9 September 2021

House of Representatives Standing Committee on Tax and Revenue

PO Box 6021

Parliament House

Canberra ACT 2600

email: [email address]

The Chair,

CONTRIBUTION OF TAX & REGULATION ON HOUSING AFFORDABILITY & SUPPLY IN AUSTRALIA

PIA SUMISSION TO HOUSE OF REPRESENTATIVES INQUIRY

1. Overview

•

Housing unaffordability cannot be solved by more supply in the market.

•

The behaviour of housing as an ‘asset’ means that not enough housing is provided by the

market to those who need ‘shelter’.

•

Planning regulation and zoning is not a ‘roadblock’ – it serves as a ‘lane marker’. Development

proposals that align with Strategic Plans flow fast.

•

The role of strategic planning and planning regulation - is directed towards:

o

creating great places - and a sustainable built environment

o

access to diverse housing, jobs and services that reduce living costs/ boost productivity

o

ensuring infrastructure investment is cost effective

o

reducing development risks

•

A focus only on maximizing supply would compromises the value of planning in shaping

productive, liveable and sustainable cities and towns.

•

Measures to reduce demand for housing assets are important – but realistically won’t progress.

•

Substantial non-market supply of social/affordable housing is needed for lower income earners.

•

Planning facilitates diverse and affordable housing through the regulatory system - and by

strategic planning for population growth and change.

•

Costs arising from mandating affordable housing can be absorbed in the price of land.

•

The absence a coherent housing market strategy has major productivity and social implications.

PIA Context

The Planning Institute of Australia (PIA) appreciates the opportunity to make a submission to the House of

Representatives Standing Committee on Tax and Revenue. Our recommendations are in

Section 8.

Planning Institute of Australia

Page 1 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

PIA is the national body representing urban and regional planners and the planning profession. We

represent approximately 5,500 members and connect with more than 10,000 planners annually through

workshops, events and professional development.

PIA has members in private sector who facilitate development, members in government who set and

assess development applications – but all have a common interest in being advocates for the public

interest. PIA has no pecuniary interest in the recommendations made by the Committee.

The housing construction sector, as part of the broader built environment and development sector, is

critical to economic wellbeing of the country. It creates the living conditions of our cities and towns that

are recognised around the world.

Planners understand the depth of community concern about housing affordability, the seriousness of this

public policy issue, and the basic human need for shelter. Housing needs to be available in diverse forms,

that are affordable across the income spectrum – and which reduce living costs by enabling easy access to

work and services.

A genuine conversation about housing affordability requires us to unpack what is influencing

unaffordability – including the market demand drivers, tax setting and property development practices.

Planners play a role ensuring urban policy settings and development approval processes don’t restrict

supply. Planning schemes will direct supply in the long-term public interest – based on adopted strategy

in order to reduce infrastructure costs and boost availability and access to services.

It is clear that superheated demand factors swamp any price impact of delivering housing supply into the

market. This is having an impact on the ability to buy a home - as well as the ability of lower income

earners to access affordable rental property. Historic and international examples (Eslake 2017; Phibbs and

Gurran 2021) show us that housing affordability is most successfully improved when investment demand

drivers are reigned in - and the government plays a role providing and enabling affordable housing

delivery.

Terms of Reference

The inquiry is to address the “

contribution of tax and regulation on housing affordability and supply in

Australia” –

via terms of reference to:

•

“(i) Examine the impact of current taxes, charges and regulatory settings at a Federal, State and

Local Government level on housing supply;”

•

“(ii) Identify and assess the factors that promote or impede responsive housing supply at the

Federal, State and Local Government level; and”

•

“(iii) Examine the effectiveness of initiatives to improve housing supply in other jurisdictions and

their appropriateness in an Australian context.”

The ToR focus entirely on the impact of housing ‘supply’. This is not sufficient to address affordability.

PIA’s response to the ToR is summarised in

Attachment A. The structure of the submission is set out

below:

Planning Institute of Australia

Page 2 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

CONTENTS

PAGE

1. Overview

1

2. The housing unaffordability problem

3

3. Housing unaffordability can’t be solved by supply in the market

4

4. Housing unaffordability could be improved by easing demand – but it won’t happen

7

5. Planning for housing supply is important – just not for affordability

7

6. Planning regulation or zoning is not a brake on supply

10

7. Improving housing affordability will require investment in social and affordable housing

11

8. Conclusion and recommendations

12

9. Attachment A: Terms of Reference response

14

10. References

16

Definitions and clarifications

Supply and affordability

CONTENTS

PAGE

1. Overview

1

2. The housing unaffordability problem

3

3. Housing unaffordability can’t be solved by supply in the market

4

4. Housing unaffordability could be improved by easing demand – but it won’t happen

7

5. Planning for housing supply is important – just not for affordability

7

6. Planning regulation or zoning is not a brake on supply

10

7. Improving housing affordability will require investment in social and affordable housing

11

8. Conclusion and recommendations

12

9. Attachment A: Terms of Reference response

14

10. References

16

Definitions and clarifications

Supply and affordability

The terms housing supply and affordability are used loosely and mean different things, PIA urges the inquiry to distinguish what

they are reporting on:

•

whether affordability refers to home purchase price - or the cost of rent

•

whether in relation to access to housing by lower income earners

•

whether living costs are taken into account

•

whether supply is considered as a rate - or static number

• whether supply is total stock, new stock or stock that may be for sale at any time

PIA regards the cost of rent as the true cost of access to housing as ‘shelter’ .-. However, the purchase

price of housing also reveals its value as an investment asset and reflects the capitalisation of rental

income – this component is becoming more prominent and is most sensitive to strong housing demand

factors (Gurran et al 2015). Prospective owners (investors) are buying a future rental stream1 and an asset

with strong tax advantages and prospects of capital gain.

Housing being for the purpose of both shelter and an investment asset – has led to deep

misunderstanding and confounded public policy.

2. The housing unaffordability problem

Housing is becoming more unaffordable to buy cross all markets, while access to rental is squeezed for

lower income earners.

The REIA Housing Affordability Report (2021) notes that mortgage repayments for owner occupiers have

increased by 180% over the last 20 years, well in excess of average wage growth (113%). The proportion

of household income required to service an average mortgage has grown from 27.2% to 35.7% over the

same period. Yates (2017) finds that since the 1970s Australia’s median house prices have quadrupled

while wages have only doubled in real terms.

The ‘problem’ has been largely framed in terms of declining access to first home ownership - or

inadequate rates of new housing production (Phibbs and Gurran 2021). Whilst these elements are

important over the long term, they do not relate to the fundamental problem that housing is becoming

less available to people who need it. If you are low income earner your choices of where and what you

live in (rent or buy) in becoming much more restricted.

1 Or avoided the cost of paying rent (being an owner).

Planning Institute of Australia

Page 3 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

In general, Australia does not have a housing supply problem - we have an affordability problem. Housing

supply is currently a

success story across many of Australia’s cities. In 2018, Australia had one of the

highest dwelling completions rates in the developed world. Except for South Korea, Australia produced

housing faster than other OECD nations at

8.2 completions per 1000 persons, up from 6.8 in 2010, – at

37,000 dwellings a year. In 2018, Sydney produced more dwellings than London, despite having a

population less than half the size. At the end of 2016, there were

more cranes (528) servicing apartment

construction down the east coast of Australia than in major cities across North America including New

York, Boston, Chicago, San Francisco, Los Angeles and Toronto (419 cranes) (Brockhoff 2018).

The evidence shows a conundrum, housing production has reached record levels but purchase prices in

the largest markets has continued to grow even faster as investor demand swamps new supply. Phillips

and Joseph (ANU 2017) highlight evidence tha

t in many parts of Australia – house building has been

running well ahead of local household growth for much of the last 30 years (except post GFC) and

especially recently since 2015. There is no accumulated shortage2, but purchase prices have continued to

increase. For example, in the City of Sydney,

overall median apartment prices rose by 52% in the five

years to 2017 in an area oversupplied relative to population.

The cessation of international travel since the outbreak of the Covid 19 pandemic has resulted in zero net

overseas migration since early 2020. Despite this drop in demand house prices have continued to soar.

It is important to note that new supply is a small fraction of the total stock of dwellings

(about 2% in

Australia) – while in 2018 it got as high as 3% in Sydney (DPIE 2019). Prices are set by the total housing

market - most of which already exists in the form of established homes or apartments. ABS data via RBA

(2017) show annual turnover rates (amount sold annually as a proportion of total stock) to tracking

around 5% for the decade.

Alongside the obvious difficulties for middle income earners affording homeownership, there is a more

insidious effect on access to rental markets exposing lower income earners. Nominal rents have not

increased as new housing supply has expanded the middle portions of the private rental sector3. However

Ong et al (AHURI) 2017) and (Hulse et al 2019) show the availability of lower priced rental property has

not improved. While the SGS Rental Affordability Index (SGS 2020) shows steady widespread geographic

contraction towards only the lowest amenity suburbs in Australia’s major cities.

3. Housing unaffordability can’t be solved by supply in the market

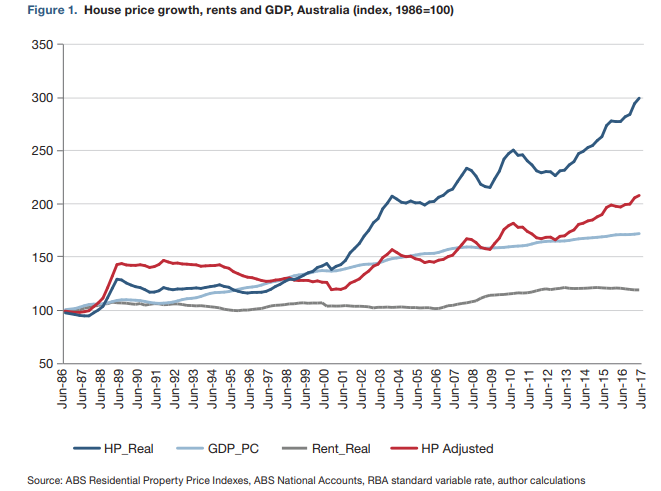

Bank of England researchers Lewis and Cumming (2019) have constructed a twenty-year model which

shows that “relative scarcity of housing has played almost no role at the (UK) national level since 2000” in

rocketing prices. The same insight is available from Australian researchers. The local evidence shows that

changes in the price of housing is decoupled from changes and growth in supply (Phillips and Joseph

2017) (see Figure below).

2 Based building completions/ demolitions, population and household occupancy (Phillips and Joseph 2017)

3 At rental prices serving middle income earners often unable to buy (Ong et al 2017)

Planning Institute of Australia

Page 4 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

Phillips and Joseph (ANU) 2017

Phillips and Joseph (ANU) 2017

Central banks (see Youel 2020) are aware that the market for housing does not perform like one for

consumable products like bananas – for one thing when house prices go up consumption often goes up

too. But it has proven inconvenient for the Central banks to explain the difference. One reason is that the

‘cupboard is bare’ of politically palatable demand side solutions dealing with monetary policy (Hutchins

2021), tax and other financial measures (Eslake 2017).

It should not be up to planners to explain this predicament - but we bring a clearer insight on what is

being traded and ‘consumed’ in the housing market.

Dwellings persist as stock in the market and are

added to with new supply (growing ~2% every year). But in any year only a small proportion of the total

(~5%) are available on the market to be bought. The small proportion of new supply created and traded

as a proportion of total stock means that it is hard for additional supply to reduce prices rapidly and

deeply. As a result residential developers are ‘price takers’ - not ‘price makers’.

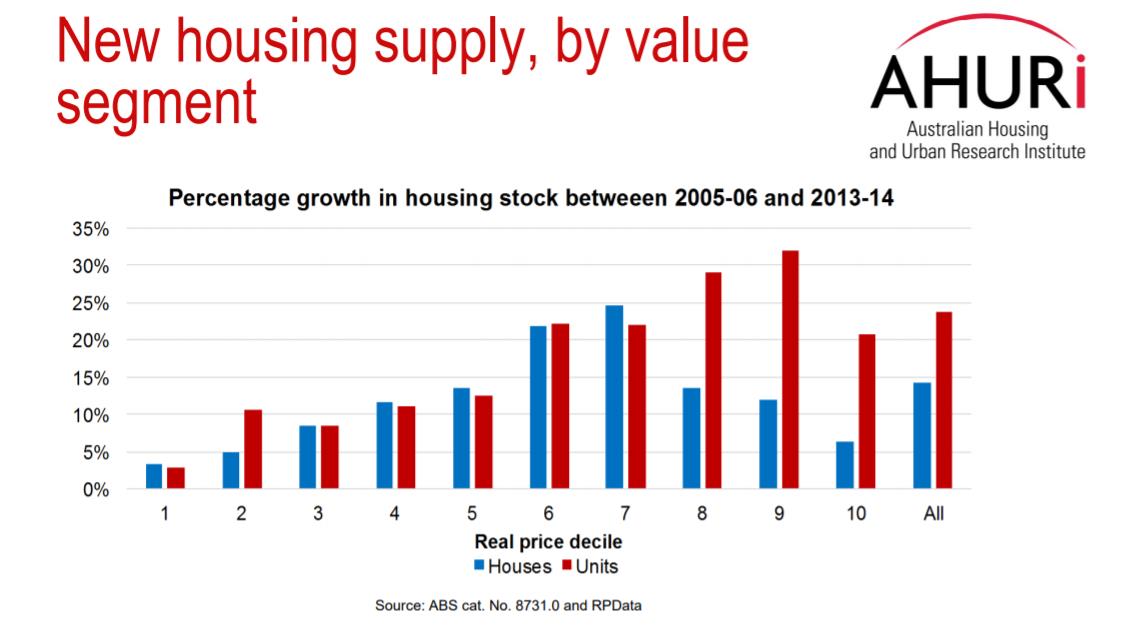

These observations are borne out by empirical research by Ong et al (2017) that supply and price are not

responsive to each other. A 1% increase in the level of real housing prices is estimated to produce a 4.7%

pa increase in new house supply - and less for units. Ong et al note these price gains translate into very

small increases in housing stock which will do little to keep up with demand pressure. The work also

highlights that the growth in supply that has been taking place has been in the mid to high price segments

Planning Institute of Australia

Page 5 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

– and that there seem to be structural impediments to the trickle down of more stock available for lower

income earners.

The figure below (from Ong et al (AHURI) 2017) highlights the relative increase in supply of higher price

units and moderate price houses – while supply which may be affordable to the lower income earners is

less available in the market.

There are highly localised examples of intense supply shortages impacting purchase price such as in

booming mining / tourist towns - but this does not undermine the macro proposition that new supply is

not able to grow fast enough to substantially affect price. Supply will not grow fast for several reasons:

•

Finance limitations - residential development financiers actively manage risk and would restrict

lending where there is evidence of a potential for oversupply and the security of their returns to

be threatened.

•

Labour and construction materials - the construction sector has limited capacity to scale up and

down quickly. The HIA (2021) Trades Report recorded the biggest trade shortages since 2004 ,

with many skills and materials (eg bricklayers, carpenters, tiling, roofing and specifically timber)

being hard to access. The HIA note that the easing of these constraints will take time and the re-

establishment of international supply chains.

•

Commercial decisions to build land banks take time – commercial decisions to purchase and

maintain substantial land banks are strategic and not able to be rapidly changed.

•

Market absorption rates dictate delivery – Private actors in the market behave rationally to

maximise profit and bring their new stock to market at a speed/amount that the market will

absorb without having to discount price. This can result in drip feeding the market to avoid

depressing prices – so long as holding costs are less than the prospects of future price growth.

Murray (2019) notes that major property developer’s annual reports reveal their rational

intention to supply housing at a flexible/slow rate to maximise shareholder return.

Planning Institute of Australia

Page 6 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

All private sector actors respond to the rate of housing absorption – either by restricting access to finance

to reduce risk exposure or by controlling the flow of sales in the market. This is rational behaviour to

maximise profits but is not widely understood or disclosed (Phibbs and Gurran 2021, Murray 2020).

Murray (2021) notes that dwelling development is an “asset reallocation decision, not a production

quantity decision”. Therefore, choices to develop new housing are tied to asset market factors, not

production factors, such as construction cost. Undeveloped land also remains an asset, earning a

potential return in the form of capital gain regardless of a developer’s decision and timing to construct.

4. Housing unaffordability could be improved by easing demand incentives – but it won’t happen

The literature discusses the overwhelming influence of factors that superheat housing demand and make

it relatively more attractive as an investment asset (Phibbs and Gurran 2021, Daley and Wood 2016,

Rowley et al 2020). The main factors include:

• low interest rates

• access to mortgage finance

• tax advantages to housing investment (eg Negative Gearing, Capital Gains Tax

Discounts/Exemptions and means testing of pension excluding home)

• first home owner’s bonuses / subsidies

The ‘hyper-commodification’ of housing as an asset has divorced it from conventional market behaviour

(Madden and Marcuse 2016). The price of housing no longer reflects its value as a ‘roof to live under’.

Commentators such as John Daley (2021) and Saul Eslake (2017) express little hope that while a majority

benefit from elevated house prices the political economy won’t shift to allow a wind back of these strong

and more rapidly acting influences on demand. If demand incentives are not wound back, the challenge to

supply social and affordable housing off market will increase.

5. Planning for housing supply is important – just not for affordability

Roles of planning

Housing supply enables economic activity and jobs across the property and construction sector. Enabling

supply and promoting conditions where development is viable and can fulfil a place outcome is central to

planning. Rowley et al (2020) demonstrated that “

proactive local planning for growth (outer ring) and or

urban renewal (inner ring) was also a key factor driving supply” – alongside integrated infrastructure

planning.

But planning processes are designed for more than being a housing ‘sausage machine’. Planners have a

key role in housing supply, but are one of many who provide services to develop communities. Planners

provide capabilities to :

• undertake strategic planning, forward thinking, plan for land that is suitable and ensuring links

with infrastructure and transport;

• improve liveability in growing and changing urban areas by setting quality, diverse, sustainable

building and place outcomes;

Planning Institute of Australia

Page 7 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

• translate land use strategy into spatial plans via rezoning, considering and making trade-offs

among local community views and broader stakeholders; and

• manage the development assessment process on behalf of the public to assure alignment

between proposals and adopted community outcomes.

Planning housing for long-term population growth and change

Although more housing supply is shown to not have a rapid or deep effect on house price, the provision of

new and well-suited supply is essential to house a future growing population with changing dwelling

needs and means. PIA (2016) published a discussion paper on planning for

Australia towards 50 million

outlining the megatrends impacting the housing and city making task.

Making provision for long-term growth and change is a key role of strategic planning. It requires the

preparation of land supply pipelines supported by integrated funding and delivery of infrastructure in

greenfields and existing urban areas. PIA has set out the value of

a National Settlement Strategy (PIA

2018,

Brockhoff 2018) and developed planning parameters to align infrastructure for this purpose.

Planning housing for liveable communities – integrated with infrastructure and services

The availability of zoned and serviced land aligned with infrastructure strategy de-risks urban

development decisions and frees up the flow of investment vital for economic activity across the sector

and the fulfilment of strategic plans that will deliver value for the broader community (Brockhoff and

Spiller 2019).

The essential purpose of planning (and its regulation) is to maximise the aggregate (measurement) of

liveability for all members of the community. This is achieved by the Government allocating monopoly

rights for the use of land according to a plan that balances the needs of the individual against the living

conditions sought by all in the community. The Government makes a spatial expression of these

conditions by engaging the community and endorsing the trade-offs in a land use plan.

The outcome of a well-planned settlement is reduced living costs to access facilities, work or services and

enjoy some amenity (The CIE 2012). These avoided costs need to be considered alongside the price of

renting or mortgaging a dwelling.

Planning is a pre-requisite for cost-effective housing delivery

Having a sequenced plan with knowledge of where patterns of housing growth and activity can be located

is a pre-requisite for cost effective infrastructure delivery. Integrated planning reduces headworks costs,

utilises spare capacity and focuses human activity where there are clustered services and transport

choices. Infrastructure Australia (2021) highlight the economic value of this place-based approach in their

discussion paper

Planning Liveable Cities and the

Australian Infrastructure Plan (IA 2021).

The planning and zoning tools which enable orderly sequencing of development and maximise the

public’s return on infrastructure are the same that enable housing supply.

Rowley at al (2020) notes that while the planning system can create opportunities for desired

development, decisions about whether and when to submit applications and construct are ultimately

made by the development industry and reflect market factors. Ultimately housing supply is driven by

Planning Institute of Australia

Page 8 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

market conditions and the ability of a developer to deliver an acceptable return. Variations in market

conditions and the availability of quality development sites at different stages along the pipeline drive

uneven patterns of supply.

The planning profession is constantly engaged in improving the pattern and flow of supply aligned with

land use and infrastructure investment strategy. This involves each level of government; investing in

major infrastructure provision and upgrades; coordinating land-supply processes and making available

developable sites; and streamlining development approval processes for projects that meet local planning

requirements, including expectations for diverse, sustainable, well designed and affordable housing

options.

Planning for housing supply includes community expectations for improved amenity and liveability

Many private and public costs on new housing development and construction are integral to achieving the

living conditions expected by the community through their planning strategy.

A suite of infrastructure costs is shared and levied through contributions plans - and cover items such as

access roads and drainage. PIA’s

Infrastructure and its Funding Position and Discussion Paper sets out the

rationale for attributing sharing these costs between the developer and the community.

Planning regulation also sets an expectation for the quality and sustainability of construction – and set

requirements for the delivery of more diverse housing types and affordable housing units. Where these

costs are predictable, they become an element of the total viability equation. Ultimately, these costs can

be passed back to the price of the land assuming the purchase price was reckoned accordingly. There is

literature on the extent to which infrastructure charges and affordable housing contributions work

against speculation and operate as user charges and inclusionary requirements (Spiller, Mackvecius and

Spencer (SGS) 2018) and Spiller 2021). The figure below (extract Spiller et al 2018) sets out the rational for

known affordable housing/ inclusionary zoning costs being passed back to the land owner.

harges and a es

harges and a es

onstruc on

onstruc on

marke ng

marke ng

ross

a

n e

d a

lisa

na

nc o

e n

and nance

alue

c

o o

st rs total

ross r

c e

o t

s u

tsrn

sales revenue

eveloper argin

eveloper argin

for Pro t and isk

for Pro t and isk

H

pli

pli

esidual and alue

esidual and alue

urrent value

is ng

edevelopment values

edevelopment

with H

2

Planning Institute of Australia

Page 9 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

6. Planning regulation or zoning is not a brake on supply

6. Planning regulation or zoning is not a brake on supply

The Inquiry terms of reference an

d media release highlight “restrictive planning laws as a major cause of

shortages in supply”. This ignores the unresponsiveness of housing price and misunderstands the positive

role of planning shaping housing supply.

What does planning regulation (and zoning) do?

A functioning planning system is about translating goals for a place into policy and regulation that best

achieves this intention - with least cost and delay. Zoning is one of the tools at the disposal of city

managers to curate a valuable place outcome. Zoning is the spatial representation of where different

development decision-making criteria should be used. It shapes land uses and locates buildings to enable

sustainable growth aligned with strategy. Importantly, planning and zoning does not regulate when and

how fast dwellings are built.

Together with codes and other tool, zoning enables development to continue to deliver public value

(Brockhoff and Spiller 2019). Marcus Spiller estimated the cumulative net benefit of a plan for Melbourne

at over $25 billion. In Sydney, The CIE (2012) estimated the savings from different urban structures for

Sydney at between $2K and $10K every time a new house is built under the metropolitan plan.

Achieving valuable outcomes is worth the regulatory complexity involved. Planners agree planning tools

and zoning can be improved. Planners understand that housing and business reallocation is always

occurring and that the planning system must ensure that the right settings for emerging enterprises are

available. However, reform should only be targeted towards that regulation which is in excess of the rules

and incentives needed to achieve a strategic plan outcome. This is an area where PIA continues to be

positively engaged in partnership with Government and industry.

Australian jurisdictions have already progressed substantial planning regulatory reform and offer a ‘light

touch’ (Phibbs and Gurran 202 ). The adoption of housing targets, standard instruments, growth of ‘code

assessable’ development pathways (up from 2% to >40% by 2016, NSW Government (2017) - and the use

of independent panels are examples from most jurisdictions.

Modelling regarding a ‘zoning effect’ is wrong

RBA authors Kendall and Tulip (2018) (using models based on Glaeser and Gyourko (2003), have made

misleading claims that not only is zoning a barrier to supply but it is responsible to considerable additional

costs (+73%) on the price of supplying housing. The authors incorrectly ascribe the difference in average

price of housing and the marginal cost of supplying them to a ‘zoning effect’. However, their static

modelling methodology is incapable of attributing the results to planning regulation or anything else with

the potential to limit capacity. By not taking into account the ‘market absorption rate’4 in a dynamic

model, their conclusions are irrelevant. At best, the ‘costs’ they attribute to a ‘zoning effect’ reflect

amenity value and access to jobs and services in a well-planned city.

PIA and academic economists (Phibbs and Gurran, 2021 and Murray, 2021) have pointed out these

serious concerns to the Productivity Commission and to RBA authors of ‘

The Apartment Shortage’ and

4 Rate at which stock can be sold into the market while maintaining price.

Planning Institute of Australia

Page 10 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

‘The Zoning Effect’

‘The Zoning Effect’. It is unfortunate that the publishers did not take an opportunity to test the method

and implications of the work among a balanced professional audience prior to publication. Unfortunately,

these misleading studies continue to be quoted by property interests and the NSW Productivity

Commission (2019, 2020).

Why zoning is a ‘lane marker’ not a ‘road block’ to supply

The ‘market absorption rate’ is also a critical factor in considering whether planning and zoning controls

are on the ‘critical path’ for housing delivery and act as a delay or substantial cost. Murray (2021) points

out that many sites will remain undeveloped even though the price of housing assets exceeds

development costs, but the constraint is economic - not regulatory. Murray notes that the rate at which

new dwellings are sold into the market is dictated by the speed at which successive new sales impact

market price. This asset market’s appetite for buying new dwellings will determine the overall rate of new

supply, the absorption rate, regardless of planning regulations. While planning does regulate location,

form and density - it does not regulate the speed at which development is taken up in the market.

Rowley at al (2020) indicate that only 68% of all approvals in NSW (75% in Victoria) actually resulted in a

completed building (period 2006-2016).

Data on development delivery since the 1990s (Phillips and Joseph ANU 2017) offers compelling evidence

on the sustained high levels of throughput and how accommodating planning systems around Australia

are shown to be in servicing the high asset demand for housing.

Rates of development approvals (as a proportion of applications) have also remained high and relatively

steady (Sneesby 2020). Review by Phibbs and Gurran (2021) indicate that major Australian markets like

Sydney have been responsive to demand and delivered 44,000 dwelling completions in 2018 alone.

Interestingly during periods when approvals have fallen, approval rates remained the same. Sneesby

(2020) points out in shorthand: “No one is buying, so no one is building, so no one is putting in

applications, so there is less to approve.”

The data suggests that the planning system can respond to changing dwelling demand and has becoming

increasingly responsive due to extensive planning reform and integrated strategic land use and

infrastructure planning. In fact, the data would suggest that there are more, bigger, better, dwellings per

capita in Australia now compared to any point in history (Murray 2021).

7. Improving housing affordability will require investment in social and affordable housing

PIA’s submission illustrates that there are structural reasons - unrelated to planning, why the private land

and housing market is not allocating affordable supply to lower income earners in the market. The

persistence of demand factors driving up the asset value of housing works against market delivery of

affordable housing.

PIA continues to support a housing vision that supports security, comfort, independence and choice for all

people at all stages of their lives. To achieve this large-scale non-market delivery will need to augment the

private market. PIA (2016) supports:

Planning Institute of Australia

Page 11 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

• Advocating and facilitating the delivery of the social infrastructure necessary to support

affordable, accessible and appropriate housing for vulnerable members of the community,

including low income families, people with special needs.

• Considering infill and urban renewal precincts as areas for value capture to provide essential

property and social infrastructure and affordable housing.

• Promoting the implementation of innovative planning policies that support affordable housing

(including mandatory inclusionary zoning)

8. Conclusion and recommendations

1. Abandon the ‘supply myth’

The misunderstanding of powerful demand drivers in an investment asset market for housing

confounds any public policy response to address affordability of housing for shelter - and dispel the

‘supply myth’.

PIA agrees with Maclennon et al (202 ) who note “there is a substantial capacity deficit - of skills,

institutions and governance structures – to both understand the housing system and construct a

coherent housing market strategy and the policies to deliver it.”

This inquiry demonstrates that we have a poor understanding of both housing in the macro economy

and how it shapes our cities. It is vital that public decisions regarding stimulus of the property sector

and improving pathways to ownership respond to the broader role of housing in shaping cities and

providing needed shelter.

Recommendation 1: Establish a standing ‘commission’ on housing strategy - with a broad base of

skills (including planners) to provide a source of truth and coherent policy in the public interest.

2. Nurture effective planning and development systems

Planning continues to be important shaping liveable communities, sustainable buildings and enabling

orderly housing supply and cost-effective infrastructure delivery as population grows and changes.

Strategic planning, zoning and development assessment processes are among the tools of the trade –

and we apply these with close community and stakeholder involvement in the outcomes.

The findings of this inquiry must not prejudice the value provided by good planning. Unsophisticated

attempts to fast track supply by eliminating planning processes do not work. UK experience (since the

Letwin Inquiry) demonstrate that not only does planning not control the rate of supply, but that

simplistic planning reforms are resulting in poor urban outcomes and lack of support. PIA continues to

pursue nuanced planning reform that reduces transaction costs while achieving the outcomes of

strategic planning.

Recommendation 2: Do not recommend misguided and simplistic planning reform responses based

on the prevailing misunderstanding of how planning operates in the housing market.

Planning Institute of Australia

Page 12 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

3. Promote integrated strategic planning

3. Promote integrated strategic planning

A key role of planning in enabling housing supply is the coordination, sequencing, funding and delivery

of growth infrastructure. Infrastructure contributions and value capture are an equitable component of

the funding. With clear and consistent planning these costs are passed back to the land owner rather

than act as a cost on development.

Recommendation 3: Recognise the critical role of integrated strategic land use and infrastructure

planning (and funding) in creating liveable cities.

4. Deliver social and affordable housing at scale

Powerful demand drivers of the housing market as an asset are locked-in and access to housing as for

lower income earners will remain tight. It will be necessary to significantly increase the availability of

non-market social and affordable housing – as well as new initiatives to diversify housing choices.

Planning has a small but enabling role for diverse housing types - as well as enabling infrastructure

contributions and the dedication of land, space and funds via mandatory inclusionary zoning for

affordable housing.

Recommendation 4: Recognise the significant and growing need for social and affordable housing

forms to be available at scale – and support measures that fund or facilitate delivery.

PIA has addressed in summary the issues arising from each term of reference in

Attachment A.

PIA will remain engaged with the Federal Government on the role of planning in housing markets. Please

do not hesitate to contact myself or our CEO David Williams, if we can be of assistance.

Yours sincerely

John Brockhoff

PIA National Policy Manager

Planning Institute of Australia

Page 13 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

ATTACHMENT A : PIA RESPONSE TO Terms of Reference

ATTACHMENT A : PIA RESPONSE TO Terms of Reference

“(i)…Impact of current taxes, charges and regulatory settings… on housing supply”

Factor

Impact

Collective impact of demand

Increased demand for housing as an asset (relative to other assets) –

incentives: CGT (exemptions /

simultaneously increasing supply and purchase price.

discounts) / Negative gearing

(Note – factors superheating demand would have a negative feedback on supply

/ Pension means testing

through:

(excluding home) / first home

• incentivising speculation and increasing costs associated with less

buyer subsidies

integrated planning / infrastructure / approval pathways.

• Incentivising land banking and drip feeding the rate of supply to the

market – because the potential for future yield or price could be

greater.

Interest rates (sustained low)

As above – improves access to capital and drives demand for housing assets.

Lending controls which

Impacts cost/availability of capital. Reduced access to finance – resulting in less

reduce financial risk exposure capacity to deliver supply (especially in those industry sectors most reliant)

Stamp duty

As a transfer tax, they penalise movement among property and prejudice the

most economic use (and supply) of land and buildings.

“(ii) Identify and assess factors that promote or impede responsive housing supply…”

Factor

Impact (Promote / Impede)

Integrated strategic planning

Promotes supply - enabling an orderly housing supply pipeline – with

and funding

infrastructure delivered most cost-effectively.

Infrastructure charges

Developers are typically ‘price takers’. Where the quantum is known and

predictable – the impost can be passed back to the price of land following a

period of readjustment.

The delivery of infrastructure via these charges can benefit amenity, reduce

living costs - and potentially feed back into land value. The outcome can enable

infrastructure, build public value and promote supply.

Aligned planning assessment

Where assessment regulation (land use decision criteria) is clear and favours

pathways

development aligned with strategic outcomes it promotes supply and build

public value.

Planning / zoning regulatory

Does not affect the rate of development – but contributes to public value as well

settings

as the quality, amenity and reduced living costs – and potentially feedback into

land value.

Housing (quantum) targets in

Promotes supply by offering an incentive for long term integrated strategic land

planning strategy

use and infrastructure planning for orderly growth (an aid in overcoming

NIMBYism).

Planning codes streamlining

Promotes supply as it can de-risk development and potentially improve access to

assessment for development

finance.

– or for specific / innovative

housing forms (eg medium

density / co-living etc)

Planning Institute of Australia

Page 14 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

Mandated housing diversity

Ultimately promotes supply that better meets community shelter needs.

requirements

Reinforces community expectations for development meeting actual shelter

needs. Can have an impact on the availability of capital – but is an essential

obligation and effectively a ‘licence’ to participate in the market and receive

development rights.

Mandatory Inclusionary

As above (see infrastructure charges) – noting that MIZ requirements once

Zoning (MIZ) for affordable

established can ultimately be passed back to the price of land.

housing

Value capture measures – (eg

The public hold the monopoly of development rights and can retain windfall

windfall gains at rezoning)

where mechanisms exist. The existence of value capture measures can dampen

speculation and the impacts it has on the behaviour of the market.

Building quality and

An expectation as part of the licence to operate. Reduces risk, promotes access

sustainable design controls

to finance and promotes supply accordingly.

Land supply via public

Promotes counter-cyclical supply and sustain industry capacity, can de-risk

development corporations

difficult sites and

Non-market housing supply -

An essential element of housing supply (needed at scale) to address unmet

public /NFP housing supply

shelter needs.

and rent subsidy of social and

affordable housing

“(iii) Examine the effectiveness of initiatives to improve housing supply in other jurisdictions and their

appropriateness in an Australian context.”

Initiative

Appropriateness to Australia

UK large scale social housing

Highly appropriate as the private asset market fails to deliver sufficient stock as

delivery

shelter for lower income earners.

UK affordable housing

Highly appropriate. MIZ is necessary to increase the scale and viability of the

requirements (% of new units) CHP sector. Highly appropriate as an inclusionary requirement – delivery of AH is

part of the licence to develop.

UK (Letwin report) zone

This is a confusing report – after learning the obvious that private landowners /

simplification reforms‘

developers do not voluntarily flood the market to depress prices – the report

assumption of sustainable

does not recommend any policy reform addressing this. The findings relating to

development’

supply are inappropriate and destructive. It denies the public value of well

aligned strategic planning and cost-effective infrastructure delivery. It works

against achieving strategic place outcomes. UK is now retreating from flagged

zoning / approval process reforms.

UK (Letwin report)

Ineffective – as the councils cannot be accountable for development behaviour

compulsory housing delivery

and rate of their delivery of approved dwellings.

targets for councils

US (zoning reform – racial

Not relevant - US zoning has had a different context and is seen as entrenching

integration objective)

racial exclusion. Current reforms are a distinct social initiative.

US (rent control)

Australia has typically had forms of rent control (eg AH in perpetuity) or rent

subsidy (eg NRAS) – they are an important driver of the AH sector.

NZ supply / land release focus

Being abandoned – as NZ moves towards a demand side focus to address

/ merit assessment initiatives

housing affordability. NZ is also moving away from an ‘effects based’ planning

system. Brockhoff and Spiller (2020) comment on this pro-market reform has

generated a risk laden, transaction cost heavy system of planning. The NZ

Government is now turning its attention to reinstating a ‘vision based’ model.

Planning Institute of Australia

Page 15 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

References

References

Brockhoff J (2018)

https://thefifthestate.com.au/columns/spinifex/more-housing-hasnt-fixed-australias-

affordability-crisis-its-time-for-a-national-settlement-strategy/

Brockhoff J and Spiller M (2019

) https://sourceable.net/why-planners-and-economists-should-take-city-

strategy-seriously/

Daley J (2021 ) Gridlock: Removing barriers to policy reform Grattan Institute.

Daley J and Wood D (2016) Hot property, Negative gearing and capital; gains tax reform, Grattan Institute.

https://grattan.edu.au/wp-content/uploads/2016/04/872-Hot-Property.pdf

Eslake S (2017) Pearls and Irritations

https://johnmenadue.com/making-housing-affordable-series-saul-

eslake-the-causes-and-effects-of-the-housing-affordability-crisis-and-what-can-and-should-be-done-

about-it/

Gurran N and Phibbs P (2014) Are Governments Really Interested in Fixing the Housing Problem? Policy

Capture & Busy Work in Aust

. https://www.tandfonline.com/doi/abs/10.1080/02673037.2015.1044948

Gurran N et al (2015) Housing markets, economic productivity, and risk: international evidence and policy

implications for Australia Volume 1: Outcomes of an Investigative Panel authored by Nicole Gurran, Peter

Phibbs, Judith Yates, Catherine Gilbert, Christine Whitehead, Michelle Norris, Kirk McClure, Mike Berry,

Paul Maginn and Robin Goodman.

HIA (202 ) ‘Perfect Storm’ (ref Trades Report) https://hia.com.au/housing/in-focus/2021/economics-

perfect-

storm?utm_source=social&utm_medium=Facebook&utm_campaign=Publications&utm_content=040821

Hulse K, Reynolds M, Nygaard C, Parkinson S and Yates J (2019) The supply of affordable private rental

housing in Australian cities: short-term and longer-term

changeshttps://www.ahuri.edu.au/__data/assets/pdf_file/0024/53619/AHURI-Final-Report-323-The-

supply-of-affordable-private-rental-housing-in-Australian-cities-short-term-and-longer-term-changes.pdf

Hutchins G (2021) ABC Interest rates not the right 'tool' to address runaway house prices, Reserve Bank

says https://www.abc.net.au/news/2021-05-06/guy-debelle-rba-monetary-policy-house-prices-

employment/100121976

Infrastructure Australia (2021) Australia Infrastructure Plan.

Infrastructure Australia (2017) Planning Liveable Cities.

Kendall R, & Tulip P 2018. The Effect of Zoning on Housing Prices. Research Discussion Paper 2018-03.

Reserve Bank of Australia.

Letwin O (2018) Independent review of build out (Final report for UK Parliament)

https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/752

124/Letwin_review_web_version.pdf

Lewis J and Cumming F (2019) https://bankunderground.co.uk/2019/09/06/houses-are-assets-not-goods-

taking-the-theory-to-the-uk-data/

Planning Institute of Australia

Page 16 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

Maclennan et al (2021) Housing: Taming the elephant in the economy (City Futures UNSW)

file:///C:/Users/JohnBrockhoff/Downloads/Synthesis_report-

final_version_12.06.pdfhttps://policyscotland.gla.ac.uk/new-report-housing-taming-the-elephant-in-the-

economy/

Madden D and Marcuse P (2016) In Defence of Housing. New York: Verso.

Murray, Cameron. 2019. Time is money: How landbanking constrains housing supply. Available at SSRN

3417494.

Murray C (2020) The Australian Housing Supply Myth (EconPapers)

https://econpapers.repec.org/paper/osfosfxxx/r925z.htm

Murray C (2020a) The truch behind the housing supply nonsense.

https://thefifthestate.com.au/innovation/residential-2/the-truth-behind-the-housing-supply-nonsense/

NSW Government (2017) Local development performance monitoring. Available at: https://www.

planningportal.nsw.gov.au/opendata/dataset/local-development-performance-monitoring-2015-16.

NSW Productivity Commission (2019) White Paper – Kickstarting the Productivity Discussion

https://www.productivity.nsw.gov.au/discussion-paper

NSW Productivity Commission (2020) Green Paper – Continuing the Productivity Conversation.

https://www.productivity.nsw.gov.au/green-paper

Ong R, Dalton T, Gurran N, Phelps C, Rowley S and Wood G (2017) Housing supply responsiveness in

Australia: distribution, drivers and institutional settings. AHURI.

Phibbs P and Gurran N (2021

) The role and significance of planning in the determination of house prices in

Australia: Recent policy debates - Peter Phibbs, Nicole Gurran, 2021 (sagepub.com) Economy and Space

2021 Vol 53(3) 457-79.

Phillips B and Joseph C (2017) Regional housing supply and demand in Australia ANU Centre for Social and

Research Methods.

PIA (2016) Planning Institute of Australia: Housing Position Statement.

https://www.planning.org.au/policy/Housing-0616

REIA (2021) Housing Affordability Report.

The CIE (2012) The benefits and costs of alternative growth paths for Sydney, focussing on existing urban

areas, for Department of Planning NSW.

RBA (2017)

https://www.rba.gov.au/publications/bulletin/2017/mar/pdf/bu-0317-3-housing-market-

turnover.pdf

Rowley S, Gilbert C, Gurran N, Leishman C and Phelps C (2020) The uneven distribution of housing supply

2006–2016, AHURI Final Report No. 334, Australian Housing and Urban Research Institute Limited,

Melbourne, https://www.ahuri.edu.au/research/final-reports/334,doi: 10.18408/ahuri-8118701

SGS (2020) Rental Affordability Index: Research report https://www.sgsep.com.au/projects/rental-

affordability-index

Planning Institute of Australia

Page 17 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act

Sneesby T (2020) https://thefifthestate.com.au/innovation/design/dont-blame-planning-for-a-supply-

shortage-and-rising-house-prices/

Spiller M, Mackevicius L and Spencer A (2018)

https://www.sgsep.com.au/assets/main/SGS-Economics-

and-Planning-Development-contributions-for-affordable-housing.pdf

Spiller M (2021) https://sourceable.net/windfall-tax-backlash-misunderstands-property-rights/

Yates J (2017) Housing Australia (CEDA report). The supply of affordable private rental housing in

Australian cities: short-term and longer-term changes

Yates J (2009) Tax expenditures and housing. Brotherhood of St Laurence.

Youel S (2020)

Bank of England finally admits high house prices are determined by finance, not supply and

demand - Positive Money.

Planning Institute of Australia

Page 18 of 18

Australia’s Trusted Voice on Planning

AUSTRALIAN CAPITAL TERRITORY c/- PO Box 5427 KINGSTON ACT 2604 | ABN: 34 151 601 937

Phone: 02 6262 5933 | Fax: 02 6262 9970 | Email: [email address] |

@pia_planning Planning Institute of Australia planning.org.au/act