11 May 2022

Max Shierlaw

[FYI request #19091 email]

Tēnā koe Max

Request for Information – Local Government Official Information and Meetings Act

(LGOIMA) 1987

We refer to your official information request dated 8 April 2022 for:

“… all correspondence, meeting notes and any other official information relating to the

Philip Jones report on pages 228-257 of the Council agenda papers of 7 May 2020.

Please include any draft reports or part of the full report, either in draft or final,

received by the Council preceding the published report, submitted by Philip Jones or

Philip Jones & Associates or by staff or colleagues of Philip Jones and any

correspondence, file notes, meeting notes or any other official information relating to

communication between Jones and the Council about those draft reports.

Please also include any internal emails within the Council about the Jones report, both

drafts and final report, including discussions about the preparation of the Council

agenda papers and officers' report pertaining to the Jones report.”

Attached is a copy of the

final report from Philip Jones and communications relating to it.

Private information has been withheld from these documents under section 7(2)(a) of the

LGOIMA. The final report can be located on the Hutt City Council’s websit

e here. Copies of the

draft reports and some associated communications are withheld under section

7(2)(f)(i) of the LGOIMA, to maintain the effective conduct of public affairs through the free

and frank expression of opinions.

You have the right to seek an investigation and review by the Ombudsman of this response.

Information about how to make a complaint is available at

www.ombudsman.parliament.nz or

freephone 0800 802 602.

Please note that this letter may be published on the Council’s website.

Nāku noa, nā

Susan Sales

Senior Advisor, Official Information and Privacy

4 May Mayor, DM, CE, Jarred, Caryn

Out of Scope

Budget - email to all staff going out, budget paper for review. Phillip Jones report. One

pager from Jo regarding the report. Requested by Mayor and subcommittee chairs. Touch

base before finalised. Phillip Jones to attend?

Out of Scope

under the Local Government Official Information and Meetings Act

Released

From:

From: Bruce Robertson s7(2)(a)

Sent: Saturday, 2 May 2020 8:41 am

To: Jenny Livschitz <[email address]>

Cc: Philip Jones s7(2)(a)

Subject: Re: Hutt City report

Act

Hi Jenny

Please find attached the requested bio. Apologies for the slightly dramatic photo - any formal one

suggests I am younger, haha!

And well done on getting Phil’s engagement in to this area. From past involvement with Hutt, I think

the sort of review that Phil can provide has been really needed. To date I think Hutt has been

somewhat insular to broad developments in the sector - and Phil’s work will assist you as a

leadership team forge an upgraded path.

Kind regards

Bruce

Bruce Robertson

Director

RBRobertson Ltd

s7(2)(a)

Lo

On 1/05/2020, at 2:53 PM, Jenny Livschitz <[email address]> wrote:

under t

under the Local Government Official Information and Meetings Act

Hi Bruce

ed

A quick note to thank you for the work that you’re doing on this report with Philip. Really

appreciated!

I’m wondering if you have a brief bio about yourself. I would like to include this alongside the report

Released

when it goes to the Mayor.

Thanks again , and have a great weekend.

Jenny

s7(2)(f)(i)

under the Local Government Official Information and Meetings Act

Released

From:

From: Jo Miller

Sent: Saturday, 2 May 2020 12:44 PM

To: Campbell Barry; CNB; Tui Lewis; Simon Edwards; Deborah Hislop

Subject: Fwd: Hutt City report

Please see attached , Bruce Robertson, former Assistant Auditor General’s biography as

promised . Bruce has peer reviewed the Philip Jones report which I have shared with you .

Philip Jones bio will come on seperate email . Thanks Jo

Act

Sent from my iPad

Ngā mihi nui

Jo Miller Chief Executive

Hutt City Council, 30 Laings Road Private Bag 31912, Lower Hutt 5010, New Zealand

T 04 570 6773

M 027 213 7550

W www.huttcity.govt.nz

Follow me on Twitter : @jomillernz

IMPORTANT: The information contained in this e-mail message may be legally privileged or confidential. The information is

intended only for the recipient named in the e-mail message. If the reader of this e-mail message is not the intended recipient,

you are notified that any use, copying or distribution of this e-mail message is prohibited. If you have received this e-mail

message in error, please notify the sender immediately. Thank you.

Begin forwarded message:

Date: 2 May 2020 at 8:40:51 AM NZST

To: Jenny Livschitz <[email address]>

Lo

Cc: Philip Jones s7(2)(a)

Subject: Re: Hutt City report

Hi Jenny

under t

under the Local Government Official Information and Meetings Act

ed

Please find attached the requested bio. Apologies for the slightly dramatic photo - any formal

one suggests I am younger, haha!

And well done on getting Phil’s engagement in to this area. From past involvement with

Released

Hutt, I think the sort of review that Phil can provide has been really needed. To date I think

Hutt has been somewhat insular to broad developments in the sector - and Phil’s work will

assist you as a leadership team forge an upgraded path.

Kind regards

Bruce

Bruce Robertson

Director RBRobertson Ltd

s7(2)(a)

Act

Lo

under t

under the Local Government Official Information and Meetings Act

ed

Released

Bruce Robertson

RBruce Robertson Ltd

Act

Bruce is an established governance and risk expert within the local government sector, with active

membership of audit and risk committees since leaving the Office of the Auditor-General in 2015. He

has been confirmed as an independent member of 12 Audit and Risk Committees1 including Auckland,

Hamilton City, Tauranga City and Bay of Plenty Regional Councils for the 2019-22 local body

triennium..

In most of these roles, as well as leading and participating in the work of the committees and

governance of the councils , his work has included a substantial development dimension in supporting

the growing understanding and maturity of risk management within the council itself. This work has

included workshops on risk (especially to establish a council’s highest level risks – the “top 10” –

through to seminars with a council’s risk management and ‘risk champions’).

Lo

As an independent member, he is required from time-to-time, to deal with sensitive issues in support

of council’s governance. Generally, these are confidential but have involved such matters as staff

conflicts of interests and sensitive ratepayer concerns.

Aligned to these roles, Bruce convened a series of risk and assurance seminars nationally in 2018 to

under t

under the Local Government Official Information and Meetings Act

develop elected member and senior management’s understanding of development of effective audit

and risk committees. In February 2020, he will contribute in SOLGM’s Risk Management Forum.

ed

Bruce also works as an independent reviewer of organisations and significant council activities. Recent

review roles include “health checks” on the overall capability and capacity of entities to “perform and

Released

deliver” (DIA, Review of Kaikoura and Hurunui District Councils, 2015; North Canterbury Fish and

1 Chair of Gisborne District Council, Invercargill City Council, Otorohanga District Council, Southland District

Council, Thames Coromandel District Council, Waipa District Council, Waitomo District Council; Deputy Chair of

Bay of Plenty Regional Council, Far North District Council, Hamilton City Council; independent member of

Auckland Council.

Game Council, Review of aspects of governance and management, 2018 and Central South Island Fish

and Game Council, Management of conflicts of interest; 2019) and review of the capability and

capacity of key functions (Hastings District Council, Water operations post-Havelock North, 2017 and

2018; Christchurch City Council, Loss of ‘secure’ status for its water supply, 2018).

Recently he completed reviews of Okara Park (Whangarei District Council/Northland Events Centre

Trust, 2019), events management issues (Tauranga City Council management of Soper Reserve, 2019)

Act

and commercial investments (Invercargill City Council, investment in the Don St premises, 2019).

Bruce is assisting with risk management of the refurbishment and rebuild of Yarrow Stadium (Taranaki

Regional Council) and has recently worked with Whakatane District Council on a review of their

internal management functions to ensure Council is fit for the future challenges it will face and can

help the community with capturing and maximizing the opportunities developing in the ‘Eastern Bay’.

His governance and management engagements have varied across maturity reviews of approaches to

risk (Porirua City Council, Risk Maturity Assessment, 2019), providing governance support to decision-

makers (Kaikoura District Council; 2018 and on-going), guiding and supporting financial management

reform and change management (Invercargill City Council, 2019), “Finance 101” seminars

(Whakatane District Council 2019; LGNZ’s finance module for new councillors, 2019) through to

facilitating strategic priorities seminar (Whangarei District Council, 2019).

Bruce is part of the assessors for Local Government New Zealand’s CouncilMARK assessment

programme, and he is a recognised facilitator, and presenter of governance and strategy workshops

Previously he was Assistant Auditor-General, Local Government in the Office of the Auditor-General.

Through his time in this role, he was heavily involved in the implementation of the planning, financial

management and accountability provisions of the Local Government Act 2002 as well as their

amendment.

He is a graduate of the University of Otago (Commerce and History) and is a Fellow Chartered

Accountant (FCA) of Chartered Accountants of Australia and New Zealand. He maintains an active

programme of self-development, as expected of a professional member of the Institute.

Bruce is Queenstown-based, where he lives with Pip, his wife. They have three adult children.

Lo

under t

under the Local Government Official Information and Meetings Act

ed

Released

Chief Executive’s statement to Council meeting 7 May 2020

Out of Scope

ct

RelOut of Scope

Out of Scope

t

I draw your attention to the 22 page report in your agenda today by Philip Jones from PJ &

Associates which has been peer-reviewed by Bruce Robertson, former Assistant Auditor

General. The Mayor requested that the report be commissioned and I am pleased that we

have done so. The report notes the following in respect of the proposed financial strategy we

have pressed pause on:

This is an improvement on the existing strategy and there are further improvements to be

made, in particular by defining the need for increased funding for renewal expenditure and

considering the impact of a balanced budget and noting the intention to increase revenues

over time to “balance the budget”.

In conclusion, the proposed financial strategy and the approach taken in the development of

the proposed amendment to the 2018-2028 Long term plan is a significant improvement.

The reason for this improvement from the existing strategy is by clearly explaining the need

to increase expenditure and move to a tighter balanced budget test consistent with good

practice. This wil assist in forming a sound and financially prudent approach for the

development of the 2021-2031 Long term plan.

under the Local Government Offi

Out of Scope

R

From:

From: Jo Miller <[email address]>

Sent: Saturday, 2 May 2020 10:19 am

To: Jenny Livschitz <[email address]>

Cc: Philip Jones s7(2)(a)

Subject: Re: Final report

Fantastic , thanks both

Ngā mihi nui

Jo Miller Chief Executive

Hutt City Council, 30 Laings Road Private Bag 31912, Lower Hutt 5010, New Zealand

T 04 570 6773

M 027 213 7550

W www.huttcity.govt.nz

Follow me on Twitter : @jomillernz

IMPORTANT: The information contained in this e-mail message may be legally privileged or confidential. The information is

intended only for the recipient named in the e-mail message If the reader of this e-mail message is not the intended recipient,

you are notified that any use, copying or distribution of this e-mail message is prohibited. If you have received this e-mail

message in error, please notify the sender immediately. Thank you.

On 2/05/2020, at 10:04 AM, Jenny Livschitz <[email address]> wrote:

Thanks again Philip

Jo I have bios from Philip and Bruce which could go alongside these. I’ll forward these onto you next

ocal Government Official Information and Meetings Act

I can pull it together in these memo.

Sent from my iPhone

On 2/05/2020, at 9:44 AM, Jo Miller <[email address]> wrote:

u

Thank you so much Philip for doing this at speed .

Could I possibly trouble you to put in the exec summary that it has been prepared by you & peer

reviewed by Bruce with details of your joint stature ?

Many thanks . I really appreciate all that you have done . Jo

Released

Ngā mihi nui

Jo Miller Chief Executive

From:

From: Deborah Hislop <[email address]>

Sent: Saturday, 2 May 2020 2:43 pm

To: Jo Miller <[email address]>; Campbell Barry <[email address]>;

Simon Edwards <[email address]>; Tui Lewis <[email address]>; CNB

<[email address]>

Cc: Jenny Livschitz <[email address]>; Caryn Ellis <[email address]>;

Jarred Griffiths <[email address]>

Subject: RE: Final report

Thank you Jo and Jenny for the bio and the financial report. Both very good reading.

Cheers

Deborah

From: Jo Miller

Sent: 02 May 2020 12:38

To: Campbell Barry; Simon Edwards; Tui Lewis; CNB; Deborah Hislop

Cc: Jenny Livschitz; Caryn Ellis; Jarred Griffiths

Subject: Fwd: Final report

Dear All

Please find attached independent financial report from Philip Jones , peer reviewed by Bruce

Stevenson . This accords with our conversations over the last couple of weeks. I will forward

Philip and Bruce bios under seperate email . Campbell we can discuss at our Monday

morning catch up the best way to get this into the wider council arena etc .

Thanks all , happy to discuss.

Jo

Sent from my iPad

Ngā mihi nui

Jo Miller Chief Executive

Hutt City Council, 30 Laings Road Private Bag 31912, Lower Hutt 5010, New Zealand

T 04 570 6773

M 027 213 7550

W www.huttcity govt.nz

Follow me on Twitter : @jomillernz

under the Local Government Official Information and Meetings Act

Released

IMPORTANT: The information contained in this e-mail message may be legally privileged or confidential. The information is

intended only for the recipient named in the e-mail message. If the reader of this e-mail message is not the intended recipient,

you are notified that any use, copying or distribution of this e-mail message is prohibited. If you have received this e-mail

message in error, please notify the sender immediately. Thank you.

Begin forwarded message:

From: Philip Jones s7(2)(a)

Date: 2 May 2020 at 9:39:10 AM NZST

To: Jenny Livschitz <[email address]>, Jo Miller

<[email address]>

Subject: Final report

Good morning

Attached is the final report. This has ben a challenge to ensure the right message is given without

seriously criticising the previous approach.

Bruce’s final comments are:

Professionally we say it will be more robust - and that is defendable simply on the grounds of the

tighter test (in line with good practice) and without us having actually say it is the right answer at

this point.

Kind regards Philip Jones

under the Local Government Official Information and Meetings Act

Released

From: Jenny Livschitz <[email address]>

Sent: Monday, 4 May 2020 2:11 pm

To: Jo Miller <[email address]>

Cc: Caryn Ellis <[email address]>

Subject: Extra report

This is what I have put together quickly – Ok?

under the Local Government Official Information and Meetings Act

Released

1

07 May 2020

Hutt City Council

04 May 2020

1

07 May 2020

Hutt City Council

04 May 2020

File: (20/388)

Report no:

Council financial strategy

DECISION MAKING

CHECKLIST

This checklist is designed to assist report writers and decision makers to more easily

understand and comply with the obligations of the Local Government Act, whilst providing

a legal record of how the process was followed.

There are specific obligations in the Local Government Act 2002 for Council to consider a

range of factors when making decisions. The Decision Making Checklist is applicable to

all reports

seeking a decision to SLT, Council, Community Committees or Community

Boards.

What is the decision you are seeking in your report? No decision. Noting report

only.

under the Local Government Official Information and Meetings Act

Who is responsible for making this decision? Finance & Performance Committee

Check Council’s

Terms of Reference the

Delegations Register and

Functions and

Delegations for Community Boards 2016-2019

Released

LEGISLATIVE REQUIREMENTS

Does this decision fit the purpose of local government by

enabling local decision-making and action by, and

on behalf of, the communities; and promoting the social, economic, environmental, and cultural well-

being of communities in the present and for the future ☒

DEM15-3-1 - 20/388 - Council financial strategy

Page 1

2

07 May 2020

Does your report show how this decision

Not applicable

yes

achieves this purpose (see above) in the most

cost efficient way?

Does your report state whether this is a

significant decision, and if so, on what basis it is Not applicable

yes

significan

t? Refer to significance policy

Does the report show that I have considered

how this decision will affect people in the

Not applicable

yes

community?

OPTIONS

Comments

Have I considered

all practicable options in my

Not applicable

yes

report?

Does the report show that I have assessed the

costs and benefits (or pros and cons) of each of Not applicable

yes

those options?

FINANCIAL CONSIDERATIONS

Comments

Does my report show how this decision would

be funded?

yes

(If you answer ‘existing budgets’ please specify

the budget year).

Have I considered the short term and long term

financial implications of this decision in my

Not applicable

yes

report?

Do I need to prepare a business case with my

no

Not applicable

report?

CONSISTENCY WITH OTHER COUNCIL PLANS

Comments

Does the report recommend a decision that

would substantially deviate from current plans

(including the Annual or Long Term Plan, The

Not applicable

no

District Plan, asset management plans or

under the Local Government Official Information and Meetings Act

policies or strategies); or

Does the report recommend a decision that

supplements or replaces any current plans or

Not applicable

yes

policies?

Released

CONSULTATION

Comments

Should this issue be consulted on?

Refer to the Not applicable

Yet to be determined

Community Engagement Strategy

DEM15-3-1 - 20/388 - Council financial strategy

Page 2

3

07 May 2020

If so, have I identified a consultation plan and

identified who I need to consult with?

Not applicable

no

Refer to the Community Engagement Strategy

Am I aware of any existing community views

(including the Youth Council) regarding this

Not applicable

no

decision?

Should I consult with Māori on this decision?

Refer to Community Engagement Strategy and

Not applicable

All community if required

Contact the Kaitakawaenga Kaupapa Maori

OTHER CONSIDERATIONS

Comments

Which other staff members within Hutt City

Yes

Legal, policy

Council should I talk about this decision with?

How would I communicate this decision?

N/A

(Consider both internally and externally)

Have I made a plan for the implementation of

Not applicable

yes

this decision?

Does this report require specialist input (for

example, advice from the legal team, the

Not applicable

yes

Communications team, Human Resources,

Finance, or Risk Management)?

Health and Safety: Are there any health & safety

implications or risks to others in making this

decision? If so have these risks been assessed Not applicable

no

in accordance with the Health & Safety at Work

Act 2015 and what actions may be taken to

reduce the risk of harm?

Purpose of Report

under the Local Government Official Information and Meetings Act

1. For Council receive the report and advice in relation to the Financial Strategy

developed for the proposed amendment to the 2028-2028 Long Term Plan.

Released

Recommendations

That Council:

(i) note the report on the Financial Strategy, attached as Appendix 1 to the

report;

DEM15-3-1 - 20/388 - Council financial strategy

Page 3

4

07 May 2020

Background

2.

At the request of the Mayor a report has been prepared on the proposal to

amend the 2018-2028 Long term plan and the existing financial strategy, refer

Appendix 1. The report was prepared independently by Phillip Jones of PJ &

Associates, and has been peer reviewed by Bruce Robertson of RBruce

Robertson Ltd. Their bios are attached as Appendix 2 and 3 to this report.

3. Extract from the report

In conclusion, the proposed financial strategy and the approach taken in the

development of the proposed amendment to the 2018-2028 Long Term Plan is a

significant improvement. The reason for this improvement from the existing strategy

is by clearly explaining the need to increase expenditure and move to a tighter

balanced budget rest consistent with good practice. This will assist in forming a sound

and financially prudent approach for the development of the 2021-2031 Long Term

Plan.

Legal Considerations

4. The relevant legislation is referenced in the report, attached as Appendix 1.

Financial Considerations

5. There are no further financial considerations apart from those referenced in

the report, attached as Appendix 1.

Appendices

No. Title

Page

1

Appendix 1 - Report on Council financial strategy

2

Appendix 2 - Philip Jones bio

3

Appendix 3 - Bruce Robertson bio

under the Local Government Official Information and Meetings Act

Author: Jenny Livschitz

Chief Financial Officer

Released

Approved By: Jo Miller

Chief Executive

DEM15-3-1 - 20/388 - Council financial strategy

Page 4

5

07 May 2020

under the Local Government Official Information and Meetings Act

Released

DEM15-3-1 - 20/388 - Council financial strategy

Page 5

From:

From: Jo Miller <[email address]>

Sent: Wednesday, 15 April 2020 7:58 am

To: Jenny Livschitz <[email address]>

Subject: Re: LG depn requirements final after comments.doc

Helpful Jenny , thanks

Sent from my iPad

Ngā mihi nui

Jo Miller Chief Executive

Hutt City Council, 30 Laings Road Private Bag 31912, Lower Hutt 5010, New Zealand

T 04 570 6773

M 027 213 7550

W www.huttcity.govt.nz

Follow me on Twitter : @jomillernz

IMPORTANT: The information contained in this e-mail message may be legally privileged or confidential. The information is

intended only for the recipient named in the e-mail message. If the reader of this e-mail message is not the intended recipient,

you are notified that any use, copying or distribution of this e-mail message is prohibited. If you have received this e-mail

message in error, please notify the sender immediately. Thank you.

On 14/04/2020, at 5:05 PM, Jenny Livschitz <[email address]> wrote:

Hi

FYI a paper written by Philip in 2011 and published by LGNZ. OAG also reviewed paper ahead of

publication.

A few extracts

under the Local Government Official Information and Meetings Act

-

“

In the local authority context depreciation is especially important as it ensures that today’s

ratepayers pay their fair share of consumption of the assets. Depreciation is therefore a vital

component of the process of setting rates and charges.”

Released

-

The LGA provides local authorities with a set of exceptions where they may depart from the

requirements of the balanced budget. However, these exceptions do not provide a licence for

any local authority to depart at will from a balanced budget (e.g. the political decision to hold

back on amount of depreciation a council may “fund” to keep rates down in an election

year). They require careful thought and analysis of the funding needs and the overall financial

strategy to best deliver sustainable community services over the long term.

-

As a result of revaluing assets depreciation will increase. However, as the purpose of

depreciation is to charge the people who are using the asset their share of that asset, if the

value has increased, in theory the people using the asset should pay a greater share. If the

value has increased so do the future renewal costs.

Cheers

Jenny

From: Philip Jones [mailto:s7(2)(a)

]

Sent: Tuesday, 14 April 2020 4:06 PM

To: Jenny Livschitz

Subject: LG depn requirements final after comments.doc

<LG depn requirements final after comments.doc>

under the Local Government Official Information and Meetings Act

Released

Depreciation in the Local Government context

There has been much comment over the requirement for the local government sector to account for

and fund depreciation. The purpose of this paper is to put context around the requirements to

include depreciation in the accounts and budgets of local authorities.

The legislation and accounting standards

Section 100 subsection 1 of the Local Government Act 2002 (LGA) states:

A local authority must ensure that each year’s projected operating revenues are set at a level

sufficient to meet that year’s projected operating expenses.

The requirement to set operating revenues at a level sufficient to meet operating expenses includes

depreciation because section 1111 (LGA) obliges councils to follow generally accepted accounting

practice (GAAP), which defines ‘operating expenses’. As depreciation is an operational expense it

must be included with other operational costs including interest when a council sets its operating

revenue.

What the legislation requires is that councils ensure that projected revenues are at least equal to

projected operational expenditure including depreciation, unless it is prudent to do otherwise. The

cash or funding generated by the revenue may be used for present capital needs (including

renewals), debt reduction or set aside for future capital needs. This helps ensure sound asset

management practice and continuity of service to future generations.

Purpose of depreciation

There is confusion over the purpose of depreciation as many believe that the purpose of

depreciation is to provide for the replacement of an asset. In fact depreciation reflects the use or

consumption of the service potential implicit in as asset. GAAP defines depreciation as follows:

Depreciation is the systematic allocation of the depreciable amount of an asset over its useful

life.

As depreciation reflects the consumption of the asset over its useful life, there are two critical

factors in determining the expense. The first is the cost or revalued amount, and the second is the

useful life. It is therefore not related to the physical wearing out, for example able to sit on a park

bench in year one (or flush toilet) is the same benefit to a ratepayer as being able to sit on park

bench in year 15, 16, and 17 ( or flush toilet).

under the Local Government Official Information and Meetings Act

The purpose of depreciation is not to provide for the replacement of the asset(s), however this may

be an intended or unintended consequence as many councils have assumed that depreciation is for

the replacement of an asset.

Released

The approach to depreciation in the local government context is no different than the commercial

sector when depreciation is accepted as a legitimate operating expense; the only real difference is

1 All information that is required by any provision of this Part or of Schedule 10 to be included in any plan, report, or other

document must be prepared in accordance with generally accepted accounting practice if that information is of a form or

nature for which generally accepted accounting practice has developed standards.

the useful lives of local government infrastructure assets are significantly longer than many assets

used in the commercial sector.

Funding or cash implications of depreciation

In the local authority context depreciation is especially important as it ensures that today’s

ratepayers pay their fair share of consumption of the assets. Depreciation is therefore a vital

component of the process of setting rates and charges.

As depreciation, is a non-cash item of expenditure, the inclusion of the depreciation expense with

the total operational expenditure will result in a funding surplus from operations. It is then a

council’s decision as to how that surplus funding should be allocated. Broadly there are four

options:

I.

Repay debt

II.

Pay for renewal expenditure

III.

Acquire new assets

IV.

Transfer to a reserve for the replacement or future renewal of an asset.

While these are the most common options, there is no reason why a council can not apply another

option if it believes that is a prudent2 use of council’s funds.

Generally a council should consider all options across its different activities and then that decision

should be made as part of its Financial Strategy.

Exceptions to the Balanced Budget Requirement

Much of the concern around section 100 has arisen from the notion that this section requires the

‘funding of depreciation’ which has been interpreted by many as the transfer of the depreciation

expense to a specific reserve or accumulation of cash to be used either for the replacement of an

asset or for the loan repayment associated with the acquisition of that asset. In fact, there is no

direct legal requirement to “fund depreciation” as many have assumed. However, there is a

requirement to be prudent in the setting of funding levels.

Prudence

What the Act does is create a rebuttable presumption that forecasting a surplus is financially

prudent.

Financial prudence is not defined in the Act. But the legislation provides some insight into what is

intended by this phrase. In the standard dictionary sense prudence means ‘careful’, ‘sensible’, or

under the Local Government Official Information and Meetings Act

‘habit of acting with careful deliberation’. A local authority that does not operate a balanced budget

and has been cavalier in its treatment of the above matters may well be acting imprudently.

There is one other statutory reference that provides an indication of Parliament's view of what is

considered financially prudent. Section 102 specifies certain financial policies which are required to

Released

be adopted by every council. The legislative rationale for requiring these policies is 'in order to

provide predictability and certainty about sources and levels of funding'. This can be seen as an

2 Section 101 requires a council to manage its revenues, expenses, assets, liabilities, investments, and general financial

dealings prudently and in a manner that promotes the current and future interests of the community

indication that predictability and certainty of funding levels and sources was seen as an element of

being financially prudent.

Application of the concept of prudence in relation to establishing the level of operating revenue for

the purposes of LTP forecasting/budgeting would require the local authority to set operating

revenue at such a level that applies an unbiased assessment in areas of judgement based on the best

available information. The most significant area of judgement that impacts the level of forecast

operating expense, and therefore the level of operating revenue needed to enable council to

adequately fund the level of service represented by the forecast operating expenses, is the useful

life of the numerous components comprising the infrastructure assets of the Council. Other

judgements included in the determination of operating revenue include the level of revenue sources

other than rates in any period.

under the Local Government Official Information and Meetings Act

Released

Section 100 Exemptions

Section 100 is in two parts, the first part relates to the requirement to have a balanced budget as

discussed above and the second part relates to the exemptions of where councils can decide not to

have a balanced budget and the criteria in which that decision is made.

(1) A local authority must ensure that each year’s projected operating revenues are set at a

level sufficient to meet that year’s projected operating expenses.

(2) Despite subsection (1), a local authority may set projected operating revenues at a different

level from that required by that subsection

if the local authority resolves that it is

financially prudent to do so, having regard to—

(a) the estimated expenses of achieving and maintaining the predicted levels of service

provision set out in the long-term plan, including the estimated expenses associated

with maintaining the service capacity and integrity of assets throughout their useful life;

and

(b) the projected revenue available to fund the estimated expenses associated with

maintaining the service capacity and integrity of assets throughout their useful life; and

(c) the equitable allocation of responsibility for funding the provision and maintenance of

assets and facilities throughout their useful life; and

(d) the funding and financial policies adopted under section 102.

The LGA provides local authorities with a set of exceptions where they may depart from the

requirements of the balanced budget. However, these exceptions do

not provide a licence for any

local authority to depart at will from a balanced budget (e.g. the political decision to hold back on

amount of depreciation a council may “fund” to keep rates down in an election year). They require

careful thought and analysis of the funding needs and the overall financial strategy to best deliver

sustainable community services over the long term.

The legislation requires council to consider all four criteria not just one of them. In summary the

subsections refer to:

i.

(a)the estimated expenses of achieving and maintaining the predicted levels of service;

ii.

(b)the projected revenue available to fund i.e. having the cash available at the right

time;

iii.

(b)maintaining the service capacity and integrity of assets throughout their useful life;

not just in the 10 years of the LTP, but for the whole life;

iv.

(c)the equitable allocation of responsibility for funding to ensure the revenue is fairly

charged; and

under the Local Government Official Information and Meetings Act

v.

(d)the funding and financial policies which ensures that there is certainty of the sources

of funding required.

Within the Act, the balanced budget test in section 100 focuses on deficits. While an operating

deficit may indicate that the local authority’s levels of service and/or financial operations are

unsustainable and result in current costs being shifted to future generations, a surplus does not

Released

necessarily mean that the LTP is financially prudent.

One method a number of councils are using to meet the provisions of section 100 is to use the

average of future renewal expenditure to set revenue rather than the forecast depreciation expense.

In these cases the depreciation is still recognised as an expense but not used for the setting of

revenue. This is sometimes known as the Long Run Average Renewal approach (LRARA). This

approach averages the renewal expenditure for the next 25-35 years and uses this in the calculation

of funding requirements. However, LRARA cannot be used to calculate the depreciation expense as

it is forward-looking and, this does not comply with the accounting concept of consumption. But

more importantly if depreciation is calculated correctly then over the life cycle of an asset (ignoring

the impacts of inflation and revaluation) the depreciation expense and LRARA based funding need

calculation would be of the same or similar values.

Basis of Depreciation

As depreciation reflects the consumption of the asset over its useful life, there are two critical

factors in determining the expense.

Cost or revalued amount

While the cost of an asset is relative easy to ascertain, because councils’ assets provide benefit for a

long period of time (50-100 years) councils revalue to reflect the fair value (book value) which for all

infrastructural assets is based on Depreciation Replacement Cost (DRC) This is the replacement cost

based on the replacement value of an equivalent asset, less the accumulated depreciation.

As a result of revaluing assets depreciation will increase. However, as the purpose of depreciation is

to charge the people who are using the asset their share of that asset, if the value has increased, in

theory the people using the asset should pay a greate share. If the value has increased so do the

future renewal costs.

Useful life

One of the most difficult tasks in assessing the depreciation expense is assessing the asset’s useful

life. While there are standard useful lives and often manufacturers give a minimum useful life, there

are a number of factors that dictate the ultimate useful life. However, these can be grouped into

either condition based or performance based. Condition relates to the physical attributes of the

asset, while performance relates to the ability of the asset to meet the level of service requirements.

The range of useful lives are reflected in each council's accounting policies which are included within

the financial statements and these can vary significantly from council to council. It is not uncommon

for one council to have a standard useful life of 80 years and another council to have a standard

useful life of 160 years for the same asset because of different aspects, including construction

methods, environmental constraints, topography and soil types. The change in useful lives results

appropriately in a different depreciation expense.

under the Local Government Official Information and Meetings Act

Summary

The core question when considering a forecast operating deficit is whether current ratepayers are

Released

paying an appropriate level of rates bearing in mind the services they are receiving. This will typically

involve deeper analysis of the apparent position to identify whether, for example, the deficit arises

from a mismatch between the period in which expenses and revenues are recognised in terms of

GAAP.

From: Philip Jones s7(2)(a)

Sent: Friday, 1 May 2020 3:40 pm

To: Jenny Livschitz <[email address]>

Subject: RE: Bio

Attached

Kind regards

Philip Jones

s7(2)(a)

From: Jenny Livschitz <[email address]>

Sent: Friday, 1 May 2020 14:57

To: Philip Jones s7(2)(a)

Subject: Bio

Hi Philip

I have to confess that I can’t remember where I filed your bio that you gave me previously. Could

you please resend.

thanks

Ngā mihi

Jenny Livschitz Chief Financial Officer

Hutt City Council, 30 Laings Road, Private Bag 31912, Lower Hutt 5040, New Zealand

T 04 570 6736,

M 027 238 5980,

W www.huttcity.govt.nz

under the Local Government Official Information and Meetings Act

Released

s7(2)(a)

Introducing Philip Jones CA of PJ & Associates

Philip Jones has been consulting to a variety of Local

Government related organizations since June 2007.

Philip specialises in financial management and

strategy, risk and asset management, financial

policies and financial governance. He sits as an

independent on a number of local authority’s Audit

and Risk committees both as a member and a chair.

Between 1993–2007 Philip was the Chief Financial Officer and Group

Manager Revenue and Finance for Western Bay of Plenty District Council

(WBOPDC), Tauranga.

Areas of expertise

Philip has a wide range of financial skills and because of his unique

understanding of both asset and financial management, he brings a unique

understanding of what can be complex issues. Key areas of expertise

include:

Facilitator in Financial Governance providing an understanding of

finance for elected members

Development and review of Funding & Financial policies including

Treasury, Revenue & financing, Rating and Development & Financial

contributions policies

Development and review of Financial Strategies which are unique

to each particular Council

Long Term Plans (LTP) development: from the planning stages to

the detailed knowledge of the financial & reporting requirements

under the Local Government Official Information and Meetings Act

Risk Management Strategies

Audit & Risk Committee - member and facilitator

Funding evaluations for various capital expenditure requirements

Released

Review of finance functions

Asset Management Plans (AMP): review of financial requirements of

asset management plans and the linkage to other processes and

documents.

Major work completed since June 2007

Auckland Council – Mayor’s Office

• Development of procurement strategy and policy

Association of Local Government Rating NZ Inc - (On Going)

• Facilitate and develop the annual seminar for rates officers

Bay of Plenty Regional Council

• Assistance with LTPs including Financial strategy

• Assistance with Development of long-term (50 years) funding

model for rivers and drainage

• Assistance with Funding Impact Statement and Rates resolution

compliance including Rotorua Lakes Targeted Rates

Carterton District Council – (On Going)

• Independent Chair of Audit & Risk Committee

Chatham Islands Council (On Going)

• Provision of external advice on reporting requirements and

assistance with LTPs including Financial strategy

Kaikoura District Council

•

Revenue Streams Health Check

•

Subsequent financial advice including updating of Treasury

policy and jointing Local Government Funding Agency

Kaipara District Council

•

Financial Health and Sustainability Audit

•

Subsequent financial advice

• Assistance with identifying options to resolve rating

irregularities

Kawerau District Council – (On Going)

•

Independent Chair of Audit & Risk Committee

Hawkes Bay Regional Council

•

Development of long-term (50 years) funding model for rivers

and drainage

under the Local Government Official Information and Meetings Act

•

Review of Delivery of service as required by section 17A LGA

•

Assistance with Funding Impact Statement and Rates resolution

compliance

Horowhenua District Council – (On Going)

Released • Independent Chair of Finance, Audit & Risk Committee

Local Government Commission

• Identify the impacts of uniform land value and capital rating for

the general rates across the three Wairarapa councils

Introducing Philip Jones Page 2 of 6

Local Government New Zealand

• Development and presenter for;

o

New Elected Members,

o

Financial Governance 101,

o

Financial Governance 201, and

o

Audit & Risk Committees - Roles & Functions

• Development of best practice guide for Audit & Risk Committees

• Development and review of specific financial reports and

requirements

•

Masterton District Council – (On Going)

•

Independent Chair of Audit & Risk Committee

•

NAMS (New Zealand Asset Management Support)

• Development and presenter of a variety of training courses on

asset management and levels of service.

Napier City Council – (On Going)

• Development of risk management strategy

• Assistance in developing LTP and associated policies including

Development & Financial contributions

• Provision of strategic financial advice

•

Society of Local Government Managers

• Development and presentation of financial integration for LTPs,

application of prudent financial management and balanced budget

principles

• Development of rewrite of “More Dollars & Sense” for 2015 –

2025 LTPs

• Presenter at a number of coursers and seminars

Ruapehu District Council – (On Going)

• Independent Chair of Audit & Risk Committee

under the Local Government Official Information and Meetings Act

South Taranaki District Council

• Assistance with LTPs including Financial strategy

• Assistance with completion of annual report

Released • Facilitator for the Revenue and Financing Policy Review

Thames Coromandel District Council

• External appointee to Audit & Risk Committee

Wairoa District Council

Introducing Philip Jones Page 3 of 6

• External appointee to Finance, Audit & Risk Committee

• Operational Review – Financial compliance

• Ongoing financial and risk advice

Wanganui District Council

• Facilitator for the Revenue and Financing Policy Review

Western Bay of Plenty District Council

• Completed financial contributions for Omokoroa structure plan

• Strategic financial advice

• Preparing revised financial contributions for District Plan review

for public consultation February 2009 including a review of

submissions and final planners report.

• Assistance with LTPs

Whakatane District Council

• Completed finance review

• Revenue and Financing Policy Review

• Assistance with LTPs including Financial strategy

• Assistance with completion of annual report and annual plans

• Assistance with funding options

Acting General Manager Finance – (Part time)

Whangarei District Council

• External appointee to Audit & Risk Committee

Other clients include:

• Canterbury Earthquake Recovery Authority

• Department of Internal Affairs

• Dunedin City Council

• Environment Canterbury

• Fiji Road Authority

• Hamilton City Council

under the Local Government Official Information and Meetings Act

• Hastings District Council

• Kapiti Coast District Council

• Matamata-Piako District Council

•

Released Nelson City Council

• Northland Regional Council

• New Plymouth District Council

• Rangitiki District Council

• Tasman District Council

Introducing Philip Jones Page 4 of 6

• Tauranga City Council

• Southland District Council

• South Wairarapa District Council

• Stratford District Council

• Tararua District Council

• Various Regional Councils - review of rate setting requirements

under the Local Government Official Information and Meetings Act

Released

Introducing Philip Jones Page 5 of 6

Details of experience prior to 2007

Since 1993, Western Bay of Plenty District Council has seen a considerable amount

of growth, (population increased from 28,000 to 42,000). During this time Philip

was the senior manager responsible for all finance functions. He was responsible

for the development of funding models to provide long term funding of four new or

upgraded sewage plants, and three water expansions. He provided advice on the

funding and accounting treatment for the first roading Performance-Based Contract

which included both operations & maintenance, together with any capital

expenditure, including renewals. During that time, WBOPDC external debt has

increased from $4 million to approximately $80 million. During that time, Philip was

instrumental in developing the Treasury policy and procedures to ensure one of the

lowest costs of interest in the country.

From 1997 to 2007 Philip has been a lead member of the

Society of Local

Government Managers (SOLGM) Financial Working Party. The working party

was set up to provide advice and develop best practice in New Zealand for Financial

Management. In this role he has spoken at a significant number of conferences and

seminars in both New Zealand and Australia, and was invited to present four

sessions to Financial Managers in South Africa run by Applied Fiscal Research Centre,

an adjunct of the University of Cape Town.

He was also SOLGM’s financial representative on

NAMS (Now

New Zealand Asset

Management Support previously

National Asset Management Steering

Group). Resulting from this, Philip has peer reviewed three manuals produced by

NAMS – International Infrastructure Management Manual (IIMM) 2000, the IIMM

Australia/New Zealand 2002 update and the Valuation & Depreciation Guidelines,

including the update for International Financial Reporting Standards (IFRS). He was

also on the executive for NAMS.

In 2005/2006, Philip was also the SOLGM representative on the

Joint Officials

Group on the review of funding for Local Authorities.

Also, in 2005/2006 he led the development of the JIGSAW guide on development of

Long Term Council Community Plan (LTCCP now Long Term Plan or LTP).

This guide which is best practice, was a joint venture between SOLGM & NAMS,

bringing together all the requirements of an LTCCP including asset management,

financial reporting and policy development.

New Zealand Local Authorities are required to comply with all General Accepted

Accounting Practice (GAAP). When the New Zealand Institute of Accountants issued a

new Accounting standard on Fixed Assets (Plant Property & Equipment), Philip

represented the public sector in reviewing submissions, and made recommendations

to the

Financial Reporting Standards Board (FRSB) as to any changes.

With the new Local Government Act 2002 he has been a member of the

Know How

Working Party on planning and reporting for the implementation of the new act.

Whilst working for WBOPDC, Philip has undertaken

funding policy review work for

other councils in New Zealand, and assisted a large council in South Australia with the

under the Local Government Official Information and Meetings Act

integration of financial and asset management.

Philip has been the Project Manager for the review and amendment of

Financial

Contributions under the Resource Management Act that were made operative in

2003 without challenge.

Released

Western Bay of Plenty was an early complier with the 1996 amendment to the Local

Government Act (known as the No 3 amendment). Philip was the Project Manager to

ensure Council’s compliance. This included development of Council’s first

Assets

Management Plans, Funding & result of this he has continued to develop

knowledge of the linkages between finance and asset management.

Introducing Philip Jones

Page 6 of 6

From:

From: Philip Jones s7(2)(a)

Sent: Tuesday, 28 April 2020 11:04 am

To: Bruce Robertson s7(2)(a)

Cc: Jenny Livschitz <[email address]>

Subject: Hutt City report

Hi

Attached is my report for your peer review.

One you have read it, do you want to give me call to agree next steps?

Both Jo Miller (CEO) and Jenny Livschitz (CFO) have seen it.

Kind regards

Philip Jones

s7(2)(a)

under the Local Government Official Information and Meetings Act

Released

Kia ora all,

Just under three weeks ago I requested (through the Chief Executive) a report about our existing

financial strategy (adopted in 2018), and the changes proposed in the Long Term Plan Amendment

and how that proposed budget was put together.

I asked that an expert independent third party prepare a report on the different approaches. As you

will be aware, there have been suggestions that the proposed new way of setting our budget is

wrong, and was misleading Councillors.

I made this request after discussing the issue with the chairs of our standing committees, and

unanimous agreement that the issue needed to be settled so we could all focus on moving forward.

I have attached this report for your information. This will also be on the agenda for Thursday as a

noting report.

I also attached the bios of Philip Jones (author) and Bruce Robertson (peer reviewed) for your

information. I suspect you wouldn’t find many others in the Local Government financial

management sector who are more qualified.

Personally I found the report very reassuring that we are on the right path with what was in our

proposed LTP amendment, and it reinforces the quality of the advice given to us by Council Officers

around the setting of our budget.

Kind Regards,

Campbell

Mayor

under the Local Government Official Information and Meetings Act

Released

s7(2)(a)

1 May 2020

Report to Hutt City Council on the proposal to amend the 2018-2028 Long term plan and

existing financial strategy

Executive summary

In March the Council agreed to go out to the public to consult on a proposed 7 9 % rates

increase in order to invest in key infrastructure, and put the city on a more secure and

sustainable financial footing going forward.

This report considers the existing 2018-2028 Long term plan which includes the existing

financial strategy was adopted by Council in June 2018 and the proposed amendment to the

2018-2028 Long term plan which was considered in March 2020 together with the proposed

amended financial strategy.

Council, through its proposed amendment to the 2018-2028 Long term plan, has signalled

that there would be a total expenditure increase of $321,815K over the next ten years, of

which 58% relates to capital expenditure, and of which 49% will be incurred in the next four

years as demonstrated in the table below The proposed amendment and annual plan key

message included in the following comments:

Since the last LTP we have received new reports and information on what’s needed to

maintain and improve our Three Waters infrastructure and our transport network.

Annual Forecast Forecast Forecast Forecast Forecast Forecast Forecast Forecast Forecast

Total 10

Changes to expenditure

Plan

Years

Increase/(Decrease)

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

$000

$000

$000

$000

$000

$000

$000

$000

$000

$000

$000

Increase (decrease) in

136,636

18,054

12,852

12,172

13,076

14,280

16,062

15,796

10,270

14,142

9,932

operational expenditure

Increase (decrease) n capital

185,179

(7,096) 24,277

48,090

35,070

22,698 (47,912) (23,824) 42,134

44,773

46,970

expenditure

Total Increase (decrease) in 321,815 10,958 37,129 60,262 48,146 36,978 (31,850) (8,028) 52,404 58,915 56,902

expenditure

This increase in expenditure has resulted in the Council amending its existing financial

strategy.

under the Local Government Official Information and Meetings Act

However, on the 9th April 2020 Council resolved not to progress the Long term plan

amendment and rather to develop a one year “emergency budget” Annual Plan 2020/21 at

3.8% rates increase as a result of COVID-19.

A financial strategy is required by section 101A of the Local Government Act 2002 (LGA) and

Released its purpose includes the facilitation of prudent financial management.

The existing financial strategy that is contained in the existing1 2018-2028 Long term plan

has three aims:

•

Strengthening Council’s financial position in anticipation of projects and

programmes that may need funding in the next 20-30 years.

•

Ensuring rates were affordable to our community and competitive when compared

to local authorities with a similar population and a significant urban centre.

•

Delivering services more efficiently than our peer local authorities.

The existing financial strategy is one of affordability i.e. keeping rates low, and building

capacity for future expenditure by reducing the borrowing limits. This in itself restricts both

operating and capital expenditure, without considering the longer-term impacts.

This existing strategy reflects restrained approach but does not document what the Council

considers as being prudent. As one of the purposes of a financial strategy is to facilitate

prudent financial management, the strategy should include a statement on how the Council

intends to manage its finances prudently.

A review of the last three years Annual reports confirms that the Council has a very

constrained approach to financing capital expenditure. By removing the non-cash gains and

losses from both the actual and budgeted operating results, this discloses accumulated

actual deficits of $22,849K (budgeted deficits of $20,095K). This approach is not financially

sustainable in the long-term and if not corrected this will ultimately result in a significant rise

in rates.

This then, questions whether that existing approach was prudent. The existing financial

strategy does not consider prudence nor does it consider the impact of having an

unbalanced budget in the first year of a long-term plan. The proposed deficits were

commented on briefly in the body of the Long term plan.

To be prudent, a local authority must consider at least the following:

•

Current financial position including debt levels and available head room to provide

for unanticipated events which require local authorities to undertake additional

borrowing.

•

Physical state of infrastructure including future needs, and also including

maintenance and the funding of asset replacement to meet the intend levels of

service.

•

Overall approach to funding including the use of depreciation.

•

The community’s appetite for increase in rates and debt.

The requirement to have a balanced budget is contained with the Local Government Act

2002 and requires all local authorities to set their budgeted revenues at a level meet that

under the Local Government Official Information and Meetings Act

year’s budgeted operating expenses, until the authority resolves it is not prudent to do so.

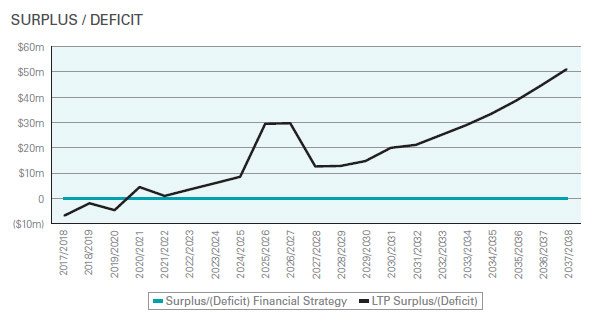

While the Financial statements2 supporting the proposed amendment to the 2018-2028

Long term plan disclose a significant deficit in the first year, there are surpluses in the

following years. However, this forecasted result includes capital revenue, which has been

excluded when Council has considered its proposed financial strategy. As the proposed

Released

1 See Appendix 1 for an extract of existing Financial strategy

2 See appendix 2 summary of Revenue and expenditure budgets for the proposed Annual & amendment

to LTP

Report on proposal to amend the 2018-2028 Long term plan and existing financial strategy

Page 2 of 22

amendment to the 2018-2028 Long term plan discloses surpluses after year 1, therefore

Council will have a balanced budget for the remaining periods.

The Council in considering the need for additional operational and capital expenditure has

amended3 the financial strategy as part of the proposed amendment to the Long term plan

and 2020/21 Annual plan to reflect the following key principles of:

•

Promoting the sustainable funding of services

•

Affordability of rates

•

Delivering services effectively and efficiently

•

Achieving intergenerational equity by spreading the costs between both present and

future ratepayers

•

Maintaining prudent debt levels

•

Strengthening Council’s financial position.

This is an improvement on the existing strategy and there are further improvements to be

made, in particular by defining the need for increased funding for renewal expenditure and

considering the impact of a balanced budget and noting the intention to increase revenues

over time to “balance the budget”.

In conclusion, the proposed financial strategy and the approach taken in the development of

the proposed amendment to the 2018-2028 Long term plan is a significant improvement.

The reason for this improvement from the existing strategy is by clearly explaining the need

to increase expenditure and move to a tighter balanced budget test consistent with good

practice. This will assist in forming a sound and financially prudent approach for the

development of the 2021-2031 Long term plan.

Philip Jones

Principal

under the Local Government Official Information and Meetings Act

Released

3 See appendix 3 an extract of proposed comments, strategy and principles supporting the proposed

Annual & amendment to LTP

Report on proposal to amend the 2018-2028 Long term plan and existing financial strategy

Page 3 of 22

Purpose of report

The following issues are considered in the report are:

1. The existing and proposed Financial strategies including how the principle of the

balanced budget test as set out in section 100 Local Government Act 2002 (LGA),

and consideration the Balanced budget benchmark as set in Local Government

(Financial Reporting and Prudence) Regulations 2014 have been considered.

2. How depreciation is calculated including the identification of assumptions and how

these change over time including why it is important to consider the revalued

amount, not the historical cost when meeting the balanced budget test.

3. Commentary on approach as set out in the 2018-2028 Long term plan for

achievement of balanced budget and the results in the Annual reports for the years

ended 30 June 2017, 2018 & 2019 focusing on Operating surpluses (deficits) and net

operating cash.

4. Commentary on the proposed approach as set out in the proposed amendment to

the 2018-2028 Long term plan including proposed amendment to the for financial

strategy achievement of balanced budget.

As the report is based on the initial proposal to amend the 2018-2028 Long term plan and

financial strategy, these are referred to in the report as proposed amendment to the 2018-

2028 Long term plan and the proposed Financial strategy. These are compared with the

existing 2018-2028 Long term plan and the existing Financial strategy contained within that

plan.

Consideration of prudence

There is a fundamental requirement for prudent financial management contained in section

101 Local Government Act 2002 (LGA) which requires all local authorities to manage its

revenues, expenses, assets, liabilities, investments, and general financial dealings prudently.

Section 100 subsection 1 of the LGA states:

A local authority must ensure that each year’s projected operating revenues are set at a

level sufficient to meet that year’s projected operating expenses.

However, section 100, then goes on to say:

2) Despite subsection (1), a local authority may set projected operating revenues at a

different level from that required by that subsection if the local authority resolves

that it is financially prudent to do so, having regard to—

under the Local Government Official Information and Meetings Act

(a) the estimated expenses of achieving and maintaining the predicted levels of service

provision set out in the long-term plan, including the estimated expenses

associated with maintaining the service capacity and integrity of assets

throughout their useful life; and

(b) the projected revenue available to fund the estimated expenses associated with

maintaining the service capacity and integrity of assets throughout their useful

Released

life; and

(c) the equitable allocation of responsibility for funding the provision and maintenance

of assets and facilities throughout their useful life; and

(d) the funding and financial policies adopted under section 102.

Report on proposal to amend the 2018-2028 Long term plan and existing financial strategy

Page 4 of 22

What the Act does is create a rebuttable presumption that forecasting a surplus is financially

prudent.

Financial prudence is not defined in the Act. But the legislation provides some insight into

what is intended by this phrase. In the standard dictionary sense prudence means ‘careful’,

‘sensible’, or ‘habit of acting with careful deliberation’. A local authority that does not

operate a balanced budget and has been cavalier in its treatment of the above matters may

well be acting imprudently.

There is one other statutory reference that provides an indication of Parliament's view of

what is considered financially prudent. Section 102 specifies certain financial policies which

are required to be adopted by every council. The legislative rationale for requiring these

policies is 'in order to provide predictability and certainty about sources and levels of

funding'. This can be seen as an indication that predictability and certainty of funding levels

and sources is seen as an element of being financially prudent.

Application of the concept of prudence in relation to establishing the level of operating

revenue for the purposes of LTP forecasting/budgeting would require the local authority to

set operating revenue at such a level that applies an unbiased assessment in areas of

judgement based on the best available information. The most significant area of judgement

that impacts the level of forecast operating expense, and therefore the level of operating

revenue needed to enable council to adequately fund the level of service represented by the

forecast operating expenses, is the useful life of the numerous components comprising the

infrastructure assets of the Council. Other judgements included in the determination of

operating revenue include the level of revenue sources other than rates in any period.

The requirement to set operating revenues at a level sufficient to meet operating expenses

includes depreciation because section 111 (LGA)4 obliges all local authorities to follow

generally accepted accounting practice (GAAP), which defines ‘operating expenses’. As

depreciation is an operational expense it must be included with other operational costs

including interest when a local authority sets its operating revenue.

What the legislation requires is that a local authority ensure that projected revenues are at

least equal to projected operational expenditure including depreciation, unless it is prudent

to do otherwise. The cash or funding generated by the revenue may be used for present

capital needs (including renewals), debt reduction or set aside for future capital needs. This

helps ensure sound asset management practice and continuity of service to future

generations.

Purpose of depreciation

under the Local Government Official Information and Meetings Act

There is confusion over the purpose of depreciation as many believe that the purpose of

depreciation is to provide for the replacement of an asset. In fact, depreciation reflects the

use or consumption of the service potential implicit in an asset. GAAP defines depreciation

as follows:

Released

4 Section 111 States All information that is required by any provision of this Part or of Schedule 10 to be

included in any plan, report, or other document must be prepared in accordance with generally accepted

accounting practice if that information is of a form or nature for which generally accepted accounting

practice has developed standards.

Report on proposal to amend the 2018-2028 Long term plan and existing financial strategy

Page 5 of 22

•

Depreciation is the systematic allocation of the depreciable amount of an asset over

its useful life.

•

As depreciation reflects the consumption of the asset over its useful life, there are two

critical factors in determining the expense. The first is the cost or revalued amount, and the

second is the useful life. It is therefore not related to the physical wearing out, for example

to be able to sit on a park bench in year one (or flush toilet) is the same benefit to a

ratepayer as being able to sit on park bench in year 15, 16, and 17 (or flush toilet).

The purpose of depreciation is not to provide for the replacement of the asset(s), however

this may be an intended or unintended consequence as many councils have assumed that

depreciation is for the replacement of an asset.

The approach to depreciation in the local government context is no different than the

commercial sector where depreciation is accepted as a legitimate operating expense; the

only real difference is the useful lives of local government infrastructure assets are

significantly longer than many assets used in the commercial sector.

As depreciation reflects the consumption of the asset over its useful life, there are two

critical factors in determining the expense. Both of these can change dramatically over the

life of the asset.

Cost or revalued amount

While the cost of an asset is relatively easy to ascertain, because councils’ assets provide

benefit for a long period of time (50-100 years), councils revalue to reflect the fair value

(book value) which for all infrastructural assets is based on Depreciation Replacement Cost

(DRC). This is the replacement cost based on the replacement value of an equivalent asset,

less the accumulated depreciation. It is important to note there is a requirement that an

entity annually considers the fair value of its assets and that at least every five years it

revalues its assets. Most local authorities revalue at least every three years.

As a result of revaluing assets depreciation will increase based on an equivalent replacement

cost. However, as the purpose of depreciation is to charge the people who are using the

asset their share of that asset, if the value has increased, in theory the people using the

asset should pay a greater share. If the value has increased so do the future renewal costs.

Useful life

One of the most difficult tasks in assessing the depreciation expense is assessing the asset’s

useful life. While there are standard useful lives and often manufacturers give a minimum

useful life, there are a number of factors that dictate the ultimate useful life. However,

these can be grouped into either condition based or performance based. Condition relates

under the Local Government Official Information and Meetings Act

to the physical attributes of the asset, while performance relates to the ability of the asset to

meet the level of service requirements.

The range of useful lives are reflected in each council's accounting policies which are

included within the financial statements and these can vary significantly from council to

Released council. It is not uncommon for one council to have a standard useful life of 80 years and

another council to have a standard useful life of 160 years for the same asset because of

different aspects, including construction methods, environmental constraints, topography

and soil types. The change in useful lives results appropriately in a different depreciation

expense.

Report on proposal to amend the 2018-2028 Long term plan and existing financial strategy

Page 6 of 22

Furthermore, as more and better information becomes available, then the useful life of an

asset can increase or decrease.

Conclusion on depreciation

As depreciation is a significant expense for Hutt City Council (24% of operating expenditure),

therefore the calculation and how that expense is considered in setting its overall revenue is

an important component when defining if the Council is acting prudently.

Importance of the financial strategy as defined in section 101A5 LGA

The financial strategy is a key part of telling the story of both the long-term plan and also

considering how the local authority is intending to manage its finances in a prudent manner.

While there are two key pieces of legislation that require a local authority to consider

prudence, there is often other factors outside of the legislation that council must consider in

developing both its financial strategy and its view on prudence. Each Council must consider

its own factors including:

•

Current financial position including debt levels and available head room to provide

for unanticipated events which require local authorities to undertake additional

borrowing.

•

Physical state of infrastructure including future needs and also including

maintenance and the funding of asset replacement to meet the intend levels of

service.

•

Overall approach to funding including the use of depreciation.

•

The community’s appetite for increase in rates and debt.

•

The overall direction and desired end point for the financial status for the local

authority.

•

A synthesis of the financial issues and consequences arising from the policy and

service delivery decisions elsewhere in the LTP and how the local authority intends

to manage those consequences.

Taken together the financial and infrastructure strategy provide the reader with a sense of

the costs, risks and trade-offs that underpin the development of the expenditure

programmes in the LTP which informs the reader as to the appropriate issue or the “right

debate”.

Consideration of the Prudence regulations

under the Local Government Official Information and Meetings Act

5 Section 101A Financial strategy

(1) A local authority must, as part of its long-term plan, prepare and adopt a financial strategy for all

of the consecutive financial years covered by the long-term plan.

Released (2) The purpose of the financial strategy is to facilitate—