WELLINGTON CITY

Client:

WELLINGTON CITY

Client:

Wellington City Council

INCLUSIONARY ZONING

Project No: 52114

ECONOMIC ASSESSMENT

Date:

August 2021

INITIAL DATA FINDINGS

W: www.propertyeconomics.co.nz E: [email address] P: 09 479 9311 PO: Box 315596, Silverdale 0944

SCHEDULE

Code

Date

Information / Comments

Project Leader

SCHEDULE

Code

Date

Information / Comments

Project Leader

52114.1

August 2021

Draft Report

Tim Heath / Phil Osborne

DISCLAIMER

This document has been completed, and services rendered at the request of, and for the

purposes of Wellington City Council only.

Property Economics has taken every care to ensure the correctness and reliability of all the

information, forecasts and opinions contained in this report. All data utilised in this report has

been obtained by what Property Economics consider to be credible sources, and Property

Economics has no reason to doubt its accuracy.

made in reliance of any report by Property Economics. It is the responsibility of all parties acting

on information contained in this report to make their own enquiries to verify correctness.

COPYRIGHT

© 2021 Property Economics Limited. All rights reserved.

CONTACT DETAILS

Tim Heath

Mob: 021 557713

Email:

[email address]

Web:

www.propertyeconomics.co.nz

W: www.propertyeconomics.co.nz

2

52114.1

THEORETICAL CAPACITY

•

Property Economics utilised the results from WCC Theoretical Capacity modelling

•

Only Comprehensive redevelopment was considered

•

Apartment options came in three different sizes, small, medium and large apartments

which averaged 70sqm, 100sqm and 150sqm respectively.

As a caveat Property Economics consider the average apartment sizes applied in the

WCC Theoretical Capacity Model are high, particularly for the purposes of this study and

potential reconciliation with demand.

The assessment of inclusionary zoning has been undertaken across three different suburbs and

zones, including:

1. Te Aro - Central Area zone

2. Johnsonville - Centre and Medium Density Residential zones

3. Tawa - Rapid Transit zone

Appendix 1 shows a map of each of these three suburbs as well as the sub-zones that have been

incorporated as part of this assessment.

Capacity is mutually exclusive between the three typology options. Building Large Apartments

removes the capacity for Medium or Small.

TABLE 1: THEORETICAL CAPACITY – TOTAL YIELD

Theoretical

Entire Suburb

Within Centre Zones

Large

Medium

Small

Large

Medium

Small

Capacity

Apartment

Apartment

Apartment

Apartment

Apartment

Apartment

Johnsonville

20,345

31,215

45,150

4,079

6,226

8,982

Tawa

37,405

57,099

81,865

14,963

23,028

32,599

Te Aro

3,464

5,290

7,655

2,235

3,415

4,942

Total

61,214

93,604

134,670

21,277

32,669

46,523

Source: Property Economics, WCC

Accounting for the number of dwellings removed from the theoretical capacity.

TABLE 2: EXISTING DWELLINGS BY SUBURB

Existing

Within

Entire

Centre

Dwellings

Suburb

Zones

Johnsonville

3,149

561

Tawa

4,420

1,748

Te Aro

526

336

Total

8,095

2,645

Source: Property Economics

W: www.propertyeconomics.co.nz

3

52114.1

1.1.

FEASIBLE CAPACITY

Feasible Capacity what is viableto build at an assumed 20% profit margin.

TABLE 3: FEASIBLE CAPACITY

Entire Suburb

Within Centre Zones

Large

Medium

Small

Large

Medium

Small

Apartments

Apartments

Apartments

Apartments

Apartments

Apartments

la y Johnsonville

20,345

31,215

45,150

4,079

6,226

8,982

ci

tic Tawa

37,405

57,099

81,865

14,963

23,028

32,599

etr a p Te Aro

3,464

5,290

7,655

2,235

3,415

4,942

eo

a

h

C

T

Total

61,214

93,604

134,670

21,277

32,669

46,523

y

Johnsonville

325

911

882

301

851

829

e l

ti

bi

c

Tawa

103

297

344

77

205

211

s

a

p

ea

a Te Aro

797

1,924

2,703

769

1,674

2,475

F

C

Total

1,225

3,132

3,929

1,147

2,730

3,515

y

Johnsonville

1.6%

2.9%

2.0%

7.4%

13.7%

9.2%

tili

Tawa

0.3%

0.5%

0.4%

0.5%

0.9%

0.6%

bi

%

s

Te Aro

23.0%

36.4%

35.3%

34.4%

49.0%

50.1%

eaF

Total

2.0%

3.3%

2.9%

5.4%

8.4%

7.6%

Source: Property Economics

1.2.

FEASIBLE CAPACITY - MAXIMUM PROFIT OPTION

This section utilises the highest profit typology option for each site. Net Yield shows total built

capacity adjusted for demolished dwellings.

TABLE 4: FEASIBLE CAPACITY - MAXIMUM PROFIT OPTION FOR CENTRE ZONES

Medium

Small

Maximum Profit

Total Yield

Net Yield

Apartments Apartments

Johnsonville

851

851

813

Tawa

205

205

200

Te Aro

571

1,744

2,315

2,185

Total

1,627

1,744

3,371

3,198

Source: Property Economics

W: www.propertyeconomics.co.nz

4

52114.1

2.

INCLUSIONARY ZONING OPTIONS

WCC is investigating the two potential inclusionary zoning options. The first option will require

any developer building more than 2,400sqm of floorspace to provide between 1 10% of the

new floorspace as assisted housing.

opments

that may have a negative impact on their feasibility.

In contrast, the second option incentivises developers to provide assisted housing through an

increase in the height restriction. Specifically, WCC has proposed to allow developers to build

an additional 25% floorspace in return for 10% - 50% of this additional floorspace being

provided as assisted housing.

Ultimately, the impact that these inclusionary zoning options will have on the modelled

feasibility is highly dependent on what the developer receives from the assisted housing

dwellings. For the purposes of this assessment, we have run two revenue scenarios using a 30%

and 50% reduction in the revenue received for an assisted home in comparison to one sold at

full price. Additionally, we estimate the number of assisted homes provided from each

inclusionary zoning option at both the upper end of the spectrum (i.e. 10% and 50% for

inclusionary zoning options 1 and 2 respectively) and in the middle of the proposed spectrum

(i.e. 5% and 25% respectively). This result in a total of four different scenarios tested for each of

the two inclusionary zoning options.

Specifically, these assumptions can be written as follows:

•

The developer sells the assisted housing at a 30% or 50% reduction in sale price.

This also translates to a reduction in real estate fees and GST. All other costs

associated with building the home are identical between the full price and assisted

housing options as it is assumed they will be of the same quality.

•

For the first inclusionary zoning option, if the additional floorspace is greater than

2,400sqm, then the number of assisted houses is equal to either 5% or 10% rounded

down. For example, if a development is posed to construct 32 dwellings, then 10%

of the development would equate to 3.2 dwellings. This is rounded down to 3

dwellings which in this instance, represents under 10% of the d

floorspace (approximately 9.4%). The same methodology is applied for the 5%

scenario which in this instance, would result in a single assisted dwelling.

•

For the second inclusionary zoning option, the number of homes built on each site

has been increased by 25% rounded down. Of these additional homes, either 25%

or 50% is assumed to be built as assisted housing. In the case of the 32-dwelling

development, a 25% increase in housing results in an additional 8 dwellings. Under

the 25% and 50% assisted housing assumption, 2 and 4 of these dwellings would be

considered assisted housing respectively.

W: www.propertyeconomics.co.nz

5

52114.1

2.1.

INCLUSIONARY ZONING OPTION 1

The four scenarios assessed are as follows:

Scenario 1: Up to 10% of the development is contributed to assisted housing at a 30%

discount. This results in up to a 3% decrease in revenue (10% * 30%).

Scenario 2: Up to 10% of the development is contributed to assisted housing at a 50%

discount. This results in up to a 5% decrease in revenue.

Scenario 3: Up to 5% of the development is contributed to assisted housing at a 30%

discount. This results in up to a 2.5% decrease in revenue.

Scenario 4: Up to 5% of the development is contributed to assisted housing at a 50%

discount. This results in up to a 1.5% decrease in revenue.

TABLE 5: COMPARISON OF OPTION 1’S IMPACT ON FEASIBLE CAPACITY

Feasible

Without

Assisted Housing 10% Assisted Housing 5%

Assisted

Capacity

30%

50%

30%

50%

Housing

Discount

Discount

Discount

Discount

Johnsonville

723

526

420

558

526

Tawa

205

148

116

205

148

Te Aro

319

319

319

319

319

Total

1,247

993

855

1,082

993

Source: Property Economics

TABLE 6: NUMBER OF FEASIBLE ASSISTED HOMES BUILT UNDER OPTION 1

Assisted

Assisted Housing 10%

Assisted Housing 5%

Housing

30% Discount

50% Discount

30% Discount

50% Discount

Johnsonville

47

38

19

18

Tawa

13

10

7

5

Te Aro

28

28

12

12

Total

88

76

38

35

Source: Property Economics

W: www.propertyeconomics.co.nz

6

52114.1

2.2.

INCLUSIONARY ZONING OPTION 2

As with the first inclusionary zoning option, we have assessed four different scenarios which are

as follows:

Scenario 1: Up to 50% of the additional homes is contributed to assisted housing at a

30% discount.

Scenario 2: Up to 50% of the additional homes is contributed to assisted housing at a

50% discount.

Scenario 3: Up to 25% of the additional homes is contributed to assisted housing at a

30% discount.

Scenario 4: Up to 25% of the additional homes is contributed to assisted housing at a

50% discount.

TABLE 7: COMPARISON OF OPTION 2’S IMPACT ON FEASIBLE CAPACITY

Assisted Housing

Feasible

Without

Assisted Housing 50%

25%

Assisted

Capacity

Housing

30%

50%

30%

50%

Discount

Discount

Discount

Discount

Johnsonville

851

1,087

607

1,411

1,249

Tawa

205

369

148

635

527

Te Aro

2,315

3,207

2,809

3,653

3,531

Total

3,371

4,663

3,564

5,699

5,307

Source: Property Economics

W: www.propertyeconomics.co.nz

7

52114.1

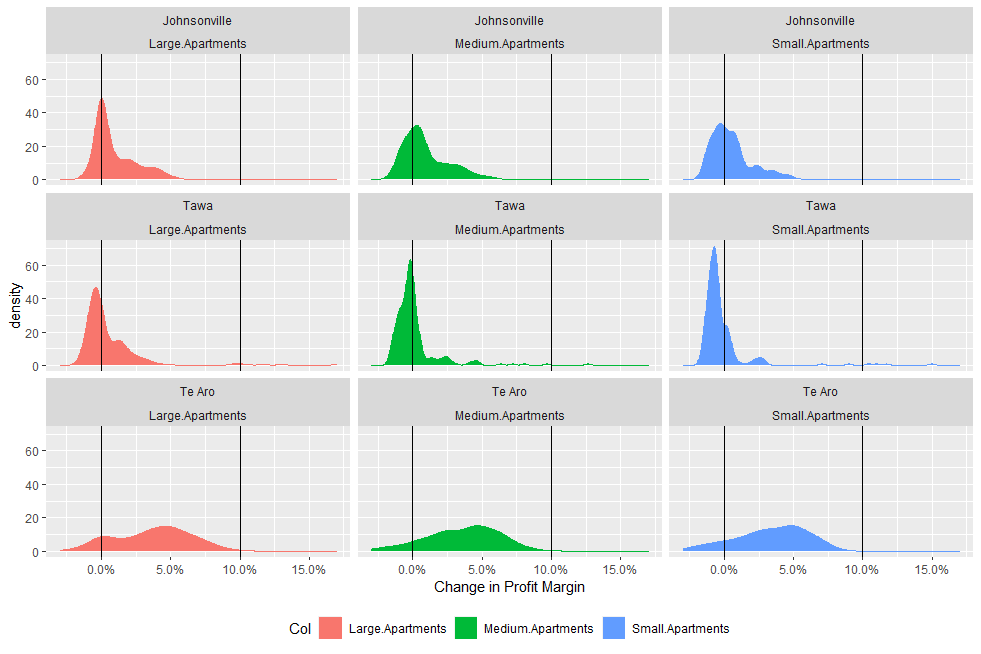

FIGURE 1: IMPACT OF INCLUSIONARY ZONING OPTION 2 ON NET PROFIT % - SCENARIO 1

Source: Property Economics

TABLE 8: NUMBER OF FEASIBLE ASSISTED HOMES BUILT UNDER OPTION 2

Assisted

Assisted Housing 50%

Assisted Housing 25%

Housing

30% Discount

50% Revenue

30% Discount

50% Revenue

Johnsonville

82

5

54

42

Tawa

19

0

26

21

Te Aro

212

108

88

72

Total

313

113

168

135

Source: Property Economics

W: www.propertyeconomics.co.nz

8

52114.1

APPENDIX 1 – DEVELOPMENT SITE MAPS

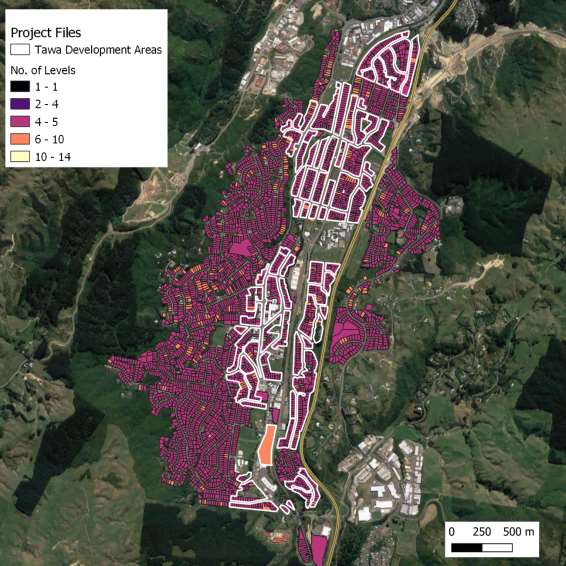

FIGURE 2: TAWA DEVELOPMENT AREAS

Source: Property Economics

W: www.propertyeconomics.co.nz

9

52114.1

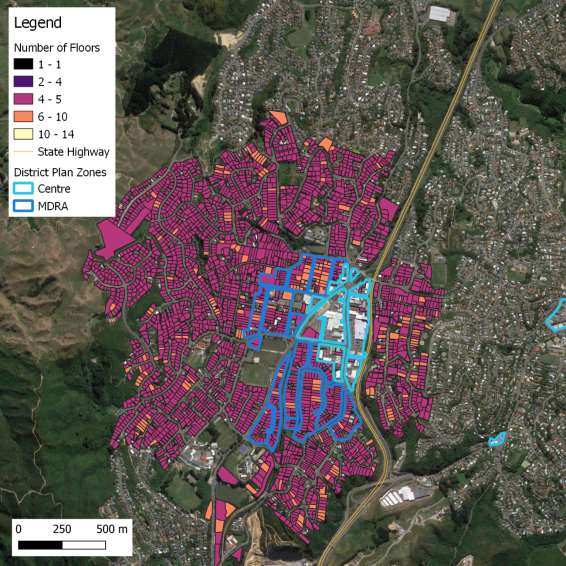

FIGURE 3: JOHNSONVILLE DEVELOPMENT AREAS

Source: Property Economics

W: www.propertyeconomics.co.nz

10

52114.1

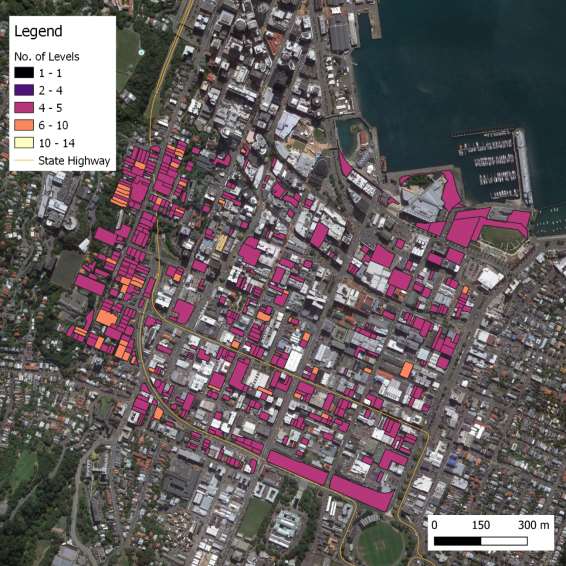

FIGURE 4: TE ARO DEVELOPMENT AREAS

Source: Property Economics

W: www.propertyeconomics.co.nz

11