CLASSIFICATION

Cabinet talking points for oral item on industrial

allocation updates

Purpose

1. This aide memoire attaches talking points for an oral item to the Cabinet meeting of 8

July 2024 on industrial allocation updates.

Background

2. Communications will soon be issued to firms receiving industrial allocation. We will

inform those firms of their new allocative baselines1, which have been determined

following our recent data collection and review exercise. The eventual regulatory

updates will impact all allocations for 2024 onwards.

3. Additionally, you and Hon Simeon Brown have proposed to meet with NZ Steel to

provide your decision on industrial allocation for co-generated electricity.

4. The oral Cabinet item gives your colleagues early notice of those communications. It is

possible firms could react to the communications and ask questions of Ministers.

5. Stakeholders could raise other questions on industrial allocation, such as on the

Government’s work on alternatives like a carbon border adjustment mechanism, and on

increasing the allocation phase out rates.

6. The attached talking points note that as the Minister responsible for industrial allocation

policy in the emissions trading scheme, you are the Minister best placed to respond to

such enquiries. The talking points also provide background information on industrial

allocation and some data on the magnitude of changes.

Next steps

7. Following the oral item to Cabinet, we will email the new allocative baselines to firms

receiving industrial allocation. We will note they are not final numbers as further changes

are expected for updates to the general electricity allocation factor (being reported to you

by the Electricity Authority at the end of July) and for other emission factor changes.

8. Final allocative baselines will be set through amendment regulations later this year. We

will reengage with firms after those decisions.

1 Annual allocation = allocative baseline (emissions per unit of production for that industrial activity) ×

(amount of production in the year by the firm) × (rate of assistance for that industrial activity, being

66% or 86%). The rate of assistance is being reduced one percentage point per year until 2030, and

two percentage points from 2031.

BRF-5001

2

CLASSIFICATION

CLASSIFICATION

9. We wil also work with your office and the Minister for Energy’s office to set a meeting

with NZ Steel. A draft Cabinet paper is being prepared that seeks Cabinet agreement to

the policy change. You will receive a draft before 25 July.

10. We note that no decision has been made on a review of industrial allocation phase out

rates for specific industries. We have not covered that work in the talking points, but if it

proceeds, careful communications will be needed with impacted firms and potentially

with your Cabinet colleagues. Those matters were discussed in our briefing BRF-4875.

Signatures

Kate Whitwell

Manager, ETS policy

Climate Change Mitigation and Resource Efficiency

4 July 2024

Hon Simon WATTS

Minister of Climate Change

Date

BRF-5001

3

CLASSIFICATION

CLASSIFICATION

Talking points for Cabinet on industrial allocation updates

•

I wish to inform Ministers of updates to the number of emission units the Government will be

providing to firms from this year. A particular matter concerns NZ Steel.

•

Industrial allocation is a $350 million fiscal cost to the Crown every year. It is being phased out

at 1 percentage point per year until 2030.

•

The purpose of industrial allocation is to shield firms in certain emissions intensive and trade

exposed industries from facing full emission costs.

•

Because those firms compete in international markets, emission pricing puts them at a

material cost disadvantage.

•

Allocations have been made using very old data until now. That data is from 2006 to 2009.

•

New data has been collected and rates of allocation will be updated before the end of this

year. This will impact allocations for 1 January 2024, onwards. This is part of implementing

reform legislation from last year.

•

The net reduction in the Crown’s cost for industrial allocation from updates to rates of

allocation, excluding matters relating to NZ Steel or NZAS, is expected to be roughly 150,000

NZUs or 2.5% or $9 million per year.

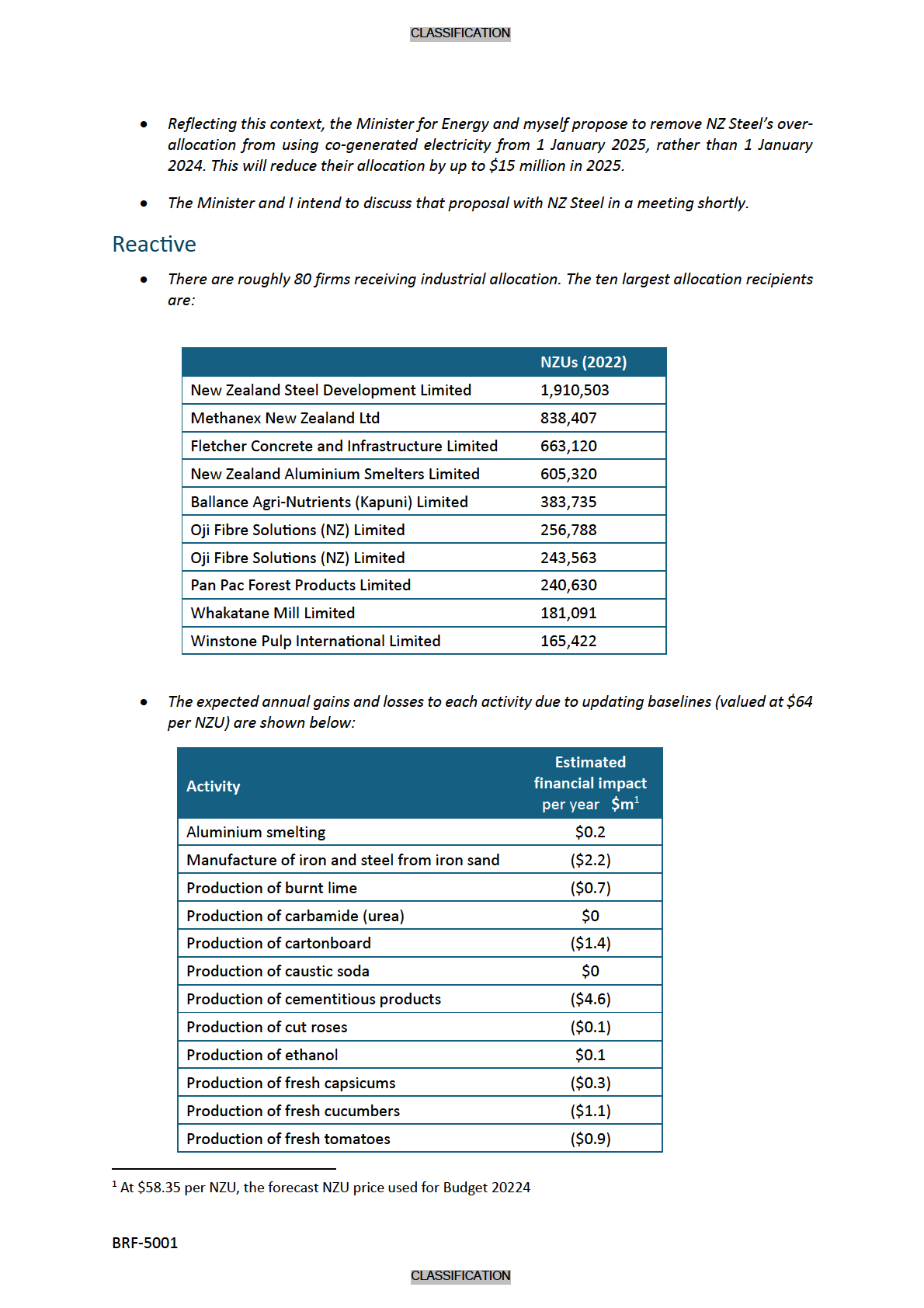

•

Firms impacted range from small glasshouse tomato and rose growers to some our largest

firms such as Methanex.

•

My officials will communicate these new rates of allocation to firms in the coming days. This

will help those businesses prepare for the new settings.

•

Some businesses may raise concerns with Ministers. Other questions on the framework and

future of industrial allocation may also appear. I am already aware of concerns from Fletcher

Building regarding these changes.

•

I ask Ministers to direct such concerns to myself for addressing.

•

Additionally, the Minister for Energy and I have agreed to a proposal concerning NZ Steel’s

industrial allocation. That proposal is subject to Cabinet consideration in the near future.

•

NZ Steel has been receiving industrial allocation since 2010 for consuming electricity from its

cogeneration plant. But that electricity is not impacted by emissions pricing.

•

The Crown has a funding agreement with NZ Steel for the installation of an electric arc furnace.

Considerable resources have been put into that project from the Crown and NZ Steel to date.

•

The project is running ahead of schedule and is expected to deliver one million tonnes of

emission reductions per year from the end of 2025.

•

NZ Steel has written to the Ministry for the Environment linking the future of that project with

changes to the industrial allocation treatment of their cogeneration electricity use.

BRF-5001

CLASSIFICATION

CLASSIFICATION

Production of glass containers

$0.1

Production of hydrogen peroxide

($0.1)

Production of lactose

($0.3)

Production of market pulp

($0.7)

Production of methanol

$2.3

Production of packaging and industrial paper

$1.2

Production of protein meal

$0.9

Production of reconstituted wood panels

($0.2)

Production of tissue paper

($0.6)

Production of whey powder

($0.1)

•

Some individual firms will be more impacted than others. For example, Fletcher Building may

have its rate of allocation for making clinker2 reduced by up to 15% (approximately $5 million

per year).

•

While the allocative baselines decrease for most industries, they increase for others. These

tend to be highly natural gas dependent activities like producing methanol. Because the

greenhouse gas intensity of natural gas increases as a well is drawn down, the emissions from

using that gas in production will increase.

•

The assessment of the data by officials found two reasons for reductions in rates of allocation:

o

Industry changes, where more polluting firms have closed over time, meaning the

industry emissions per unit of production is now better than it was previously.

o

Efforts to reduce emissions in the last decade, such as through switching from using

coal to electricity.

2 The most emissions intensive component of producing cement

BRF-5001

CLASSIFICATION