What is the goals?

• Understanding the nominated funds are acceptable investment.

• The investment period starts from AIP date, by email/letter

• Saving time after pre- stage and waiting for transfer and investment

Investment period begins

BJ7.25 When the investment period begins

• If the investment already meets the investment requirements, the required investment period

begins on the date of the letter of advising approval in principle.

• If the investment is made after approval in principle, the required investment period wil begin on

the date the investment requirements are met.

• The date the investment period begins is specified in the letter to the successful principal applicant

that advises the conditions on their resident visa (see BJ8.10).

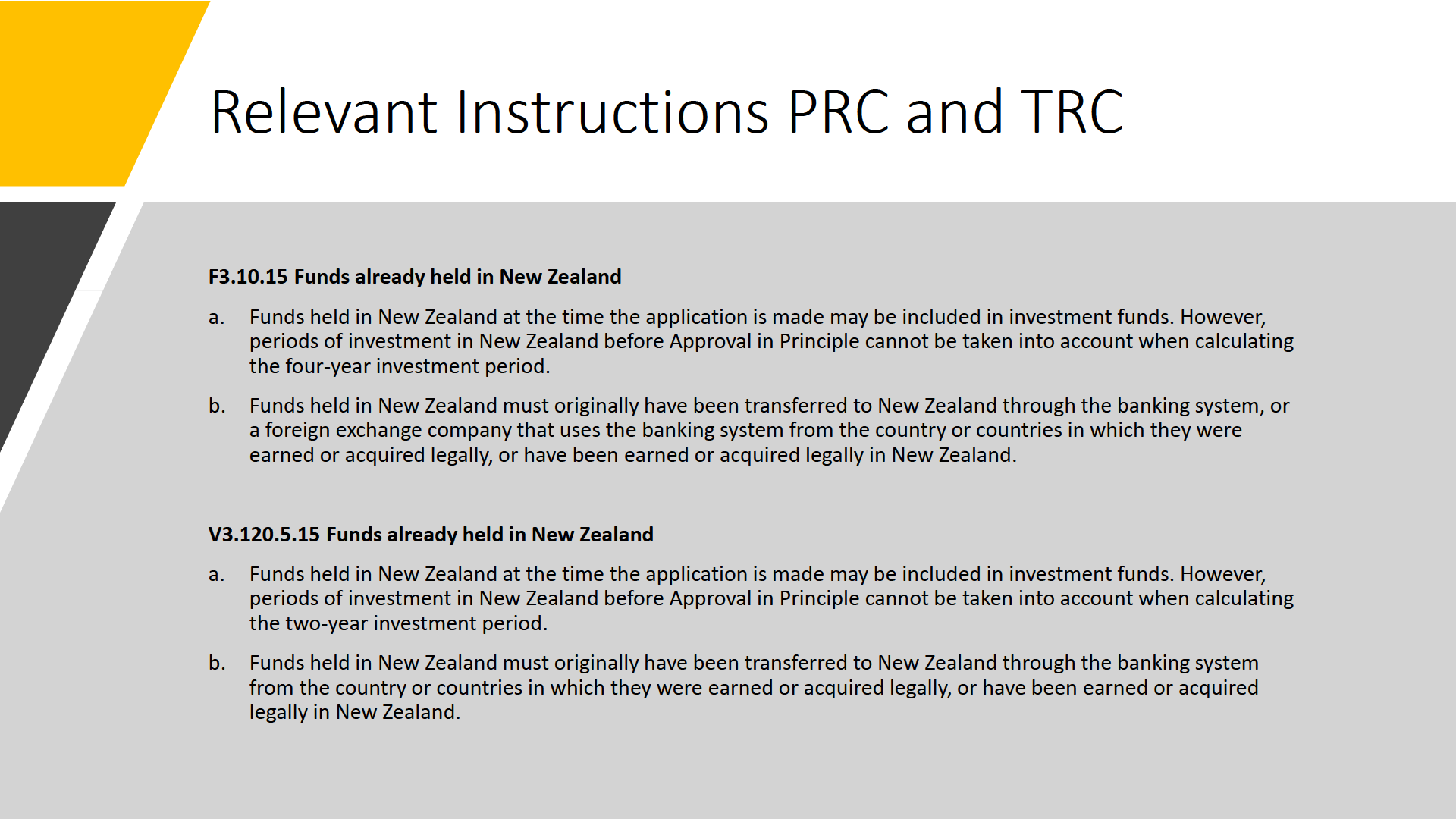

F3.25.25 When the investment period begins

• If the investment already meets the investment requirements, the required investment period

begins on the date of the letter advising approval in principle.

• If the investment is made after approval in principle, the required investment period wil begin on

the date the investment requirements are met.

• The date the investment period begins is specified in the letter to the successful principal applicant

that advises of the conditions on their resident visa (see F3.30.10).

Acceptable investment in Inv 1

BJ3.10.25 Definition of 'acceptable investment’

a. An acceptable investment means an investment that:

i. is capable of a commercial return under normal circumstances; and

ii. is not for the personal use of the applicant(s) (see BJ3.10.30); and

iii. is invested in New Zealand in New Zealand currency; and

iv. is invested in lawful enterprises or managed funds (see BJ3.10.35) that comply with al relevant laws in force in New

Zealand; and

v. has the potential to contribute to New Zealand's economy; and

vi. invested in either one or more of the following:

o bonds issued by the New Zealand government or local authorities; or

o bonds issued by New Zealand firms traded on the New Zealand Debt Securities Market (NZDX); or

o bonds issued by New Zealand firms with at least a BBB- or equivalent rating from international y recognised

credit rating agencies (for example, Standard and Poor's); or

o equity in New Zealand firms (public or private including managed funds and venture capital funds); or

o bonds issued by New Zealand registered banks; or

o equities in New Zealand registered banks; or

o residential property development(s) (see BJ3.10.40); or

o commercial property (see BJ3.15.5); or

o bonds in finance companies (see BJ3.10 (d)); or

o eligible New Zealand venture capital funds (see BJ3.10.45); or

o philanthropic investment (see BJ3.15.10); or

o ‘Angel funds or networks’ investments.

Note: New Zealand registered banks are defined by the New Zealand Reserve Bank Act 1989.

Acceptable investment in Inv 2

BJ5.50 Definition of ‘acceptable investment’

a. An acceptable investment means an investment that:

i. is capable of a commercial return under normal circumstances; and

ii. is not for the personal use of the applicant(s) (see BJ5.50.1 below); and

iii. is invested in New Zealand in New Zealand currency; and

iv. is invested in lawful enterprises or managed funds (see BJ5.50.5) that comply with al relevant laws in force in New

Zealand; and

v. has the potential to contribute to New Zealand's economy; and

vi. is invested in either one or more of the following:

o bonds issued by the New Zealand government or local authorities; or

o bonds issued by New Zealand firms traded on the New Zealand Debt Securities Market (NZDX); or

o bonds issued by New Zealand firms with at least a BBB- or equivalent rating from international y recognised

credit rating agencies (for example, Standard and Poor's); or

o equity in New Zealand firms (public or private including managed funds and venture capital funds); or

o bonds issued by New Zealand registered banks; or

o equities in New Zealand registered banks; or

o residential property development(s) (see BJ5.50.10) or

o commercial property (see BJ5.50.20); or

o bonds in finance companies (see BJ5.50 (d));or

o eligible New Zealand venture capital funds (see BJ5.50.15); or

o philanthropic investment (see BJ5.40.1); or

o ‘Angel funds or networks’ investments.

Note: New Zealand registered banks are defined by the New Zealand Reserve Bank Act 1989.

Acceptable investment in PRC

F3.10.25 Definition of 'acceptable investment'

a. An acceptable investment means an investment that:

i. is capable of a commercial return under normal circumstances; and

ii. is not for the personal use of the applicant(s) (see F3.10.30); and

iii. is invested in New Zealand in New Zealand currency; and

iv. is invested in lawful enterprises or managed funds that comply with al relevant laws in force in New Zealand (see

F3.10.35); and

v. has the potential to contribute to New Zealand's economy; and

vi. is invested in either one or more of the following:

o bonds issued by the New Zealand government or local authorities; or

o bonds issued by New Zealand firms traded on the New Zealand Debt Securities Market (NZDX); or

o bonds issued by New Zealand firms with at least a BBB- or equivalent rating from international y recognised

credit rating agencies (for example, Standard and Poor's); or

o equity in New Zealand firms (public or private including managed funds) (see F3.10.35); or

o bonds issued by New Zealand registered banks; or

o equities in New Zealand registered banks; or

o residential property development(s) (see F3.10.40); or

o bonds in finance companies (see F3.10.25 (c)).

Note: For the purposes of these instructions, convertible notes are considered to be an equity investment.

New Zealand registered banks are defined by the New Zealand Reserve Bank Act 1989.

Acceptable investment in TRC

V3.120.5.25 Definition of 'acceptable investment'

a. An acceptable investment means an investment that:

i. is capable of a commercial return under normal circumstances; and

ii. is not for the personal use of the applicant(s) (see V3.120.5.30 below); and

iii. is invested in New Zealand in New Zealand currency; and

iv. is invested in lawful enterprises or managed funds that comply with al relevant laws in force in New Zealand (see

V3.120.5.35); and

v. has the potential to contribute to New Zealand's economy; and

vi. is invested in either one or more of the following:

o bonds issued by the New Zealand government or local authorities, or

o bonds issued by New Zealand firms traded on the New Zealand Debt Securities Market (NZDX); or

o bonds issued by New Zealand firms with at least a BBB- or equivalent rating from international y recognised

credit rating agencies (for example, Standard and Poor's); or

o equity in New Zealand firms (public or private including managed funds) (see V3.120.5.35); and or

o bonds issued by New Zealand registered banks; or

o equities in New Zealand registered banks; or

o residential property development(s) (see V3.120.5.40); or

o bonds in finance companies (see (c) below).

Note: For the purposes of these instructions convertible notes are considered to be an equity investment.

New Zealand registered banks are defined by the New Zealand Reserve Bank Act 1989.

Property already in NZ

• The property is under PA or joint(PA and SA) names, and the property

is the nominated funds.

• If the NZ property is the nominated funds at the pre- stage, then at

TOFI stage the property will be liquidated and invested in acceptable

investment.

At Pre & Post – AIP stage:

• The nominated funds are the PA’s

Equity in NZ

shares in the NZ company. PA

needs to provide the valuation of

firm(Public

the company showing PA shares

or Pravity)

valuation

• The acceptable investment is the

PA’s equity in the NZ company

Equity,

Shares or

At Pre & Post – AIP stage:

NZ Debt

• The nominated funds is the

value/clean cost of the shares

Securities

• The acceptable investment is the

clean cost of the shares

Market

• The nominated funds is the

value/clean cost of the bonds

Bonds

• The acceptable investment is

the clean cost of the bonds

• Most Residential Property

Residential

Development investments are

through NZ company

Property

• Similar to assessing investment in NZ

Development(

equity(shares valuation in assessing

New

nominated funds, company’s equity

Development)

as a completed investment.) we

don’t need to assess underline

investment

• The nominated funds is the

valuation of the commercial

Commercial

property

Property in

• The acceptable investment is the

how much PA or his company

NZ

invests into the commercial

property/valuation of the

commercial property

• Can the PA claim the NZ property as acceptable investment, and PA

rents out the property for commercial return and does not use as

personal use?

• Son-in-law gives NZ company shares to PA under Inv 2 application, is

it an acceptable investment for pre & post application? the

investment was made by PA?