Key messages

1. Of icials invite feedback on the draft “Strengthening the NZ ETS” section of the

consultation on the second emissions reduction plan (ERP2), which reflects advice in

this paper. See

Appendix One.

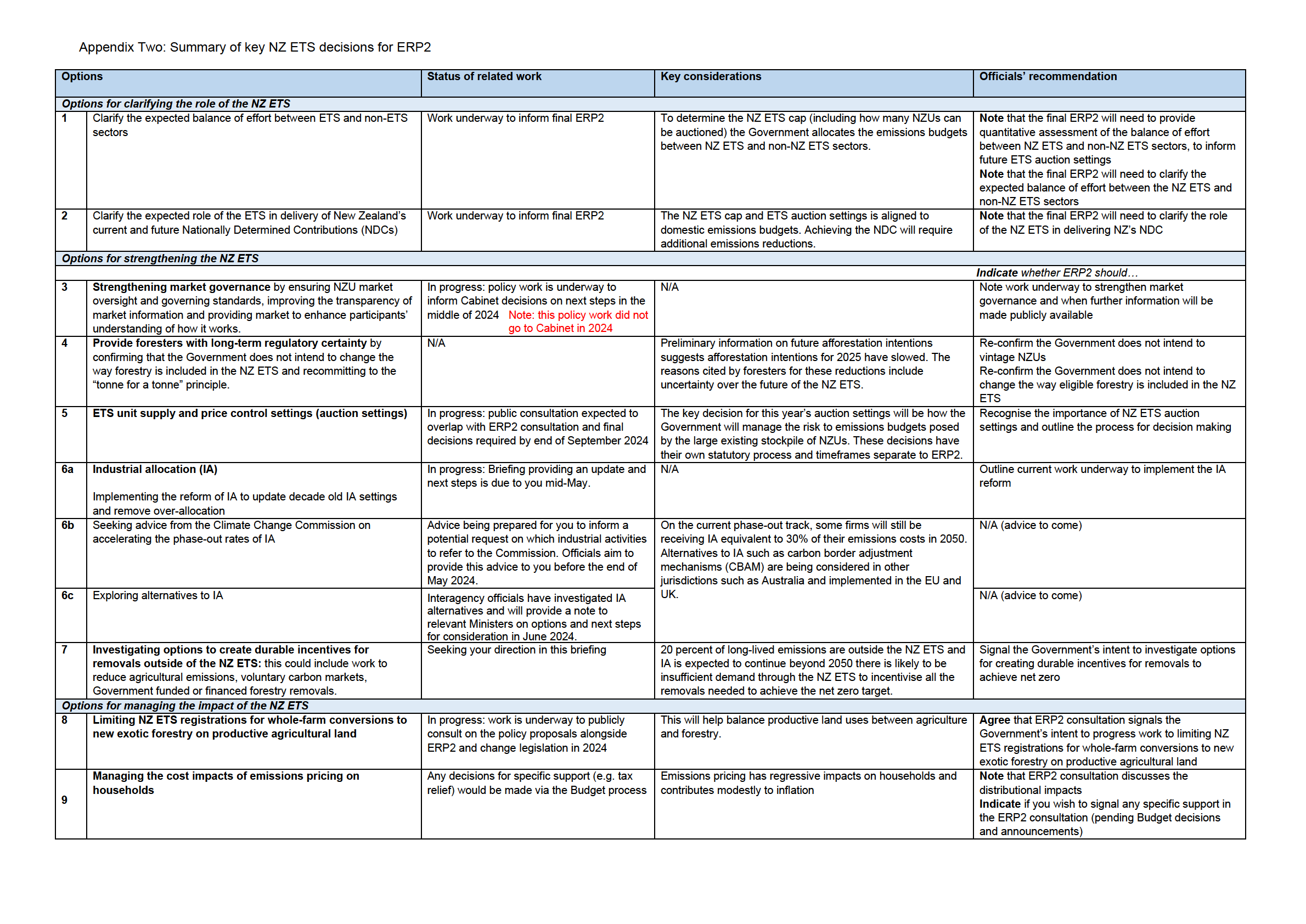

2. Of icials recommend using the development and publication of ERP2 to clarify the role of

the NZ ETS in the Government’s strategy and outline relevant areas of work.

Appendix

Two provides a summary of how officials propose this be sequenced.

3. A key part of the Government’s climate mitigation approach is to restore a market-led

approach by using the NZ ETS to follow the most efficient, flexible, and cost-effective

path to 2050. The effectiveness and credibility of the Government’s overall strategy wil

therefore be driven largely by its management of the NZ ETS.

4. The NZ ETS supports a least-cost strategy by allowing NZ ETS participants to determine

the cheapest way to meet their NZ ETS obligations. However, the NZ ETS does not

guarantee a given emissions outcome in the short term (i.e. within an emissions budget),

due to the ability to bank NZUs across budget periods, and the large existing stockpile.

5. The most recent updates to interim emissions projections suggest that the ability to meet

emissions budgets has become more challenging compared with projections from

December 2023. The central estimates for New Zealand’s emissions for EB2 and EB3

are above emissions budgets limits but stil within the uncertainty bands of the modelling

(BRF-4682 refers). We recommend the Government considers options to strengthen the

NZ ETS, to help manage this increased risk.

6. Restoring market confidence and stability to the NZ ETS to help ensure a credible

market to support emissions reductions and the economy is one of the Government’s

key climate priorities. Explaining how the Government intends to manage the NZ ETS

wil be central to this and includes clarifying its role, how the Government intends to

strengthen the NZ ETS and how it wil manage any NZ ETS impacts.

7. It wil be important to clarify both the expected balance of effort between NZ ETS and

non-NZ ETS sectors and the expected role of the NZ ETS in delivery of New Zealand’s

current and future Nationally Determined Contributions (NDCs).

8. Policy options to strengthen the NZ ETS include the following. Some of these are longer-

term than EB2, but providing clear long-term signalling about potential future policy

directions, and inviting feedback at this stage, helps to avoid surprises and support

market confidence in the near term:

a. Enhancing market governance, assurance and operations.

b. Providing foresters with long-term regulatory certainty, to encourage afforestation.

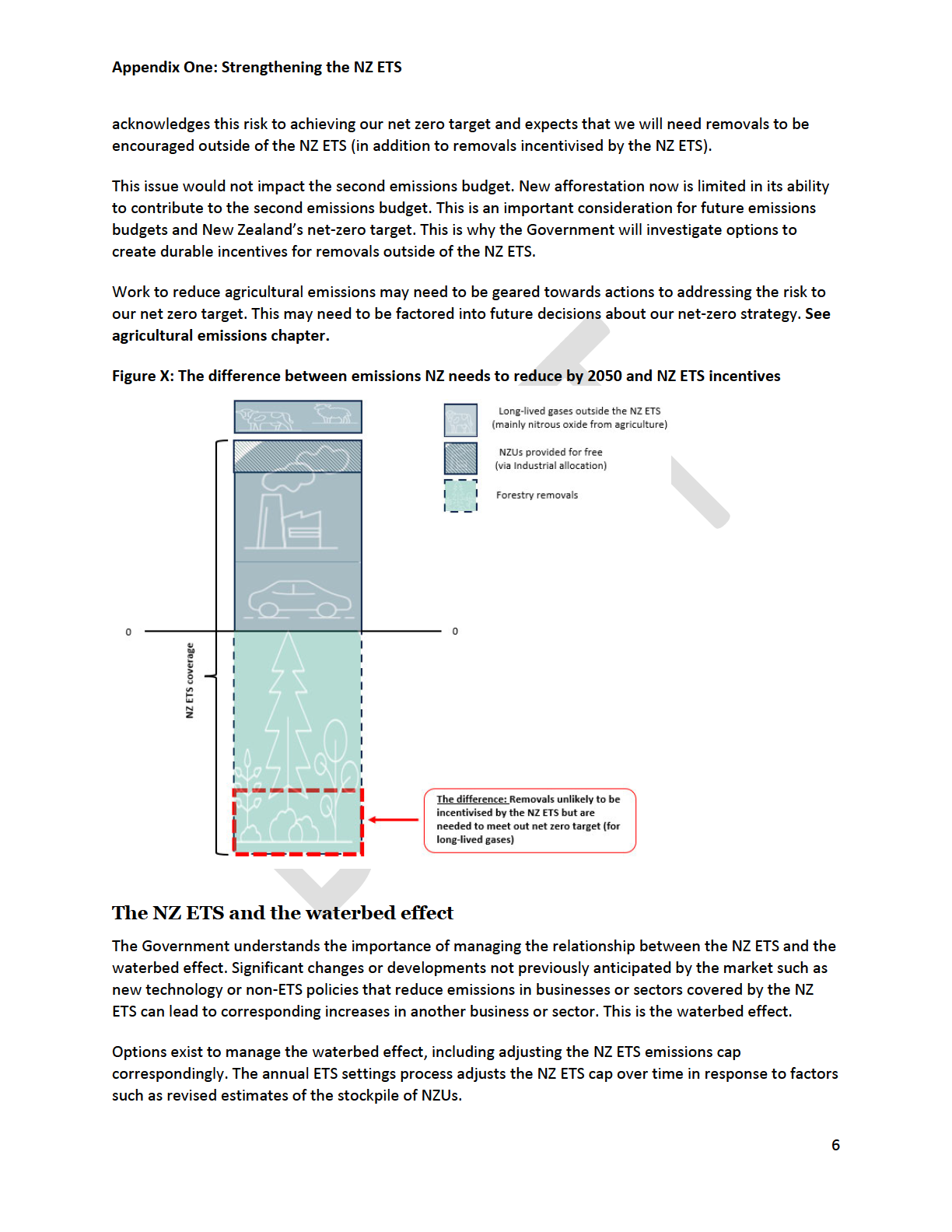

c. Taking decisions on NZ ETS unit supply and price control settings (auction settings)

to manage the risk the stockpile poses to achievement of EBs.

d. Determining next steps for work on Industrial Al ocation (IA).

e. Creating durable incentives for removals, outside and in addition to the NZ ETS, to

achieve net zero.

BRF-4718

2

9. The Government can also provide clarity by setting out how it wil manage any impacts

of the NZ ETS, including balancing productive land uses between agriculture and

forestry and managing the cost impacts of emissions pricing on households.

Recommendations

We recommend that you:

a.

note that the New Zealand Emissions Trading Scheme (NZ ETS) is central to the

Government’s plan to follow the most efficient, flexible, and cost-ef ective path to 2050,

and the effectiveness of the Government’s overall strategy wil therefore be driven largely

by its management of the NZ ETS

b.

note that

the NZ ETS does not guarantee a given emissions outcome within an

emissions budget, due to the ability to bank NZUs across budget periods, and the large

existing stockpile

c.

note the most recent updates to interim emissions suggest that the ability to meet

emissions budgets has become more challenging compared with previous projection

from December 2023

d.

note that of icials therefore recommend the Government considers options to strengthen

the NZ ETS to help ensure a credible market to better incentivise net emissions

reductions

Opportunities to clarify the role of the NZ ETS

e.

note that the final ERP2 wil need to provide a quantitative assessment of the balance of

effort between NZ ETS and non-NZ ETS sectors, to inform future NZ ETS auction

settings

f.

note that the final ERP2 wil need to clarify the role of the NZ ETS in delivering NZ’s NDC

Options to strengthen the NZ ETS

g.

indicate whether ERP2 consultation should:

i

Note work underway to enhance market governance, assurance and

Yes / No

operations, and when further information wil be made publicly

available

ii Re-confirm the Government does not intend to vintage (or place

Yes / No

expiry dates on) NZUs

iii Re-confirm the Government does not intend to change the way

Yes / No

eligible forestry is included in the ETS, and re-commit to the ‘tonne for

a tonne’ principle

iv Recognise the importance of NZ ETS auction settings, and outline the Yes / No

process for decision-making

BRF-4718

3

v Outline current work underway to implement the 2023 IA reform

Yes / No

vi Recognise the risk that, under current set ings, the NZ ETS will not

Yes / No

incentivise sufficient removals to achieve the 2050 net zero target

vii Signal the Government’s intent to investigate options for creating

Yes / No

durable incentives for removals to achieve net zero (outside, and in

addition to, the NZ ETS)

h.

note advice is due to you for your consideration on other options relating to industrial

allocation to strengthen the NZ ETS in May and June

Options for managing the impact of the NZ ETS

i.

agree that ERP2 consultation should outline the Government’s approach to Yes | No

managing NZ ETS impacts, particularly an approach to balancing

productive land uses between agriculture and forestry

j.

note that ERP2 consultation discusses the distributional impacts

k.

indicate if you wish to signal any specific support (e.g. tax relief) in the ERP2

consultation (pending Budget decisions and announcements)

Next steps

l.

provide feedback on the draft emissions pricing section of ERP2 consultation.

Signatures

Mark Vink

Hon Simon WATTS

General Manager

Minister of Climate Change

Markets

Date:

Date: 9 May 2024

BRF-4718

4

NZ ETS and the second emissions reduction plan

Purpose

10. This briefing seeks your direction on:

i

key decisions required to progress the NZ ETS work programme

ii whether to signal these in the ERP2 consultation.

11. It also seeks your feedback on the draft NZ ETS content for the ERP2 discussion

document.

Background

12. The NZ ETS has an important role to play in supporting the Government’s least-cost

strategy by allowing NZ ETS participants to determine the most cost-effective way to

reduce their NZ ETS obligations. However, the NZ ETS does not guarantee a given

emissions outcome in the short term (i.e. within an emissions budget), due to the ability

to bank NZUs across budget periods, and the large existing stockpile.

13. The Government can restore market confidence and stability to the ETS to help ensure a

credible market to support net emissions reductions and the economy by (1)

clarifying

the role of the NZ ETS, (2)

strengthening the NZ ETS such as through the annual NZ

ETS auction settings (e.g. by reducing unit supply) by (3)

managing the impacts of the

NZ ETS.

14. Of icials have prepared a draft section of the ERP2 consultation, titled “Strengthening

the NZ ETS”. See

Appendix One. This draft section reflects advice in this briefing about

what NZ ETS policy work could be signalled, to al ow stakeholders to provide feedback

both on NZ ETS specific matters as well as to provide insight on the Government’s wider

approach to climate change mitigation.

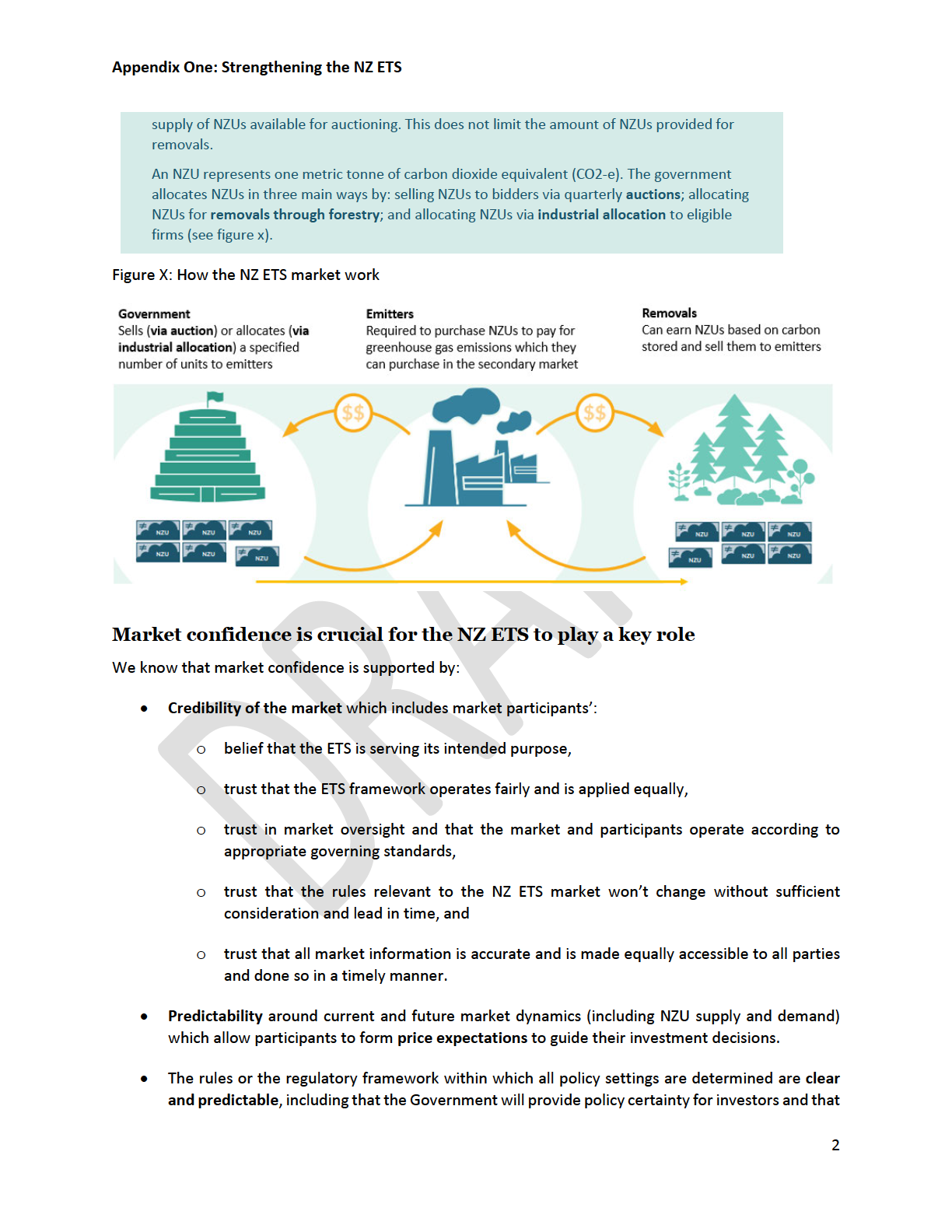

Auction volumes wil decline as the NZ ETS cap is reduced in line with emissions budgets

15. This means the influence auction settings have on the NZ ETS market wil decline, as

wil the Government’s ability to use auction settings to influence NZ ETS outcomes.

Based on current settings, but stil subject to future auction settings decisions, we

anticipate auctions may end around 2033. We expect forestry NZUs to then be the major

form of NZU supply.

Clarifying the role of the NZ ETS

16. The Government can support market confidence, stability, and credibility by clarifying the

expectation of the NZ ETS.

BRF-4718

5

Determining the balance of effort between NZ ETS and non-NZ ETS sectors

17. To determine the NZ ETS cap (including how many NZUs can be auctioned) the

Government allocates the emissions budgets between NZ ETS and non-NZ ETS.

Decisions to date have based this on the sector sub-targets outlined in ERP1.

18. The more explicit final ERP2 is about the Government’s intended approach to gross and

net emissions reductions [BRF-4430 refers] and the balance of effort between NZ ETS

and non-NZ ETS sectors, the more clarity this will provide to NZ ETS market

participants. This will also inform future decisions on NZ ETS auction settings. Advice

wil be provided to you later in the year informed by consultation feedback to inform

relevant decisions for the final EPR2.

19. As auction volumes decline, the Government’s ability to influence this balance of effort

via the NZ ETS wil be significantly constrained.

Clarifying the expected role of the NZ ETS in delivery of New Zealand’s NDCs

20. The NZ ETS cap and NZ ETS auction settings are aligned to domestic emissions

budgets. Achieving the NDC wil require additional emissions reductions.

21. The Government could tighten the NZ ETS cap beyond what is needed to achieve

emissions budgets, as part of a plan to achieve the NDC.

22. The NZ ETS auction settings consultation process is testing whether NZ ETS settings

should be adjusted to account for additional policies that reduce emissions. Should

Cabinet agree to adopt this approach, it could be outlined in the final ERP2 when

published. This approach would support delivery of the NDC, though wil reduce the

supply of NZUs via auction. Al other things being equal, this would place upward

pressure on prices and potentially less auction revenue (depending on the relationship

between number of units sold and price of these units).

23. Although reduced auction volume wil reduce the ‘cap’ and can strengthen the NZ ETS, if

auction volume ends in the 2030s this would limit the Government’s ability to incentivise

additional abatement via the NZ ETS and therefore the ability of the NZ ETS to make

additional contributions to future NDCs.

Strengthening the NZ ETS

24. The Government has opportunities to strengthen the NZ ETS within its existing

parameters, without significant structural reform. Some of this work is already underway,

we are seeking your direction on whether you wish to pursue further work and what you

want to signal this in ERP2 consultation.

Enhancing market governance, assurance and operations

25. The Government is working to strengthen market governance. In particular, the

Government wants to ensure there is appropriate oversight of, and standards governing,

the NZU market. The Government is also exploring ways of improving the transparency

of market information, and ways of providing information about the market to enhance

participants’ understanding of how it works.

BRF-4718

6

26. The draft ERP2 discussion document notes this work is underway.

Providing foresters with long-term regulatory certainty

27. Forestry’s contribution to EB2 is largely locked in (due to the lag between planting and

significant volumes of carbon removals). Restoring confidence to the forestry sector to

encouraging afforestation now wil make a significant contribution from EB3 onwards.

28. Preliminary information on future afforestation intentions suggests afforestation

intentions for 2025 have slowed from just over 50,000 hectares (2022/23 survey) to

around 17,000 hectares (2023/24 survey). The reasons cited by foresters for these

reductions include uncertainty over the future of the ETS.

29. ERP2 consultation can support regulatory certainty by reconfirming that the Government

does not intend to change the way eligible forestry is included in the NZ ETS, and

recommit ing to no vintaging of (placing expiry dates on) NZUs and to the “tonne for a

tonne” principle.

30. The Land Use Class policy discussed in paragraph 44 is relevant to regulatory certainty

for forestry entering the NZ ETS. As with any new regulation, development of this policy

may contribute to some short-term uncertainty for foresters, which wil be resolved as the

new policy is implemented.

NZ ETS auction settings

31. A key decision for this year’s auction settings wil be how the Government will manage

the risk to emissions budgets posed by the large existing stockpile of NZUs.

32. These decisions have their own statutory process and timeframes. Of icials therefore

recommend that ERP2 consultation reiterates why these decisions are important, and

outline the process which is being followed, but not provide technical detail or invite

further input from stakeholders.

33. Final decisions on ETS auction settings wil be made public by the end of September.

The final ERP2 could include discussion and explanation of these decisions.

Next steps for industrial al ocation

34. Reforms were legislated last year to update decade old IA settings and remove over-

allocation. The ERP2 consultation notes this as an area of ongoing work.

35. IA is being phased-out.1 On the current phase-out track, some firms will still be receiving

IA equivalent to 30% of their emissions costs in 2050. The Climate Change Response

Act 2002 establishes a process by which the Government can consider whether these

phase-out rates are appropriate, on an activity-by-activity basis. This statutory process

includes seeking advice from the Climate Change Commission. Advice is being

prepared for you to inform a potential request on which industrial activities to refer to the

Commission. Of icials aim to provide this advice to you before the end of May 2024.

1 The rate of IA issued to participants declines each year according to legislated default phase-out

rates. These rates are 1 percentage point per annum until 2030, 2 percentage points per annum from

2031-2040, and 3 percentage points per annum from 2041 onwards.

BRF-4718

7

36. Alternatives to IA such as carbon border adjustment mechanisms (CBAM) are being

considered in other jurisdictions such as Australia and implemented in the EU and UK.

Following a commitment in the first emissions reduction plan, interagency officials have

investigated IA alternatives and wil provide a note to relevant Ministers on options and

next steps for consideration in June 2024.

Creating durable incentives for removals to achieve net zero

37. To achieve New Zealand’s net zero target for 2050 and beyond, all remaining

greenhouse gas emissions (except for biogenic methane), wil need to be matched by a

removal each year.

38. There is likely to be insufficient demand through the ETS to incentivise all the removals

needed to achieve the net zero target, posing a risk to achieving this target because:

i

A significant amount (approximately 7.5Mt per annum or 20%) of emissions covered

by New Zealand’s net zero target (such as agricultural nitrous oxide) are outside the

NZ ETS. Even with non-NZ ETS policies (such as measures to accelerate

development and rollout of agricultural mitigation technologies and agricultural

emissions pricing) to reduce these emissions, it’s unlikely they wil reduce to zero so

there wil be some need for removals to offset them by and beyond 2050.

ii Under current settings, some industrial emitters carrying out emissions-intensive

and trade-exposed activities wil continue receiving some NZUs for free (via IA)

beyond 2050.

39. This issue was raised by the Climate Change Commission in its advice to the

Government on ERP2.

40. This issue wil not impact achievement of the second emissions budget, so the

Government could choose not to address it in ERP2. It is an important consideration for

future emissions budgets and for setting New Zealand on a pathway to achieving the

net-zero target. Due to the lag between planting and significant volumes of carbon

removals, officials recommend beginning policy work now to consider durable incentives.

41. Of icials recommend the Government recognise this issue in ERP2 consultation and

commit to developing options to address it.

42. You have also indicated an interest in a framework for rewarding additional forms of

removals i.e. non-forestry. These are currently discussed in a separate section of the

draft ERP2 discussion document.

Managing the impacts of the NZ ETS

43. Market confidence can be supported by the Government being clear on which NZ ETS

impacts it proposes to address and how. It can provide the market with a level of

confidence that flow on impacts of the NZ ETS are being managed and the Government

is therefore less likely to make unanticipated interventions such as via the NZ ETS.

BRF-4718

8

Balancing productive land uses

44. Progressing and completing the design and implementation of limits on NZ ETS

registrations for whole-farm conversions to new exotic forestry on productive agricultural

land wil support regulatory certainty for the forestry sector. Of icials recommend that the

ERP2 consultation outlines the Government’s intent to progress this. This is included in

both the NZ ETS and forestry sections of the ERP2 discussion document. 9(2)(g)(i)

45. How forests are managed also has implications for adaptation – the Forestry chapter of

the ERP2 discussion document sets out the Government’s approach to managing the

adaptation risks and opportunities of forestry.

Managing socioeconomic impacts

46. Emissions pricing has regressive impacts on households and contributes modestly to

inflation.2 Indexation of benefits provides partial compensation to the lowest income

households. The Treasury estimates that 72-84% of low-income households receive

some form of indexed payment, and these payments compensate for between 40-80%

of increasing costs from emissions pricing (depending on the benefit received).

47. The final ERP2 must include a plan for managing the impacts of climate change

mitigation including distributional impacts. Officials recommend that ERP2 discusses

distributional impacts of the NZ ETS more broadly, including via the content on

distributional impacts. You may want to signal any specific support (e.g. tax relief)

agreed via the Budget process in the NZ ETS content of the ERP2 discussion document.

Other considerations

48. Any Tiriti, legal, financial, regulatory, or legislative implications would be canvased in any

further briefings on related work.

Next steps

49. We seek your feedback on the draft NZ ETS content for the ERP2 discussion document,

in particular any changes needed to either the substantive content, or the overall framing

in the week beginning 13 May, so we can incorporate it into the full EPR2 discussion

document due to you the following week.

50. Of icials will also reflect any work you want to signal in ERP2 consultation in the paper

seeking Cabinet’s approval to consult on ERP2.

51. Of icials also seek your direction on whether you want to take an NZ ETS work

programmes Cabinet paper in the second half of 2024. Informed by ERP2 consultation.

2 A $10 increase in the ETS price increases consumer inflation by about 0.1%, mostly through its

impact on fuel and electricity prices.

BRF-4718

9

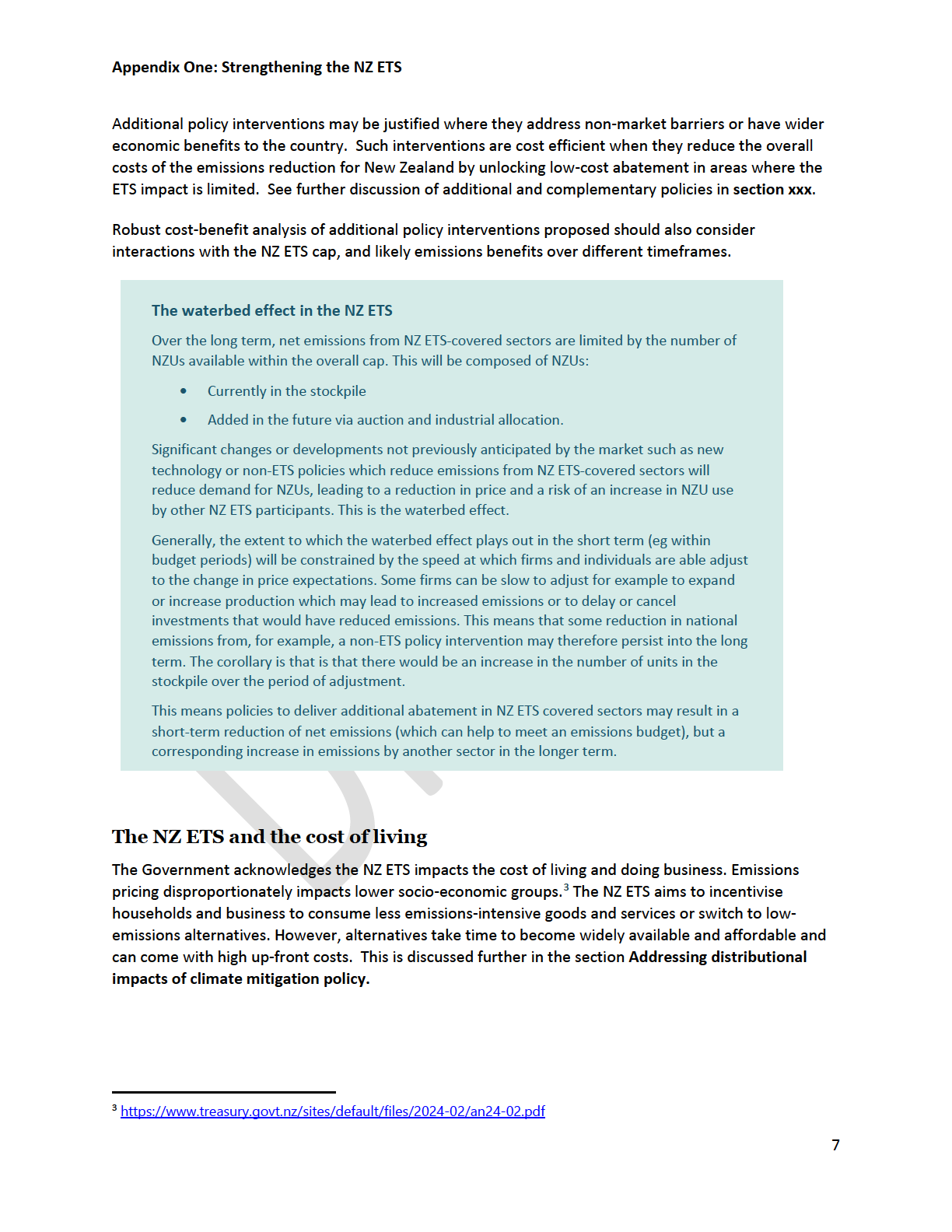

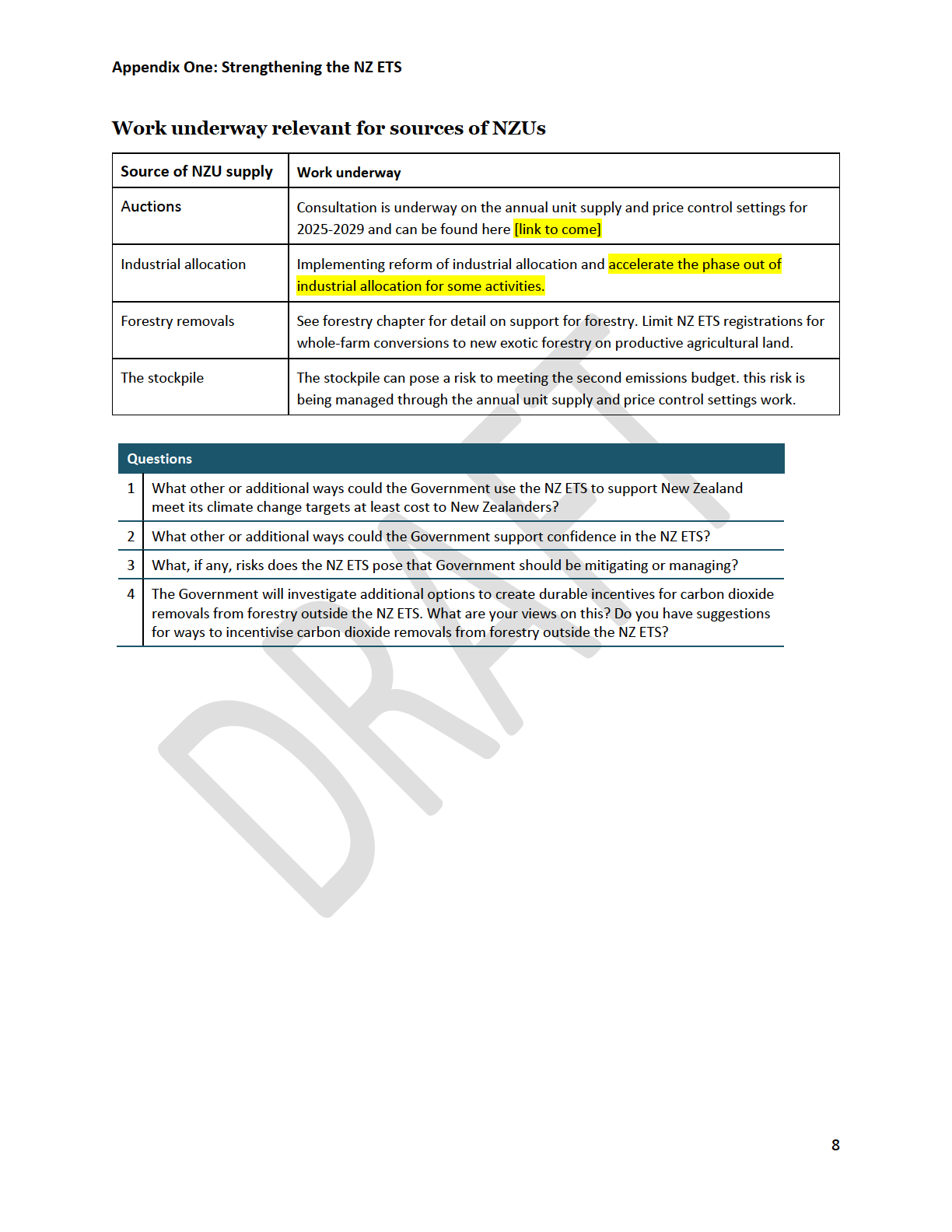

Appendix One: Strengthening the NZ ETS

BRF-4718

10

Appendix Two: Summary of key NZ ETS decisions for ERP2

BRF-4718

11