[IN CONFIDENCE RELEASE EXTERNAL]

26OIA1325

23 September 2025

A O’Sullivan

[FYI request #32256 email]

Dear A O’Sullivan

Thank you for your request made under the Official Information Act 1982 (OIA), received on 8

September 2025. You requested an update on previously supplied data on taxpayers with residential

rental property investments. We responded to a previous request from you on 27 March 2025

(25OIA2086) at which stage the filing of tax returns for the 2023-24 tax year was incomplete. We

directed you to a previously released OIA

(2024-10-29-total-number-of-taxpayers-who-declared-

income-from-rental-properties.pdf) with information covering the tax years 2019-20 through to 2022-

23, and incomplete data for 2023-24 on the following topics:

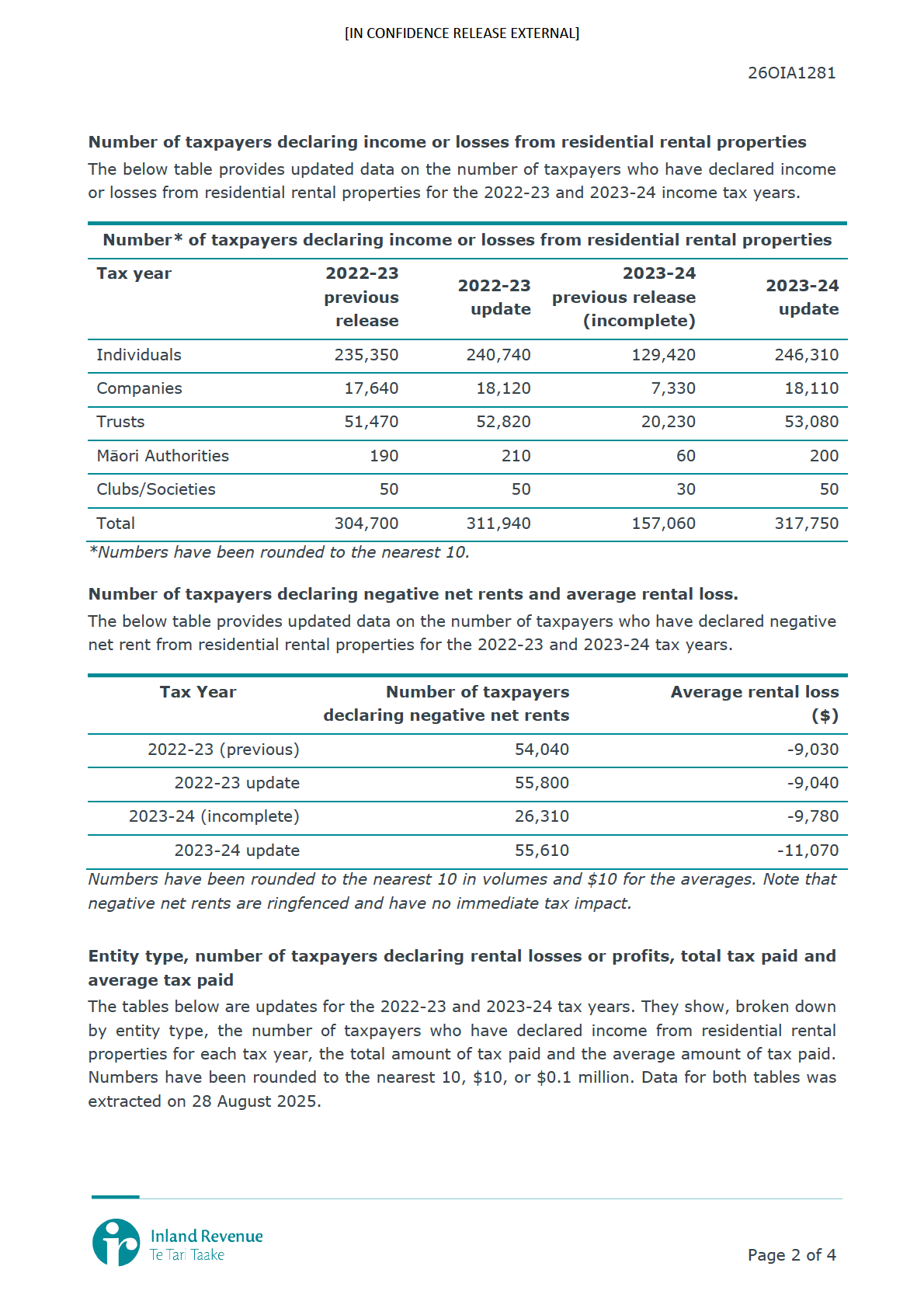

• Number of taxpayers declaring income or losses from residential rental properties

• Number of taxpayers declaring negative net rents and average rental loss

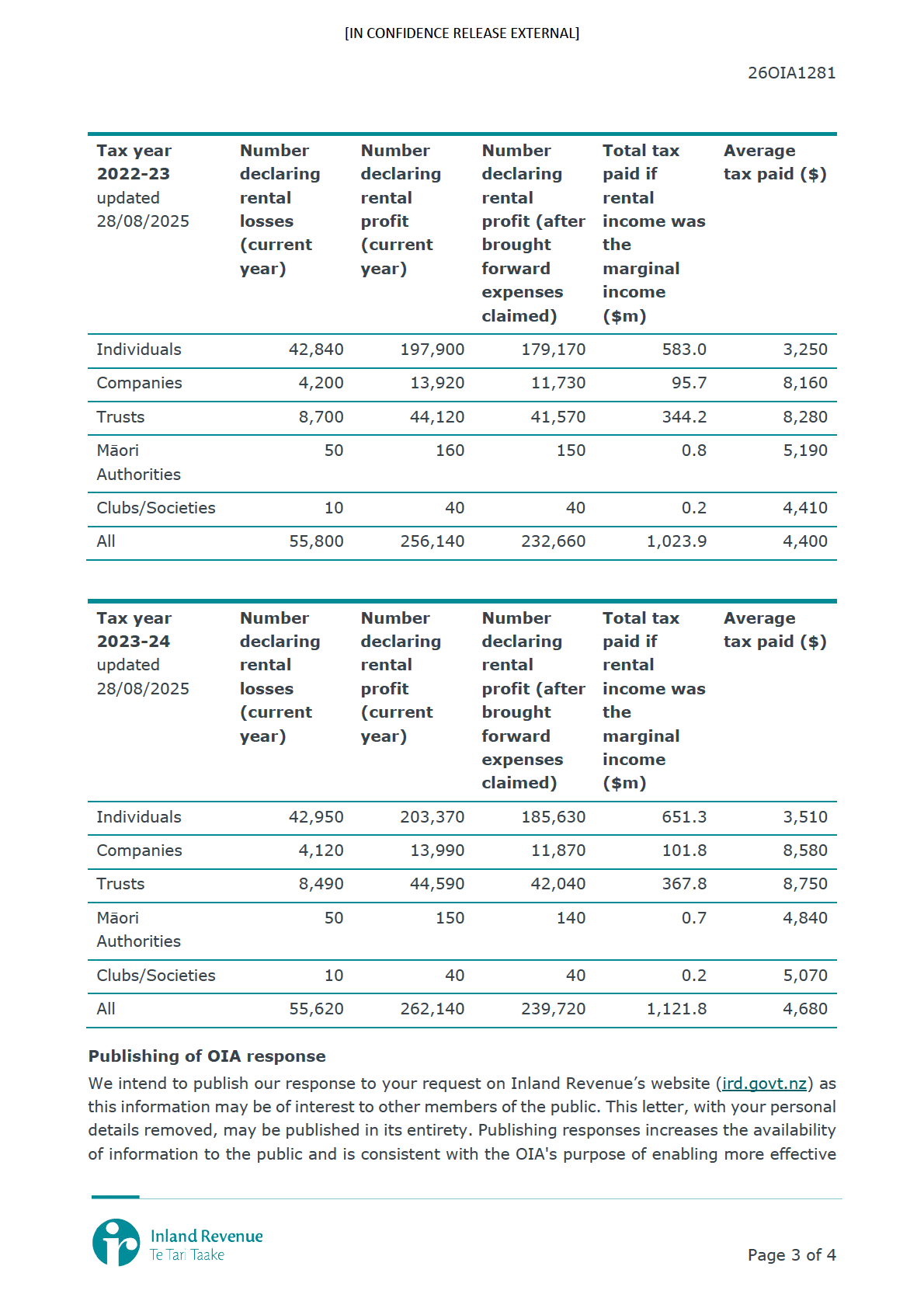

• For each year and broken down by entity type, the number of taxpayers declaring rental losses

or profits, total tax paid, and average tax paid.

On 8 September you requested:

Further to request 25OIA2086 and response to, please advise final information for 2024 tax

year.

The updated information you have requested has been detailed in a response to another OIA request

issued in September 2025. Please find attached a copy of that response.

Some information has been withheld in the attachment under section 9(2)(a) of the OIA, to protect

the privacy of a natural person. As required by section 9(1) of the OIA, I have considered whether

the grounds for withholding the information is outweighed by the public interest. In this instance I do

not consider that to be the case.

Please note that the updated information was extracted from income tax returns available in Inland

Revenue’s systems as at 28 August 2025.

Thank you again for your request.

Yours sincerely

Sandra Watson

Policy Lead – Forecasting & Analysis

Page 1 of 1

[IN CONFIDENCE RELEASE EXTERNAL]

26OIA1281

4 September 2025

s 9(2)(a)

Dear s 9(2)(a)

Thank you for your request made under the Official Information Act 1982 (OIA), received on 26

August 2025. You requested an update on previously supplied data on taxpayers with residential

rental property investments. We responded to previous requests from you in October 2024

(25OIA1443, 25OIA1444, 25OIA1445 and 25OIA1446 refer) at which stage the filing of tax

returns for the 2023-24 tax year was incomplete. The tables previously released covered the tax

years 2019-20 through to 2022-23, with incomplete data for 2023-24 on the following topics:

•

Number of taxpayers declaring income or losses from residential rental properties

•

Number of taxpayers declaring negative net rents and average rental loss

•

For each year and broken down by entity type, the number of taxpayers declaring rental

losses or profits, total tax paid, and average tax paid.

On 26 August 2025 you requested:

“I am writing to enquire as to whether or not the OIA request attached above can be

updated for the 2023/24 financial year? That is, if you have a final total for the numbers

covered by these questions for that year.”

Information released

Return filing for the 2023-24 tax year is now largely complete albeit not final as adjustments to

returns can continue for a number of years. We have updated both the 2022-23 and 2023-24

tax years in the tables below. The updates were extracted from income tax returns available in

Inland Revenue systems as at 28 August 2025.

A taxpayer is defined as having positive residential rental income if their residential rental income

is more than their reported current year residential deductions. Note that a taxpayer may not

have a tax obligation in that year if they can claim ring-fenced expenses from an earlier year to

offset the income. A taxpayer is defined as having negative residential rental income if their

residential rental income (2022-23 and 2023-24) is less than their reported current year

residential deductions. Note that negative residential rental income is ring-fenced and has no

immediate tax impact.

Calculations of tax paid on residential rental income are done as if the (positive) residential rental

income was the last dollar earned.

Page 1 of 4

Document Outline