[IN CONFIDENCE RELEASE EXTERNAL]

25OIA2204

13 May 2025

Nicholas Lee

[FYI request #30835 email]

Dear Nicholas Lee

Thank you for your request made under the Official Information Act 1982 (OIA), received on 27

April 2025. You requested the following:

I request access to all memos, communications and documents in the possession or under

the control of Inland Revenue related to "IRS Notice 2024-78" [link to notice]. I additionally

request access to all memos, communications, and documents related to "IRS Notice 2023-

11" [link to notice].

Of particular interest are any matters relating to the requirements set forth on page 8 of 2024-

78 and page 11 of 2023-11, regarding eligible Model 1 IGA jurisdictions.

I further kindly request that the documents include all communications between the

government and financial institutions regarding the obligation of Model 1 IGA countries [New

Zealand] as specified in the notice to "Encourage FFIs located in a Model 1 IGA jurisdiction to

not discriminate against U.S. citizens that do provide a U.S. TIN."

There are four requirements, hereafter referred to as Requirement (1) through (4), set out on

page 11 of

IRS Notice 2023-11 and page 8 of

IRS Notice 2024-78.

Information being released

There are three emails in scope of your request, detailed in the table below. I am partially

releasing these emails, attached as

Appendix A, with some information withheld under section

9(2)(a) of the OIA to protect the privacy of natural persons.

Please note that the information relating to Requirement (3) is included in the email dated 28

February 2025.

Item Date

Document

1.

23/01/2023 Email titled: Notice 2023-11 – FFI Temporary U.S. TIN Relief

2.

18/04/2023 Email titled: New TIN Codes For FATCA where a valid US TIN is not held for

reportable account.

3.

28/02/2025 Email titled: Extension of Temporary Relief for Foreign Financial

Institutions to Report U.S. Taxpayer Identification Numbers.

As required by section 9(1) of the OIA, I have considered whether the grounds for withholding

the information requested is outweighed by the public interest. In this instance, I do not

consider that to be the case.

Page 1 of 2

[IN CONFIDENCE RELEASE EXTERNAL]

25OIA2204

Information withheld and refused

I am withholding the information relating to Requirement (2) in full under section 6(b) of the

OIA, as the making available of that information would be likely to prejudice the entrusting of

information to the Government of New Zealand on a basis of confidence by the Government of

any other country or any agency of such a Government or any international organisation.

I am refusing your request for the information relating to Requirement (1) and Requirement (4)

under section 18(d) of the OIA, as the information is publicly available through the following

links:

Item Date

Document

Website address

1.

01/05/2018 IR1090: Foreign Account Tax

ird.govt.nz/international-

Compliance Act: provision of US

tax/exchange-of-

TINs

information/fatca/important-

documents

2.

12/06/2014 United States Intergovernmental

taxpolicy.ird.govt.nz/tax-treaties

Agreement (FATCA)

Right of review

If you disagree with my decision on your OIA request, you have the right to ask the Ombudsman

to investigate and review my decision under section 28(3) of the OIA. You can contact the office

of the Ombudsman by email at: [email address].

Publishing of OIA response

We intend to publish our response to your request on Inland Revenue’s website (ird.govt.nz) as

this information may be of interest to other members of the public. This letter, with your personal

details removed, may be published in its entirety. Publishing responses increases the availability

of information to the public and is consistent with the OIA's purpose of enabling more effective

participation in the making and administration of laws and policies and promoting the

accountability of officials.

Thank you again for your request.

Yours sincerely

Anu Anand Service Leader, International Revenue Strategy

Page 2 of 2

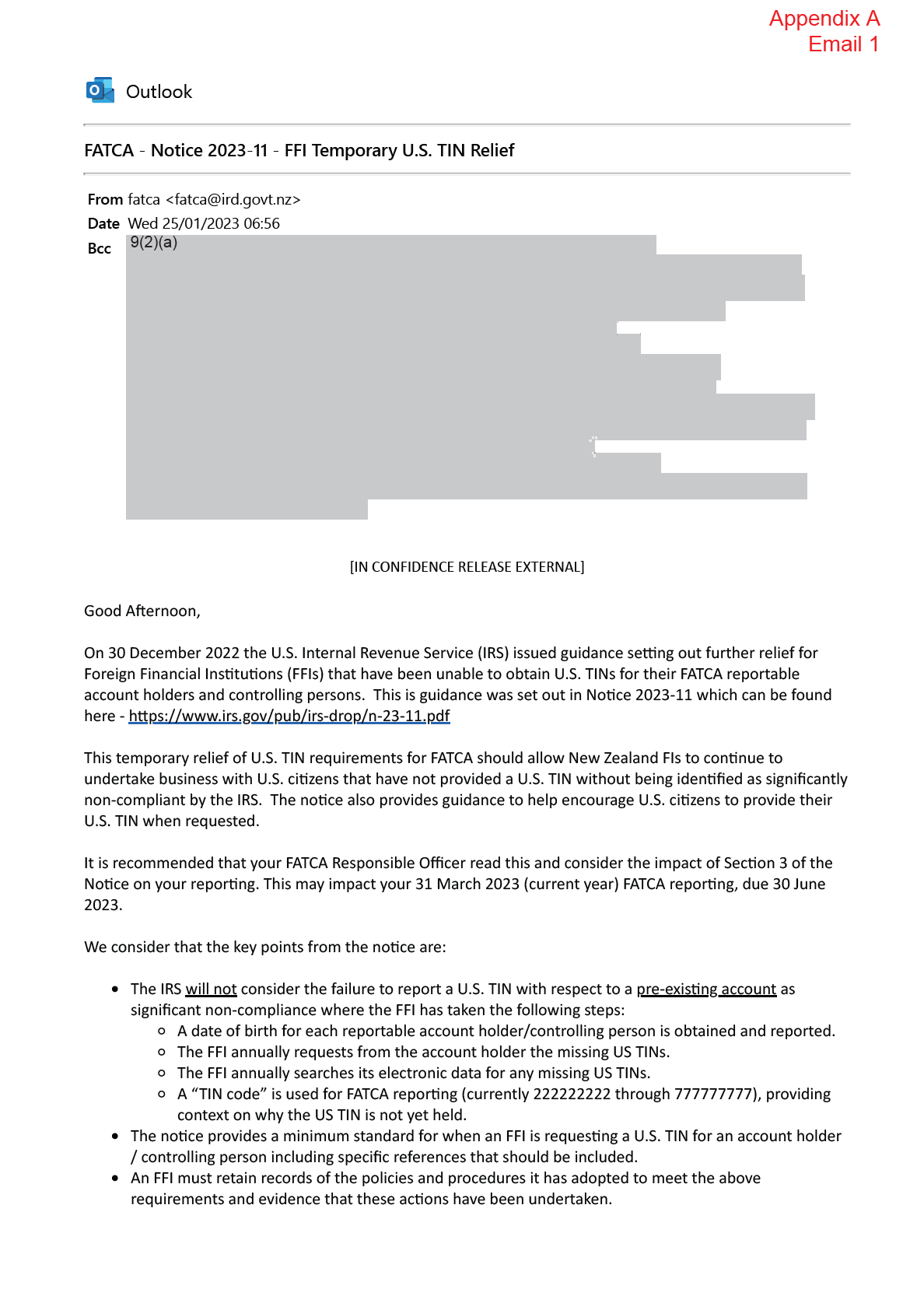

The use of “TIN codes” and date of birth information for FATCA reporting where a U.S. TIN has not been

obtained aligns with previous guidance from the IRS. New TIN codes will be issued in early 2023 by the IRS

however the existing TIN codes (issued May 2021) will remain valid for the current year FATCA reporting.

Kind regards

The FATCA Team.

IN CONFIDENCE

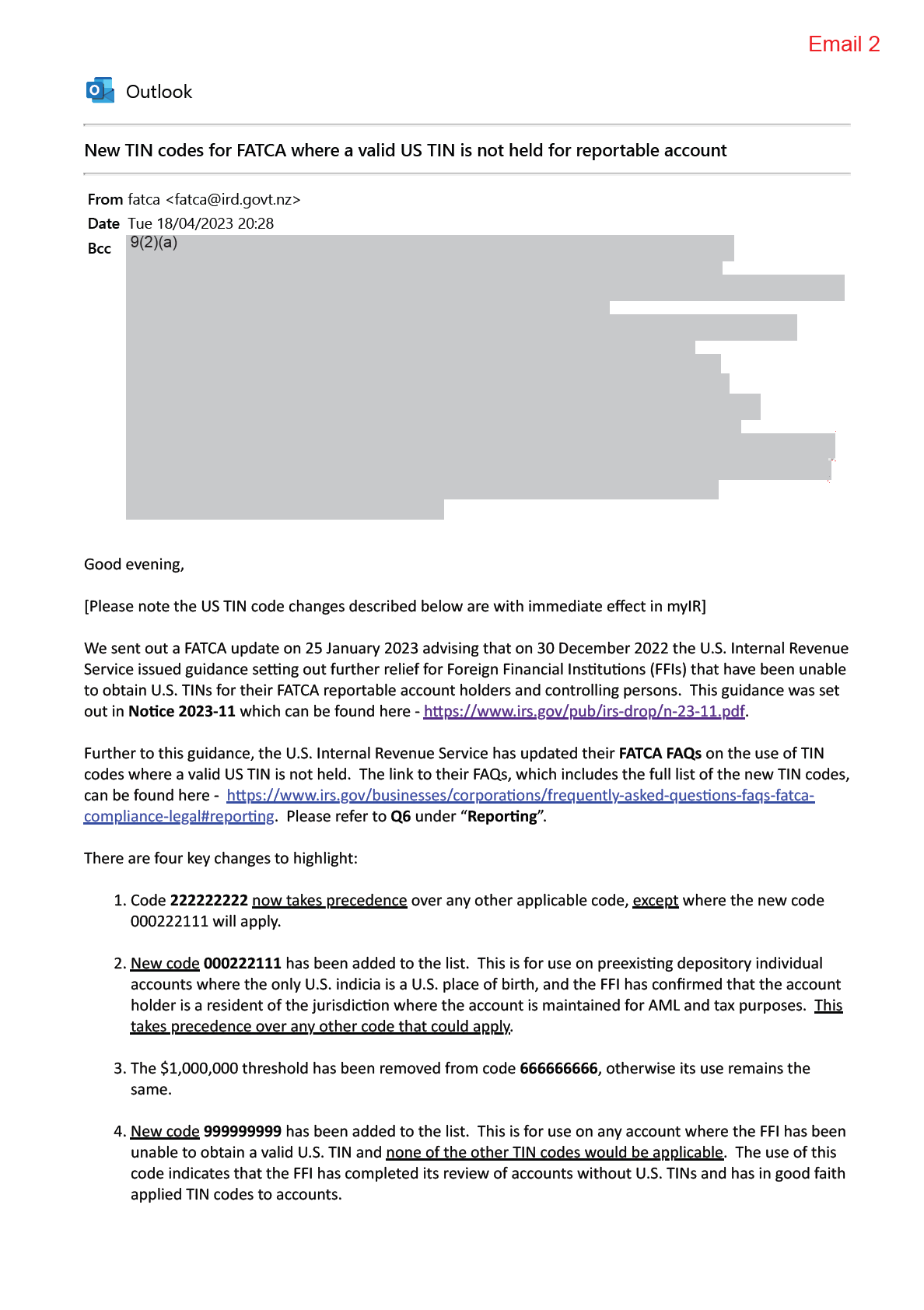

In addition, FFIs can no longer use the TIN code

AAAAAAAAA. You would be already aware that this was not a

valid TIN option for the previous reporting period when the U.S. Internal Revenue Service introduced the use

of TIN codes. The ongoing use of AAAAAAAAA does not meet the requirements for a FFI to get relief under

Notice 2023-11 and, as such, is no longer available to use. This change is effective now for all reporting years,

including prior year reporting. So, if you need to do any "new" or "corrected/amended" files in myIR for prior

year reporting the AAAAAAAAA TIN code cannot now be used.

Inland Revenue has implemented these changes in myIR to allow for these TIN code options to be used. If you

use the Excel option to report for FATCA, please ensure that you download and use the latest template that

has been now updated with the above chnages.

If you have any questions regarding the use of these TIN codes, please email us at [email address].

Kind regards

The AEOI Team | Inland Revenue CRS queries email: [email address] FATCA queries email: [email address] Link to our CRS/FATCA information: Exchange of information (ird.govt.nz) Wellington | New Zealand

In Confidence – External Release

Email 3

From:

fatca

Cc:

fatca

Subject:

Extension of Temporary Relief for Foreign Financial Institutions to Report U.S. Taxpayer Identification

Numbers

Date:

Friday, 28 February 2025 1:40:39 pm

[IN CONFIDENCE RELEASE EXTERNAL]

Dear Sir/Madam,

We are writing to advise about the implications of the latest Notice issued by the U.S. Internal

Revenue Service (IRS) for New Zealand Foreign Financial Institutions (FFIs) reporting for FATCA.

Notice 2024-78 provides an extension to the

temporary relief for FFIs that have not been able to

obtain U.S. TINs for their pre-existing FATCA reportable account holders and controlling persons.

Its extends, and adds to,

Notice 2023-11 (issued 30 December 2022) which outlines what FFIs

must do in order to obtain relief from the U.S. determining they are significantly non-compliant

with their FATCA obligations.

We consider that the key points from the notice are:

The relief extends for calendar years 2025, 2026, and 2027. This will not impact your 31

March 2025 (current year) FATCA reporting, due 30 June 2025. You should continue to

follow the guidance under Notice 2023-11 for the current year in order to obtain the relief.

It relates to pre-existing accounts only and does not apply to new accounts opened after

the IGA came into force.

FFIs must report a valid date of birth and use the prescribed TIN code where a U.S. TIN has

not been obtained.

The notice further sets out expectations for FFIs regarding their annual efforts to obtain

U.S. TINs and documentation of such efforts. An FFI must retain records until 2031 of the

policies and procedures it has adopted to meet these requirements and evidence that

these actions have been undertaken.

FFIs are asked not to discriminate against U.S. citizens that are captured by FATCA reporting

requirements.

Further information:

Notice 2024-78: Notice 2024-78, Extension of Temporary Relief for Foreign Financial

Institutions to Report U.S. Taxpayer Identification Numbers

Notice 2023-11: Foreign Financial Institution Temporary U.S. Taxpayer Identification

Number Relief

If you have any questions, please email us at [email address].

Kind Regards,

The AEOI Team

Inland Revenue | Wellington | New Zealand

CRS queries: [email address] | FATCA queries [email address]

Link to our CRS/FATCA information: Exchange of information (ird.govt.nz)