11 May 2023

Mr Lance Watson

[FYI request #22437 email]

Tēnā koe Lance Watson,

On 12 April 2023

, you sent two emails to the Ministry of Social Development

(the Ministry) requesting, under the Official Information Act 1982 (the Act),

the following information:

•

A breakdown of the number of New Zealand Superannuation and

Veteran's Pension recipients for each of the categories listed here:

https://aus01.safelinks.protection.outlook.com/?url=https%3A%2F%2

Fworkandincome.govt.nz%2Fmap%2Fdeskfile%2Fnz-superannuation-

and-veterans-pension-tables%2Fnew-zealand-superannuation-and-

veterans-pension-

ra.html&data=05%7C01%7CSimon.Bennett019%40msd.govt.nz%7Ce

f2e56d5419c4b3d2b2b08db3b98e50f%7Ce40c4f5299bd4d4fbf7ed001a

2ca6556%7C0%7C0%7C638169300093721936%7CUnknown%7CTWF

pbGZsb3d8eyJWIjoiMC4wLjAwMDAiLCJQIjoiV2luMzIiLCJBTiI6Ik1haWwi

LCJXVCI6Mn0%3D%7C3000%7C%7C%7C&sdata=HsiBpJGy5kDhtMi7

%2FJLGVJGIb1nQrFHZ7gkuWw%2ByMcI%3D&reserved=0

This includes different tax codes. As an example:

M Tax code:

Single, living alone:

Single, sharing accommodation:

Married person or partner in a civil union or de facto relationship:

Married or in a civil union or de facto relationship, both qualify:

Married or in a civil union or de facto relationship, grandparented non-

qualified partner included on or after 1 October 1991:

Married, grandparented non-qualified partner included before 1 October

1991:

Hospital rate:

And then the same for S tax code, and SH, ST, SA.

This does not need to show separate stats for NZS and VP, these can be

combined.

Can this please be the numbers as at 1 April 2023. If not possible,

then current numbers are fine.

•

Based on my understanding, the net rate of superannuation is calculated

with the following method:

Gross Rate - Tax (rounddown to nearest cent).

As an example, the current Single, Living Alone rate of NZ Super is

$578.67 Gross per week. For the M Tax code, the formula for calculating

the net rate is as follows (In Excel Formula formatting):

=578.67 - ROUNDDOWN(269.23*0.105 + (ROUNDDOWN(578.67,0) -

269.23)*0.175,2)

=496.37

269.23 is the tax bracket 14000 divided by 52 to get the weekly tax

bracket, and rounded down.

This comes from documentation received from MSD, and can be

confirmed by checking current NZ Super rates in MAP, and further

confirmed by replacing 578.67 with other M tax code rates to see that

the method still works.

My concern here are two components of the calculation.

1. 269.23, it is exceptionally odd in a tax calculation to round a tax

bracket before it is put into a calculation, as this means we're using a

slightly incorrect tax bracket.

2. ROUNDDOWN(578.67,0), It is fairly common to round down annual

income to the nearest dollar when paying tax, but this doesn't apply to

weekly/fortnightly amounts. No other benefit type does this. In this

instance it means (0.67*52=)$34.84 is going untaxed each year.

My Official Information Request is as follows:

Page 2 of 9

1. Can you confirm the method MSD uses to calculate the net rate of

NZS from the gross rate, or if this is calculated in reverse after Annual

Gross Adjustment, the method to calculate the gross rate from the net.

Especially if the calculation is different from my understanding above.

2. Why does MSD round down the tax bracket when performing the

gross to net calculation?

3. Why does MSD round down the weekly/fortnightly gross rate, leaving

the remaining cents untaxed?

Please find below

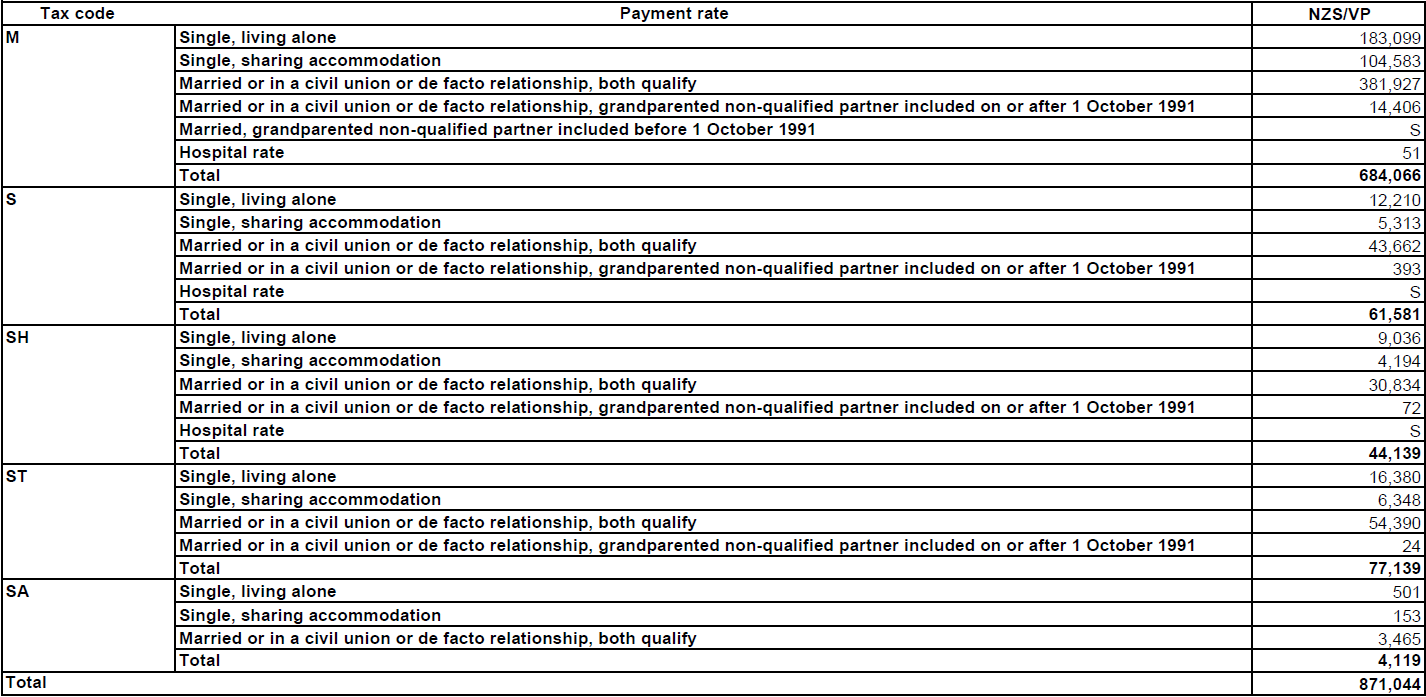

Appendix One containing

Table One that answers your

request for the number of recipients of New Zealand Superannuation (NZS)

and the Veteran’s Pension (VP), broken down by payment rate and tax code.

You will note that the information regarding some individuals is withheld under

section 9(2)(a) of the Act in order to protect the privacy of natural persons.

The need to protect the privacy of these individuals outweighs any public

interest in this information.

In the interest of clarity, I will respond to each question from the second part

of your request in turn.

1. Can you confirm the method MSD uses to calculate the net rate of

NZS from the gross rate, or if this is calculated in reverse after

Annual Gross Adjustment, the method to calculate the gross rate

from the net. Especially if the calculation is different from my

understanding above.

NZS rates are updated each April according to

section 15 an

d section 16 of the

New Zealand Superannuation and Retirement Income Act 2001 (NZSRIA).

Section 15 states that the net rates must be increased by the amount of the

annual Consumers Price Index (CPI) change for the most recent December

year.

Section 16 states that, if necessary, the net married/coupled rate is adjusted

so that it is at least 66% of the net average wage, but no more than 72.5%.

The two main single net rates are then set at 60% (single sharing) and 65%

(single living alone) of the married/coupled net rate.

Thereafter, the Ministry calculates the gross rates from the new net rates.

For the married/coupled rate:

Net April 23 = $381.82 per week per person

Page 3 of 9

An initial estimate of gross is created as below. The Ministry then adjusts it

by the required amount to ensure that net to gross followed by gross to net

takes us back to original net.

Gross = GrossThres2 + (NetRate – NetThres2) / (1 – TaxRate2)

= $269.23 + ($381.82 - $240.96) * (1 - 0.175)

= $269.23 + $170.74

= $439.97 (439.9684 as no rounding in some parts)

GrossThres2 = Round (14,000/52,2) = $269.23

NetRate = $381.82

NetThres2 = GrossThres2 * (1 – TaxRate1) = $269.23 * (1 – 10.5%) =

$240.96

To calculate Net we start with integer part of gross:

Tax = Int(Gross) * TaxRate1 + (Int(Gross) – Thres1/52) * (TaxRate2 -

TaxRate1)

= $439 * 0.105 + ($439 - $269.23) * (.175 - .105)

= $46.10 + $11.88

= $57.98 (57.97885)

This is then truncated to two decimal places = $57.97

Net = Gross less Tax

= $439.97 - $57.97

= $382.00

This differs to the original CPI/wage adjusted net amount of $381.82 by 18

cents.

The 18 cents is, therefore, deducted from the initial gross calculated above to

give a final gross amount of $439.79.

These calculations may be seen in columns U and AJ to AO in the sheet

named [Table1] of the Annual General Adjustment (AGA) spreadsheet that

the Ministry supplied to you last year.

They give the same results as calculations inside the Ministry’s payment

system (SWIFTT) does.

The weekly lookup tables published by Inland Revenue (IRD) includes the

ACC earners levy (see the link below):

https://www.ird.govt.nz/-/media/project/ir/home/documents/forms-and-

guides/ir300---ir399/ir340/ir340-

2023.pdf?modified=20220321212434&modified=20220321212434

However, if we alter our tax rates to include the 1.46% levy (April 22 to March

23 year as linked above) then the calculations outlined above will give a gross

married person rate of $440.00. Looking this up on page 27 of the IRD table

Page 4 of 9

gives tax of $64.57. This exactly agrees with the fictional net amount of

$375.43 (please note: the net rate differs because the 1.46% ACC levy is

treated in the AGA model as a tax change to be incorporated before the CPI

adjustment is made).

The fact that these amounts are the same indicates that the calculation is

correct.

The Ministry is aware that the answer may be slightly different when using the

IRD online calculator. On several occasions, Inland Revenue assured the

Ministry that both versions are correct, and that they do not have a preferred

approach.

The Ministry notes that the process below gives the identical answers to above,

given the gross amount already calculated.

gw = int(Gross)

paye = gw * TaxRate1

tax = paye + (gw – Thres1/52) * (TaxRate2 - TaxRate1)

Tax = Int(Round(100 * tax, 1)) / 100

Net = Gross - Tax

2. Why does MSD round down the tax bracket when performing the gross

to net calculation?

The tax bracket is simply rounded after dividing by 52. It is not rounded down.

Further, the rounded figure is only used when estimating which tax bracket,

the given net or gross amount falls into. It is also used to estimate the net

threshold and the initial gross amount.

The formula (Thres1/52) used immediately above and on the previous page

for net calculations is not rounded.

It is also noted that the rounding difference in the 14,000/52 tax threshold is

0.00077 cents, producing negligible differences that would be easily covered

by rounding elsewhere in the calculations.

3. Why does MSD round down the weekly/fortnightly gross rate, leaving

the remaining cents untaxed?

As indicated in the second part of the answer to question 1, the tax tables

published by IRD truncate weekly payment rates to the next lowest dollar.

For those who declare other earnings in addition to NZS or VP, there may well

be residual income tax to be paid to IRD at the end of the income tax year.

Page 5 of 9

Please note that the tax tables long predate IRD’s online calculators.

Section 15 (2) of the NZSRIA states that the gross rates listed in Schedule 1

are adjusted in accordance with changes to the CPI “after the deduction of

standard tax”.

Section 15 (1) defines “standard tax” as “the amount of tax reckoned on a

weekly basis that would be deductible in accordance with the tax code “M”

stated in schedule 5, part A,

clause 4, table row 1 of the Tax Administration

Act 1994.”

This will account for why the Ministry uses the weekly tables rather than the

fortnightly tables.

Earlier references to specific tax legislation included the weekly tax table as an

appendix. At the time, the Ministry was instructed to use the figures in the

appendix. This approach remains, whereby the Ministry agrees with tax

amounts published in the weekly tax tables (without the ACC levy).

In each case, the IRD tables say to use the lower whole dollar amount (i.e.,

drop any cents per week) and notes that the tables may differ to the online

calculator results (both on page 9).

The principles and purposes of the Official Information Act 1982 under which

you made your request are:

• to create greater openness and transparency about the plans, work and

activities of the Government,

• to increase the ability of the public to participate in the making and

administration of our laws and policies and

• to lead to greater accountability in the conduct of public affairs.

This Ministry fully supports those principles and purposes. The Ministry

therefore intends to make the information contained in this letter and any

attached documents available to the wider public. The Ministry will do this by

publishing this letter and attachments

on the Ministry’s website. Your personal

details will be deleted, and the Ministry will not publish any information that

would identify you as the person who requested the information.

If you wish to discuss this response with us, please feel free to contact

[MSD request email].

Page 6 of 9

If you are not satisfied with this response about New Zealand Superannuation,

Veteran’s Pension and tax, you have the right to seek an investigation and

review by the Ombudsman. Information about how to make a complaint is

available

at www.ombudsman.parliament.nz or 0800 802 602.

Ngā mihi nui

Bede Hogan

Policy Manager (Income Support)

Page 7 of 9

Appendix One

Appendix One

Table One: The number of recipients of New Zealand Superannuation (NZS) and Veteran’s Pension, broke down by

payment rate and tax code

Notes:

• The data tables include the number of NZS and VP recipients, tax codes (‘M’, ‘S’, ‘SH’, ‘ST’, ‘SA’), and payment rate categories.

• These data tables have had random rounding to base three applied to all cell counts in the table.

• A value of one or two will always be rounded to three.

• The impact of applying random rounding is that columns and rows may not add exactly to the given column or row totals.

• The published counts will never differ by more than two counts.

• In certain circumstances, low numbers may potentially lead to individuals being identified. Due to privacy concerns, numbers for some

categories of clients were suppressed and replaced by an ‘S’.

Page 9 of 9

Document Outline