1982

Act

Information

Official

the

under

Released

Appendix A

Document 1

Te Tari Taiwhenua

Department of Internal Affairs

Purpose

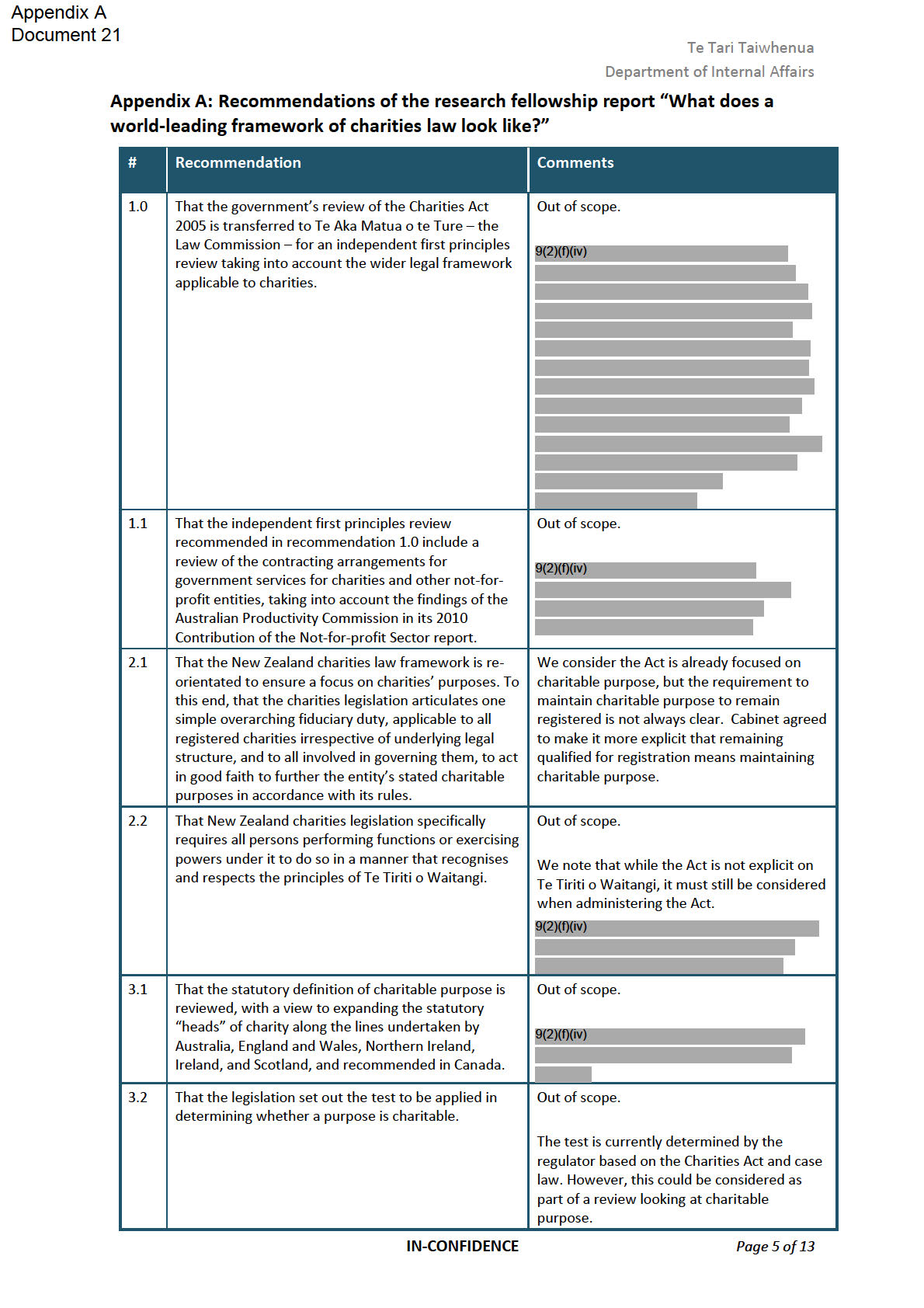

1.

This aide memoire supports your oral item at the Cabinet Social Wellbeing Committee

(SWC) meeting on the 17 March 2021. Your oral item updates SWC on the work to

modernise the Charities Act 2005 (the Act). Attached is:

a)

an oral item paper to table at SWC, outlining your proposed approach to

modernising the Act in

Appendix A;

b)

talking points to support the oral item in

Appendix B;

c)

suggested responses to possible questions from SWC members in

Appendix C;

and

d)

Cabinet Committee Oral Item Request Template in

Appendix D.

1982

Background on the oral item

2.

Cabinet made initial decisions on the scope of the work to modernise the Act in 2018.

Act

You have confirmed you wish to continue with this work as a priority for your portfolio.

The oral item is an opportunity to update SWC on your intentions for this work

including:

a)

that you intend to make practical improvements to the Act;

b)

that you are taking a staged approach to focus on addressing the more pressing

and practical issues for the sector as the priority. Stage one considers:

o

charities’ obligations (including reporting requirements);

Information

o

the regulator’s powers and decision-making;

o

the accessibility of appeals; and

o

charities’ accumulation of funds and business activities;

Official

c)

that you wil consider a process for stage two next year which wil focus on the

remaining matters from public consultation including advocacy by charities; and

the

d)

that you will seek policy decisions from Cabinet on reporting requirements for

charities, and charities accumulation of funds and business activities in June 2021.

You will take the remaining issues to Cabinet in December 2021.

3.

Your office wil need to submit a request to Cabinet Office to present the oral item by

under

10.00am, Thursday 11 March 2021, and submit the oral template form (Appendix D).

4.

The Minister of Revenue is not a member of SWC. Given the Minister’s interest in the

tax component of the work, we suggest you also update the Minister of Revenue on

your intentions for this work. We can draft a letter for you to enable this.

5.

We will provide advice on policy options for reporting requirements for small charities,

and an engagement plan which includes details about publicly announcing the work in

Released

the week beginning 15 March 2021.

Hon Priyanca Radhakrishnan

Minister for the Community

and Voluntary Sector

/

/

IN CONFIDENCE

Page 2 of 10

Appendix A

Document 1

Te Tari Taiwhenua

Department of Internal Affairs

Appendix A: Oral item Cabinet Social Wellbeing Committee 17 March 2021 -

Modernising the Charities Act 2005

1982

Act

Information

Official

the

under

Released

IN CONFIDENCE

Page 3 of 10

Appendix A

Document 1

Te Tari Taiwhenua

Department of Internal Affairs

Oral item - Cabinet Social Wellbeing Committee: Modernising the Charities Act

The Charities Act provides a registration, reporting and monitoring system to support public

trust and confidence in charities

1. More than 27,000 charities are registered under the Charities Act (the Act). Charities

spend around $18 billion annually on charitable purposes and manage $65 billion in

assets. Some charities are widely known, such as Plunket Society or the Salvation Army.

Many more are small charities that make a huge difference in communities, from

maintaining marae to running toy libraries.

I intend to resume policy work to modernise the Charities Act

2. Modernising the Act is about enabling the charities sector to thrive and to continue their

1982

valuable contribution to community wel being and social cohesion.

3. I intend to start by making practical improvements. To do so requires careful balancing of

Act

principles like transparency with the compliance burden that small charities face from

extensive annual reporting. I will take a balanced approach to looking at the business

activities charities are involved in, while being mindful that the sustainability of some

charities is directly related to running successful businesses.

A staged approach to deliver change and to pass an amendment bil this term

4. I wil build on and progress the work that my col eagues launched last term. In 2019, wide-

ranging and passionate views came through on the Act, through 27 community meetings

Information

and 363 submissions on a discussion document.

5. In restarting this work, I will shortly announce stage one. Stage one will lead to an

amendment bill this term for a number of key areas publicly consulted on last term.

6. Stage one looks at: charities’ obligations; the regulator’s powers and decision-making; the

Official

accessibility of appeals on decisions; and charities’ accumulation of funds and business

activities. Progressing the remaining matters consulted on last term, such as advocacy by

charities, is important. I wil investigate a process for stage two next year.

the

Targeted engagement before taking the first set of policy proposals to Cabinet

7. Policy development and testing with key stakeholders will focus first on small charities’

reporting requirements, and charities’ accumulation of funds and business activities. I

under

intend to take the first set of policy proposals to Cabinet in June 2021. I will then return to

Cabinet in December 2021 with the remaining policy issues for stage one. I will ensure

that Ministers with portfolio interests in this work are kept informed of progress.

Recommendation

8. It is recommended that the Cabinet Social Wellbeing Committee:

Released

8.1.

notes that the Minister for the Community and Voluntary Sector intends to resume

work to modernise the Charities Act 2005;

8.2.

notes that stage one of this work focuses on more practical issues to improve the

operations of the charitable sector with fundamental matters to be considered as

part of a later stage; and

8.3.

notes that the Minister for the Community and Voluntary Sector intends to publicly

announce the resumption of the work to modernise the Charities Act 2005 shortly.

IN CONFIDENCE

Page 4 of 10

Appendix A

Document 1

Te Tari Taiwhenua

Department of Internal Affairs

Appendix B: Talking points for Cabinet Social Wel being Committee on 17 March

2021: Modernising the Charities Act

Inform and update on the work to modernise the Charities Act

• I want to update you on the work to modernise the Charities Act that my col eagues

launched in the previous term.

• In 2018 we began to look at how wel the Act is working. We gained extensive information

from public consultation in 2019 about the issues and opportunities that charities face.

• There are more than 27,000 charities registered under the Charities Act. As we know,

charities contribute hugely to the strength of communities across New Zealand – in sports,

the arts, health, and other countless activities that make a real difference to people’s lives.

1982

My aim is to progress the modernisation of the Charities Act to deliver real world benefits

• Given the significance and contribution of the sector to communities, I am keen to

Act

continue this work, and I am committed to achieving practical improvements this term.

• My goal is to pass legislative amendments to modernise the Act by 2023.

• The modernisation work will ensure that the Charities Act:

o is effective and fit for purpose;

o promotes continued public trust and confidence in the charitable sector; and

o helps deliver real world benefits to charities.

Information

Taking a staged approach to deliver more practical benefits first

• To deliver real change and benefits, a staged approach is important. Most charities are

small and are trying to meet their obligations, but the balance between the compliance

burden and transparency needs addressing.

Official

• Stakeholders were consulted on a wide range of matters in 2019.

• Stage one will lead to an amendment bill, and will look at:

the

o the obligations that charities have under the Act, including the annual reporting

requirements that small charities face, as well as the duties for officers of charities;

o the regulator, in the sense of its powers, accountability and decision-making under its

current structure (being the

under independent Charities Registration Board and Charities

Services within the Department of Internal Affairs);

o the accessibility of appeals within the current structure of appeal bodies; and

o charities’ business activities and their accumulation of funds.

• I will consider a process for stage two next year, but it will focus on the remaining matters

from public consultation. This means:

Released

o any additional purposes that might be appropriate for the Act;

o Te Ao Māori (in the sense of more fundamental consideration beyond the Te Ao Māori

lens that wil be applied to al of the stage one matters); and

o where the line is for advocacy by charities.

Next steps

• I plan to announce my decision to resume work on modernising the Charities Act in the

near future.

IN CONFIDENCE

Page 5 of 10

Appendix A

Document 1

Te Tari Taiwhenua

Department of Internal Affairs

• I will return to you in June and December this year for policy decisions on stage one

matters.

• The first set of policy decisions will be on the objectives for this work, the reporting

requirements for small charities and the business and accumulation activities charities are

involved in. My officials will carry out targeted consultation with key stakeholders to test

and refine the proposals ahead of Cabinet consideration.

• I will keep you informed at key points, as the diverse activities that charities perform

overlaps with many of your portfolio interests. Revenue is one portfolio that this work

overlaps particularly closely with, as charities receive favourable tax treatment.

• I look forward to continuing to work together on modernising the Charities Act.

1982

Act

Information

Official

the

under

Released

IN CONFIDENCE

Page 6 of 10

Appendix A

Document 1

Te Tari Taiwhenua

Department of Internal Affairs

Appendix C: Suggested responses to possible questions from SWC members

Significance and scope of this work

1. Why is this work important?

• The community sector is diverse and complex, and forms a vital part in our society.

• Modernising the Charities Act by delivering some practical improvements will achieve

real world benefits for the community sector.

• Public consultation showed there are significant issues to address, like the compliance

burden smal charities face through reporting obligations.

2. Are you looking at contracting arrangements for government services?

1982

• No, this is a legislative review of the Charities Act.

3. Is this a first principles review of the Act?

Act

• No, key concepts underpinning the Act - particularly a registration, reporting and

monitoring system for charities - remain sound.

• This work is about addressing substantive issues, while building on the Act’s strengths.

• Overall, this work continues to be guided by the 2018 terms of reference that went to

Cabinet and is not about starting from scratch. 9(2)(f)(iv)

Information

4. Why are these issues out of scope for stage one?

•

Charitable purpose. ‘Charitable purpose’ (meaning the relief of poverty, advancement

of education or religion, or any other matter beneficial to the community) was

excluded from the work launched in 2018, and was therefore not publicly consulted

Official

on in 2019. Charitable purpose can and does continue to evolve through case law.

Charitable purpose triggers strong views and opinions, and any process to consider it

would need careful planning.

the

•

Advocacy. Clarity is important on where the line is drawn when charities advocate.

With an advocacy case currently before the courts, I intend to consider advocacy in

stage two. Charities Services advise me they are also working to improve sector

understanding and applica

under tion of the current law.

•

Te Ao Māori. Te Ao Māori lens wil be used throughout this work. The issues specific

to iwi/Māori charities wil be picked up under the topics as needed. Any process to

consider Te Ao Māori in light of the more fundamental matters (like the meaning of

‘charitable purpose’ that derives from 400 years of case law) would need careful

planning.

Released

•

Structure of regulator or appeals mechanism. 9(2)(f)(iv)

9(2)(f)(iv)

IN CONFIDENCE

Page 7 of 10

Appendix A

Document 1

Te Tari Taiwhenua

Department of Internal Affairs

9(2)(f)(iv)

Timing/engagement/process

6. Why do targeted engagement, and not public consultation during the upcoming policy

development phase?

• Public consultation from 2019 provided a wealth of information about the issues and

opportunities that charities face, as well as the views of individuals, broader not-for-

profits and others.

• This base forms a solid foundation to work from, and will be added to by targeting our

engagement on specific policy proposals to key stakeholders most likely to be

affected.

1982

7. 9(2)(f)(iv)

Act

8. 9(2)(f)(iv)

Information

Connections between this work and other portfolio interests

Official

9. How do you intend to manage any crossovers between this work and other portfolio

interests?

the

• Close connections at the officials’ level and at the Ministerial level will be important,

as the Charities Act is not the only legislation that affects charities.

• For example, registered charities structured as incorporated societies would, in time,

be affected by the Incorporated Societies Amendment Bill if it progresses through the

under

House to enactment.

• Tax is another area of importance, where registration as a charity provides tax

benefits. I have written to the Minister of Revenue to inform him of my plans for this

work and will continue to keep him informed, as appropriate.

Substance of policy areas for the first phase of stage one

Released

10. What are you considering when looking at charities’ business activities?

• Business income is important to the financial sustainability of many charities.

• Charities can run businesses, if the profits only go to charitable purposes.

• An issue that may need further consideration is, for example, the risk that charitable

funds are not used for charitable purposes (e.g. a charity putting money into a failing

business).

IN CONFIDENCE

Page 8 of 10

Appendix A

Document 1

Te Tari Taiwhenua

Department of Internal Affairs

11. What are you considering when looking at charities’ accumulation of funds?

• Accumulation of funds is usually a good thing e.g. a charity saving for a new

community facility or growing assets to benefit current and future generations

(including iwi and hapu charities that hold settlement assets).

• An issue that may need further consideration is the risk to charitable funds where

charities without explanation accumulate significant funds over time, distributing little

or nothing to charitable purposes.

12. Are you looking at reporting requirements of small charities?

• Yes, we are considering whether the compliance burden on those very smal charities

is appropriate and how this could be balanced with the need for transparency in the

use of charitable funds.

1982

13. What other areas wil you look at in stage one?

Act

• I will look at the role of the regulator. This will include looking at the regulator’s

powers, accountability and transparency to the sector and the public. For example,

looking at potential enforcement tools available to the regulator where officers are

not meeting their obligations.

• I will look at the accessibility of the appeals process within the current structure.

Information

Official

the

under

Released

IN CONFIDENCE

Page 9 of 10

1982

Act

Information

Official

the

under

Released

1982

Act

Information

Official

the

under

Released

Appendix A

Document 2

Te Tari Taiwhenua

Department of Internal Affairs

Purpose

1.

This briefing provides proposed communications to announce that work is resuming to

modernise the Charities Act 2005 (the Act). This briefing also advises you of the

Department of Internal Affairs’ (the Department’s) proposed approach to stakeholder

engagement for this work, ahead of the first set of Cabinet decisions in June 2021.

Included in this briefing is:

1.1. a draft media release announcing that work is resuming to modernise the Act

(

Appendix A);

1.2. draft talking points to support you with the media release (

Appendix B);

1.3. a letter to update the Minister of Revenue on work to modernise the Act

(

Appendix C); and

1982

1.4. the key stakeholders the Department intends to engage with during policy

development (

Appendix D)

.

Act

Announcing the resumption of work to stakeholders and the wider charities sector

2.

You have decided to resume the work commenced in 2018 to modernise the Act

[briefing CVS2020000231 refers]. You have an opportunity to publicly announce your

decision, and to share with key stakeholders how you wish to progress the work.

3.

We suggest a media release as a positive way to communicate your decision to resume

the work. Given the strong levels of engagement during public consultation in 2019,

Information

we anticipate much of the sector wil be keenly interested in this work resuming.

4.

Appendix A contains a draft media release for your consideration. We understand that

Cabinet Social Wellbeing Committee (SWC) confirmed the scope and sequencing of

this work on 17 March 2021. In addition, with your fol ow up meeting scheduled for 22

March 2021 with Ministers Henare and Williams,

Official we recommend a media release in

the week beginning 22 March 2021.

5.

To support any media and stakeho

the lder engagement that you may wish to do,

Appendix B attaches talking points to support the media release. Following the

announcement, some stakeholders may wish to meet with you to discuss your

intentions for the work. We wil work with your office to support these meetings.

under

Reconnecting with and informing key stakeholders of the decision to resume work

6.

Fol owing the media release, we wil update the Department’s webpage and

communicate to key stakeholders via email. For example, we will ensure that we

promptly inform the Charities Registration Board and the Sector Group (a key

stakeholder group) that this work is resuming. If you do not wish to announce the

resumption through a media release, we seek your agreement to refer to the

resumption on the

Released Department’s webpage and contact key stakeholders in the week

beginning 29 March 2021.

7.

As noted late last year [briefing CVS202000231 refers], we propose not to restart the

Core Reference Group. In informing them about the work resuming, we anticipate that

some members may be disappointed at the decision. We wil inform them that we

intend to still seek the input of individual group members, as appropriate, as we target

the expertise needed for particular topics. As discussed in the second section of this

IN CONFIDENCE

Page 2 of 13

Appendix A

Document 2

Te Tari Taiwhenua

Department of Internal Affairs

briefing, stakeholder input will remain crucial to policy development and will inform

the later design of the amendment bil .

Keeping Ministerial colleagues informed

8.

We understand that SWC confirmed the scope and sequencing of this work on 17

March 2021. The Minister of Revenue is not a member of SWC but will likely have a

significant interest due to the connection between charities’ registration status and

their tax treatment. We suggest you update the Minister of Revenue on your decision

to resume work to modernise the Act. We have provided a draft letter for your

consideration as

Appendix C.

9.

We also note that Ministerial consultation wil be important ahead of progressing

papers through the Cabinet process. We will work at the officials’ level to keep other

1982

agencies informed as they brief their Ministers and we will support you in your

engagement with your Ministerial colleagues.

Act

10. The Ministers of Revenue and Finance will likely have a greater interest in the

connection between their portfolios and the work on topics for the June 2021 Cabinet

paper. The interests of the Ministers of Justice and Social Development and

Employment, along with the Attorney General as the protector of charities, will likely

lie in the work for the October 2021 Cabinet paper. We suggest engaging with these

Ministers more closely as policy options are developed to ensure the options are fit for

purpose.

Information

Engaging with stakeholders during policy development

Summary of earlier stakeholder engagement

11. In February 2019, the Department released a public discussion document titled

Modernising the Charities Act 2005. The discussio

Official n document was exploratory in

nature. The discussion document asked about the issues faced in the sector, but did

not propose options for consideration.

the

12. During the consultation period, the Department held 27 public community meetings

around the country. These meetings included six hui, one Pacific fono and one meeting

for representatives of ethnically diverse communities. More than 1,200 people

attended these gatherings. The Department received 363 written submissions on the

under

discussion document.

13. The Department also released an online meeting presentation video for members of

the public that were unable to attend a community meeting. This video was viewed

live by more than 350 attendees and has since been viewed more than 650 times on

demand. The Department’s webpage for this work received more than 7,000 views

during the consultation period.

Released

Engaging with targeted stakeholders is essential to developing and testing policy options

14. Public consultation provided a wealth of information about the issues and

opportunities that charities face, as well as the views of individuals, broader not-for-

profits and others. This feedback forms a solid foundation to continue working from.

15. Our engagement will now target specific stakeholders as we develop policy options

ahead of the first set of Cabinet decisions in June 2021. Stakeholder expertise is

IN CONFIDENCE

Page 3 of 13

Appendix A

Document 2

Te Tari Taiwhenua

Department of Internal Affairs

essential when considering policy options on technical topics like charities’

accumulation of funds and business activities.

16. Demonstrating that consultation has informed policy development is also an essential

element to the assessment of the Regulatory Impact Statement that accompanies

Cabinet papers. Consultation wil continue to be important later in the process, when

informing design of the amendment bil . The Legislation Design and Advisory

Committee will assess and advise on the amendment bil against the contents of the

Legislation Guidelines, which include effective consultation.

17.

Appendix D outlines the key stakeholders we intend to consult with as representatives

for the sector and subject matter experts. For example, the Sector Group, with its

wide-ranging membership, will be a key stakeholder group for this work. We have also

1982

noted the key agencies we wil be working with.

18. To ensure an appropriate cross-section and representation of the sector, we have

selected stakeholders who:

Act

a. have a high interest in a topic(s) that are in scope for this work; and/or

b. have high influence in topics(s) that are in scope for this work; and/or

c. demonstrated understanding and expertise of the topics in the 2019 public

consultation; and/or

d. provide diversity of views (based on the public consultation); and/or

e. represent a diverse range of charities across different sectors, t

Information iers and

geographical spread.

19. This list of stakeholders is subject to stakeholders’ availability and continued interest in

engaging on the work.

20. We also note that targeted engagement means not being able to consult with

Official

everyone who may be interested in the work. We recognise the risk that some

stakeholders may voice their concern about not having the opportunity to participate

the

in this next phase. The talking points at

Appendix B emphasise that at a minimum,

Select Committee consideration of the amendment bill will provide an opportunity for

all stakeholders, and the wider public, to participate.

21. We will also add to this key stakeholders list, as needed, as we move into the

under

remaining topics for stage one policy development ahead of Cabinet decisions in

October 2021. We will also update the wider charities sector at appropriate

milestones.

Released

IN CONFIDENCE

Page 4 of 13

Appendix A

Document 2

Te Tari Taiwhenua

Department of Internal Affairs

Recommendations

We recommend that you:

a)

EITHER

i)

agree to a media release announcing that work to

Yes / No

modernise the Charities Act 2005 is resuming

AND

ii)

note that the Department wil communicate to key

stakeholders and update the Department of Internal

Affairs website about the resumption of work fol owing

the media release

(recommended option)

1982

OR

iii)

agree that if a decision is made not to issue a media Act

release, the Department will begin to communicate to

Yes / No

key stakeholders and update the Department of Internal

Affairs website in the week beginning 29 March 2021;

b)

note the draft talking points provided to support the media release;

c)

notify the Minister of Revenue of your decision to resume this work;

Yes / No

and

Information

d)

note the importance of consultation to policy development, ahead

of legislative drafting, and the key stakeholders the Department wil

engage with

.

Official

the

under

Sela Finau

Policy Director

Released

Hon Priyanca Radhakrishnan

Minister for the Community

and Voluntary Sector

/

/

IN CONFIDENCE

Page 5 of 13

1982

Act

Information

Official

the

under

Released

Appendix A

Document 2

Te Tari Taiwhenua

Department of Internal Affairs

Appendix B: Draft talking points to support media release

Resuming work to modernise the Charities Act 2005

I am keen to deliver real world benefits to help charities in New Zealand

• In 2018 we began to look at how wel the Act is working. We gained extensive

information from public consultation in 2019 about the issues and opportunities that

charities face.

• There are more than 27,000 charities registered under the Charities Act. Charities spend

around $18 billion annually on charitable purposes and manage $65 billion in assets.

• Charities contribute hugely to the strength of communities across New Zealand – in1982

sports, the arts, health, and other countless activities that make a real difference to

people’s lives.

• Given the significance and contribution of the sector to communities, I am committed to

Act

achieving practical improvements and pass legislative amendments to modernise the Act

this term.

9(2)(f)(iv)

• 9(2)(f)(iv)

Information

• Stage one will lead to an amendment bill, and will look at:

o the obligations that charities have under the Act, including the annual reporting

requirements that small charities face, as well as the duties for officers of charities;

Official

o the regulator, in the sense of its powers, accountability and decision-making under

its current structure (being the independent Charities Registration Board and

the

Charities Services within the Department of Internal Affairs);

o the accessibility of appeals within the current structure of appeal bodies; and

o charities’ business activities and their accumulation of funds.

•

under

9(2)(f)(iv)

Importance of modernising the Charities Act

Modernising the Charities Act is important to maintain public trust and confidence in the

charities sector

Released

• The community sector is diverse and complex and forms a vital part in our society.

• Modernising the Charities Act by delivering some practical improvements will achieve

real world benefits for the community sector.

• Public consultation showed there are significant issues to address, like the compliance

burden smal charities face through reporting obligations.

IN CONFIDENCE

Page 7 of 13

Appendix A

Document 2

Te Tari Taiwhenua

Department of Internal Affairs

• The changes can be made without a first principles review because key concepts

underpinning the Act - particularly a registration, reporting and monitoring system for

charities - remain sound. 9(2)(f)(iv)

Targeted consultation approach taken for the upcoming policy development phase

I intend to take a targeted approach to consultation to engage with the key stakeholders

most likely to be affected

• Public consultation from 2019 provided a wealth of information about the issues and

opportunities that charities face, as well as the views of individuals, broader not-for-

profits and others.

• This forms a solid foundation to work from, and there is now an opportunity to maintain

1982

engagement with a more targeted scope of stakeholders as we develop policy options

for stage one of the work.

Act

• At a minimum, Select Committee consideration of the amendment bill will provide an

opportunity for al stakeholders, and the wider public, to participate again.

Topics for policy development in stage one

Topics that stage one policy development wil explore are:

1.

reporting requirements for small charities

• This issue will consider the appropriateness of the compliance burden

Information on small

charities, and its balance with the need for transparency in the use of charitable

funds.

2.

charities’ accumulation of funds and business activities

• Understanding the risk to charitable funds is important, where charities without

Official

explanation accumulate significant funds over time, distributing little or nothing to

charitable purposes. the

• It is also important to acknowledge that accumulating funds is often necessary for

a charity to save for a new community facility or to grow assets to benefit current

and future generations (including iwi and hapu charities that hold settlement

assets). under

• Business income is important to the financial sustainability of many charities.

• However, an issue that may need further consideration is, for example, the risk

that charitable funds are not used for charitable purposes (e.g. a charity putting

money into a failing business).

3.

duties of officers

• Charities register under the Charities Act, but often incorporate and have legal

Released

obligations under other legislation, like the Incorporated Societies Act.

• Consideration is required, as officers of charities may have very similar duties

under more than one piece of legislation.

4.

regulator’s powers, accountability and decision-making (under its current structure)

• Independence of the regulator’s decision-making was an important issue for

submitters during public consultation in 2019.

IN CONFIDENCE

Page 8 of 13

Appendix A

Document 2

Te Tari Taiwhenua

Department of Internal Affairs

• Options to strengthen the perceived independence and performance of the current

regulator will be considered, such as whether the current number of members for

the Charities Registration Board is appropriate.

5.

accessibility of appeals (within current structures)

• Currently charities can only appeal decisions taken by the Charities Registration

Board to the High Court. The time and significant cost involved can be a barrier to

appeals.

• Intermediate options for a more accessible appeals process will be considered.

1982

Act

Information

Official

the

under

Released

IN CONFIDENCE

Page 9 of 13

Appendix A

Document 2

Te Tari Taiwhenua

Department of Internal Affairs

Appendix C: Draft letter to the Minister of Revenue

[date] March 2021

Hon David Parker

Minister of Revenue

Update on resuming work to modernise the Charities Act

Tēnā koe David

1982

I am writing to update you on work to modernise the Charities Act 2005 that commenced

last term. I am resuming this work as a top priority in my portfolio. I also updated col eagues

Act

on the scope and sequencing last week at Cabinet Social Wellbeing Committee.

9(2)(f)(iv)

The first stage will lead to enactment of an

amendment bill this term covering many key areas that were publicly consulted on last term.

The first stage includes several issues you may have an interest in, such as:

• reporting requirements for small charities;

• charities’ accumulation of funds; and

Information

• charities’ business activities.

I intend to seek Cabinet approval on policy decisions for these issues in June 2021. I will

share my early views and consult with you as the policy proposals develop. As part of this

work, I will also be contacting you later in the year about appeals issues for charities, in your

Official

role as Attorney-General. If you have any questions in the meantime, please get in touch.

the

Nāku iti noa, nā

under

Hon Priyanca Radhakrishnan

Minister for the Community and Voluntary Sector

Released

IN CONFIDENCE

Page 10 of 13

1982

Act

Information

Official

the

under

Released

Appendix A

Document 2

Te Tari Taiwhenua

Department of Internal Affairs

Private foundations

Accumulation can be important to private foundations, who may have an

(a subset of Tier 1

interest in both the business and accumulation policy proposals. We

and 2 charities)

received submissions from Tier 1 and 2 private foundations on these issues

in public consultation.

We will look to engage with individuals involved in small charities. We will

Specific individuals

identify these individuals from public submissions in 2019, or from our work

Small Charities involved in small

to date. For example, we will likely approach Charmaine Brown, who was on

charities (to be

the Core Reference Group. Charmaine is a Chartered Accountant with

confirmed)

significant experience in the not for profit sector through her involvement

with several small charities and marae.

Charities Services and

Regulator

Charities Registration Charities Services and the Registration Board together comprise the

Board

regulator. They are well placed to share their insights on current workings.

1982

Charities’ registration status connects to their tax treatment. The

Government Response to the Tax Working Group’s final report was that

Act

Inland Revenue (IR)

business and accumulation issues would be considered as part of IR’s Tax

Policy Work Programme and through work to modernise the Charities Act.

As such, IR have a high interest in this work.

The External

Reporting Board

XRB set the reporting standards for not-for-profits and will want to input on

(XRB)

recommendations relating to reporting/transparency of funds.

MBIE will be advising on the recently introduced Incorporated Societies Bill.

Ministry of Business, The Bill affects the significant proportion of charities that are also

Government

Innovation and

incorporated societies. Information

Employment (MBIE)

Te Puni Kokiri will be interested on the impact of any proposal on Māori

Te Puni Kokiri (TPK)

charities/iwi/post settlement governance groups. They may be able to

and Te Arawhiti

provide advice on applying a te ao Māori lens to the business and

accumulation issues. We will also seek advice from Te Arawhiti on

Official

approaches to engaging with Māori and iwi for this project.

Ministry of Justice

(MoJ) and Crown Law The Ministry of Justice and Crown Law will have a key interest in any policy

the

Office

proposals regarding the appeals process.

Iwi, particularly mature post settlement groups such as Waikato Tainui and

Waikato Tainui

Ngāi Tahu, have established charitable arms and will have significant

Raupatu Lands Trust

interests in the business and accumulation topics. This is because these

under

and Group and Ngāi

groups tend to maintain substantial levels of assets and surplus funds and

Tahu Charitable

operate several businesses. This is to grow settlement funding and provide

Group

benefits for future generations. Donna Flavell was on the Core Reference

Iwi and Māori

Group and is Chief Executive of Te Whakakitenga o Waikato Incorporated.

Te Hunga Rōia Māori o Aotearoa provides te iwi Māori representation in the

Te Hunga Rōia Māori legal profession. The Society includes a significant membership of legal

o Aotearoa – The

practitioners, judges, parliamentarians, legal academics, policy analysts,

Māori Law society

researchers and Māori law students. The Society will provide valuable Māori

Released

perspective on our proposals.

Ian Murray is an academic/professor based in Western Australia who has

Ian Murray

published research on charity law and accumulation. His studies include

consideration of intergenerational distribution of charitable funds and other

related issues.

Academics

Michael Gousmett is an independent researcher who has written

Michael Gousmett

extensively about charitable business. He was featured in the New Zealand

Law Journal in March 2000, where he wrote about the transparency of

charitable business and provided examples.

IN CONFIDENCE

Page 12 of 13

Appendix A

Document 2

Te Tari Taiwhenua

Department of Internal Affairs

We may contact submitters from public consultation in 2019 that

Individual

demonstrated high interest and consideration of the impacts of the issues,

submitters

Individual submitters or unique views or expertise that are unlikely to be represented through our

other engagement.

1982

Act

Information

Official

the

under

Released

IN CONFIDENCE

Page 13 of 13

1982

Act

Information

Official

the

under

Released

1982

Act

Information

Official

the

under

Released

1982

Act

Information

Official

the

under

Released

1982

Act

Information

Official

the

under

Released

1982

Act

Information

Official

the

under

Released

1982

Act

Information

Official

the

under

Released

1982

Act

Information

Official

the

under

Released

1982

Act

Information

Official

the

under

Released

1982

Act

Information

Official

the

under

Released

Appendix A

Document 12

Te Tari Taiwhenua

Department of Internal Affairs

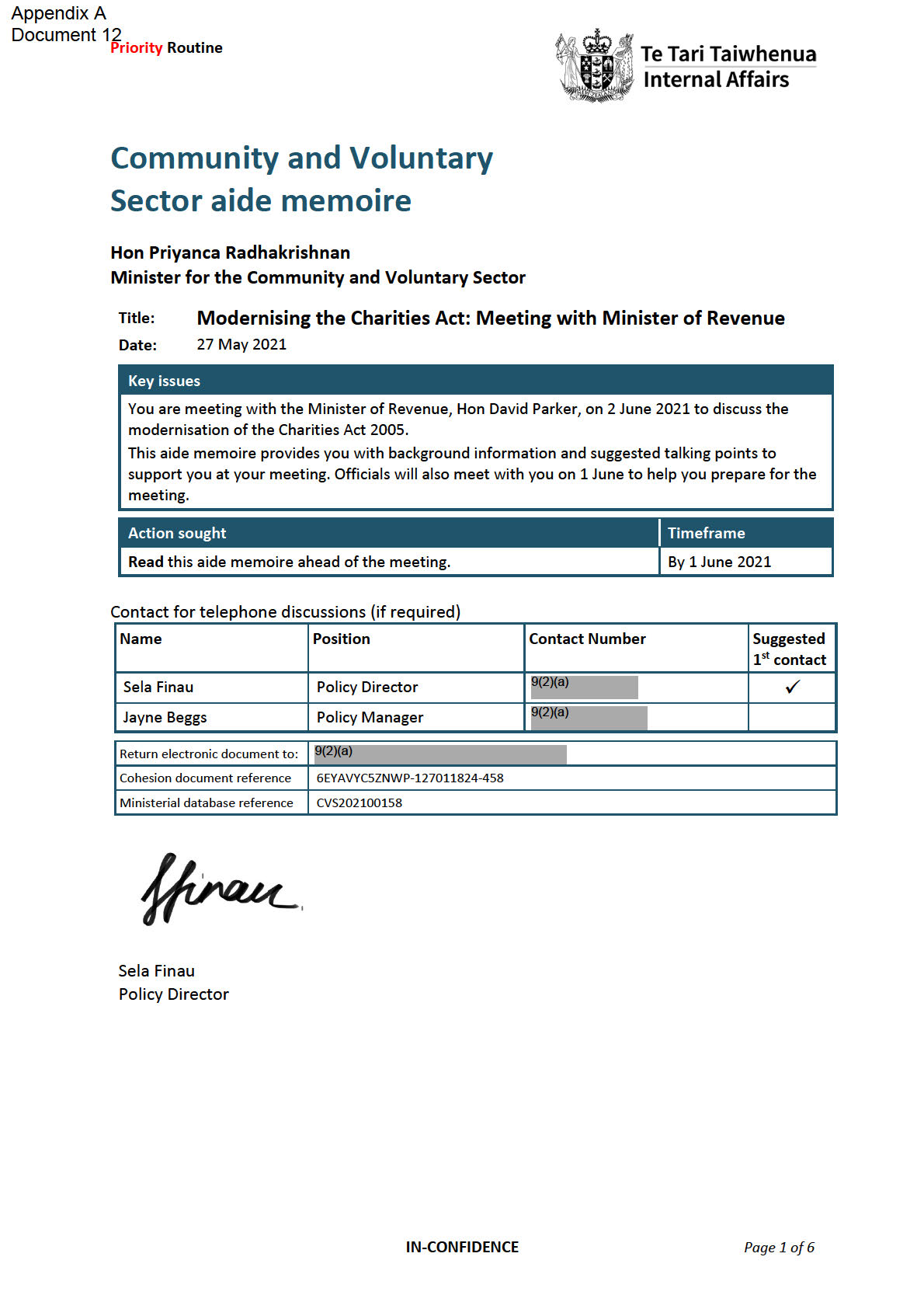

Purpose

1.

This aide memoire provides you with background information and talking points for

your meeting with the Minister of Revenue, Hon David Parker, on 2 June 2021.

Background

2.

One of the ways Government supports charities is through providing favourable tax

treatment. This includes income tax deductions and exemptions, tax concessions for

donations, GST concessions, and fringe benefit tax concessions for certain employees.

3.

You recently wrote to Hon Parker informing him that work had resumed on

modernising the Charities Act 2005 (the Act) as a top priority in your portfolio. You

identified topics that he may have interest in because of the relationship with the tax

1982

regime. These are:

3.1

Charities with business activities;

Act

3.2

Charities accumulating funds; and

3.3

Reporting requirements for small charities.

4.

The purpose of the meeting is to tell him the matters that are in scope of these topics,

and how they are progressing. You wil be supported at the meeting by Department

officials Sela Finau (Policy Director) and Jayne Beggs (Policy Manager).

5.

9(2)(f)(iv)

Information

Topics for discussion

Official

Charities with business activities

6.

Business activities are a well-established way for charities to raise funds. For example,

the

universities requiring tuition fees from students to advance education, or a hospice

using funds from an opportunity shop to provide palliative care to terminally ill

patients. For iwi charities, like Ngāi Tahu and Waikato Tainui, business operations are

considered critical for generating a sustainable financial return to support the long-

under

term economic and social development of their iwi members. Around 20 per cent of

registered charities may have business activities.1

7.

While we are not considering fundamental issues like whether charities should be able

to engage in business activities, we have identified that the regulator’s approach to

determining if a charitable business meets registration requirements is not transparent

enough. There is also a perception that the approach lacks legitimacy. We are currently

consulting wit

Released h targeted stakeholders on operational changes to address this.

8.

We are also exploring possible issues that may warrant amendments to the Act

including officers of charities using business activities for private profit, poor business

decisions putting charitable funds at risk, and whether consolidated financial reporting

obscures these problems.

1 Based on filed self-reported annual returns for 1 July 2019 – 30 June 2020. Includes charities that have

reported at least $100,000 for service trading income associated with trading operations, cost of trading

operations, and/or other revenue from exchange transactions. Refer CVS202100103 for more information.

IN-CONFIDENCE

Page 2 of 6

Appendix A

Document 12

Te Tari Taiwhenua

Department of Internal Affairs

9(2)(f)(iv)

9.

9(2)(f)(iv)

10. 9(2)(f)(iv)

1982

11. 9(2)(f)(iv)

Act

Charities accumulating funds

12. The topic on charities accumulating funds stems from the Government’s response to

the Tax Working Group recommendations in 2019. The Tax Working Group took the

view that to qualify for tax exemption, accumulated funds should be used for

Information

charitable purposes. However, the Group also recognised that charities have many

valid reasons to accumulate funds.

13. We recently advised you that we consider there is a problem with a lack of

transparency around if, when and how fundraising charities will distribute

accumulated funds to charitable purpose. Fundraising charities are different to other

Official

charities in that they only further charitable purpose once they distribute funds. There

is evidence of considerable variance in funding distribution by some fundraising

charities, but no clarity on why this

the is the case.

14. We are currently consulting with targeted stakeholders on what they think about this

problem and a range of draft options to address it. These options are:

14.1 no change;

under

14.2 guidance from Charities Services on furthering charitable purpose;

14.3 reporting more on accumulation in the annual return;

14.4 requiring a distribution plan; and

14.5 setting minimum distribution requirements.

Released

9(2)(f)(iv)

15. 9(2)(f)(iv)

IN-CONFIDENCE

Page 3 of 6

Appendix A

Document 12

Te Tari Taiwhenua

Department of Internal Affairs

16. 9(2)(f)(iv)

The appeals topic may also be of interest

17. You noted in your letter to Hon Parker that you would also be in touch about the

appeals topic due to his role as Attorney-General. He may wish to discuss where this

work is heading.

18. We recently provided background information to you on the Act’s appeals framework,

noting that we are looking at:

1982

18.1 what decisions are available for appeal under the Act;

18.2 what type of appeal may be appropriate; and

Act

18.3 what body should hear the appeals.

19. We got feedback from the sector on issues relating to the appeals framework as part

of the 2019 consultation. Feedback was about the inability to appeal decisions made

by Charities Services, the inability to provide both new evidence and oral evidence at

appeals hearings, and the inaccessibility of the High Court for most charities, given the

significant costs involved. We wil brief on you on problem definitions and options to

test with targeted stakeholders on these matters in mid-June.

Information

Next steps

20. Continued coordination and engagement with the Minister of Revenue will be

important as you progress this work, particularly if tax policy matters affecting

charities are also progressed under the Revenue portfolio. You may wish to meet with

Official

Hon Parker again, during consultation on the draft Cabinet paper, to discuss his views

on the proposals.

the

Talking points

21. Suggested talking points for the meeting are provided in

Appendix A.

under

Released

IN-CONFIDENCE

Page 4 of 6

Appendix A

Document 12

Te Tari Taiwhenua

Department of Internal Affairs

Appendix A: Suggested talking points

Overview of work to modernise the Charities Act

•

I am keen to ensure progress is made to modernise the Charities Act and intend to

deliver an amendment bill this term.

•

I have directed officials to address issues that will have practical impacts on the day-to-

day running of charities, rather than looking at more fundamental matters.

•

I want to support charities, so they can get on with their good work, but I also want to

ensure that they are transparent to the public and other interested parties.

•

The topics of focus are reporting requirements for small charities, charities

accumulating funds, charities engaging in business activities, obligations of charities,

1982

the regulator, and the appeals mechanism.

•

I recognise the strong connection between the Charities Act and the tax system a

Act nd

am keen to discuss how things are tracking on areas of mutual interest.

Charitable business

•

Business activities are a well-established way for charities to raise funds – I am not

seeking advice on whether charities should be able to engage in business activities.

•

Looking at practical matters, my officials have advised me that there is a lack of

transparency around what the regulator considers when registering charitable

Information

businesses. Officials have just finished consulting with targeted stakeholders on how

that could be addressed.

•

Officials have also advised me there may be some issues with charities using business

for private profit or making business decisions that risk charitable funds. I note the Tax

Working Group considered this in the context of pr

Official ivate foundations.

•

I will keep you up to date on how work on private benefit and conflicts of interest in

charities progresses and wil be ke

the en to hear your views.

Charities accumulating funds

•

Accumulating funds is an important way for charities to do good work. However, for

some charities, the need to

under accumulate is less clear.

•

My officials have advised me that it is not clear that fundraising charities, like

charitable businesses and private foundations, will distribute their accumulated funds.

•

Officials have just finished consulting with targeted stakeholders on options to

improve transparency of fundraising charities.

•

There are a range of draft options on the table which I have not yet made decisions on.

Released

•

The options are status quo, guidance from Charities Services on furthering charitable

purpose, more reporting on accumulation, requiring a distribution plan, or setting

minimum distribution requirements.

•

I am awaiting advice from officials on a preferred option following targeted

stakeholder engagement. I wil let you know where I land on that and seek your views.

IN-CONFIDENCE

Page 5 of 6

Appendix A

Document 12

Te Tari Taiwhenua

Department of Internal Affairs

Next steps

•

Officials will advise me on preferred options for the business and accumulation topics

now that targeted engagement has been completed.

•

My officials will continue to work closely with your officials, and I will keep you up to

date on how work is progressing ahead of taking proposals to Cabinet in September.

•

You will have further opportunity to input when I consult on the Cabinet paper. I

would be keen to talk with you again in September to get your views on the proposals.

•

I note you may consider changes to tax policy settings that could impact charities - it

will be important for us to remain coordinated.

Back pocket talking points on the appeals work if raised by Hon Parker

1982

•

Officials have advised me there may be issues with:

Act

o only being able to appeals decisions of the Charities Registration Board (and

not Charities Services);

o that new evidence and oral evidence cannot be heard at appeals hearings; and

o that appealing to the High Court is inaccessible for most charities given the

costs involved.

•

I am awaiting further advice from officials and look forward to getting your input on

this.

Information

Official

the

under

Released

IN-CONFIDENCE

Page 6 of 6

1982

Act

Information

Official

the

under

Released

1982

Act

Information

Official

the

under

Released

1982

Act

Information

Official

the

under

Released

1982

Act

Information

Official

the

under

Released

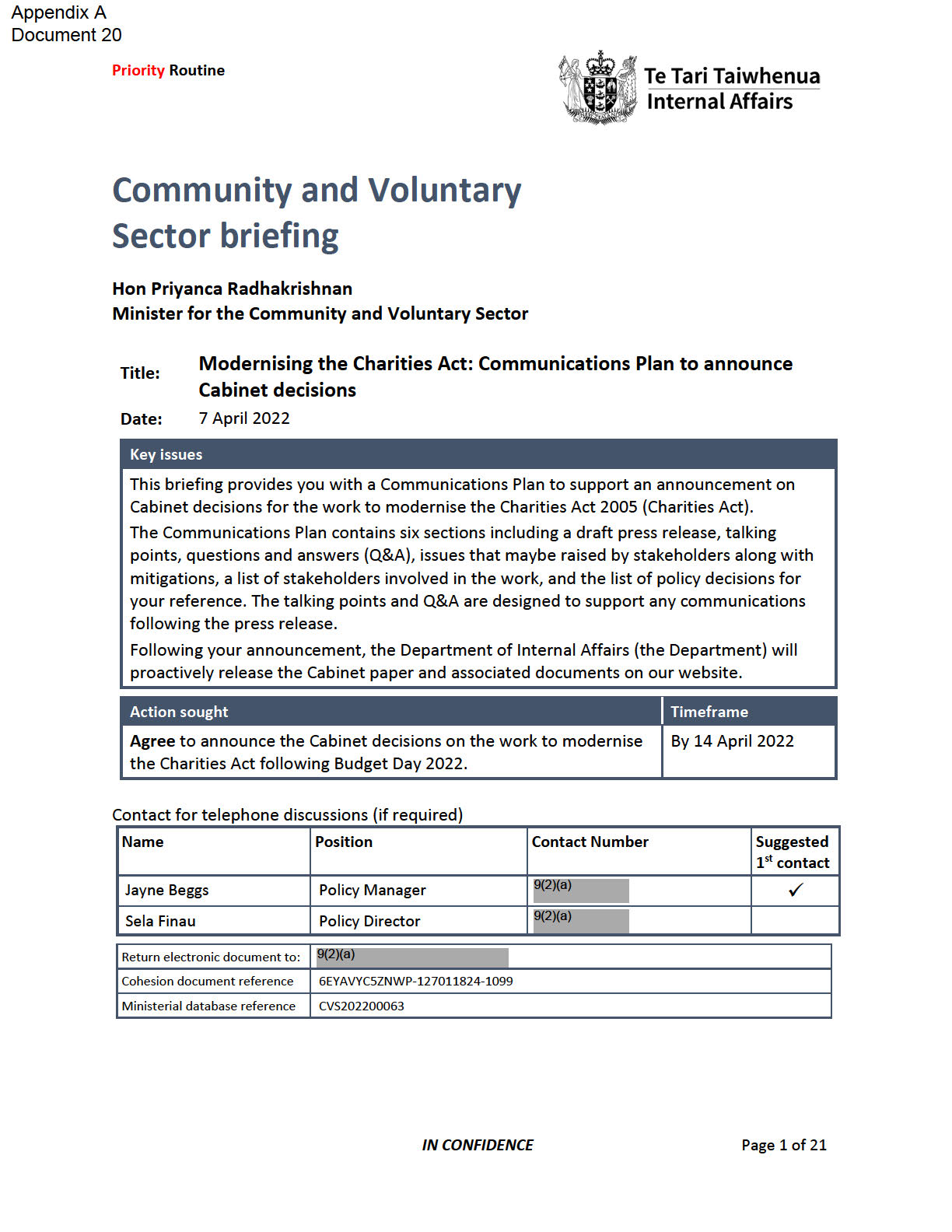

Appendix A

Document 20

Te Tari Taiwhenua

Department of Internal Affairs

Purpose

1.

This briefing provides you with a Communications Plan (refer

Appendix A) to support you

to announce Cabinet decisions on the work to modernise the Charities Act 2005. The Plan

contains the fol owing elements:

1.1

a draft press release;

1.2

talking points;

1.3

questions and answers;

1982

1.4

issues that may be raised by stakeholders and suggested mitigations;

1.5

a list of stakeholders involved in the work; and

Act

1.6

the list of policy decisions to modernise the Charities Act.

Background

2.

Cabinet agreed to the policy decisions for the work to modernise the Charities Act on

14 February 2022 [CAB-22-MIN-0021 refers]. The Department have since briefed you on

potential announcement approaches in February 2022 (CVS02200019 refers) and about

proactive release of the Cabinet paper and associated documents in March 2022

Information

(CVS202200040 refers). The Department is now providing you with a Communications

Plan that reflects our likely success in the Budget 2022 process.

3.

The Department considers that the work to modernise the Charities Act is of greatest

interest to the charitable and not-for-profit sectors. Therefore, we are providing a

Communications Plan that will suit these stakeholders. As part of the plan, we have liaised

Official

with relevant agencies (Inland Revenue and Ministry of Business, Innovation and

Employment) to ensure consistency of communications. Some potential Q&A related to

those agencies’ work is provided in the attached plan.

the

Communications Plan

4.

The Department recommends that you make your announcement via press release

fol owing Budget Day (19 May 2022). We advise liaising with the Minister of Finance and

under

the Prime Minister’s Office to confirm timing. When your press release goes live, we will

update the Department’s website with information about the policy decisions along with

the proactively-released Cabinet paper and associated documents.

5.

The talking points and Q&A within the plan are intended to support additional

communications on the announcement. The list of policy decisions is also attached for

your reference when communicating the policy decisions. The Communications and Policy

Released

teams at the Department wil also support your office with media inquiries as needed.

The Department will share your announcement through our social media channels and

we suggest that you use your social media channels to enhance the distribution of your

message.

IN CONFIDENCE

Page 2 of 21

Appendix A

Document 20

Te Tari Taiwhenua

Department of Internal Affairs

Potential stakeholder risks and mitigations

6.

The objective of the work to modernise the Charities Act was to ‘encourage and support

charities to continue their trusted and vital contribution to community wel being, while

ensuring that contribution is sufficiently transparent to interested parties and the public’.

The policy decisions provide a balanced package that meet this objective, with a focus on

practical improvements. However, the balanced approach means there will be people

who may disagree with some of the decisions.

7.

The potential issues that people may raise along with suggested mitigations are detailed

1982

in Section 4 of the Plan. In Section 5, we have also provided you with a comprehensive list

of stakeholders that were involved in the engagement process and are likely to be

interested in the announcements. There is a risk some people will feel their views hav

Act e

not been heard, or that they did not have the opportunity to contribute. This can be

mitigated by emphasising the Select Committee stage is another opportunity for

feedback.

8.

To avoid the potential for incorrect reporting of this work among the charitable sector,

we can also provide an update through the Charities Services newsletter to ensure

accurate information reaches these stakeholders. The newsletter is sent to all registered

charities and any additional interested parties who have signed up to receive the

Information

information.

Next steps

9.

Subject to your availability and agreement from your colleagues, we suggest an

announcement on the work to modernise the Charities Act is made in late May 2022

Official

fol owing Budget 2022 announcements.

the

under

Released

IN CONFIDENCE

Page 3 of 21

Appendix A

Document 20

Te Tari Taiwhenua

Department of Internal Affairs

Recommendations

10. We recommend that you:

a)

Agree to announce the Cabinet decisions on the work to modernise

Yes/No

the Charities Act fol owing Budget Day 2022; and

b)

Note the Department will proactively release the Cabinet paper and

associated documents fol owing the announcement and update our

website with supporting information.

1982

Act

Sela Finau

Policy Director

Information

Official

Hon Priyanca Radhakrishnan

the

Minister for the Community

and Voluntary Sector

/

/

under

Released

IN CONFIDENCE

Page 4 of 21

Appendix A

Document 20

Te Tari Taiwhenua

Department of Internal Affairs

Appendix A: Communications Plan

Announcing decisions on modernising the Charities Act

Section 1: Draft press release

Charities and communities to benefit from changes to the Charities Act

1982

Making it easier to help the community is the focus of changes being made to the Charities Act, says

Community and Voluntary Sector Minister Priyanca Radhakrishnan.

“Charities are a valued part of our society, and the past two years have crystal ised why we need t

Act o take

care of them in the same way they take care of our communities,” says Minister Radhakrishnan.

The newly announced changes wil include introducing increased transparency on accumulated funds,

reduced reporting requirements for very small charities, clarifying the role of officers of charities, and a

more accessible judicial appeals body.

“We are working to help support charities to thrive while also ensuring trust and confidence by the

public in our charitable sector.”

Information

For very small charities, the benefit will come from an easing of financial reporting requirements to the

regulator.

“I want to lighten the burden on our smallest charities, who are often the ones volunteering to provide

important services in our communities.

Official

“This will lessen their operating costs and al ow volunteers to spend more time doing the mahi they

love. It is estimated that 12 percent of all registered charities will benefit from this proposal.”

the

Minister Radhakrishnan is also proposing to improve transparency and fairness by requiring larger

charities to be more transparent to the public about why they have accumulated funds such as cash,

assets or other resources.

“It is well established that a number of New Zealand’s largest charities have significant accumulated

under

funds they use to achieve their charitable purpose. There is an interest in these funds and what they are

used for, so we want to make this information more readily available.

“Transparency builds trust, and the public need to be able to trust charities to be responsible with their

tax-free income.”

These increased transparency efforts will also extend to the responsibilities of the regulator.

The Charities Registrat

Released ion Board will be required to publish all decline and deregistration decisions and

provide a clear process for formal objections.

Charities will be able to appeal a wider range of decisions and where appeals are made to significant

decisions, they wil now be made to an expanded Taxation Review Authority instead of the High Court,

which was legally complex, time-consuming, and expensive, disadvantaging smaller charities.

IN CONFIDENCE

Page 5 of 21

Appendix A

Document 20

Te Tari Taiwhenua

Department of Internal Affairs

The new appeals process will be less formal, allow charities to self-represent, and have more relaxed

rules of evidence. The timeframe for lodging an appeal will be extended from 20 days to two months.

“I want to make it easier and less costly for charities to appeal decisions. It is important that our system

doesn’t just work for those who have the resources to navigate it. It must provide the same service and

the same access for everyone,” says Minister Radhakrishnan.

To enable this, $2.6 million is being made available as part of Budget 2022.

These changes are expected to come into effect in 2023 fol owing amendments to the Charities Act. The

1982

public wil have an opportunity to provide feedback through the Select Committee process.

ENDS

Act

Background

• The Charities Act provides a registration, reporting and monitoring system for entities that carry out

charitable purposes, and therefore has a clear public benefit.

• The system helps approximately 28,000 registered charities to retain the public’s trust and

confidence that charitable funds are being managed appropriately. While registering for charitable

status is voluntary, it brings benefits, including eligibility for tax exemptions and funding

opportunities.

Information

• The charitable sector is diverse, ranging from large iwi organisations, churches, and education

providers to local providers of social services, toy libraries, and sports clubs.

• Charities contribute greatly to New Zealand society, spending over $19 billion over the past financial

year.

• They benefit a range of communities by providing services that directly respond to community need.

Official

This was highlighted during the COVID-19 pandemic when charities provided a wide variety of

support such as food parcels and emergency accommodation.

• Since the Charities Act was introduced in 2005, the sector’s operating environment has changed.

the

Crown entity reforms resulted in the disestablishment of the Charities Commission in 2012. The

Commission’s functions were transferred to the Charities Registration Board and the Chief Executive

of Te Tari Taiwhenua Department of Internal Affairs.

• Changes to reporting requirements in 2015 required charities to report to financial reporting

under

standards specified by the External Reporting Board (a Crown entity) for greater transparency and

consistency.

• Changes to reporting requirements for very small charities will complement the work being done by

the External Reporting Board to reduce and simplify the existing Tier 4 standard for small charities.

Released

IN CONFIDENCE

Page 6 of 21

Appendix A

Document 20

Te Tari Taiwhenua

Department of Internal Affairs

Section 2: Talking points

Cabinet has approved policy proposals for work to modernise the Charities Act

•

In 2018, Cabinet agreed to a review of the Charities Act to with the aim of modernising the Act.

•

Public consultation occurred in 2019 on a range of issues, however, work was put on hold in 2019

due to COVID-19 and resumed in late 2020.

•

Policy development on a range of topics was completed at the end of 2021. In February 2022,

Cabinet approved the policy proposals.

1982

•

I expect to introduce the Charities Amendment Bil to Parliament this year with the aim of passing

the Bil by 2023. The public wil have an opportunity to provide feedback through the Select

Committee process.

Act

The charitable sector is diverse and makes a great contribution to New Zealand society

•

The sector is diverse and includes sports clubs, churches, providers of education, and social

services. There are about 28,000 registered charities in New Zealand.

•

Over half of charities in New Zealand are smal and often volunteer run.

•

Charities benefit communities by providing services that respond to community need. This was

demonstrated during the COVID-19 pandemic when charities provided support such as food

parcels and emergency accommodation.

Information

•

Charities spent over $19 billion over the last financial year.

Significant changes since the Charities Act’s commencement in 2005 prompted the Modernising the

Charities Act work programme

•

The Charities Commission was disestablished in 2012 and its functions were transferred to the

Official

Charities Registration Board and the Chief Executive of the Department of Internal Affairs,

delegated to Charities Services (the charities regulator).

the

•

From 2015, charities were required to report to financial reporting standards specified by the

External Reporting Board.

The objective of the work programme is to deliver real world benefits to charities

•

The aim of the Modernising the Charities Act work is to support charities to continue contributing

under

to community wellbeing while ensuring public transparency.

•

The Government considers the fundamentals of the Charities Act (which is a registration,

reporting and monitoring system for charities) to be sound.

•

I am proposing practical improvements to address challenges charities face. These challenges

include the compliance burden, inaccessibility of the current appeals framework, and lack of

clarity of the role of charities’ officers.

Released

Improving the accessibility of appeals and expanding the decisions available for appeal

•

Currently many charities, particularly smaller ones, find the High Court appeal process to be

inaccessible due to the legal complexity and costs involved.

IN CONFIDENCE

Page 7 of 21

Appendix A

Document 20

Te Tari Taiwhenua

Department of Internal Affairs

•

I propose to use the Taxation Review Authority to hear appeals under the Charities Act. The

Authority will provide greater accessibility and the updated appeals framework will allow charities

to self-represent, reducing costs.

•

The appeals process wil become less formal with more relaxed rules of evidence so that more

evidence can be potential y considered.

•

I also seek to expand the range of decisions that can be appealed. This change wil include

significant decisions of the Chief Executive of Internal Affairs.

•

Further, I propose to extend the timeframe for lodging an appeal to two months making it easier

for small charities that might not meet frequently.

1982

Increasing the regulator’s transparency, accountability and decision-making processes Act

•

I propose to require the charities regulator to publish all decline and deregistration decisions and

provide a clear process for charities to object to significant decisions.

•

Additionally, I propose to extend the timeframe for submitting information to the regulator from

20 working days to two months, increasing the Charities Registration Board’s composition from

three to five members, and require the Department of Internal Affairs to consult with the

charities sector about guidance material.

•

Increasing the number of Board members to five will improve the diversity of the Board and

address potential quorum and conflict of interest issues.Information

•

These changes acknowledge that many charities are volunteer run and need time to engage in the

decision-making process. These changes also support participation in the charities system, provide

greater clarity, and allow charities to focus on their important mahi.

Requiring larger charities to report reasons for accumulated funds

Official

•

Larger charities (tiers 1, 2 and 3) will be required to report the reasons for their accumulated

funds, to provide clarity on why funds are held to help improve public trust and confidence.

•

Charities Services will co-design with iwi changes to the annual return form so that te ao Māori

the

views of accumulation are reflected.

Easing reporting requirements for very small charities

•

Currently, very small charities have disproportionate reporting requirements relative to the level

under

of transparency and accountability required.

•

I am proposing to exempt very small charities from the External Reporting Board’s financial

reporting standards. Very small charities will still be required to file an annual return containing

basic financial information.

•

This will balance transparent reporting while reducing the compliance burden faced by very small

charities. Around 12 percent of all registered charities will benefit from this exemption. The

exemption threshold wil be set through regulations.

Released

Improving the compliance and enforcement function

•

This work will make three improvements to the compliance and enforcement function for

charities.

IN CONFIDENCE

Page 8 of 21

Appendix A

Document 20

Te Tari Taiwhenua

Department of Internal Affairs

•

I propose to make explicit the currently implicit obligations for charities to remain qualified for

registration.

•

The definition of serious wrongdoing will be clarified to include an offence punishable by at least

two years imprisonment.

•

I propose to enable the Charities Registration Board to disqualify an officer for serious

wrongdoing or a significant/persistent breach of obligations,

without deregistering the charity.

Four changes wil be made to clarify the role of an officer of a charity

•

I intend to clarify the role of an officer as someone who supports the charity to meet its

1982

obligations and holds responsibility for governing the charity.

•

I propose to amend the definition of officer to include anyone with significant influence regardless

Act

of the type of charity.

•

I propose that charities must review their rules document every year to encourage a closer look at

their governance arrangements.

•

I propose to update the disqualifying factors for becoming an officer to include financing of

terrorism offences and one officer in a charity must be 18 or over (people can currently hold

officer positions from the age of 16).

•

These four changes will improve the accountability and governance of charities and produce

better alignment with other legislation that charities might be governed by such as the Companies

Information

Act and Trusts Act.

Official

the

under

Released

IN CONFIDENCE

Page 9 of 21

Appendix A

Document 20

Te Tari Taiwhenua

Department of Internal Affairs

Section 3: Questions and answers

General Q&A

What is the purpose of this work?

The objective of modernising the Charities Act is to support charities to continue their contribution to

community wellbeing while ensuring sufficient public transparency. I am making practical improvements

to address the challenges that charities face.

1982

What prompted the Modernising the Charities Act work programme?

There has been significant change since the Charities Act was introduced in 2005. We have seen changes

Act

in the wider operating environment for charities, the disestablishment of the Charities Commission, and

charities being required to report to financial standards set by the External Reporting Board.

What is the charitable sector like in New Zealand?

The sector is diverse with around 28,000 registered charities in New Zealand across the width and

breadth of community services. Over half of charities in New Zealand are small and are often volunteer

run.

How do charities contribute to New Zealand society?

Information

Charities provide services which respond to community need. During the COVID-19 pandemic, charities

provided wide-ranging support such as food parcels and emergency accommodation. Charities also

spent over $19 billion over the last financial year.

How wil the changes help charities to support their communities?

Official

This is a balanced approach; I propose to make it easier for charities to do their work while considering

the need for accountability in managing tax-free funds. We have focused on practical improvements

the

that will make the day to day running of charities easier, especially our smallest charities.

What wil change for charities in practice?

The changes I am proposing will have practical benefits for charities and the communities they serve.

under

Some changes are operational and will be implemented over the coming year, while other changes

require amendments to the Charities Act.

Additional detail:

I propose to reduce the burden of financial reporting for our smallest charities, which means more time

focusing on their important mahi. Large charities will now share why they have accumulated funds,

giving more context to how their financial position contributes to the goals of the charity and its

Released

community.

All charities will have a better idea of how the regulator makes decisions affecting them, be more

involved in regulatory decision-making, and not have to go to the High Court to chal enge a decision,

which wil save time and money.

IN CONFIDENCE

Page 10 of 21

Appendix A

Document 20

Te Tari Taiwhenua

Department of Internal Affairs

Who did you consult with to develop the policy changes?

Targeted engagement with key stakeholders in 2021 built on a solid foundation of feedback from public

consultation in 2019. The targeted engagement was representative of the sector and included a Core

Reference Group, the Charities Sector group, iwi and others.

Timeframes

When do you expect the Charities Act to be amended?

I intend to introduce a Charities Amendment Bill to Parliament this year and will aim to pass the Bill in

1982

2023.

Why has the work to modernise the Charities Act taken so long?

Act

Work was interrupted and placed on hold due to COVID and the need to redeploy resources.

Fundamental matters – out of scope

What happened with al the other issues raised in the 2019 public consultation?

The changes I have proposed will make practical improvements. I was keen to focus on these areas to

make a difference to how charities operate in the short to medium term.

Information

Additional detail:

Other more fundamental matters raised in the public consultation, like how te ao Māori principles could

be considered in the Act, where the line is for political advocacy by charities, and the definition of