Policy report:

Debt to Government: Comparing IR and MSD’s

Policy report:

Debt to Government: Comparing IR and MSD’s

approaches to writing off debt

Date:

27 June 2022

Priority:

Medium

Security level:

In Confidence

Report number: IR2022/308

REP/22/6/553

Action sought

Action sought

Deadline

Parliamentary Under-

Note the contents of this report.

N/A

Secretary to the Minister

Refer report to Minister for Child Poverty

of Revenue

Reduction, Minister for Social Development

and Employment, Minister of Revenue,

Minister of Justice and Minister of Housing.

Contact for telephone discussion (if required)

Name

Position

Telephone

Samantha Aldridge

Principal Policy Advisor, Inland s 9(2)(a) OIA

Revenue

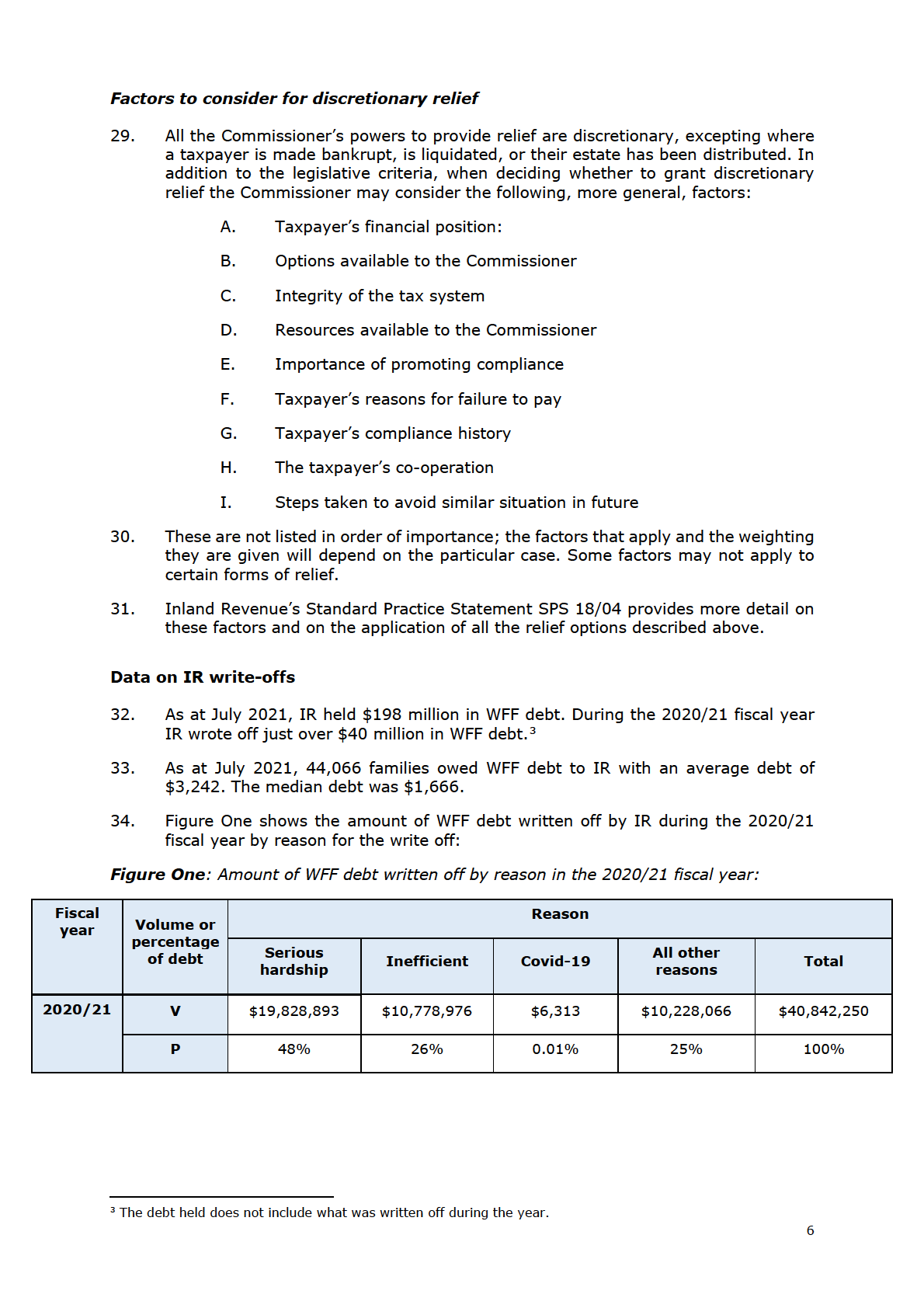

Adaire Koia-Ward

Senior Policy Analyst, Ministry s 9(2)(a) OIA

of Social Development

1

Purpose and context

5.

Following your request for information on 13 May, this report compares IR and

MSD’s approaches to writing off debt. It provides information from each agency on

the legislative provisions allowing them to write off debt (in the context of each

agency’s role and functions) and their operational practices.

6.

Information on IR’s approach relates to debt created via the overpayment of WFF

tax credits.1 The write-off powers discussed in this paper are not necessarily

applicable to other payments administered by Inland Revenue, such as student

loans and child support. Information on MSD’s approach relates to debt created via

the overpayment of benefits and recoverable assistance.

Inland Revenue’s approach to WFF debt

The creation of debt

7.

WFF entitlements are calculated as an annual figure according to a customer’s

income and family circumstances. Customers may receive their entitlement during

the year (weekly or fortnightly) or at the end of the tax year.

8.

If a customer’s income or circumstances change during the year, this will change

their entitlement. If they are receiving payments weekly or fortnight, failure to

update IR of these changes in a timely manner may result in an overpayment.

Customers who receive payments at the end of the year can also be overpaid if

their initial entitlement is recalculated (e.g., if additional income is declared after

the end of year ‘square up’ is completed).

9.

Not all WFF overpayments result in debt as they only become debt after the

repayment is due. The due dates will vary depending on the customer’s filing

obligations.

Legislative provisions

10.

The Tax Administration Act 1994 (the Act) has an overarching provision which

requires the Commissioner to collect the highest net revenue over time that is

practicable within the law, having regard to the resources available to the

Commissioner, the importance of promoting compliance (especially voluntary

compliance), and the compliance costs incurred by taxpayers.

11.

The Income Tax Act 2007 provides that the Commissioner may recover WFF

overpayments from a customer as if the amount was income tax payable by that

customer. Therefore, the same powers that apply to the collection of tax also apply

to the collection of WFF overpayments.

12.

The Act gives the Commissioner powers to provide relief by writing off debt,

remitting penalties/interest, or entering into instalment arrangements where this is

considered appropriate.

13.

A debt, including any shortfall penalties, cannot be written off where the customer

is liable to pay a shortfall penalty for either taking an abusive tax position or evasion

in relation to the debt. However, late filing penalties, late payment penalties, and

use of money interest on the underlying tax can still be written off.

1 Although MSD administers the payment of some WFF tax credit components for its customers (Family tax credit

and Best Start tax credit payments), al WFF debt is established, managed, and col ected by IR.

3

14.

If, after considering the taxpayer’s circumstances, the Commissioner concludes that

relief under the Act is not appropriate, they may either collect the amount owing or

apply to have the taxpayer made bankrupt.

15.

Relief powers available under the Act are summarised below.

Relief powers

16.

An amount of WFF debt may be written off if collecting it:

16.1 would place the taxpayer in “serious hardship”; or

16.2 is considered an inefficient use of IR’s resources.

17.

The concepts of serious hardship and inefficient use of resources, as they apply to

IR administration, are discussed below.

18.

The following relief powers are also available to IR:

18.1 Where an amount is considered irrecoverable, the Commissioner may write

it off.

18.2 When a taxpayer is made bankrupt, is liquidated, or their estate has been

distributed, the Commissioner must write off amounts that cannot be

recovered.

18.3 Interest or certain penalties may be remitted if to do so is consistent with

the Commissioner’s duty to collect the highest net revenue over time through

voluntary compliance.

18.4 A remission of penalties/interest may be granted if an event/circumstance

beyond the customer’s control provides a reasonable justification for not

meeting their obligations (for which they were given the penalty), for

example, a death or illness of a family member.

18.5 Interest may be remitted when there has been an emergency event declared

in an Order in Council which prevented the taxpayer from making the

payment.

18.6 The Commissioner will write off outstanding tax/debt when the balance

payable after the end of the tax year is $50 or less i.e., is ‘de minimis’2.

19.

There is no specific provision allowing for the write-off of debt when it arises from

IR error. However, IR error will be taken into consideration when determining

whether to grant relief on other grounds.

Serious hardship

20.

Where a customer is unable to make repayment in full, they may request their debt

be written off under the serious hardship provision. Customers may be asked to fill

out a hardship relief request form and provide documentation to prove they are in

hardship.

21.

The Tax Administration Act sets out categories which staff use to determine whether

a customer is in serious hardship. A customer may be in serious hardship when:

21.1 they or their dependant has a serious illness;

2 For IR3 filers (the self-employed) the balance must be $20 or less.

4

21.2 they would likely be unable to meet minimum living expenses estimated

according to normal community standards of cost and quality;

21.3 they would likely be unable to meet the cost of medical treatment for an

illness or injury of the taxpayer, or of their dependant;

21.4 they would likely be unable to meet the cost of education for their

dependant; or

21.5 any other factor that the Commissioner thinks relevant would likely arise.

22.

If a customer is determined to be in serious hardship, relief options include:

22.1 a full or partial write-off (including fully writing off core tax, interest, or

penalties);

22.2 an instalment arrangement to pay some or all of the debt; or

22.3 a combination of the two.

23.

Customers who enter an instalment arrangement may either make payments

themselves or have their weekly/fortnightly WFF entitlement reduced to cover

repayments (this option must be initiated and agreed to by the customer).

Inefficient use of resources

24.

The Act gives the Commissioner the discretion to write off debt where collecting

outstanding amounts is expected to be an inefficient use of the Commissioner’s

limited administrative resources.

25.

IR determines which WFF debts to write off automatically under this provision

according to the value of the debt and the customer’s family scheme income.

Customers who have any of the following in place will be excluded from the

automatic write-off:

25.1 any active account halts

25.2 an open or pending audit case

25.3 legal action underway

25.4 fraud indicators

25.5 a repayment arrangement

26.

Precise parameters for the debt value and family scheme income are determined

on an annual basis in consideration of factors such as economic conditions in New

Zealand and consistency with write-offs for other products (e.g., Income Tax).

These parameters are not provided to staff or customers. s 18(c)(i) OIA

.

27.

WFF debt may also be written off as an inefficient use of the Commissioner’s

resources on a case-by-case basis.

28.

There will be some instances where the Commissioner will pursue debt even though

the cost of collection may be higher than the outstanding tax because of their

obligation to ensure the integrity of the tax system and promote taxpayer

compliance (e.g., where the debt is connected to fraud).

5

The Ministry of Social Development’s approach to Recoverable Hardship

Assistance and benefit overpayment debt

Re coverable Hardship Assistance and Overpayment debt

35.

As at 31 March 2022, there was more than 578,000 people with debts to MSD,

which average $3,498 per person.4 In the 2021/22 full year to 31 March 2022, MSD

has written off around $16.3 million in debt or approximately 0.76 percent of the

total debt of $2.133 billion (as at 31 March 2022). $1.3 billion is attributed to current

clients (62 percent).

Recoverable Hardship Assistance debt is established to help the client meet an immediate

and essential need

36.

Hardship assistance is the third tier5 of assistance in the welfare system. It provides

discretionary assistance and is generally one-off. It consists of Special Needs Grants

(SNG), of which some are recoverable, and Advance Payments of Benefits

(Advances) and Recoverable Assistance Payments (RAPs), which are always

recoverable.6

37.

Hardship Assistance is relatively unique in that hardship is the driver for granting

recoverable assistance. Eligibility for hardship assistance is targeted at those with

limited cash and assets who have immediate and specific needs that cannot be met

by their own resources. For recipients of recoverable hardship assistance, debt

occurs when clients contact MSD and request support to meet their immediate and

essential needs.

Overpayment debt can occur when a client’s personal or financial circumstances change

38.

Overpayment debt can occur when a clients’ circumstances change and MSD does

not receive this information in time to update their payments accordingly. Clients

are required to notify MSD of any change in their circumstances, including income

they receive that affects their benefit entitlement.

39.

A few examples include debts created when a client is late in declaring a change in

income which would lead to a reduction in MSD payments, or as the result of data

matching with other agencies or following a fraud investigation.

Legislative provisions to write off and recover debt

40.

The Social Security Act 2018 (the Act) imposes a legislative duty on MSD to take all

reasonably practicable steps to recover debt and empowers MSD to recover debts

to the Crown.7 This is reflected in MSD’s current recovery and write-off provisions.8

41.

Section 362 of the Social Security Act 2018 establishes MSD’s duty to recover debts.

It recognises that welfare assistance is a major form of public expenditure and that

the public is entitled to expect that MSD will effectively recover welfare debts. This

is also part of MSD’s obligations to manage public money responsibly under the

Public Finance Act 1989.

4 Note that this figure includes al types of debs, including recoverable assistance, overpayments, social housing

debt, Student Al owance debt, and fraudulent debt.

5 The first tier of support in the welfare system is main benefits, the second tier is supplementary assistance.

6 The third tier also includes on-going support in the form of Temporary Additional Support (TAS) which is a

supplementary limited time payment for those who cannot meet their regular essential living costs from

chargeable income and other resources, and Emergency Housing Special Needs Grants (EHSNGs) and Housing

Support Products (HSPs) which are both recoverable.

7 Defined at regulation 206 of the Social Security Regulations 2018.

8 Social Security Act 2018, section 362.

7

42.

MSD must determine a rate or method9 of debt recovery, but MSD has discretion

about what this can be, including the option to defer (suspend) recovery, and these

can be amended as clients’ circumstances change.10

43.

MSD does not enforce penalties on debt except in cases of fraud, but this is only

used in a small number of circumstances.

44.

The Act also provides for exceptions to the duty to recover debt made in the Social

Security Regulations 2018 (the Social Security Regulations) and Ministerial

Directions.11 There are currently four main exceptions to MSD’s duty to recover

debt:

44.1 if the debt was caused by error;

44.2 if exceptions are provided for in the Social Security Regulations;

44.3 if the debt is uneconomic to recover; or

44.4 if the Ministers of Finance and Social Development and Employment have

agreed to exceptions for public finance reasons.

45.

These exceptions are explained further below.

Social Security regulations provide for how to test debts to determine whether the debt

was caused by MSD error

46.

Social Security Regulations provide for new debts, including recoverable assistance

and overpayment debts, to be tested to determine if that debt was created by MSD

error to establish whether it should be recovered.12

47.

Debt caused by MSD error must meet all of the following five criteria to be

considered non-recoverable:

47.1 the debt is a result of an error by MSD;

47.2 the client did not intentionally contribute to the error – i.e., whether the

client intentionally or deliberately took some action, or failed to take action,

or delayed action which resulted in an overpayment;

47.3 the client changed their position – i.e., when a client makes different financial

decisions with the overpayment received than they would have without that

additional money;

47.4 the client received the money in good faith – i.e., the client received the

money without any knowledge of their lack of entitlement to it; and

47.5 it would be inequitable to recover the debt – this requires full consideration

of their current circumstances, including their financial position, whether

they have the resources to repay the debt, and the degree of any error made

by Work and Income.

The Minister for Social Development and Employment and the Minister of Finance have

jointly given an authorisation about some debts that can be written off13

9 Including court proceedings and deductions from benefits and other sources.

10 Clause 4 of the Ministerial Direction states MSD must give consideration to certain matters in relation to rate

and method of recovery.

11 Ministerial Direction on Debt Recovery Amendment 2016 and Delegation from the Minister of Finance and the

Minister for Social Development and Employment to the Chief Executive of the Ministry of Social Development to

Write-off Crown Assets 2020.

12 Social Security Regulations 2018, regulation 208

13 Social Security Regulations 2017, regulation 207(3)

8

48.

The Minister of Finance and the Minister for Social Development and Employment

can also use the ability in Social Security Regulations14 to specify certain types of

debt which can be written off and delegate, pursuant to the Public Service Act 2020,

the authority to write off debts under a specific set of circumstances to the Chief

Executive of MSD. An authorisation to this effect has been given, and specified

circumstances include when:

48.1 the proceeds of the sale of assets seized by Court order are paid to the

Crown;

48.2 the debt or identity of the debtor cannot be proven;

48.3 the debtor is insolvent;

48.4 the agent is insolvent;

48.5 the debtor is deceased;

48.6 the debt is due to foreign exchange balances (due to agreement of payment

amount in foreign currency and fluctuations of exchange rates);

48.7 all economic avenues of collection have been exhausted and the debt is $50

or less;

48.8 the debt cannot be recovered due to estoppel in accordance with the

Property Act 2007 (this is in relation to student debt);

48.9 the debtor is a participant in a Witness Protection or Relocation Programme;

48.10 the debt cannot be proven to the Court’s satisfaction; or

48.11 the debt established cannot be recovered in accordance with debts caused

wholly or partly by errors to which debtors did not intentionally contribute

(regulation 208 of the Social Security Regulations15).

MSD may defer (provisionally write off) debts of less than $20,000

49.

MSD defines uneconomic to recover

16 to be when the cost of recovery outweighs

the expected return of debt. MSD currently automatically writes off debts of $50 or

less of non-current clients after 70 days of non-payment.

50.

This threshold is based on analysis from 2015 that found that the average cost of

collection is $59.80 per debt. At the time, increasing the write-off limit to $50

aligned MSD with other agencies’ write-off powers and was appropriately balanced

with the risk of changing client repayment behaviours.

51.

This approach was reaffirmed through the 2020 Delegation from the Minister of

Finance and the Minister for Social Development to the Chief Executive of the

Ministry of Social Development to Write-off Crown Assets (discussed above).

52.

Debts of higher amounts can also be assessed to determine whether collection of

that debt is appropriate if:17

52.1 the debt is less than $200 and there have been no repayments during the

previous six months;

52.2 the debt is less than $1000 and there have been no repayments during the

previous 12 months;

52.3 the debt is less than $2000 and there have been no repayments during the

last 2 years; or

14 Social Security Regulations 2018, regulation 207(1)(d)

15 Previously section 86(9A) Social Security Act 1964.

16 Social Security Regulations 2018, regulation 207(1)(c).

17 These timeframes only apply in cases where fraud is not a factor i.e., there are separate conditions for cases

of fraud. Some values of debt also require other conditions regarding client identification to be met.

9

52.4 the debt is more than $2000 but less than $20,000 and there has been no

ability to gain repayment or communicate with the debtor for at least six

years.

53.

Debts written off under these grounds can be reactivated once the client accesses

social security (including superannuation) again, as recovery is once again feasible.

This approach aligns with MSD’s duty to recover debt.

Debt recovery is written off according to conditions in the Social Security Regulations

54.

The Act empowers regulations to be made permitting changes to debt write-off

settings.18 However, since the changes to primary legislation in 2014 which clarified

MSD’s duty to recover debt, no further debt recovery regulation changes have been

made by Government.

55.

When making new or amending existing regulations to permit any methods of write-

off, the Minister for Social Development and Employment must be satisfied that

these changes are likely to:

55.1 prevent accumulation of debt by any category of beneficiary and assist those

beneficiaries to reduce their levels of debt while on a benefit;

55.2 assist any category of beneficiary to move from dependence on a benefit to

self-support through employment by ensuring that those beneficiaries do not

face increasing benefit debt repayments when they enter the workforce;

55.3 provide a positive incentive for beneficiaries to enter employment or stay in

employment; or

55.4 achieve more than one of these objectives.

56.

Any changes to current settings would have fiscal and operational implications.

Comparing IR and MSD’s approaches to writing off debt

Agency functions

57.

Under the Tax Administration Act 1994, the Commissioner of IR is charged with the

care and management of the tax system, which includes WFF tax credits. This

includes a duty to collect the highest net revenue over time that is practicable within

the law, having regard to the resources available to the Commissioner, the

importance of promoting compliance (especially voluntary compliance), and the

compliance costs incurred by taxpayers. IR’s write-off powers reflect these

responsibilities.

58.

By contrast, MSD’s debt recovery and write-off powers are primarily focused on its

legislative duty to recover debt. Section 362 of the Social Security Act 2018,

establishing MSD’s duty to recover debts, recognises that welfare assistance is a

major form of public expenditure and that the public is entitled to expect that MSD

will effectively recover welfare debts.

Legislative provisions

59.

There are two significant differences between IR and MSD’s powers to write off debt.

60.

First, IR may do so where a customer is considered to be in serious hardship.

Although MSD may take a customer’s circumstances into account when determining

18 Social Security Act 2018, ss 444 and 448. Regulation 207(1)(b), subpart 11, Social Security Regulations 2018.

10

repayment arrangements (or any subsequent amendments to existing

arrangements), they may not write off debt because a customer is in hardship.

61.

Second, IR’s power to write off debt as an inefficient use of the Commissioner’s

resources is much broader than MSD’s power to write off debt as uneconomic to

recover. IR has discretion to determine annual parameters for writing off debt as

part of an automatic process at the end of the year (in addition to the automatic

$50 de minimis write-off). s 18(c)(i) OIA In comparison, MSD’s power has a much

narrower scope. MSD writes off up to $50 in debt for non-current clients after 70

days of non-payment, but for amounts in excess of $50, collection is prioritised, or

deferred if MSD is unable to get into contact with the person.

19 s 18(c)(i) OIA

.

11