings)

4. Flow-on costings have not been developed further. Costing assumptions are yet to be

confirmed by other agencies and implementation costs are not included. In addition, we

Official

estimate student loan capital costs will be around $2m per annum.

5. Other welfare flow-on costs (such as any to the unemployment benefit) have yet to be

considered.

the

6. Transitional arrangements are yet to be considered, but may reduce savings in the short

term. For example, you may wish to consider similar grandparenting arrangements for

students with dependants for the first year (similar to those put in place for the changes to

postgraduate eligibility). In 2011, over half of recipients (53.7%) aged over 40 had

dependants.

under

7. Amendments to the Student Allowances Regulations 1998 would be required. We have

not consulted in detail with StudyLink or Treasury at this stage.

Profile of allowance recipients over 40

8. Table 1 provides basic data about recipients over the age of 40. In 2012, there were

9,453 allowance recipients aged over 40 (around 10% of all recipients).

9. Of those over age 40, women are marginally over-represented at 56.3%. Women usually

make up around 53 – 54% of overall allowance recipients. There are some peaks within

Released

age groups, between the ages of 50 and 54 women account for over 60%, but over age

65 the proportions reverse significantly (only 37% women).

4

Table 1 – Student allowance recipients (2012) over age 40 by age and gender

Age group and

Recipients

Total

Gender

40-44

45-49

50-54

55-59

60-64

65+

5,316

Female

1,709

1,486

1,147

611

277

86

(56.3%)

4,137

Male

1,391

1,058

761

468

314

145

(43.7%)

TOTAL

3,100

2,544

1,908

1,079

591

231

9,453

1982

10. Table 2 shows numbers of recipients by ethnicity, and residency. As outlined in previous

advice (METIS 743597), Māori are over-represented among older allowance recipients.

Act

This reflects that Māori tend to study at later ages. Of recipients over age 40, Māori make

up around 20% compared to around 10% of allowance recipients overall.

11. People of Asian ethnicity are also over-represented, making up 28.5% of recipients over

age 40 (compared to around 20% of overall recipients). This increases with age; Asian

recipients account for nearly 84% of recipients over age 65.

12. Among those over 40, Europeans are under-represented at 32% (generally make up 48%

of overall allowance receipt).

Table 2 - Student allowance recipients over age 40 (2012 data) by age.

Recipients

Total

Information

40-44

45-49

50-54

55-59

60-64

65+

Age

Ethnicity^

European

1,088

856

661

285

111

18

3,019

Maori

661

560

407

190

62

7

1,887

Pasifika

279

213

140

63

16

1

712

Asian

630

598

493

429

351

194

2,695

Official

Residency

Permanent Residents

745

588

390

333

270

190

2,516

Citizens and Citizens by

2,321

1,933

1,510

738

319

39

6,860

birth

the

Refugees

34

23

8

8

2

2

77

^Categories do not include multiple ethnicities or multiple provider types, e.g. those who listed as being both European and

Maori or those studying at both a Polytechnic and a University. These groups made up small proportions of the total overall.

13. Table 3 shows numbers of recipients by provider type. Recipients aged over 40 account

for around 44.1% of allowance recipients who attend wānanga. However, this only

represents around 4.4% of total wānanga enrolments.

under

14. Allowance recipients over 40 at universities and colleges of education account for 3.9%

of allowance recipients at these providers. Comparing this to overall enrolments

(inclusive of international students), student allowance recipients aged over 40 account

for approximately:

1.1% of university enrolments

2.9% of PTE enrolments

2.5% of polytechnic enrolments

Released

4.4% of wānanga enrolments.

5

Table 3 - Student allowance recipients by age and provider (2011 data1).

Age (2011 data)

OVER

40 (%

Provider

<18

18-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65+

of total

Total

type

at level

X)

1987

Uni

35

9,712

26,404

8,195

2,568

1,164

783

568

347

213

67

9

50,065

(3.9%)

241

Schools

5

1,549

204

30

25

37

35

65

48

45

37

11

2,091

1982(11.5%)

Polytechni

3865

72

5,833

9,743

4,672

2,255

1,572

1,329

1,079

722

425

214

96

28,012

c

(13.8%)

PTE&OTE

2219

45

3,001

5,006

2,800

1,313

880

705

574

368

261

176

135

15,264

P

(14.5%)

Act 1695

wānanga

10

387

676

401

349

321

402

463

385

262

146

37

3,839

(44.1%)

Grand

20,48

16,09

10,007

167

42,033

6,510

3,974

3,254

2,749

1,870

1,206

640

288

99,271

Total

2

8

(10%)

15. Table 4 illustrates the age of recipients by level of study. The green column in table 4

shows total recipients over 40. Percentages represent those over 40 as a proportion of all

recipients at each level.

Table 4 – student allowance recipients (2011 data) age by level of study (NB: postgraduates removed)

Information

Age by level of study

level of

Over 40 (as

35-

40-

45-

50-

55-

60-

<18

18-19

20-24

25-29

30-34

65+ a % of all

Total

study

39

44

49

54

59

64

recipients)

Levels 1 – 3

2,675

63

3,273

3,743

1,827

992

738

756

720

471

370

233

125

13,311

Certificates

(20%)

Level 4

1,758

39

3,061

3,404

1,588

814

575

511

425

339

238

151

94

11,239

Certificates

(15.6%)

Levels 5 – 7

1,665

Official

18

2,273

4,533

2,383

1,096

775

608

462

317

177

79

22

12,743

Diplomas

(13%)

Level 7

Bachelor’s

2,915

38

9,517

25,696

7,683

2,769

1,468 1,079

884

564

280

96

12

50,086

(5.8%)

degrees

the

Non-formal

-

-

1

-

-

-

1

-

-

-

-

-

1 (50%)

2

357

Error2

5

1,611

373

109

65

64

63

90

65

58

53

28

2,584

(13.8%)

Grand Total

167

20,482 42,033

16,098

6,510

3,974

3,254 2,749 1,870 1,206 640

288

10,007

99,271

16. While recipients over age 40 appear in higher numbers at Bachelor’s level (29.1% of

under

recipients over age 40), they account for only 5.8% of all recipients at Bachelor’s level.

This is compared to levels 1 – 3 where those over 40 make up 20% of all recipients at

this level.

17. However, counting all study levels below Bachelor’s level shows that over 60% of

recipients over age 40 are studying at sub-degree level.

Student allowance payments

18. The total amount of student allowance paid (including accommodation benefit) to

Released

recipients aged 40 and over in 2012 was $86.2m. It is estimated that reducing entitlement

1 Tables in this paper use some data from the 2011 year and some from the 2012 year (some 2012 data is yet to become

available).

2 The majority of data errors are the result of level of study not being recorded for those at secondary schools.

6

for these people down to 80 weeks would produce annual savings of $7m (as outlined in

paragraphs 3 – 5). This is largely because the majority of student allowance recipients

only access the student allowance for around 80 weeks.

19. Table 5 demonstrates this. Over the age of 40, 80% of people are only using 80 weeks of

allowance. Overall, 76.1% of people are only accessing 80 weeks of allowance. People

between the ages of 20 and 29 tend to access the allowance for longer (around 30% of

these people exceed 80 weeks). This is likely due to the cut off age for parental income

testing at 24 (more students becoming eligible for an allowance when they turn 24).

20. Data for 2004 – 2012 shows the average number of weeks of allowance accessed across

1982

the allowance scheme is 56.7 weeks. For people aged over 40, the average is slightly

lower at 51 weeks. Data from previous years indicates recipients studying at sub-degree

level used on average 38.86 weeks compared to 73.24 weeks at degree level. Māori

Act

used an average of 40.10 weeks compared to 66.26 for Asian recipients and 57.19 for

European recipients. Recipients with no dependants (55.88 weeks) had a higher average

than those with dependents (48.74 weeks).

Table 5 – proportion of people accessing the student allowance for under 80 weeks, 120

weeks

Proportion of people accessing the student allowance for under X weeks

Aged

Aged

Aged

Aged

Aged

Aged

Aged

Aged

Aged

Aged

Aged

Aged

Aged

Aged

<18

18-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65+

Overall

<40

40+

Under 80

weeks

100.0%

99.0%

71.0%

69.1%

81.2%

81.2%

82.0%

80.8%

79.3%

77.6%

76.7%

75.2%

76.1%

75.4%

80.0%

Under

120

weeks

100.0%

99.9%

87.4%

84.8%

93.3%

92.9%

93.5%

92.5%

91.3%

90.5%

89.8%

89.2%

89.6%

89.1%

92.0%

Information

Options

21. This paper sets out a menu of options on the theme of limiting student allowances for

mature students.

Official

Reduce eligibility for those over (X) age by

Reduce eligibility for those aged over

lowering the 200 week lifetime cap to

40

80 weeks

the

45

120 weeks

50

160 weeks

55

60

65

under

AND/OR Remove eligibility from those aged over

55

65 (Recommended)

22. Any option to reduce eligibility for people over a certain age could be combined with

removing allowance eligibility completely from those aged over 65. This would create a

tiered structure of reducing eligibility as people age. This tiered structure would be

characterised by reduced eligibility in line with lifetime limits over certain ages, with

eligibility entirely removed by the age of 65.

23. The main advantage of using lifetime limits to target student allowances is they are a

Released

simple means by which previous access can be measured. In the absence of creating a

more complex and costly administrative system, it can be used as a rough proxy for

existing qualifications, or at least the amount of prior education for which a person has

already received government support for. Lifetime limits are also more flexible in

7

responding to people’s individual study needs. Options in this category are likely to be

perceived as fairer than blunt age limits on eligibility for this reason.

24. The 200 week limit provides approximately five years worth of student support (based on

a 40 week year). Reducing the 200 week lifetime entitlement for people over a certain

age, for example to 80 weeks (approximately two years of study) would reduce spending

while still providing a pathway for people who may require upskilling to support

themselves, or who missed out on foundation level education earlier in life.

25. 80 weeks would generally enable a person to complete up to 240 credits of study. This

would enable people to undertake foundation level study or most certificates and

1982

diplomas (depending on their education needs). It would not be sufficient to cover degree

level study. Students aged under 55 would be able to continue studying with student loan

support.

Act

26. A reduced lifetime limit put in place from a certain age would continue to enable people to

add to their skills later in life to allow them to continue to participate in the labour force,

which recognises some of the training needs of an aging workforce. It is consistent with

refocusing of allowance on initial years of study; while it may have an impact on some

second chance learners, it would pose less of a risk than a blunt removal of eligibility.

27. An option of this nature would reduce opportunities for misuse, but not completely

eliminate any chance of the scheme being used as an alternative form of living support.

28. Removing eligibility based on age results in higher savings than options of reduced

lifetime limits, but at higher risk to access to tertiary education. Those affected would still

have access to tuition subsidies and interest-free student loans for course fees and living

Information

costs (for those under 55).

29. For that reason we recommend considering removing student allowance eligibility for

those aged over 65. Below is a summary of costings for student allowance options based

on age and lifetime limits previously provided to you.

Table 7: summary of costings previously provided

Total Savings -

People

Official

Option

Allowance and

TOTAL COSTS GRAND TOTAL

affected

UBSH (pa) (net)

1a. Remove SA eligibility from those aged

65 ($9.37m) total

$1.53m total

($7.84m) total

310 pa

the

and over

four years

four years

four years.

1b. Remove SA eligibility from those aged

55 ($55.35m)

$16.05m total

($39.30m) total

1,773 pa

and over

total four years

four years

four years.

2a. Restrict SA eligibility from those aged 55

($10.60m)

$3.24m total

($7.35m) total

and over, by lowering the 200 week lifetime

385 pa

total four years

four years

four years.

cap to

80 weeks

under

2b. Restrict SA eligibility from those aged 55

($3.61m) total

$1.8m total

($1.81m) total

and over, by lowering the 200 week lifetime

155 pa

four years

four years

four years.

cap to

120 weeks

Risks

30. If an age band is chosen as a means of prioritising access to student allowances, the

younger any age band is set the more risk is posed to government objectives about

access to tertiary education. A number of people who may have substantially benefited

Released

from tertiary study (including those within target learner groups) may no longer have the

support student allowances provide for access to tertiary education, although most will

have continued access to student loans. This is less of a risk for reduced lifetime limits

than it is for removing eligibility altogether.

8

31. The lower any potential age cut off is set the more this is likely to unduly affect certain

groups (such as Māori who tend to study at a later age) and be seen to disadvantage

parents, particularly Māori and Pasifika women who tend to have children at younger

ages than European and Asian women.

32. Some of these impacts could increase the chances of a successful legal challenge under

the New Zealand Bill of Rights Act 1990 (BoRA). Further detail on these risks was

provided to you in METIS 743597.

1982

Next steps

33. Initial indications are that further savings may be needed to balance Budget 2013,

potentially including further student loan and allowance options (METIS 752343 refers to

Act

student loan options, METIS 743597 refers to allowances options).

34. All options in this paper would require an amendment to the Student Allowances

Regulations 1998.

35. Further detail on costs, savings and implementation issues will form the next stage of

advice once preferred options for Budget 2013 have been identified. Officials seek your

feedback on which, if any, of the options in this paper to progress.

Information

Official

the

under

Released

9

1982

Act

Information

Official

the

under

Released

Document 2

Tertiary Education Report: Student allowances for mature students:

update

Date:

26 February 2013

Priority:

High

1982

Security Level:

Budget Sensitive

METIS No: 753449

Action Sought

Act

Addressee

Actions sought

Deadline

Minister for Tertiary

note further advice on possible student allowance directions

Education, Skills and

forward this paper to the Minister for Social Development

26 February

Employment

and her Associate Minister responsible for student allowance 2013

administration, Hon Chester Borrows.

Enclosure: No

Round Robin: No

Contact for Telephone Discussion (if required)

Information

Name

Position

Telephone

1st Contact

Julie Keenan

Senior Policy Manager

463 8093

027 504 6210

Penny Pender

Drafter

463 8032

The following departments/agencies have seen this report:

Official

MBIE

IR

MoE

Treasury

MoH

MSI

MSD

NZQA

NZTE

OAG

Stats

TEC

TPK

Other

the

Minister to Complete (please circle)

1 = very poor

2 = poor

3 = acceptable

4 = good

5 = very good

Minister’s Office to Complete:

Approved

Declined

Noted

Needs change

under Seen

Overtaken by Events

See Minister’s Notes

Withdrawn

Comments:

Released

Tertiary Group – TEP

1

Tertiary Education Report: Student allowances for mature students:

further advice

Executive summary

This paper provides advice on the risks and benefits associated with reducing the student

1982

allowances lifetime entitlement for people aged 35 and over, down to 80 weeks. This report

provides analysis and initial estimates of the above option and considers how this might

complement other options to target student allowances more closely based on age.

Budget 2013 decisions will be made in the context of changes needed to achieve Better

Act

Public Services targets, and before the impacts of Budget 2012 student allowance changes

are seen. We therefore recommend an incremental approach, to improve alignment with

government objectives.

We recommend you consider forwarding this paper to the Minister for Social Development

and her Associate Minister, Hon Chester Borrows, who is responsible for student allowance

administration.

Recommended actions

We recommend that the Minister for Tertiary Education, Skills and Employment:

Information

1

note the

advice on the implications of reducing the student allowances lifetime

entitlement for people aged 35 and over, down to 80 weeks

2

indicate which, if any, of the options officials should develop towards Budget 2013:

Options

Reduce eligibility for those from

Reduce eligibility for those over (X) age

Official

Y/N

Y/N

age

by lowering the 200 week lifetime cap to

35

Y/N

80 weeks

Y/N

40

Y/N

120 weeks

Y/N

the

45

Y/N

160 weeks

Y/N

50

Y/N

55

Y/N

60

Y/N

65

Y/N

under

AND/OR Remove eligibility from those aged over

55

Y/N

65 (Recommended)

Y/N

Released

2

3

forward this paper to the Minister for Social Development and her Associate Minister

responsible for student allowance administration, Hon Chester Borrows.

YES/NO

Dr Andrea Schöllmann

Group Manager

Tertiary Education

1982

Act

Hon Steven Joyce

Minister for Tertiary Education, Skills and Employment

__ __/__ __/__ __

Information

Official

the

under

Released

3

Tertiary Education Report: Student allowances for mature students:

update

Purpose of report

1. This paper provides advice on the implications of reducing the student allowances

lifetime entitlement for people aged 35 and over, down to 80 weeks. It also provides

analysis and initial estimates of the above option and considers how this might form part

1982

of a package of other options to target student allowances more closely based on age.

Background

Act

2. On 22 February 2013 you were provided with advice on the implications of reducing the

student allowances lifetime entitlement for people aged 40 and over, down to 80 weeks

(METIS 752339). This advice contained options to target student allowances more

closely based on age, with variants provided on age limits and lifetime entitlements.

3. This paper contains a variant option, of reducing the student allowances lifetime

entitlement for people aged 35 and over, down to 80 weeks. In addition, estimates

previously provided to you on 22 February (targeting those aged 40 and over) have now

been updated to reflect forecast volumes of enrolment for 2014-2017 and have shifted

because of greater refinement in the costing methodology.

4. Initial estimates for both of these options are provided below and suggest the following

Information

indicative impact:

Indicative impact (annual)

Restrict SA

Operating

Offset operating costs

Overall

Numbers

SL

entitlement

savings

($m)

savings

affected

Capital

to 80 weeks

($m)

($m)

costs

for

those

Student

Student

Accommodation

aged

Allowances

Loans

Supplement

Official

35 and

(15.8)

4.5

4.0

(7.3)

2,000

3.1

over

40 and

(11.9)

3.0

3.0

(5.9)

1,500

2.1

over1

the

(NB: doesn’t include grand-parenting costs or administration costs/savings)

5. These are indicative costings only. While the table shows figures to the nearest

$100,000 (for comparative purposes), this does not indicate accuracy at this level. Flow-

on costings require further refinement. Costing assumptions are yet to be confirmed by

other agencies and implementation costs are not included.

under

6. Other welfare flow-on costs (such as any to the unemployment benefit) have yet to be

considered but would likely decrease overall savings.

7. Transitional arrangements are yet to be considered, but may reduce savings in the short

term. For example, you may wish to consider similar grandparenting arrangements for

students with dependants for the first year (similar to those put in place for the changes to

postgraduate eligibility).

8. People aged 35 and over are more likely to have dependants; in 2011, 9,386 recipients

over age 30 had dependants (approximately 46% of recipients over 30 – and 53.7% of

recipients over 40).

Released

9. Amendments to the Student Allowances Regulations 1998 would be required. We have

not consulted in detail with StudyLink or Treasury at this stage.

1 estimates previously provided have shifted because of greater refinement in the costing methodology.

4

Profile of allowance recipients 35 and over

10. Table 1 provides basic data about recipients aged 35 and over. In 2012, there were

13,170 allowance recipients aged 35 and over (around 13% of all recipients).

11. Of those aged 35 and over, gender balance is approximately the same as for the scheme

overall (women are represented at 53.8% and usually make up around 53 – 54% of

overall allowance recipients.) There are some peaks within age groups, between the

ages of 50 and 54 women account for over 60%, but over age 65 the proportions reverse

significantly (only 37% women).

1982

Table 1 – Student allowance recipients (2012) from age 35 by age and gender

Age group and

Recipients

Total

Act

Gender

35-39

40-44

45-49

50-54

55-59

60-64

65+

7,091

Female

1,775

1,709

1,486

1,147

611

277

86

(53.8%)

6,079

Male

1,942

1,391

1,058

761

468

314

145

(46.2%)

TOTAL

3,717

3,100

2,544

1,908

1,079

591

231

13,170

12. Table 2 shows numbers of recipients by ethnicity, and residency. As outlined in previous

advice (METIS 743597), Māori are over-represented among older allowance recipients.

This reflects that Māori tend to study at later ages. Of recipients aged 35 and over, Māori

make up 19.5% compared to around 10% of allowance recipients overall.

Information

13. People of Asian ethnicity are also over-represented, making up 24.7% of recipients aged

35 and over (compared to around 20% of overall recipients). This increases with age;

Asian recipients account for nearly 84% of recipients over age 65.

14. Among those aged 35 and over, Europeans are under-represented at 34% (generally

make up 48% of overall allowance receipt).

Official

Table 2 - Student allowance recipients from age 35 (2012 data) by age.

Recipients

Total

35-39

40-44

45-49

50-54

55-59

60-64

65+

Age

the

Ethnicity^

European

1,514

1,088

856

661

285

111

18

4,533

Maori

682

661

560

407

190

62

7

2,569

Pasifika

336

279

213

140

63

16

1

1,048

Asian

552

630

598

493

429

351

194

3,247

under

Residency

Permanent Residents

785

745

588

390

333

270

190

3,301

Citizens and Citizens by

2,888

2,321

1,933

1,510

738

319

39

9,748

birth

Refugees

44

34

23

8

8

2

2

121

^Categories do not include multiple ethnicities or multiple provider types, e.g. those who listed as being both European and

Maori or those studying at both a Polytechnic and a University. These groups made up small proportions of the total overall.

15. Table 3 shows numbers of recipients by provider type. Recipients aged 35 and over

account for around 52.5% of allowance recipients who attend wānanga. However, this

only represents around 5.2% of total wānanga enrolments.

Released

16. Allowance recipients aged 35 and over at universities account for 6.3% of allowance

recipients at these providers. Comparing this to overall enrolments (inclusive of

5

international students), student allowance recipients (by provider) aged 35 and over

account for approximately:

1.8% of university enrolments

4.1% of PTE enrolments

3.5% of polytechnic enrolments

5.2% of wānanga enrolments.

Table 3 - Student allowance recipients by age and provider (2011 data2).

Age (2011 data)

1982

35+ (%

Provider

of total

<18

18-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65+

Total

type

at level

X)

Act 3,151

Uni

35

9,712

26,404

8,195

2,568

1,164

783

568

347

213

67

9

50,065

(6.3%)

278

Schools

5

1,549

204

30

25

37

35

65

48

45

37

11

2,091

(13.3%)

5,437

Polytechnic

72

5,833

9,743

4,672

2,255

1,572

1,329

1,079

722

425

214

96

28,012

(19.4%)

3,099

PTE&OTEP

45

3,001

5,006

2,800

1,313

880

705

574

368

261

176

135

15,264

(20.3%)

2,016

wānanga

10

387

676

401

349

321

402

463

385

262

146

37

3,839

(52.5%)

Grand

13,981

167 20,482

42,033

16,098 6,510

3,974

3,254

2,749

1,870

1,206

640

288

99,271

Total

(14%)

17. Table 4 illustrates the age of recipients by level of study. The green column in table 4

Information

shows total recipients aged 35 and over. Percentages represent those 35 and over as a

proportion of all recipients at each level. Grand totals in this table have been calculated

including level 8, however level 8 includes some postgraduate diplomas and certificates

that will no longer be eligible. In 2011 Levels 1 – 8 (including non-formal recipients and

missing data) there were 95,506 student allowance recipients.

Table 4 – student allowance recipients (2011 data) age by level of study (NB: Masters and Doctorals removed)

Age by level of study

Official

35+ (as a %

level of

of all

<18

18-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65+

Total

study

recipients

by level)

Levels 1 –

the

3,413

3

63

3,273

3,743

1,827

992

738

756

720

471

370

233

125

13,311

Certificates

(25.6%)

Level 4

2,333

39

3,061

3,404

1,588

814

575

511

425

339

238

151

94

11,239

Certificates

(20.8%)

Levels 5 –

2,440

18

2,273

4,533

2,383

1,096

775

608

462

317

177

79

22

12,743

7 Diplomas

(19.1%)

Level 7

under

Bachelor’s

4,383

38

9,517

25,696

7,683

2,769

1,468

1,079

884

564

280

96

12

50,086

degrees

(8.8%)

Level 8

Honours/

3173

4

745

3,277

958

240

110

86

52

36

27

5

1

5,541

Postgrad

(5.7%)

dips+certs)

1

Non-formal

-

-

1

-

-

-

1

-

-

-

-

-

2

(50%)

421

Error4

5

1,611

373

109

65

64

63

90

65

58

53

28

2,584

(16.3%)

13,308

Total

167 20,480

41,027

14,548 5,976

3,730

3,104

2,633

1,792

1,150

617

282

95,506

(14.4%)

Released

2 Tables in this paper use some data from the 2011 year and some from the 2012 year (some 2012 data is yet to become

available).

3 Includes some postgraduate diplomas and certificates no longer eligible

4 The majority of data errors are the result of level of study not being recorded for those at secondary schools.

6

18. While recipients aged 35 and over appear in higher numbers at Bachelor’s level (32.9%

of recipients aged 35 and over at levels 1 - 8), they account for only 8.8% of all recipients

at Bachelor’s level. This is compared to levels 1 – 3 where those aged 35 and over make

up 25.6% of all recipients at this level.

19. Counting all study levels below Bachelor’s level shows that 8,186 student allowance

recipients were studying at sub-degree level. At levels 1 – 8 this represents around 8.5%

of recipients and 62% of recipients over the age of 35.

1982

Student allowance payments

20. The total amount of student allowance paid (including accommodation benefit) to

recipients aged 35 and over in 2012 was $117.4m. It is estimated that reducing

Act

entitlement for these people down to 80 weeks would produce annual savings of $7.3m

(as outlined in paragraphs 3 – 5). This is largely because the majority of student

allowance recipients only access the student allowance for up to 80 weeks.

21. Table 5 demonstrates this. At ages 35 and over, around 80% of people are using less

than 80 weeks of allowance. Overall, 76.1% of people are only accessing 80 weeks (or

less) of allowance. People between the ages of 20 and 29 tend to access the allowance

for longer (around 30% of these people exceed 80 weeks). This is likely due to the cut off

age for parental income testing at 24 (more students becoming eligible for an allowance

when they turn 24).

22. Data for 2004 – 2012 shows the average number of weeks of allowance accessed across

the allowance scheme is 56.7 weeks. For people aged over 40, the average is slightly

Information

lower at 51 weeks. Data from previous years indicates recipients studying at sub-degree

level used on average 38.86 weeks compared to 73.24 weeks at degree level. Māori

used an average of 40.10 weeks compared to 66.26 for Asian recipients and 57.19 for

European recipients. Recipients with no dependants (55.88 weeks) had a higher average

than those with dependents (48.74 weeks).

Table 5 – proportion of people accessing the student allowance for under 80 weeks, 120

Official

weeks

Proportion of people accessing the student allowance for under X weeks

the

Aged

Aged

Aged

Aged

Aged

Aged

Aged

Aged

Aged

Aged

Aged

Aged

Aged

Aged

<18

18-19

20-24

25-29

30-34

35-39

40-44

45-49

50-54

55-59

60-64

65+

Overall

<40

40+

Under 80

weeks

100.0%

99.0%

71.0%

69.1%

81.2%

81.2%

82.0%

80.8%

79.3%

77.6%

76.7%

75.2%

76.1%

75.4%

80.0%

Under

120

weeks

100.0%

99.9%

87.4%

84.8%

93.3%

92.9%

93.5%

92.5%

91.3%

90.5%

89.8%

89.2%

89.6%

89.1%

92.0%

under

Options

23. This paper sets out a menu of options on the theme of limiting student allowances for

mature students.

Released

7

Options

Reduce eligibility for those over (X) age by lowering the 200

Reduce eligibility for those from age

week lifetime cap to

35

80 weeks

40

120 weeks

45

160 weeks

50

55

1982

60

65

AND/OR Remove eligibility from those aged over

Act

55

65 (Recommended)

24. Any option to reduce eligibility for people over a certain age could be combined with

removing allowance eligibility completely from those aged over 65. This would create a

tiered structure of reducing eligibility as people age.

25. The main advantage of using lifetime limits to target student allowances is they are a

simple means by which previous access can be measured. In the absence of creating a

more complex and costly administrative system, it can be used as a rough proxy for

existing qualifications, or at least the amount of prior education for which a person has

already received government support. Lifetime limits are also more flexible in responding

to people’s individual study needs. Options in this category are likely to be perceived as

Information

fairer than blunt age limits on eligibility for this reason.

26. The current 200 week limit provides approximately five years worth of student support

(based on a 40 week year). Reducing the 200 week lifetime entitlement for people over a

certain age, for example to 80 weeks (approximately two years of study) would reduce

spending while still providing a pathway for people who may require upskilling to support

themselves, or who missed out on foundation level education earlier in life.

Official

27. 80 weeks would generally enable a person to complete up to 240 credits of study. This

would enable people to undertake foundation level study or most certificates and

diplomas (depending on their education needs). It would not be sufficient to cover degree

level study. Those affected would still have access to tuition subsidies and interest-free

the

student loans for course fees and living costs (for those under 55).

28. A reduced lifetime limit put in place from a certain age would continue to enable people to

add to their skills later in life to allow them to continue to participate in the labour force,

which recognises some of the training needs of an aging workforce. It is consistent with

refocusing of allowance on initial years of study; while it may have an impact on some

second chance learners, it would pose less of a risk than a blunt removal of eligibility.

under

29. An option of this nature would reduce opportunities for misuse, but not completely

eliminate any chance of the scheme being used as an alternative form of living support.

Over 65s

30. Removing eligibility based on age results in higher savings than options of reduced

lifetime limits, but at higher risk to access to tertiary education.

31. We recommend considering removing student allowance eligibility for those aged over

65. In 2012 nearly 82.3% of student allowance recipients over age 65 were permanent

Released

residents (compared to 15% of overall recipients). Significant over-representation of

permanent residents at older ages suggests some may be accessing the allowance as an

alternative to other forms of living support (permanent residents are less likely to qualify

8

for New Zealand superannuation5, and the allowances scheme does not have a work test

as in the benefit system).

32. The benefits of providing this support are not well aligned to the objectives of the student

allowances scheme. Study undertaken by these students is unlikely to have significant

economic benefits for New Zealand, as these people are unlikely to enter the labour

market. Social benefits (for example improving English-language skills) could be

achieved through part-time study (not eligible for an allowance) or adult and community

education.

33. New Zealand citizens who qualified for Superannuation would effectively not be at a

1982

disadvantage by removal of student allowances for people over age 65. This is because

there is already a restriction on receiving the student allowance if in receipt of New

Zealand Superannuation.

Act

Impact of options

34. Below is a summary of costings for student allowance options based on age and lifetime

limits previously provided to you. All options in this paper would require an amendment to

the Student Allowances Regulations 1998.

Table 7: summary of costings previously provided

Total Savings -

People

Option

Allowance and

TOTAL COSTS GRAND TOTAL

affected

UBSH (pa) (net)

Information

1a. Remove SA eligibility from those aged

65 ($9.37m) total

$1.53m total

($7.84m) total

310 pa

and over

four years

four years

four years.

1b. Remove SA eligibility from those aged

55 ($55.35m)

$16.05m total

($39.30m) total

1,773 pa

and over

total four years

four years

four years.

2a. Restrict SA eligibility from those aged 55

($10.60m)

$3.24m total

($7.35m) total

and over, by lowering the 200 week lifetime

385 pa

total four years

four years

four years.

Official

cap to

80 weeks

2b. Restrict SA eligibility from those aged 55

($3.61m) total

$1.8m total

($1.81m) total

and over, by lowering the 200 week lifetime

155 pa

four years

four years

four years.

cap to

120 weeks

the

Student

Student

People

As flow Total (pa)

Options

allowance

loan

(implementation

affected

on

savings ($m)

flow on

costs TBC)

Restrict SA eligibility from those aged

40 (11.9)

1,500

3.0

3.0

(5.9)

under

and over, by lowering the 200 week lifetime

cap to

80 weeks6

Restrict SA eligibility from those aged

35 (15.8)

2,000

4.5

4.0

(7.3)

and over, by lowering the 200 week lifetime

cap to

80 weeks

Released

5 To qualify for New Zealand Superannuation you must be 65 years or older and you must also have lived in New

Zealand for at least 10 years since you turned 20. Five of those years must be since you turned 50.

6 estimates previously provided have shifted because of greater refinement in the costing methodology.

9

Risks

35. If age is chosen as a means of prioritising access to student allowances, the younger any

age limit is set the more risk is posed to government objectives about access to tertiary

education. A number of people who may have substantially benefited from tertiary study

(including those within target learner groups) may no longer have the support student

allowances provide for access to tertiary education, although most will have continued

access to student loans. This is less of a risk for reduced lifetime limits than it is for

removing eligibility altogether.

1982

36. The lower any potential age cut off is set the more this is likely to unduly affect certain

groups (such as Māori who tend to study at a later age) and be seen to disadvantage

parents, particularly Māori and Pasifika women who tend to have children at younger

ages than European and Asian women.

Act

37. People aged 35 and over are more likely to have dependants; in 2011, 9,386 recipients

over age 30 had dependants (approximately 46% of recipients over 30 – and 53.7% of

recipients over 40). For those affected students who support dependants, the amount

which can be borrowed for living costs through the student loan scheme plus

accommodation supplement may end up being less than the amount of student

allowance plus accommodation benefit they can currently receive. This could have an

additional impact on access objectives.

38. Some of these impacts could increase the chances of a successful legal challenge under

the New Zealand Bill of Rights Act 1990 (BoRA). Further detail on these risks was

provided to you in METIS 743597.

Information

Next steps

39. Further detail on costs, savings and implementation issues will form the next stage of

advice once preferred options for Budget 2013 have been identified. Officials seek your

feedback on which, if any, of the options in this paper to progress.

40. Initial indications are that further savings may be needed to balance Budget 2013,

Official

potentially including further student loan and allowance options (METIS 752343 refers to

student loan options, METIS 743597 refers to allowances options).

the

under

Released

10

Document 3

Aide Memoire: Tertiary education package for Budget 2013, Cabinet, 15 April

2013

Date:

12 April 2013

Priority:

High

Security Level:

Budget Sensitive

METIS No: 768522

1982

File Number

ED 30 44 00 2

Act

The attached aide memoire supports your discussion of the changes to the tertiary education

package for Budget 2013 at Cabinet on Monday 15 April 2013.

Information

Roger Smyth

Acting Group Manager, Tertiary Education

Ministry of Education

Official

the

under

Released

Aide Memoire: Tertiary education package for Budget 2013, Cabinet, 15 April

Aide Memoire: Tertiary education package for Budget 2013, Cabinet, 15 April

2013

1982

I am amending my tertiary package for Budget 2013, as recommended by Cabinet Business

Committee to Cabinet on 2 April 2013.

Act

The changes I am making to my tertiary package are as follows:

Closing the existing difference between the current Student Achievement Component

funding rates for private training establishments and tertiary education institutions

($28.7 million over four years).

Including, as an option, a variant on the initiative to reduce student allowance

entitlement for those aged 40 and over from 200 weeks to 80 weeks. The new variant

will reduce entitlement to 120 weeks. This variant has not been costed in detail.

However, it is likely to result in a marginal reduction of savings of as much as 60% for

this initiative.

Rolling forward the operating contingency ‘Transitional Funding for Industry Training’

Information

to 2013/14. This will assist with a smooth transition to the reformed industry training

system and the impact of the Industry Training Reboot (the contingency balance is

$7.5 million).

Rolling forward the capital contingency ‘Development of Real-time Single Data Return

System’ to 2013/14. Planning and decision-making to achieve the full Tertiary

Information Future State vision has taken longer than expected due to agency

Official

capability and capacity as well as the complexity and breadth of the programme (the

contingency balance is $8 million).

Minor technical changes, including:

the

o removing the words ‘in principle’ from recommendation 11 in the overall

tertiary paper, to reflect that the transfer from the industry training underspend

to Māori and Paskifika Trades training wil be a permanent change in the

baseline

under

o changing one word in recommendation 4 in the student support package, to

reflect that the information-matching agreement will be established by 1 April

2014, rather than from 1 April 2014.

The paper also notes that the Vote Science and Innovation package for Budget 2013

includes $10 million per annum to scale up Education New Zealand’s marketing and industry

capability-building activities. The paper notes that $10 million per annum will be allocated

from the operating allowance to Vote Tertiary for Education New Zealand’s initiative.

Released

2

Document 4

Budget Sensitive

Office of the Minister for Tertiary Education, Skills and Employment

Office of the Minister of Revenue

Cabinet

1982

Student support package for Budget 2013

Act

Proposal

1.

This paper seeks Cabinet’s agreement to changes to the Student Loan and Allowances

Schemes for Budget 2013.

Executive summary

2.

The tertiary education package for Budget 2013 aims to improve the contribution of

tertiary education to economic growth by increasing the proportion of young people with

higher level qualifications and by ensuring that New Zealand’s skil s base supports the

Information

needs of industry and encourages innovation. The student support initiatives outlined in

this paper enable us to achieve our priorities through Budget 2013, as set out in the

accompanying Cabinet paper

Tertiary Education Package for Budget 2013. The

student support initiatives will improve the value of the Government’s expenditure on

student support, and provide further savings to reprioritise to meet our wider tertiary

education goals.

Official

3.

Our main priority for improving the performance of the Student Loan Scheme in this

Budget is to improve repayments from overseas-based borrowers and to increase

personal responsibility for debt repayment. Our emphasis is also on ensuring that the

adjustments we make now will improve the value of the scheme in the future.

the

4.

In addition to extending our Overseas-Based Borrower Initiative (OBBCI), for which

funding is being sought from the Vote Revenue Budget package, we propose the

following:

a. Extending the current student loan and student allowances stand-down period for

permanent residents (including Australians) from 2 years to 3 years from 1

under

January 2014 to increase our confidence that permanent residents will stay in

New Zealand when they finish their study and repay their student loans.

b. Putting in place an ongoing information-sharing agreement between Inland

Revenue and Internal Affairs to obtain further contact details from overseas-based

borrowers and liable parents when they renew or apply for their passport.

c. Adjusting the overseas-based borrower repayment regime (from 1 April 2014 for

the 2014/15 tax year and beyond) to improve the long term sustainability of the

scheme by speeding up repayments of compliant overseas-based borrowers and

ensuring they can make progress on their loans. We aim to achieve this by:

Released

Introducing a fixed repayment obligation for overseas-based borrowers that is

set at no less than their annual obligation from the time they become an

overseas-based borrower. If the borrower is already overseas, their repayment

obligation will remain at the rate they face at 1 April 2014.

1

Adding higher repayment thresholds for overseas-based borrowers with larger

student loans.

d. Making it an offence for a borrower to knowingly default on an overseas-based

borrower repayment obligation so that an arrest warrant can be requested to

prevent the most non-compliant borrowers from leaving the country from 1 July

2013.

5.

As we continue to recover from the economic downturn, we propose to continue

1982

improving the value of student support spending in this Budget by targeting student

allowances more tightly on the basis of returns to study and on initial years of study

through:

Act

e. Reducing student allowance entitlement for those aged 40 and over to a

maximum of 80 weeks from 1 January 2014 (or variant of reducing entitlement for

those aged 40 and over to a maximum of 120 weeks).

f. Removing student allowances eligibility for those aged 651 and over from 1

January 2014.

6.

The student support package also includes the following initiatives:

Changing the way the cost of lending is calculated in the Student Loan Scheme,

by linking the calculation to prevailing interest rates. This initiative will bring the

calculation into alignment with accounting standards. The savings that result from

Information

this change will begin in the 2012/13 financial year.

Administrative funding to enable StudyLink to administer recent changes related

to level 1 and 2 Student Achievement Component provision agreed to by Cabinet

last year whereby a student undertaking fees-free study cannot access the fee

component of a student loan and under 18 years old enrolled in fees-free places

are ineligible to borrow through the Student Loan Scheme [CAB Min (12) 21/5A

Official

refers].

7.

Amendments to the Student Loan Scheme Act 2011 are required for initiatives (c) and

(d) above. Amendments to the District Court Rules 2009 are also needed for initiative

(d). Amendments to the Student Allowances Regulations are required for initiatives (e)

the

and (f) and for extending the student allowance stand-down for permanent residents in

initiative (a).

8.

The operating impact of the package for the 2013/14 to 2016/17 financial years is

estimated to be a saving of $109.569 million. The debt impact over the same period is

estimated to be a saving of $7.436 million.2

under

9.

The major overall impacts of the package are that it:

reduces the student loan write-down from 39.09 cents in the dollar to 34.92 cents

in the dollar (which includes a reduction to 34.89 cents in the dollar from the

student support package and an increase of 0.03 cents in the dollar from the

tertiary education package)

Released

1 This would be linked to the age of eligibility for New Zealand Superannuation. This means that if the eligibility

age of New Zealand Superannuation increases so too would the age at which student allowances eligibility is

removed.

2 This includes the option to reduce student allowance entitlement for those aged 40 and over from 200 weeks to

80 weeks. The 120 week variant is yet to be costed in detail but is likely to reduce the savings of this initiative by

as much as 60%.

2

reduces the repayment times for the almost 30,000 overseas-based student loan

borrowers who have loan balances above $15,000, providing they comply with

their obligations

on average, removes student allowances eligibility for approximately 2,860

students a year and reduces the cost of student allowances by $61.807 million

over four years (2013/14 to 2016/17).

Background

1982

10. The student support system is designed to reduce financial barriers to participation in

tertiary education. With the Government’s commitment to providing near universal

student loans and maintaining high levels of tertiary education participation, it is

Act

important that student support Budget policy changes continue to meet the objective of

improving value for the Government, particularly during difficult economic times.

11. The Student Loan Scheme provides broad access to upfront finance with repayments to

be met from future earnings. Loans involve a lower level of government subsidy than

allowances, so they are a means of managing the trade-offs between access to study

and affordability for Government.

12. Student allowances aim to address the financial barriers to study for low income groups.

They assist people to enter tertiary education who have very little upfront cash or family

resources, and who heavily discount the future benefits of qualifications. Student

allowances also provide additional support for students with higher financial needs, for

Information

example those with dependants.

13. The Government spends a significant amount of money on student support each year.

In 2011/12, the Government spent $2,255 million on tuition subsidies, students drew

$1,586 million in new student loan lending, and the Government paid $649 million for

student allowances. Tuition subsidies, student loans and student allowances combined

have represented between 6% and 7% of core Crown expenditure in each year

Official

between 1994/5 and 2011/12.

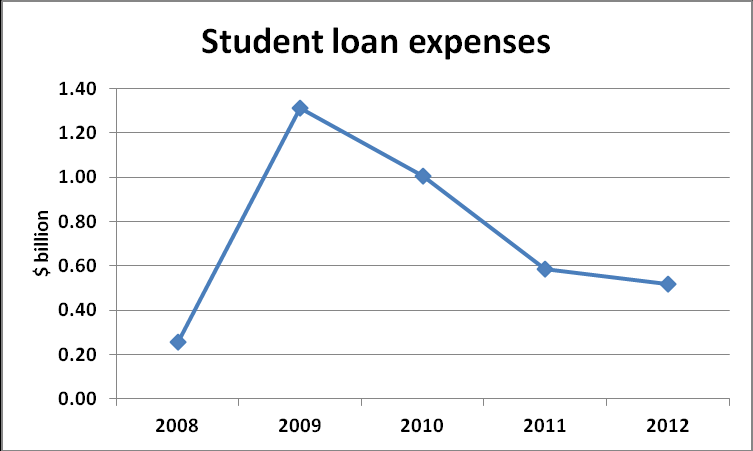

14. The figure below shows the growth of student allowance expenditure since 2008 and

the impact of the changes we have made to student loan policy, which has contributed

the

to the decrease in student loan expenditure.

Figure 1: Student allowances and loan expenditure

Student allowances expenses

0.7

under

0.6

0.5

s 0.4

llion

bi 0.3

$ 0.2

0.1

0.0

1

3

5

7

9

1

3

5

7

/0

/0

/0

/0

/0

/1

/1

/1

/1

0

2

4

6

8

0

2

4

6

0

0

0

0

0

1

1

1

1

0

0

0

0

0

0

0

0

0

2

2

2

2

2

2

2

2

2

Released

Actual

Forecast

15. OECD countries spend, on average, 20.5% of their public budgets for tertiary education

on financial aid to students. New Zealand spends more than double this proportion

3

(43.1%), and is second behind the UK (54.2%) on the proportion of total public tertiary

education expenditure that supports students.

Problem definition

Student allowances

16. Government expenditure on student allowances has increased significantly in recent

years – from $385 million in 2007/08 to $649 million in 2011/12 (a 69% increase). The

1982

number of students receiving an allowance has also increased, particularly since 2009,

due to policy changes implemented by the previous government (such as increases to

the parental income threshold) and the effects of the recession, including higher tertiary

enrolments due to increased unemployment.

Act

17. Student allowances are not well targeted to those in most need. Policy changes to the

parental income threshold mean that the original intent of allowances as a mechanism

to support students from low income backgrounds has broadened to include middle

income families.

18. In Budget 2012, we made changes to the Student Allowances Scheme to begin shifting

the focus of support back to students from lower income backgrounds by freezing

student allowances parental income thresholds. We also tightened the targeting of the

scheme so that it centres more on students in their initial years of study by removing

eligibility for postgraduate study and long programmes.

Information

19. There is room to improve the targeting of student allowances particularly for students

aged 24 and over. For students aged under 24, parental income testing provides a

useful targeting mechanism. For more mature single students, however, there is no

parallel test. Many New Zealanders for example, would be surprised to learn that

people can access student allowances for up to five years throughout their adult lives.

Student Loan Scheme

Official

20. Our analysis of the Student Loan Scheme has identified three broad types of borrower

groups that represent low value lending:

Borrowers whose labour market returns are insufficient to make progress in

the

repaying their loans (including borrowers under the repayment threshold,

borrowers with large student loans who have poor labour market outcomes, and

borrowers who use loans for non-educational purposes).

Borrowers who go overseas and do not repay (who may or may not have high

incomes).

under

Borrowers who would still participate in tertiary education if the government

subsidy on student loans was reduced (for example, while lending to this group

may be high value, it may be unnecessary).

21. In addressing these areas, recent budgets have focused on:

encouraging educational performance and decision-making (e.g. introducing a

performance element to the scheme and a 7 EFTS life-time limit)

restricting areas of high risk lending (e.g. not lending to those in default for $500

or more in a year)

Released

shifting more of the costs of tertiary study to those who can afford to pay and who

are more likely to receive higher levels of private return from their study (e.g.

increasing the repayment rate from 10% to 12% and broadening the definition of

income for loan repayment purposes)

4

improving contact with overseas-based borrowers (e.g. data-matching between

Inland Revenue and NZ Customs and requiring contact details from those wanting

to take advantage of the repayment holiday while they are overseas).

22. Prior to Budget 2010, the cost of lending was 47.39 cents in the dollar. The cost of

lending following Budget 2012 is 39.09 cents in the dollar.

23. The Government has also introduced the OBBCI to improve the level of repayments

and overall compliance of defaulting borrowers. This began as a small pilot in October

1982

2010 with a focus on borrowers in Australia, utilising private sector providers in a series

of tracing and collection studies as well as online advertising. The pilot proved

successful and achieved a return on investment of over $5 for every $1 spent within 9

months. The OBBCI has subsequently been scaled up and now also focuses on

Act

borrowers in the United Kingdom. Information-matching arrangements will be

introduced between Inland Revenue and Customs to identify borrowers in serious

default. Inland Revenue is also scoping the implementation of debt collection measures

in Canada and the United States, further legal activity, and engagement with online

payment intermediaries. The return on investment has now increased to over $10 for

every dollar spent. Additional funding to continue the OBBCI is being sought through

the Vote Revenue package.

24. Budget 2013 has assessed the scope for further improvements to the value of the loan

scheme to make further changes that do not significantly compromise the scheme’s

access objectives.

Information

Strategy for Budget 2013

25. In developing a student support package for Budget 2013, we have considered that:

the use of loans as a policy lever assumes that increased or more stable earnings

should result from study, and that credit market failure is the main reason some

people do not invest in study (i.e. people understand and are prepared to meet

the costs of study, they just do not have the financial means to meet them)

Official

tighter targeting of student allowances to those from low income families and to

the initial years of study means that future policy changes to reduce the cost of

the Student Loan Scheme need to retain relatively broad access to student loans.

the

26. Our focus, therefore, is to put in place initiatives that:

build on the success of the OBBCI programme in collecting repayments from

overseas-based borrowers (now and into the future) and increasing their personal

responsibility for debt repayment

under

further redistribute tertiary education costs according to the benefits of study by

making changes to student allowances eligibility ahead of any further options for

reducing eligibility for loans.

Released

5

Budget 2013 package

27. The proposed Budget 2013 package aims to improve the value of student support

spending in the following ways:

Improving repayments from overseas-based borrowers and increasing personal responsibility for

debt repayment by:

extending the student loan and allowance stand-down period for permanent residents

(including Australians) from 2 years to 3 years from 1 January 2014

1982

putting in place an ongoing information-sharing agreement between Inland Revenue and

Internal Affairs to collect contact detail from passport applications

adjusting the overseas-based borrower repayment regime from 1 April 2014 for 2014/15

Act

and beyond, by introducing:

o

a fixed repayment obligation for overseas-based borrowers that is set at no less than

the borrower’s annual obligation from the time they become an overseas-based

borrower. If the borrower is already overseas, their repayment obligation will remain at

the rate they face at 1 April 2014

o

additional repayment thresholds for overseas-based borrowers

making it an offence for a borrower to knowingly default on an overseas-based borrower

repayment obligation so that an arrest warrant can be requested to prevent the most non-

compliant borrowers from leaving the country from 1 July 2013.

Information

Targeting student allowances more tightly on the basis of returns to study and to initial years of

study by:

reducing the student allowance life-time limit for those aged 40 and over from 200 weeks to

80 weeks from 1 January 2014 (variant: reducing entitlement for those aged 40 and over

from 200 weeks to 120 weeks)

removing student allowances eligibility for those aged 65 years and over from 1 January

Official

2014.

28. The student support package also includes the following initiatives:

the

Changing the way the cost of lending is calculated in the Student Loan Scheme,

by linking the calculation to prevailing interest rates. This initiative will bring the

calculation into alignment with accounting standards. The savings that result from

this change will begin in the 2012/13 financial year.

Administrative funding to enable StudyLink to administer recent changes related

to level 1 and 2 Student Achievement Component provision agreed to by Cabinet

under

last year whereby a student undertaking fees-free study cannot access the fee

component of a student loan and under 18 enrolled in fees-free places are

ineligible to borrow through the Student Loan Scheme [CAB Min (12) 21/5A

refers].

Improving repayments from overseas-based borrowers

29. Overseas-based borrowers have much lower repayment compliance and slower

repayment times than New Zealand–based borrowers3. Under current valuation

Released

assumptions, if all overseas-based borrowers were compliant (still allowing for death

and bankruptcy write-offs), the value of new lending would increase by 3 cents in the

dollar.

3 The higher domestic compliance is largely due to compulsory collection through the income tax system and

sanctions which are more easily enforced when non-compliance occurs.

6

30. As at 30 June 2012, there were 701,232 borrower accounts held by Inland Revenue. Of

these borrowers, 101,095 (14%) of these borrowers were overseas-based. However,

these borrowers represented 58% of all borrowers with overdue payments (53,471) and

had 80% of all overdue repayments ($409.7 million).

Table 1: Overdue student loan repayments at 30 June

Overdue

2011

2012

%

Repayments

million

$million

change

Borrowers based

1982

-in New Zealand

$122.8

$102.6

-16.4%

-overseas

$288.9

$409.7

41.8%

Total

$411.7

$512.3

24.5%

__________________ _______ ________ __________

Act

Number of borrowers

-in New Zealand

49,803

38,577

-22.5%

-overseas

50,264

53,471

6.4

Total

100,067

92,048

-8.0%

Source: Student Loan Scheme Report, 2012

31. The number of overseas-based borrowers going into default continues to increase, with

the amount in default held by borrowers overseas having risen to $423 million by 31

January 2013. The previous three-year repayment holiday acted to mask the extent of

the problem of non-compliance of overseas-based borrowers.

32. The high level of default is primarily due to a significant portion of borrowers not

meeting their obligations of keeping Inland Revenue up to date with their contact details

Information

and making payments. Evidence to date from the OBBCI reflects the importance of

maintaining contact with overseas-based borrowers. Inland Revenue has had a 70%

compliance rate among borrowers it has contacted as part of this initiative. Up until

February 2013, the total cash collected from this initiative is $51.1 million and the costs

of the programme are $5 million. This means we have achieved a return on our

investment of $10.20 for every dollar spent.

Tightening student loan and allowances eligibility criteria for permanent residents

Official

33. Ministry of Education research indicates that permanent residents and Australians are

more likely to go overseas than New Zealand citizens and are less likely to return4.

While non-citizens who remain in New Zealand after study represent good value

the

investment and lending for the Government, those who go overseas are more likely to

default on their student loans than borrowers who are New Zealand citizens. Our data

shows that, as at 31 March 2011, of the proportion of overseas-based borrowers who

were in default, 29.3% were Australian citizens, 14.5% were Chinese citizens and

12.6% were New Zealand citizens.

under

34. To increase our confidence that permanent residents will stay in New Zealand after

study and make a contribution to our economy and society, we propose extending the

student loan and student allowance stand-down period for permanent residents

(including Australians) from 2 years to 3 years from 1 January 2014. This means that

migrants will need to have lived in New Zealand for at least three years, be ordinarily

resident in New Zealand, and have been entitled to reside indefinitely in New Zealand

for at least three years before they can receive a student loan and/or student

allowance.

35. We believe that this is a reasonable way of distinguishing which permanent residents

Released

intend to stay in New Zealand and which intend to leave. While this initiative places a