UNCLASSIFIED

All redactions on this page s 9(2)(g)(i)

CBDC FORUM USE ONLY

Need to consider whether monetary sovereignty is a key element to justify a CBDC. A CBDC is difficult

to explain simply to people. TD introduced slides that contain elements of a narrative to help with this.

Some discussion amongst members whether monetary sovereignty is the right argument – whether

trust in central bank money & value anchor are key or not. Alternative attributes around offline may be

stronger arguments.

RBNZ is focused on the wellbeing and prosperity of NZers. Money systems are changing, and there are

new forms of money. Public money has a key role, we want to protect trust in the NZD and need to

think about public money to meet our future needs.

Privacy will be a key element in the narrative, as is the need for a social license that enables people to

freely participate in society. Also, the transferability question – can it be transacted freely?

Digital currencies are coming – an opportunity exists to set the rules / arrangements to prevent CBDC

from being misused by the government or people. If there is a risk that the NZD is substituted by the

AUD, then need to consider what elements of CBDC design might mitigate those risks. Need to be

clear on what focusing on – inclusion vs. innovation vs. sovereignty. The former two can be served

without a CBDC. CBDC may only be a small part of a much larger world of digital assets.

s 9(2)(g)(i)asked whether the important question is whether it is necessary for NZ to have its own digital

currency, or just adopt others?s pointed out that this answer had to reflect the needs of NZ people.

9(2)

RT reminded that RBNZ is just in an exploratory phase and are also trying to contemplate a future

world that is vastly different to what we are facing right now. What are the drivers and risk for that

future environment, and what needs to be thought about now as a result?

TD invited Forum members to go away and think about what the narrative for how and why NZ might

need a CBDC looks like for them, and to send that through.

3.

Inclusion workshop – Quinn Pooley

QP presented the work which explored inclusion so far. This moves away from people-based

definitions of inclusion to circumstance based approaches.

s 9(2)(g)(i)

noted the need to legislate to protect cash to give people genuine choice. RT acknowledged this is

being considered as part of the separate cash policy work, and no existing legislation exists today. s 9(2)(g)(i)

said that that if the RBNZ wants to be genuine here it needs to legislate and take some action.

QP covered what meaningful choice and confidence to exercise choice means in the NZ context and

where the inclusion needs are in NZ now, relative to these criteria.

s 9(2)(g)(i)

questioned whether the statistics provided were inclusion issues, or financial

wellbeing issues?

-

Can and should a CBDC (and its ecosystem) be responsible for or solve for these

problems?

s 9(2)(g)(i)

noted that a CBDC should not make things any more difficult for people, and if it

does, the design should be reconsidered.

s 9(2)(g)(i)

noted that it is unrealistic a CBDC would be delivered right the first time for

everyone.

Members commented on ‘offline CBDC functionality’ and if an offline CBDC was not available, would it

still be a meaningful choice? Maybe reframing that question as “What happens with CBDC when it

goes offline?” could be more helpful. It will not be possible to deliver everything to everyone upfront.

Some member notes on CBDC as ‘meaningful choice’ include:

2

CBDC Forum 6 Summary

UNCLASSIFIED

Ref #20010629 v1.0

CBDC FORUM USE ONLY

UNCLASSIFIED

All redactions on this page s 9(2)(g)(i)

CBDC FORUM USE ONLY

s 9(2)(g)(i)

noted that a roadmap would help prioritise what is most important first.

-

CBDC should not disrupt cash, and not take choice away. Cash needs to be mandated

s 9(2)(g)(i)

-

CBDC needs to be widely accepted and have significant adoption to be a form of

meaningful choice.

QP noted that a CBDC could be an effective onramp to digital money and payments if it was part of

the current financial ecosystem. QP also discussed the ‘people-led’ requirements for community-driven

access (i.e., Māori and Pacifica-led). Asked the group what the other requirements might be for this?

-

RT noted that the requirements highlighted should be considered ‘opportunities’

instead.

s 9(2)(g)(i)

noted that it would be impossible to meet

all consumer needs.

s 9(2)(g)(i)

noted the many other cultures and ethnicities in Aotearoa, and how many of them

have strong links to where they came from and have regular economic transactions

with their families and friends, so the international perspectives are important here as

well. s added that this leads on to the importance of cross border transactions.

9(2

Going forward, is there an opportunity to share survey data sets amongst members of the Forum s 9(2)(g)(i)

s 9(2)(g)(ii) noted that there are plenty of generic market research which potentially could be shared to further

frame and think about these areas.

4.

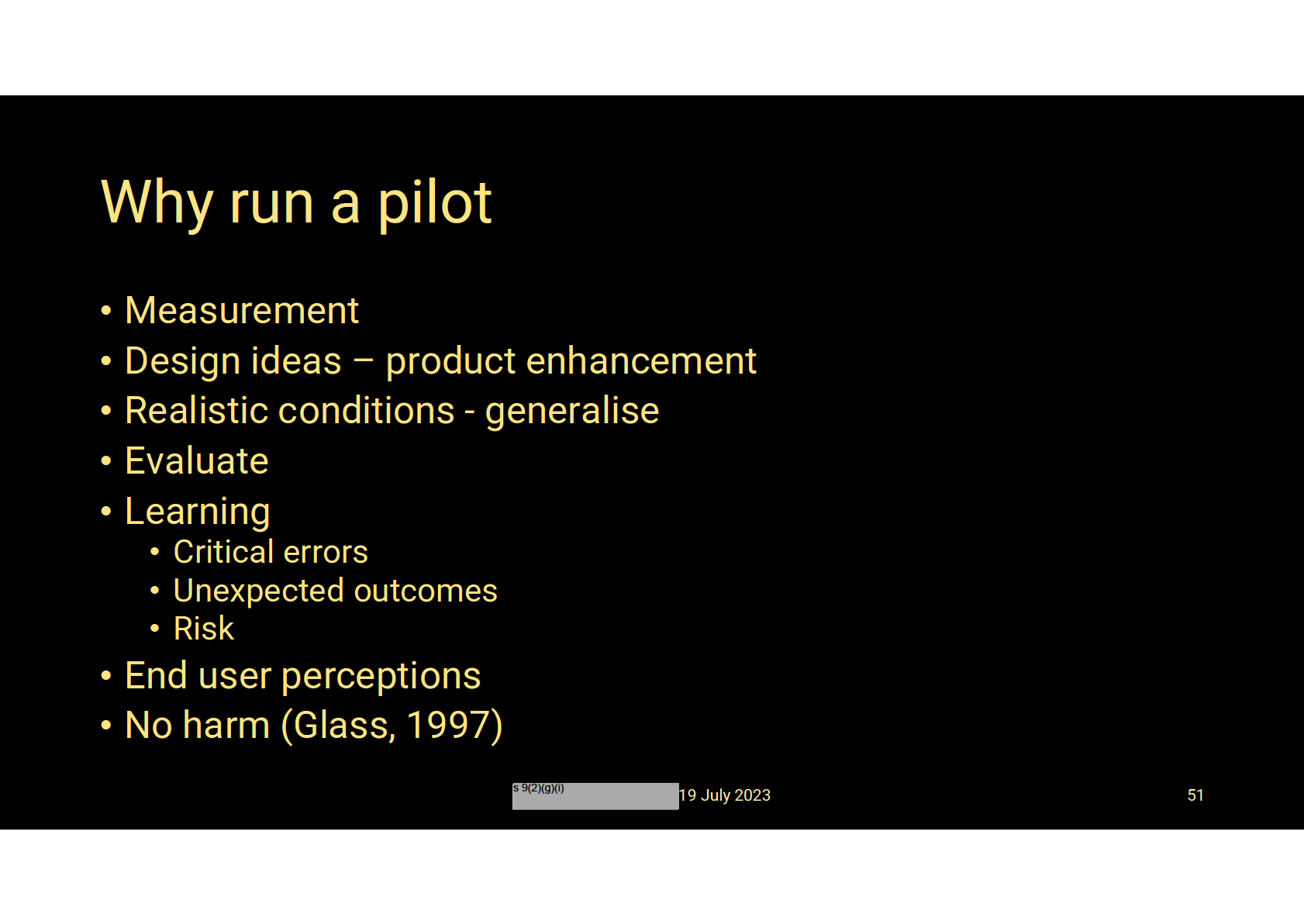

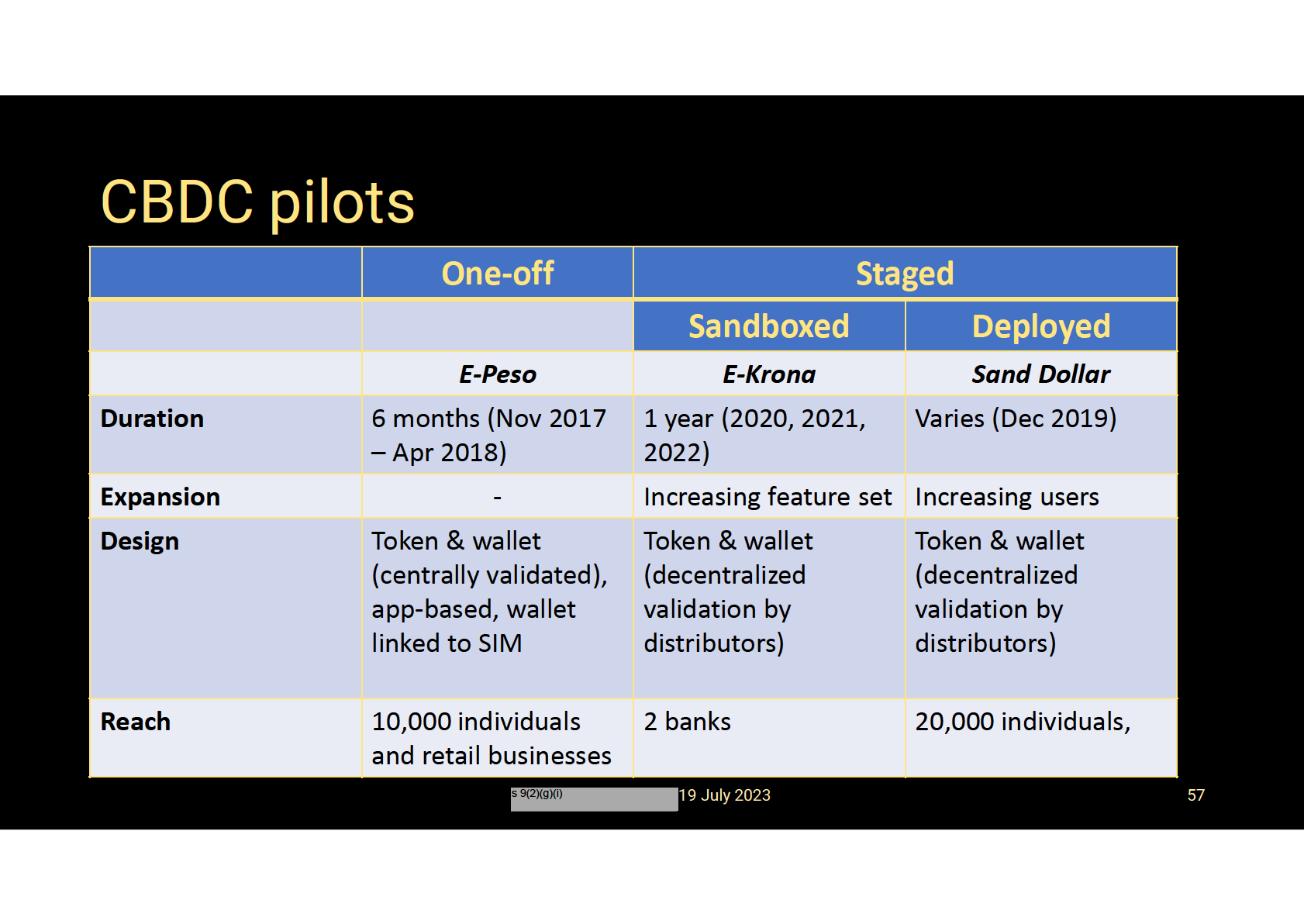

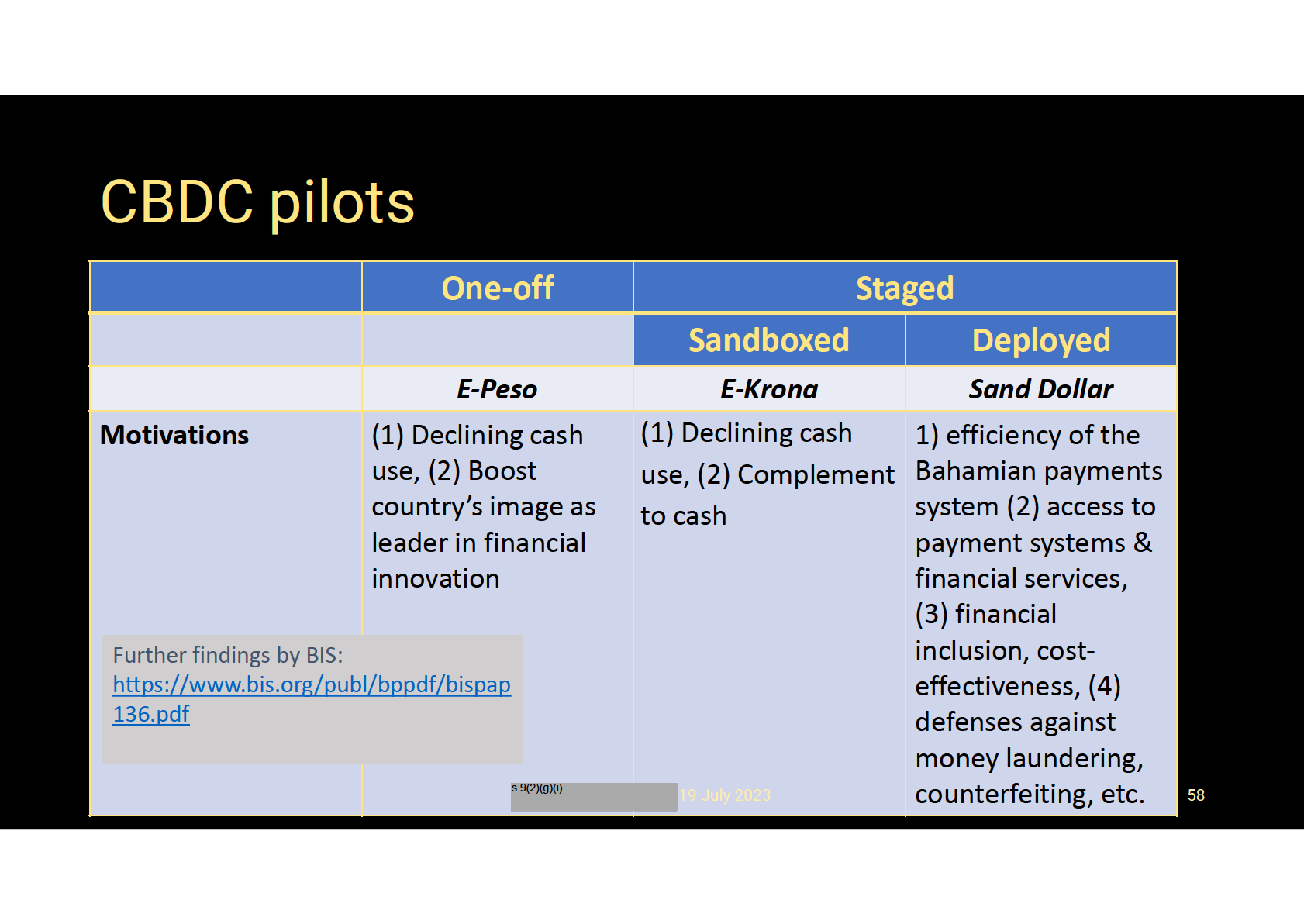

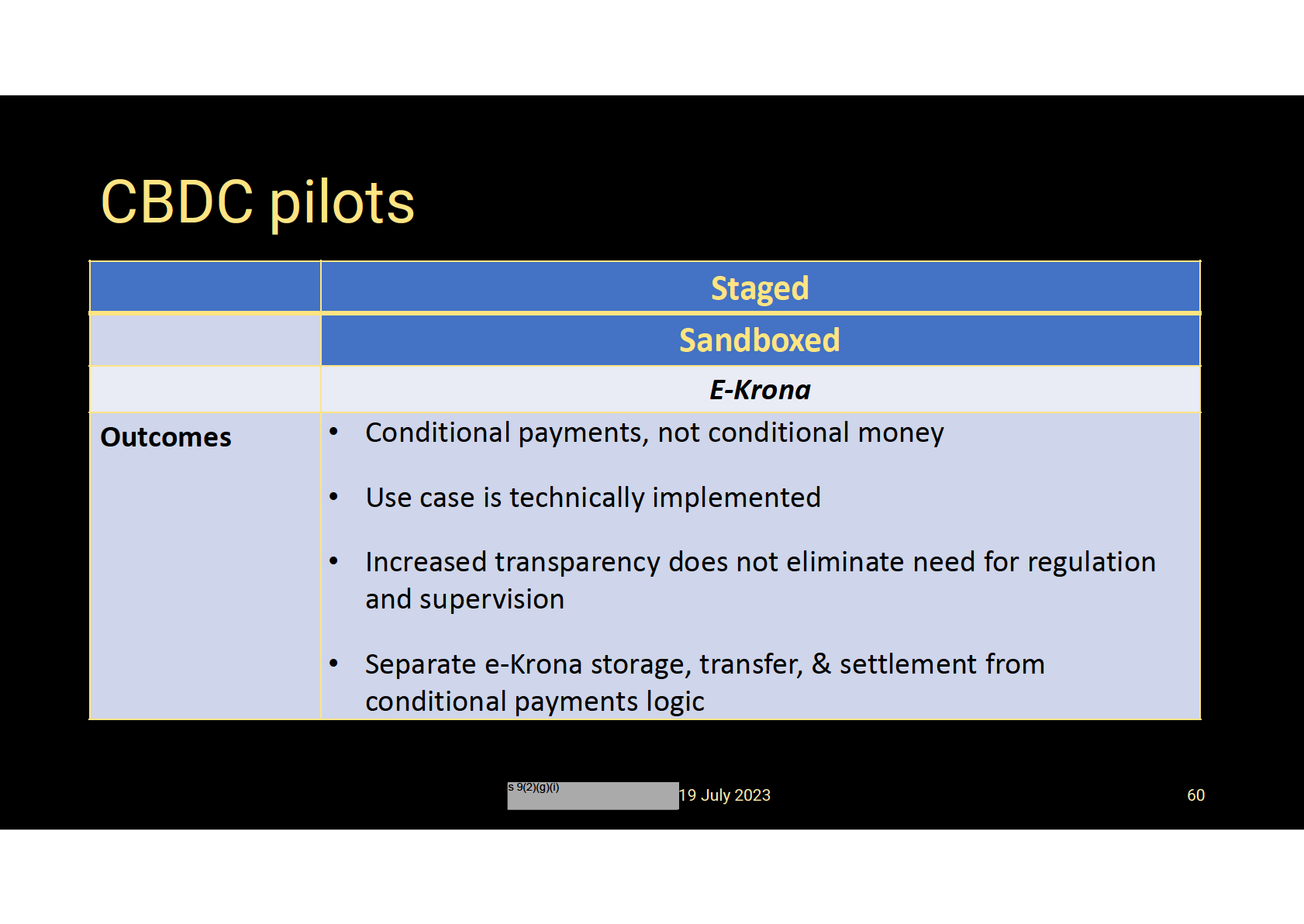

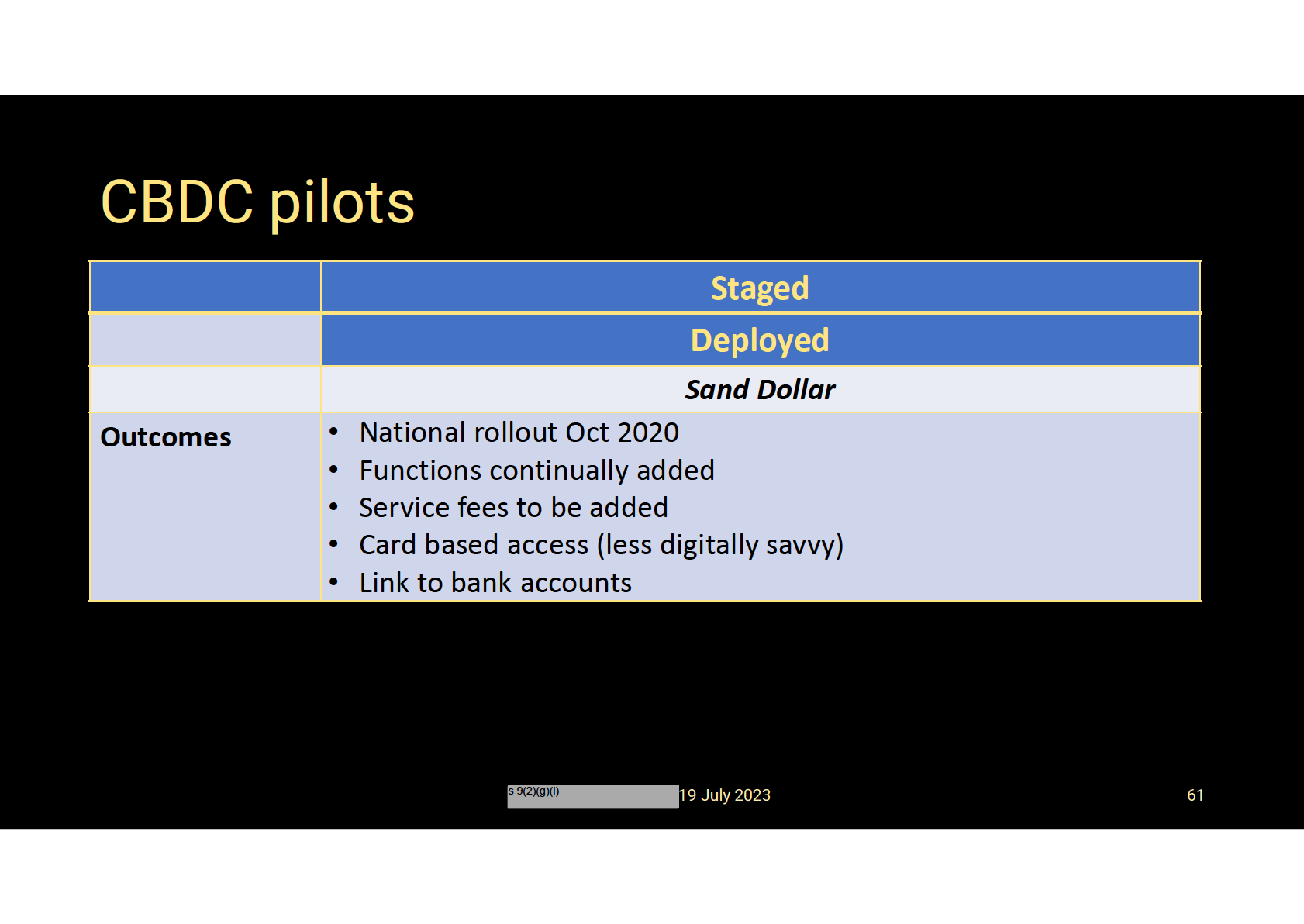

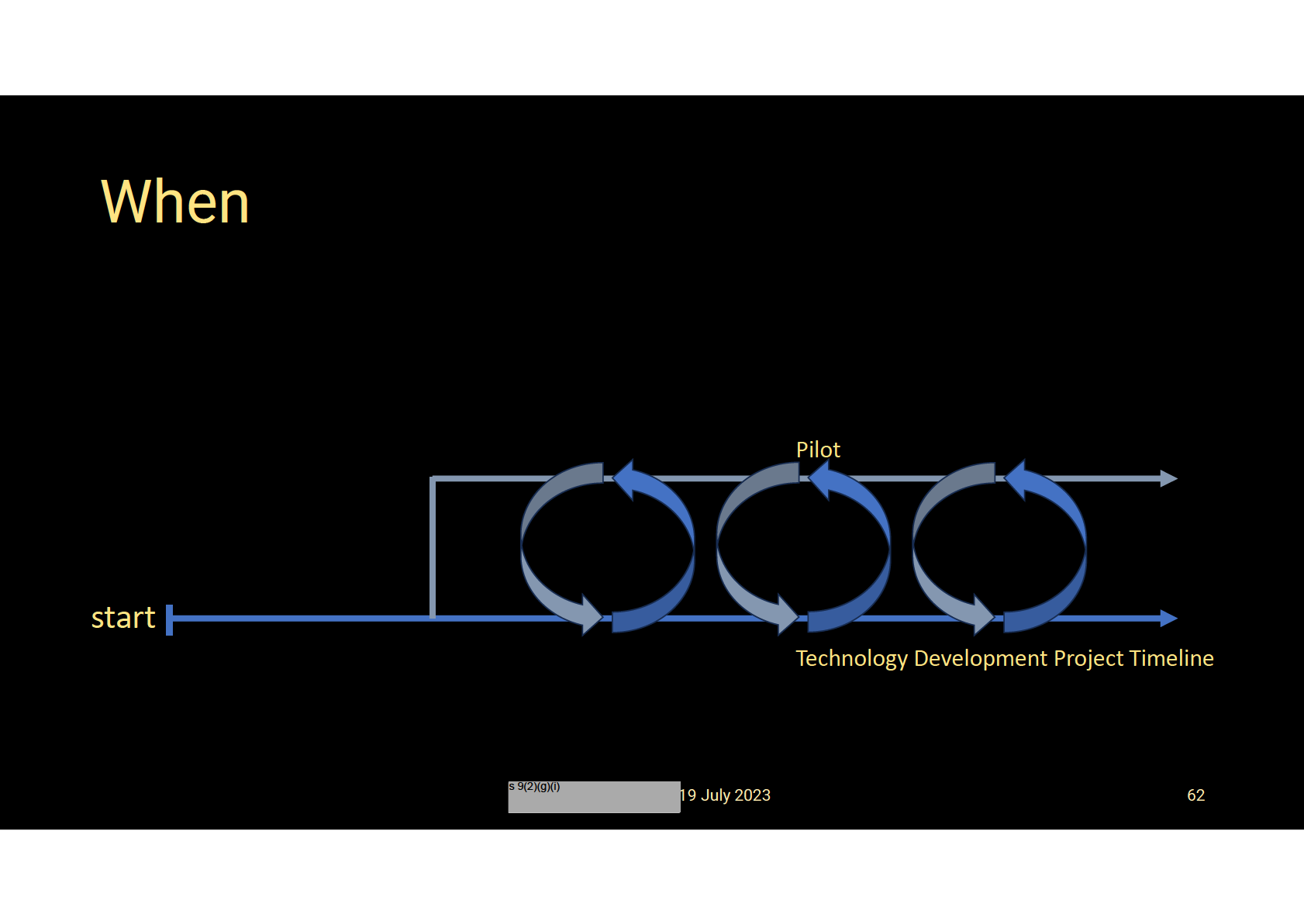

Member-led session ‘What about a pilot?’ –s 9(2)(g)(i)

s 9(2)(g)(i)

presenteds

slides describing what a pilot is, why it may be helpful, and when one could be run. It

could help refin

9(2) e the scope of a CBDC programme, and more than one pilot could be run over time

focusing on different things using a ‘Double Diamond’ Discover/Define/Develop/Deliver process. Pilots

can be an expensive thing to do, and there could be more lightweight ways to test specific things (like

interface choices... where to place a button).

s 9(2)(g)(i)

commented that

how to do something for CBDC (test technology for example) may be testable,

but harder to test whether a CBDC will deliver monetary sovereigntys 9(2) noted that choosing what to

pilot will be important, and although that may be difficult it could be he

(g)(i)lpful identifying the usage

demand level and the desired features. s considered that NZ did not need to be unique or world

beating in this space, so we should learn fr

9(2) om overseas and embrace that. s noted that the RBA pilot

approach (14 pilot cases) was end-to-end, rather than focusing on just the tra

9(2) nsactions.

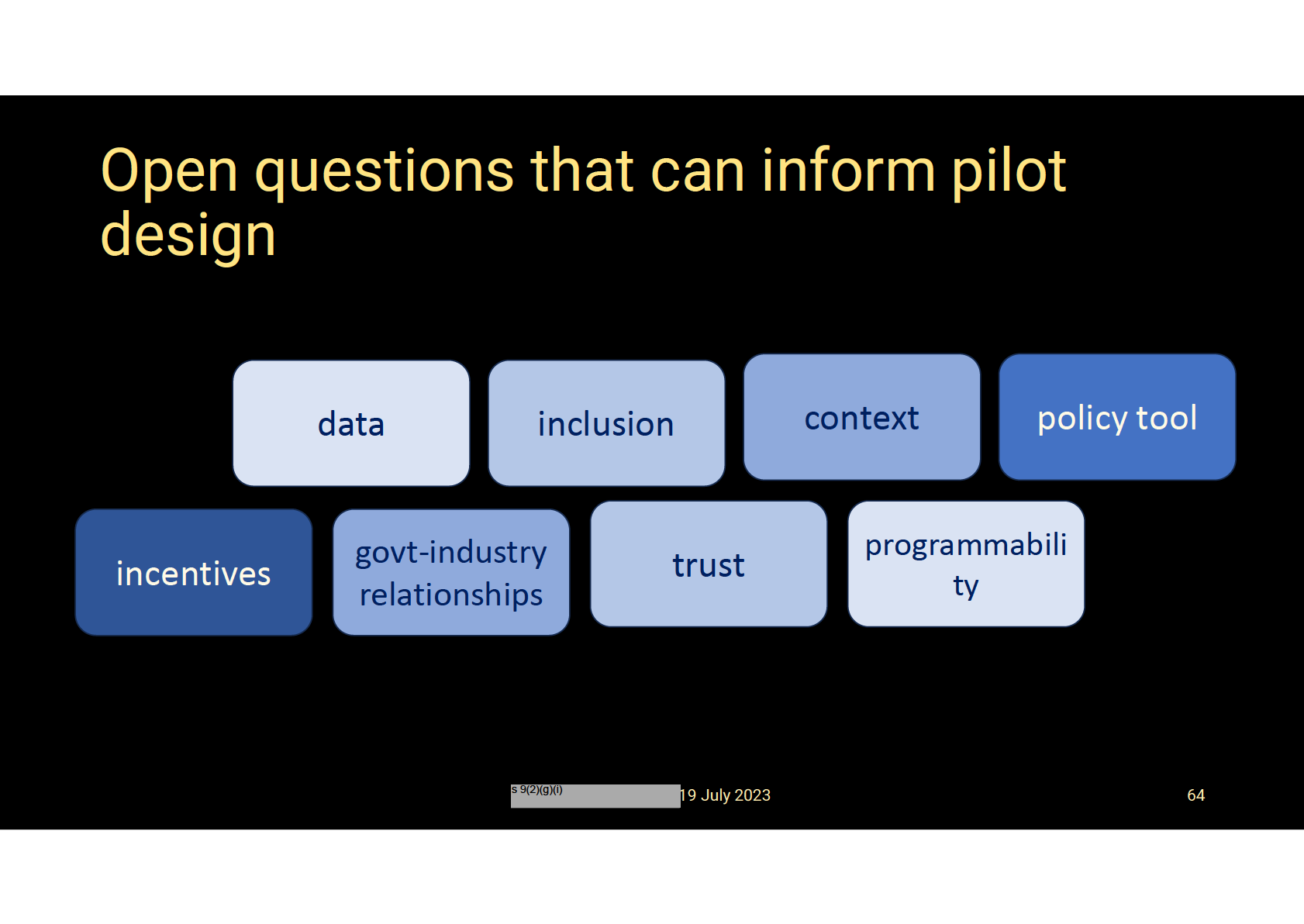

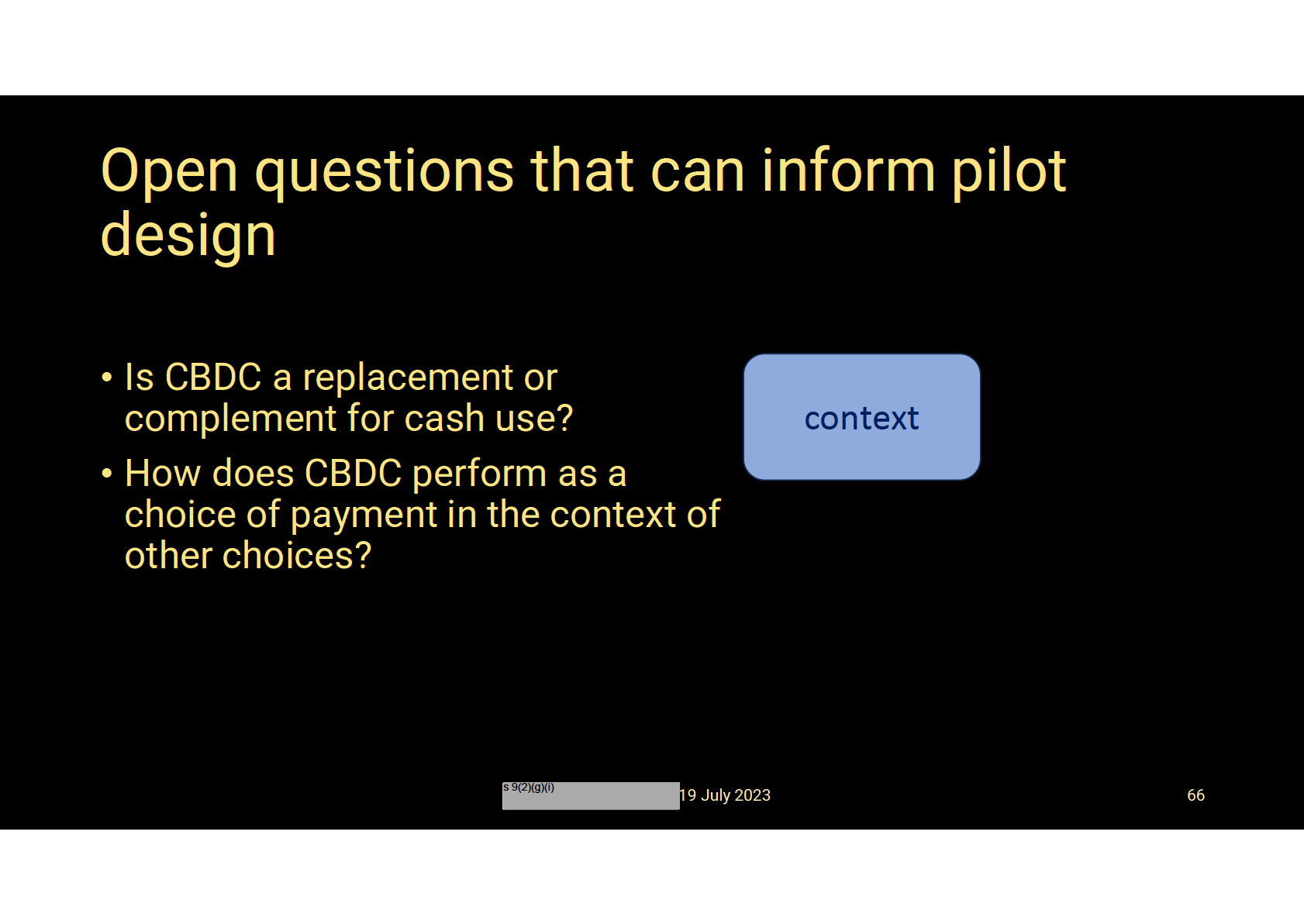

s 9(2)(g)(i) noted that there are still a lot of unanswered questions from pilots: is CBDC a replacement or

complement for cash use? How does CBDC perform as a choice of payment in the context of other

choices? Does it promote financial inclusion?

s 9(2)(g)(i) presented a roadmap to a pilot: decide when; focus on open questions that are yet to be answered;

decide on how and what to measure; agree success criteria; risk analysis.

Some member feedback below:

s 9(2)(g)(i)

– important to frame the strategic context and outcomes, where are the big risks, that

CBDC can mitigate. API Council could help support innovation or pilots.

s 9(2)(g)(i)

- pilots are not the only way to learn. A war game type scenario could be considered, e.g.,

what would it look like to lose control of money supply? Important to clarify what questions

you are trying to answer first.

s 9(2)(g)(i)

- could start with AU use cases (and other jurisdictions like UK and Canada) and just see

what would need to change for NZ? Partnering with RBA pilot companies?

3

CBDC Forum 6 Summary

UNCLASSIFIED

Ref #20010629 v1.0

CBDC FORUM USE ONLY

UNCLASSIFIED

CBDC FORUM USE ONLY

s 9(2)(g)(i)

– rather than focusing on proving / refuting specific hypothesis that we come across

today, we should explore the unknown things that we have not thought of, the future

innovations that might come along.

s 9(2)(g)(i)

- could test what needs exists for a CBDC to be successful, and to focus in on those needs.

•

MS – what about RBNZ issuing a CBDC and like the RBA/DFCRC, inviting others to pilot it in

some agreed way?

s 9(2)(g)(i)

- suggested starting with Cash System Review objectives and going where would a CBDC

be a feasible alternative that delivers on the CBDC narrative. As a starting point, to stand up

the pilot(s) use existing systems that are trusted. The payment ecosystem is becoming

complex and this needs to be simplified - the goal of CBDC should be to help achieve this.

5.

Open discussion

RT invited for any final remarks and comments:

s 9(2)(g)(i)

– is there any way to test the monetary sovereignty hypothesis? Need to check that this is

a real risk, and if so, what the cost is to NZ of losing this. The business case needs to land on a

problem statement, which is not 100% clear just now.

s 9(2)(g)(i)

– the narrative cannot be couched around monetary sovereignty and the value anchor as

people won't understand. Drafting a 3-year plan with some milestones would help identify

what inputs you need from the Forum. Identifying specific items for the Forum to help in order

to advance the consultation or business case would be helpful – e.g., draft consultation

questions or business case to facilitate a discussion/help answer the questions we may have.

s 9(2)(g)(i)

– if a table of contents for the business case is drafted, then the Forum could help identify

areas they could contribute.

s 9(2)(g)(i)

– need to refine the value anchor story because CBDC is not the solution.

• RT – there is a difference between monetary sovereignty and value anchor, which are often

conflated.

s 9(2)(g)(i)

– need to be able to explain CBDC to friends and family at a BBQ. Clarity on elements why

CBDC needed to protect sovereignty; what is NZ’s position given the currency is not a global

one? What might the infrastructure required be, and how far can we go on that today?

Structure, conduct and performance of payments – start think about what might change, by

who, and recognise the wider ecosystem impacts. Suggested that a scenario analysis might

help tease out what we need to address the needs – which might be a stablecoin instead.

•

TD – asked the Forum to prepare a written position statement on CBDC. Need three things in

next session: 1. scenario testing – including risks and uncertainties into the future; 2. need

strategic case for CBDC; 3. need to convert into a “BBQ narrative”.

6.

Wrap up

RT thanked everyone for attending today and reminded everyone to fill out the survey/give feedback

by end of the week.

4

CBDC Forum 6 Summary

UNCLASSIFIED

Ref #20010629 v1.0

CBDC FORUM USE ONLY

UNCLASSIFIED

Contents

Terms of Reference ____________________________________________________________________________ 2

Purpose and scope

2

Membership

2

Responsibilities and activities

3

Meeting frequency and duration

3

Chair and secretariat

4

Conflicts, competition law and information sharing

4

Relationship Charter

4

1 CBDC Forum: Terms of Reference

UNCLASSIFIED

Ref #20821011 v1.2

UNCLASSIFIED

Terms of Reference

Purpose and scope

The purpose of the CBDC Forum will be to provide an opportunity to engage key stakeholders

and gather input on various user needs, system governance, technology and operational aspects

of a CBDC. The Forum will offer a structured mechanism for obtaining expert views and advice on

a potential New Zealand CBDC.

The Reserve Bank has not yet made a decision on whether to introduce a CBDC. The CBDC Forum

will not focus on whether to introduce a CBDC, rather its focus will be on how to design and

implement one effectively. As such, the CBDC Forum will help us through Phase 2 of our CBDC

work programme, which aims to progress work on the design and testing of a possible CBDC.

CBDC Forum input is expected on issues, such as:

The tasks the CBDC system needs to perform (CBDC use cases);

The functional needs of CBDC users;

The various key roles in the CBDC system;

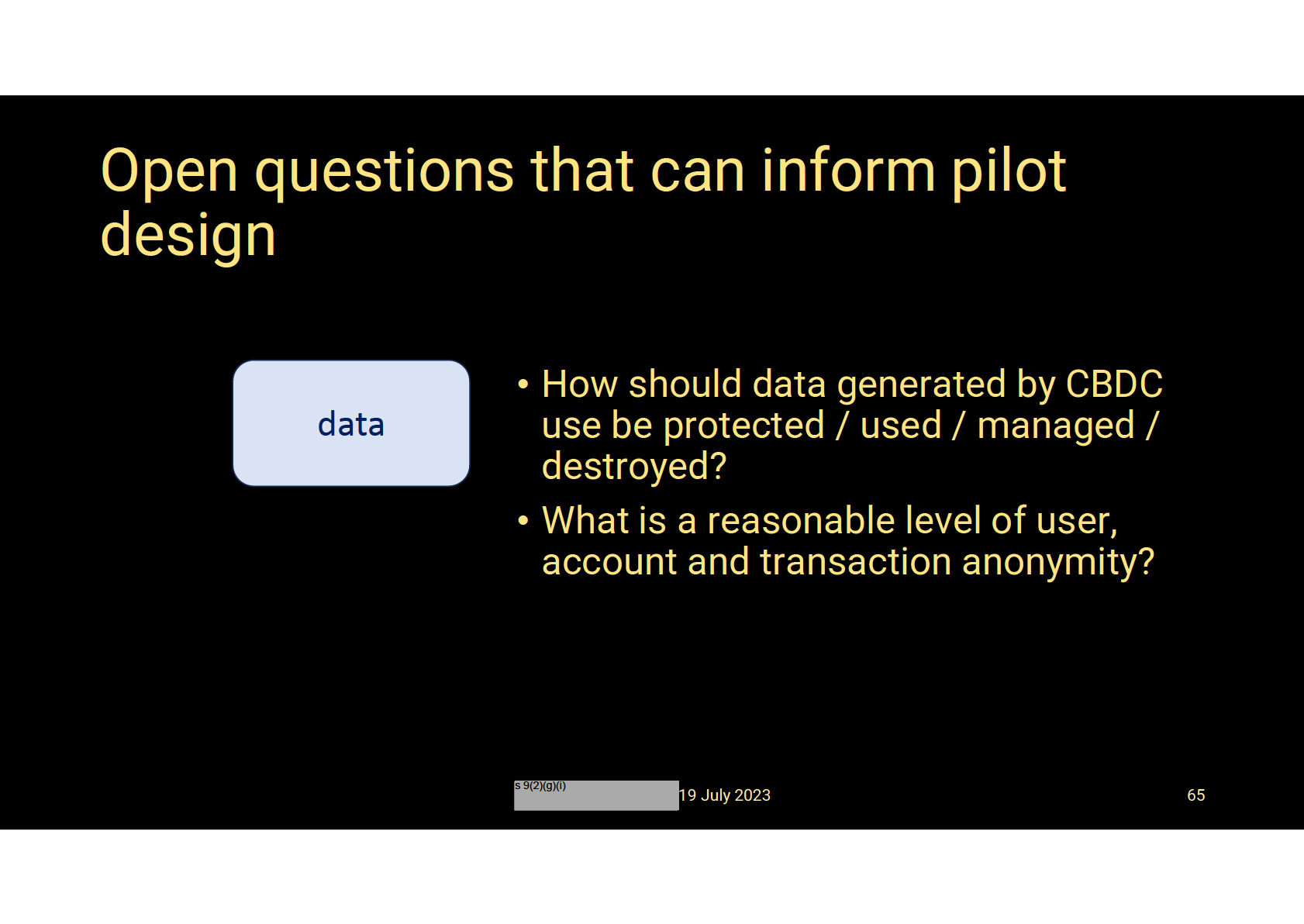

Data, privacy and anonymity considerations;

Digital and financial inclusion issues; and

Other practical challenges associated with designing, implementing and operating a CBDC.

The CBDC Forum will also help us to connect with other key stakeholders or forums to explore

policy and design issues in detail.

The CBDC Forum will provide input that helps us to design a CBDC that best meets the needs of

New Zealanders but will not have any decision-making responsibilities. For example, issues

identified and views raised by the Forum will feed into our wider CBDC work programme and,

where appropriate, be considered and discussed with our engagement partners and influencers

and raised up to decision-makers.

Complex or thematic issues identified by the Forum – like privacy and financial inclusion concerns

– could be explored further in regulatory, policy or technology deep dives. We could also run

public forums or deliberative workshops on these issues. The Forum will not be a substitute for

running public consultations or publishing informational releases on our CBDC work programme;

these will be undertaken as needed.

The CBDC Forum purpose, scope and membership will be received annually by the Reserve Bank.

This will help to ensure that the Forum remains fit for purpose as the work programme on CBDC

progresses and evolves through the various stages over time.

Membership

Participating in the CBDC Forum is at the invitation of the Reserve Bank, following an expressions

of interest process. Members will be drawn from the relevant range of CBDC stakeholders from

banks, payment service providers, fintech organisations, retailers, businesses, consumers, civil

society organisations and academia.

2 CBDC Forum: Terms of Reference

UNCLASSIFIED

Ref #20821011 v1.2

UNCLASSIFIED

The CBDC Forum will comprise a diverse set of knowledgeable participants with relevant

background and experience. Members will either be senior figures within their industry or

institutions or have skills and experience useful to the issues the CBDC Forum will be engaging on.

Members will be expected to commit to taking a constructive and open-minded approach to a

CBDC. By joining the Forum, members will need to commit to exploring how a CBDC could be

successfully deployed in New Zealand. To help facilitate this, membership will be on an individual

basis (rather than an organisational basis). This means that a member that permanently steps

down from the Forum, or is unable to attend a particular meeting, will not be able to automatical y

pass on their seat to another person within their institution. However, in the case of a member

being unable to attend a scheduled meeting, they will have the opportunity to provide written

feedback on the papers or issues being discussed ahead of the meeting.

To ensure that there is representation from experts in the topics being discussed at any particular

CBDC Forum meeting, external stakeholders may be invited to attend by the Chair, in consultation

with the Forum.

Responsibilities and activities

The Reserve Bank will engage with members of the CBDC Forum on material issues related to the

CBDC work programme, including user needs, system governance, technology, and operational

aspects of a CBDC. To promote open discussion and to al ow members to provide frank and

robust comments, meetings will be conducted under the Chatham House rule.

Members of the CBDC Forum will be expected to prepare for and participate in CBDC Forum

meetings, as well as share information, perspectives and opinions on the discussed topics that

reflect a broad perspective (rather than only representing the interests of their individual

organisations).

Members will also be able to provide input into the agenda of future meetings and request that

specific topics are included for discussion. These requests should be communicated to the

Secretariat in advance of the meeting to which the request relates. The Chair of the Forum will

ultimately decide on what is included in the final agenda. Members may also be asked to host a

session to present and lead a discussion on a topic relevant to the Forum. This provides an

opportunity for members to socialise a topic of interest to them.

The Secretariat will circulate minutes of the discussions held at the CBDC Forum with members

after the meeting. Members will be able to provide feedback and suggest changes to the contents

of the minutes to the Secretariat.

Meeting frequency and duration

The CBDC Forum will meet approximately five to six times a year. The Forum could vary the

meeting frequency where circumstances warrant it, at the discretion of the Chair and with

consultation of members. CBDC Forum meetings will be held in-person with the option to attend

virtually via Microsoft Teams. It is anticipated that meetings will predominantly be in person but

there may be occasions where a virtual meeting is held.

To ensure sufficient time for substantive discussions, scheduled in-person meetings will be for

approximately half a day. Virtual meetings will likely be for a shorter duration.

For more technical aspects of the discussion, these may be conducted through a working group

where interested members meet if the Forum identifies complex or thematic issues to explore in

3 CBDC Forum: Terms of Reference

UNCLASSIFIED

Ref #20821011 v1.2

UNCLASSIFIED

further depth. Such working groups will then report back to the wider group at the main CBDC

Forum meetings.

Chair and secretariat

The CBDC Forum will be chaired by the Manager of Money and Cash Policy at the Reserve Bank of

New Zealand. The Reserve Bank will also provide the Secretariat.

The Chair will be responsible for:

Setting the strategy for the CBDC Forum and its forward agenda;

Moderating the discussions in meetings; and

Inviting any external stakeholders to attend meetings, where appropriate.

The Secretariat will be responsible for:

Circulating minutes of the meetings with members;

Reminding members of meeting practice and hygiene, such as competition guidelines;

Coordinating responses to any public inquiries in relation to the CBDC Forum, including

publication of materials discussed at the CBDC Forum;

Preparing the agenda and materials for the meetings; and

Coordinating any outreach to other external stakeholders, if required.

Conflicts, competition law and information sharing

Members will be responsible for disclosing any conflicts of interest that may arise from their

involvement with the CBDC Forum. As part of mitigating conflicts of interest, members will be

expected to withdraw from the Forum before entering into any part of a procurement process with

the Reserve Bank related to the CBDC work programme (e.g., proof of concept).

Members should refrain from using the Forum as an opportunity to promote products or services

to the Reserve Bank or other members, and from publicising their involvement with the Forum for

the purposes of marketing in other jurisdictions.

Members must ensure that they comply with their obligations under any applicable competition

law. If members are unclear about their obligations, they should seek further guidance from their

respective organisations.

Members must also ensure that any information that they share with the Forum is not protected

by their organisation. In cases where a member is unsure of the level of protection of the

information, then it is the member’s responsibility to not share such information.

Relationship Charter

The Reserve Bank aspires to build and maintain the best ‘regulator/regulated’ supervisory

relationships possible, with all its regulated entities. As part of this, the Relationship Charter was

4 CBDC Forum: Terms of Reference

UNCLASSIFIED

Ref #20821011 v1.2

UNCLASSIFIED

established in 2018 for working effectively with our regulated entities and represents a mutual

undertaking of how the parties will work together to achieve this aspiration.1

The Reserve Bank is committed to upholding the values of the Relationship Charter when we

engage with members of the CBDC Forum – including with non-regulated entities. These include a

commitment that our behaviours will be honest, diligent, achievement focused, open-minded and

professional; and that our communication will be clear, consistent, targeted and timely. This will

help ensure that the CBDC Forum’s work is underpinned by the principle of ‘te hunga tiaki’ – the

combined stewardship of an efficient system for the benefit of all.

We expect members of the CBDC Forum to also be willing to commit to upholding the principles

of the Relationship Charter.

____________

1 See here for further details on the Reserve Bank s Relationship Charter https //www.rbnz.govt.nz/regulation-and-supervision/statements-of-approaches/statement-of-relationship-

management-approach

5 CBDC Forum: Terms of Reference

UNCLASSIFIED

Ref #20821011 v1.2