Initial thoughts on recommendations

Initial thoughts on recommendations

Our initial impression is the report is somewhat unbalanced, lacking a holistic quantitative

assessment of the impact of prudential requirements on competition, and is silent on the expected

scale of benefits of changes in regulation, including in relation to the other areas covered in the

recommendations. It tends to focus on specific elements such as risk weights in limiting

competition but dismissing the impact the D-SIB buffer - which our analysis suggests largely

cancel each other out. The report also seems to underplay how we already, and will continue to,

consider competition elements within our policy development and that fact that competition is one

of many principles we legally need to consider in pursuing our primary objective of promoting

financial stability.

Capital requirements (recommendation 1) are highlighted as an ongoing competitive barrier,

despite the significant changes made as part of the Capital Review (85% floor on IRB models, 2%

DSIB buffer requirement). While there is still a difference in capital outcomes between the large and

small banks, the report doesn't provide much detail on the materiality of this in terms of the extent

to which it affects the average cost of banks' funding.

We provided the Commission with some illustrative estimates of the impact that the capital

differences imply for banks' loan pricing, which suggested the difference in capital requirements

could amount to c. 9bps prior to the Capital Review changes, and ?bps afterwards (0bps if the

DSIB buffer is also factored in). The draft report places a lot of emphasis on the difference in capital

requirements and how this acts as a barrier to competition but doesn't include quantitative

estimates of the impact further "levelling of the playing field" would have on small banks' ability to

offer more competitive loan pricing.

Process and next steps

The draft report is open for submissions until the 18th of April. Following this, the Commission will

hold a conference to discuss the draft report with stakeholders and experts between 13th to 16th

May. The conference format is a combination of open and confidential sessions in which

Commission staff discuss their findings and recommendations and ask specific questions of

interested parties and experts.

A final report is due to be published on 20th August. Under the Act, the Minister of Commerce and

Consumer Affairs is required to respond to the final report within a reasonable timeframe following

its publication.

FSG Directors are establishing a small team to draft a more thorough response which, subject to

further discussion, may become a formal submission on the draft report (including our legal,

financial inclusion and ESAS colleagues). We have also reached out to the Treasury team leading

3 Document Title

Ref #21170199 v1.0

Document 02

From:

Michaela Halse

To:

Richard Downing; Charles Lilly

Subject:

FW: ComCom study - topics from recommendation 1 Monday, 25 March

Date:

2024 5:20:36 pm

Attachments:

image001.png

image002.png

image003.png

image004.png

image005.png

image006.png

Richard/Charles

Further to my initial email, I have noted the paragraphs which set out the specific elements of

the recommendation. I’m not sure if either of you have started putting together a response

on this recommendation, but happy to make a start now that we have a word limit. The IRB

regime recommendations would justify the majority of the focus, with the NBDT

recommendation being able to be dealt with by way of largely referencing the upcoming

consultation. So the question is how much focus (if any) do we want to give to topics not

explicitly covered in the recommendation section?

IRB regime:

Paragraph 10.9 explains that this draft recommendation includes that the RB s

hould

review the role and the operation of the IRB regime for home loans as part of the

upcoming consultation on the Capital Standard later this year to ensure that the same

level of capital is held where the risk is likely to be equivalent.

Paragraph 10.9.1 further states that the RB should

consider whether the same level of

capital should be held where risk is likely is likely to be identical (regardless of whether

the lender is IRB accredited).

Paragraph 10.9.2 then suggests the RB should

consider making it easier to acquire IRB

accreditation.

NBDTs:

Paragraph 10.12 states the RB should

provide further information about its views on the

prudential requirements that NBDTs may have under the DTA including the policy

reasons for proposed changes to the status quo, and to do so with explicit reference to

the purposes and principles of the DTA.

Other:Paragraph 7.56.4 omits reference to

Mutual Capital Instruments and references an out of

date version of BPR120.

Paragraph 7.59.2.2 suggests the

output floor could be set higher (this is 1 of the 3

examples given of whether there should be adjustments to the current capital settings –

the other 2 examples were included in the recommendation section – paras 10.9.1 and

10.9.2)

Paragraph 7.55 referring to the

entrenched competitive advantage due to the capital

settings since 2008

Thanks

Michaela

From:

From: Michaela Halse

Sent: Friday, March 22, 2024 2:21 PM

To: Richard Downing <[email address]>; Charles Lilly

<[email address]>

Subject: ComCom study- topics from recommendation 1

At Richard's request, I've pulled out some themes from the first recommendation as a starter:

IRB regime

• Entrenched competitive advantaQe - there is no recommendation here but an

underlying theme is that we are where we are due to RB regulation (especial y IRB

modelling) from 2008 on. We could ignore, or acknowledge noting this was flagged

during the Capital Review and the changes would go towards redressing some of the

perceived imbalance.

• ModellinQ - in particular, the recommendation suggests certain home loan exposures

shouldn't be modelled.

• IRB accreditation - the recommendation is that this should be easier.

• Output floor - the main body of the report also suggests we could consider raising the

output floor (7.59.2.2) but this doesn't seem to have flowed through to the

recommendation section

• Broader review - the recommendation that we should include a review of the IRB

regime fpo home loans as part of this year's standards consultation feels disingenuous

as it would be impossible to do so from a practical sense. This might need addressing

from an external stakeholder expectation management perspective .

•

There are various small issues that were raised in chapter 7 of the report that do not lead to

any specific comment in the recommendation section. For example:

• Para 7.56.4 - there doesn't seem to be acknowledgement of the introduction of MCls:

they have referred to an out of date version of BPR120 (July 2021) which predates the

October 2023 version which was revised to include MCls.

• The focus is quite heavily on the output floor and the DSIB buffer. There is only a

passing reference to the scalar. Also its quite a nuanced point, and it depends on how

frequently we expect the output floor to be triggered, but the cap review sought to

impact RWA by combining reductions to the exposures that can be modelled with the

scalar and the output floor, and so it feels the report's focus on the output floor is a bit

simplistic.

Thanks

Michaela

Michaela Halse

Senior Analyst, Financial Policy

Reserve Bank of New Zealand - Te Patea Matua

Level 13, Tower Two, 205-209 Queen St, Auckland 1010

PO Box 5240, Victoria St West, Auckland 1142

E

E [email address]

W rbnz.govt.nz

Document 04

Document 04

3/26 2:02 PM Michaela Halse

Hi Charles Lilly, as an FYI I've spoken with Richard this afternoon and agreed to start putting

together a draft intro to our response to recommendation 1, and then to put some bullets under

each individual topic identified as part of that recommendation. I'll circulate that later

today/tomorrow morning as a starter.

3/26 3:13 PM Michaela Halse

Here is the document I referred to in my previous message. It includes a generic intro and then

breaks down the main parts of the recommendation with some bullets. Please let me know what

you would like me to build out further and/or if there are other areas to consider.

Draft recommendation 1 response framework.docx

3/27 1 :53 PM Richard Downing

Hi Michaela. I will have a look at those notes you sent around. Looks like they are on teh right

track. There is nothing else waiting on completion from my perspective, unless there are

particular things Charles wants you to pick up.

3/27 1 :54 PM Michaela Halse

Thanks Richard - I saw your comments on the intro so will deal with those now

3/27 1 :55 PM Richard Downing

.__________ __, For that section I would just keep it general

3/27 2:11 PM Michaela Halse

How general? Avoid mentioning the cap review at all? or just pare it right back to a brief

mention?

3/27 2:12 PM Richard Downing

Referencing cap review is fine, just the detailed principles I would avoid, and focus on the general

idea ie. to meet financial stability objectives

3/27 2:43 PM Michaela Halse

I've revised the intro para - let me know what you think

3/28 9:05 AM Michaela Halse

If you've both had a chance to look at the points in my initial draft, I'll start turning them into

actual prose. If there are other points I should include, or if I have some wrong, please say.

3/28 9:12 AM Richard Downing

Good plan. I have added a few more comments to your document.

3/28 12:36 PM Michaela Halse

I have just about finished drafting a suggested response for of the areas I highlighted. The one

remaining one is the suggestion we should consider whether the same level of capital should

be held where the risks is likely to be identical (irrespective of IRB status). the bullets I noted

included:

•

Conceptual y support removing the ability to model certain exposures where the risk is

likely to be identical.

•

Need to understand scale of any practical issues – ie. can banks isolate relevant exposures.

3/28 12:38 PM Michaela Halse

Neither of you have commented on this - do I take it you agree? Its a fairly big shift from current

practice

3/28 12:39 PM Michaela Halse

Out of Scope

. . otherwise my suggested drafting is all in blue in the

doc linked further above in this chat

[3/28 12:46 PM] Richard Downing

Out of Scope

My

general comment is that we should emphasise that our framework, to the extent it is possible,

aligns credit risk weights to the credit risks that are associated with an exposure. So in principle I

don't see a disagreement with the statement. The "irrespective of IRB status" creates a difficulty

though since it is the extra info from IRB that gives us the confidence that an approved model wil

generate a risk weight aligned with risk. So the use of IRB is central to that assessment, whereas in

the standardised there is less info to give the extra granularity to the risk weight. S once we say

"irrespective of IRB status" it becomes hard to reconcile.

[3/28 12:51 PM] Michaela Halse

I'l put something together - I suspect there is plenty you wil want to change for al of the topics

but hopefully it gives you something to start with. Out of Scope

Out of Scope

4/2 10:28 AM Michaela Halse

11

I

---------------------------------

4/2 10:34 AM Richard Downing

Do you have an updated version of those notes you

---------------

were wor rng on ast wee ? I ave some time to look at that properly today. Otherwise, I am

happy to

wait for Charles for further instruction

4/2 10:49 AM Michaela Halse

The document linked above is in sharepoint so is up to date

4/2 10:50 AM Michaela Halse

let me know if you have issues accessing it

4/2 5:22 PM Charles Lilly

I've been going through the doc this afternoon - thanks both for contributing (especially

Michaela). I've tried to edit down some of the detail and reordered the sections so that the IRB

material is in the same place, I think this helps with the flow. I am also putting in an annex, which

will provide the quantitative example of how little this matters for loan pricing. Mostly this is

taken from the information we sent ComCom via emails which didn't make it into the draft

[4/3 11 :05 AM] Michaela Halse

Just been through and accepted changes to tidy it up. We are currently well over the word limit.

Removing the preface to each section will knock off about 250 words but we are still over 1500.

[4/3 11 :16 AM] Michaela Halse

Richard Downing - are you aware of the data Ian Woolford referred to in relation to costs of

maintaining an IRB framework? If we can access it easily, it would fit nicely with our response to

the IRB accreditation recommendation.

[4/3 11 :43 AM] Richard Downing

Hi Michael. We talked to Commerce Commission about this. I think Charles might have the info

for this.

[4/3 11:44 AM] Charles Lilly

Have just forwarded my notes on this

[4/3 11:58 AM] Michaela Halse

Thanks Charles - Ian referred to specific $ amounts, is that detail we also have? big numbers can

help focus attention...

[4/3 12:11 PM] Charles Lilly

It's not a number I would have any confidence in to put in the submission, it was something we

looked at when we were doing the denominator paper for the Capital Review (around 2018),

was about $8m I think for one of the four banks

[4/3 12:11 PM] Charles Lilly

But that's a very rough number

[4/3 12:11 PM] Michaela Halse

ok - noted

Document 05

These were the notes I made – I would estimate around 10-20 FTE for ongoing IRB

accreditation, plus any systems costs

From: Charles Lilly

Sent: Thursday, January 25, 2024 10:58 AM

To: Kerry Watt <[email address]>; Jess Rowe <[email address]>; Chris Hunt

<[email address]>; David Hargreaves <[email address]>; David Law

<[email address]>; Richard Downing <[email address]>; James Painter

<[email address]>; Angus McGregor <[email address]>; Benjamin

Hammond <[email address]>; Robbie Taylor <[email address]>; Ian

Woolford <[email address]>

Subject: RE: Pre-meet for MBIE meeting

Some notes on the IRB approach

Key messages:

• IRB involves material ongoing operating costs that Standardised banks don’t face.

• Among IRB banks, risk weights don’t vary too much given similar business

strategies/credit risks in the NZ market.

• The output floor and DSIB buffer effectively offset the benefit of lower risk weights

under IRB.

• Any impact of IRB on loan pricing is minor compared to other factors.

More detailed points:

• IRB accreditation is a complex process which entails both setup and ongoing costs

(e.g. developing and validating models, maintaining data systems, additional

reporting requirements, and additional prudential requirements). IRB banks in NZ

would typically have 10-20 local FTE focussed on IRB models and compliance, in

addition to drawing on Group resources.

• It is common for only the largest and most complex banks to be accredited to use IRB

models in most banking markets – e.g. the four largest in NZ, the six largest in

Australia.

• IRB model outcomes can vary between the four IRB banks within different lending

categories, reflecting differences in underlying credit quality as well as modelling

methodologies. The RBNZ must approve any IRB model before a bank is able to use it

in its capital calculation. Our review process involves peer benchmarking and

general y the differences in risk weight outcomes across the four banks are smal ,

which reflects that the four banks’ credit policies and business strategies are fairly

similar to one another in the NZ market.

• Since January 2022 an output floor has applied to IRB banks’ risk-weighted asset

(RWA) calculations which means that RWAs calculated using IRB models can be no

less than 85 percent of the equivalent value that would be calculated using the

Standardised approach used by al other local y incorporated banks. In most

jurisdictions the output floor on the IRB approach is set lower, at 72.5 percent of RWA,

i.e. our framework has a tighter limit on the potential RWA benefit from IRB.

• The four NZ IRB banks are also subject to a domestic-systemically important bank

(DSIB) capital buffer requirement of 2 percent of CET1. While the output floor and

DSIB buffer have distinct objectives and policy rationales, their net effect is that the

four NZ IRB banks face similar overall capital requirements as the other

locally incorporated banks.

• The difference in RWA outcomes between IRB and Standardised banks could in

theory lead to IRB banks being able to offer lending at a lower cost to borrowers due

to a lower weighted-average cost of funding. However, in practice the extent of any

differential is likely to be very small and we do not consider it to be a major

contributor to loan pricing when compared to other factors such as movements in

banks’ debt funding costs and their operating costs.

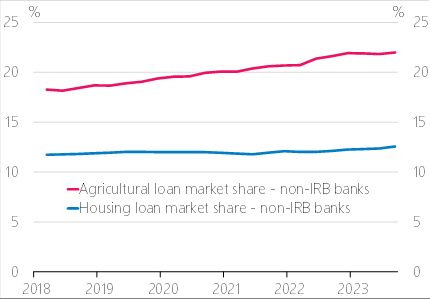

o Rabobank NZ, which uses the Standardised approach, is the third largest

agricultural lender and has steadily grown its market share in recent years (see

figure). Under the Standardised approach, agricultural lending has a 100

percent risk weight, compared to an average of around 70 percent under IRB

(before the output floor).

o In our rules residential mortgages for investors have approximately 20 percent

higher capital requirements than owner-occupier loans at a given loan-to-

value ratio, under both IRB and Standardised approaches. We do not observe

differential pricing for investor mortgages in the market, suggesting the

difference in capital requirements has only a minor impact on banks’ loan

pricing behaviour.

Figure: Lending market share of non-IRB banks

Source: RBNZ dashboard

From: FSC General <[email address]>

Sent: Monday, March 25, 2024 1:35 PM

To: FSC General; FSC General; FSC; FSCAG

Cc: Scott McKinnon; Christian Hawkesby; Adam Richardson; Kate Le Quesne; Kerry Watt; Matt

Haigh; Susan Livengood; Adrian Orr; Kerry Beaumont; Angus McGregor; Karen Silk; Ian Woolford;

Michaela Halse; Simone Robbers; Charles Lilly

Subject: Extra-ordinary combined FSC & FSCAG - Discussion on ComCom Market Study response

When: Monday, 8 April 2024 1:00 pm-2:00 pm (UTC+12:00) Auckland, Wellington.

Where: 8th Floor - Aoraki Room - Teams Meeting Room - External; Auckland Office 13th Floor

Waitematā Room (18 Seats)

________________________________________________________________________________

Microsoft Teams Need help?

Join the meeting now

Meeting ID: 445 919 908 245

Passcode: vtheBA

For organizers: Meeting options | Reset dial-in PIN

________________________________________________________________________________

Document 07

From:

Katy Simpson

To:

Richard Downing; Charles Lilly

Cc:

Jess Rowe; Kerry Watt; Michaela Halse

Subject:

RE: Extra-ordinary combined FSC & FSCAG - Discussion on ComCom Market Study response

Date:

Monday, 8 April 2024 9:26:40 am

Attachments:

comcom table - KS comments on the first row.docx

ComCom narrative KS.docx

Thanks for forwarding this on Richard, and well done Charles for your quick work to bring this

together.

I’ve had a quick look this morning and have some comments – mostly on the first row of the

table. I think we should do a bit more there to reinforce the scale of the work we did as part

of the capital review and that implementation is ongoing. I also think we could add in some

footnotes or links to explain some of the technical things, especially where ComCom got

them wrong in the main report – I think this is our main (only?) opportunity to influence on

these points. Where this is not possible before going to FSOC, I wonder if we just add some

placeholder footnotes?

On the key messages section, I’ve put in some ideas for some opening framing and a few

other thoughts, just in case they’re useful – I know you’re under time pressure and will have

comments from others so feel free to ignore of they don’t fit.

Please could I be added to the call at 1?

Thanks

Katy

From: Richard Downing <[email address]>

Sent: Monday, April 8, 2024 8:23 AM

To: Katy Simpson <[email address]>

Subject: FW: Extra-ordinary combined FSC & FSCAG - Discussion on ComCom Market Study

response

Hi Katy – not sure whether you have seen this. I saw the earlier versions, and Charles and Jess

have completed it.

Kerry has sent me the meeting invite. I intend to dial in at 1pm.

Richard

From: Kerry Watt <[email address]>

Sent: Friday, April 5, 2024 6:04 PM

To: FSC General <[email address]>; FSC <[email address]>; FSCAG

<[email address]>

Cc: Scott McKinnon <[email address]>; Christian Hawkesby

<[email address]>; Adam Richardson <[email address]>; Kate

Le Quesne <[email address]>; Matt Haigh <[email address]>; Susan

Livengood <[email address]>; Adrian Orr <[email address]>; Kerry

Beaumont <[email address]>; Angus McGregor

<[email address]>; Karen Silk <[email address]>; Ian Woolford

<[email address]>; Michaela Halse <[email address]>; Simone Robbers

<[email address]>; Charles Lilly <[email address]>; Olivia Tutty

<[email address]>; John Grey <[email address]>; Anshuman Chakraborty

<[email address]>; Nick McBride <[email address]>; David

Law <[email address]>; David Hargreaves <[email address]>; Jess Rowe

<[email address]>; Paul Conway <[email address]>; Richard Downing

<[email address]>

Subject: RE: Extra-ordinary combined FSC & FSCAG - Discussion on ComCom Market Study

response

Kia Ora

Please find attached some material in advance of Monday’s meeting to consider our

response to the ComCom market Study. Apologies for the short turn around.

The two docs outline our introductory

narrative and a

table that noting specific

recommendations and our proposed response to these. These are based on input from

SME’s from across the RB and we have more detail if anyone wants it – we will need to

include some of this material in the final response, e.g. tables and calculations, but haven’t

included them here.

From Monday’s meeting we want views and ideally agreement on:

1. The

key messages/themes in the narrative (any additions or amendments, points of

emphasis?)

2. Our

proposed responses to the recommendations, these are support, support with

amends, or not support.

We plan to update this material and provide to FSOC on Monday afternoon, in advance of

their meeting on Thursday.

We still have a couple of weeks post these meetings to draft and finalise the actual response

doc in which we will aim to:

Provide a clear narrative up front of how we think about competition as a prudential

regulator and central bank

Be positive and constructive, identifying recommendations we support but be clear on

areas where we disagree with the Commission’s findings

Be short and concise…

A big thanks to Charles in pulling this together, along with Jess and all those who have

contributed to date.

Thanks

Kerry

-----Original Appointment-----

From: FSC General <[email address]>

Sent: Monday, March 25, 2024 1:35 PM

To: FSC General; FSC General; FSC; FSCAG

Cc: Scott McKinnon; Christian Hawkesby; Adam Richardson; Kate Le Quesne; Kerry Watt; Matt

Haigh; Susan Livengood; Adrian Orr; Kerry Beaumont; Angus McGregor; Karen Silk; Ian Woolford;

Michaela Halse; Simone Robbers; Charles Lilly

Subject: Extra-ordinary combined FSC & FSCAG - Discussion on ComCom Market Study response

When: Monday, 8 April 2024 1:00 pm-2:00 pm (UTC+12:00) Auckland, Wellington.

Where: 8th Floor - Aoraki Room - Teams Meeting Room - External; Auckland Office 13th Floor

Waitematā Room (18 Seats)

________________________________________________________________________________

Microsoft Teams Need help?

Join the meeting now

Meeting ID: 445 919 908 245

Passcode: vtheBA

For organizers: Meeting options | Reset dial-in PIN

________________________________________________________________________________

Document 08

[…]

Recommendation 1 (prudential settings)

The committees considered this was a good place to give global context, that its not credible to

‘throw IRB out the window’. Comments also covered maybe giving some context around non-IRB

banks as a footnote, to note where banks currently sit in relation to the output floor (c 90s%), also

to provide more detail about how resource intensive IRB model ing is (though it was noted that we

had previously provided ComCom with this type of information).

[…]

Document 11

From:

Katy Simpson

To:

Richard Downing; Michaela Halse

Subject:

RE: Extra-ordinary combined FSC & FSCAG - Discussion on ComCom Market Study response

Date:

Monday, 15 April 2024 2:12:25 pm

Attachments:

ComCom Market Study Draft Report - RBNZ submission KS.docx

Hi both

I’ve attached my thoughts in the attached. Happy to discuss and combine our comments if

that works?

My only remaining niggle is whether there is anything we can do to pre-empt the ComCom

line that the 2% D-SIB buffer is there for a different reason and therefore shouldn’t count in

the comparison of IRB and standardised approaches? I think they’re saying that DSIBs should

hold more capital (to internalise their possible externality?), but in effect we’re allow them to

hold the same as non-DSIBs because they get to do IRB modelling. Is our line that because

IRB leads to better risk management, we’re comfortable if they end up in a similar place than

they would be without the DSIB buffer under the standardised approach – the IRB modelling

is reducing the risk/externality? I don’t think that really comes across – but maybe that’s fine…

Thanks

Katy

From: Kerry Watt <[email address]>

Sent: Monday, April 15, 2024 9:40 AM

To: FSC <[email address]>; FSCAG <[email address]>

Cc: Scott McKinnon <[email address]>; Christian Hawkesby

<[email address]>; Adam Richardson <[email address]>; Kate

Le Quesne <[email address]>; Matt Haigh <[email address]>; Susan

Livengood <[email address]>; Adrian Orr <[email address]>; Kerry

Beaumont <[email address]>; Angus McGregor

<[email address]>; Karen Silk <[email address]>; Ian Woolford

<[email address]>; Michaela Halse <[email address]>; Simone Robbers

<[email address]>; Charles Lilly <[email address]>; Anshuman

Chakraborty <[email address]>; Nick McBride

<[email address]>; David Law <[email address]>; David Hargreaves

<[email address]>; Jess Rowe <[email address]>; Paul Conway

<[email address]>; Richard Downing <[email address]>; Karen Wong

<[email address]>; Wendy Goldswain <[email address]>; Katy

Simpson <[email address]>

Subject: Extra-ordinary combined FSC & FSCAG - Discussion on ComCom Market Study response

Kia Ora

Please find attached our draft response to the ComCom’s draft report. Can you (or teams) please

review for factual accuracy and get comments back to Charles and I by CoP Tuesday 16 April.

The response reflects feedback from FSC and FOSC. The key piece of feedback from FSOC was to

add more spine to the response, i.e. being clearer and more forceful where we disagreed. We

think the attached achieves that balance between constructive and forceful.

Given the response is due on Thursday, and the clear steer we have from FSC and FSOC, at this

stage we are not after sweeping comments but rather specific comments on tone, positioning

and facts.

Thanks in advance

Kerry and Charles