Report

MACC - EECA Programme 2B Energy Efficiency Review

(Building Services)

Prepared for Wellington City Council

By Beca Ltd

3 June 2016

/

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

Revision History

Revision Nº

Prepared By

Description

Date

1

Shaan Cory

Issued for information

7 June 2016

2

3

4

5

Document Acceptance

Action

Name

Signed

Date

Prepared by

Shaan Cory

2 June 2016

Reviewed by

Ben Masters

3 June 2016

Approved by

Ben Masters

7 June 2016

on behalf of

Beca Ltd

© Beca 2016 (unless Beca has expressly agreed otherwise with the Client in writing).

This report has been prepared by Beca on the specific instructions of our Client. It is solely for our Client’s use for the purpose for which

it is intended in accordance with the agreed scope of work. Any use or reliance by any person contrary to the above, to which Beca has

not given its prior written consent, is at that person's own risk.

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // i

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

Executive Summary

The following is a summary overview of the selected building services energy efficiency opportunities assessed as part of the EECA Programme 2B energy efficiency advisory service for the proposed Museum and Convention

Centre (MACC) project. The energy efficiency review has used computer simulation modelling to benchmark annual energy use savings against a theoretical baseline building model.

Table 1 - Comparison of Building Services Energy Efficiency Opportunities

Annual Energy and Emissions Savings Benchmark

Financial Performance Indicator

Scenario

Description

Energy Use

kWh/m² per

Tonnes CO2-

Indicative

Payback

kWh per yr

$ per year

20 year NPV3

20 year IRR

(kWh/m²)

yr

e/ year

Capital Cost1

Period2

1

l

Baseline: EECA 2A report Combined Enhanced Envelope

278

-

-

-

-

-

-

-

-

tro

2

n

Baseline + Daylight Harvesting in FOH Areas

277

1

12,000

$ 1,600

2

$21k

12 years

$800

7.0%

3

Co

s

Baseline + Economiser

274

3

51,000

$ 7,000

7

$5k

1 years

$89,000

142.5%

e

ti

4

i

n

Baseline + Exhaust Air Heat Recovery

272

6

96,000

$ 5,000

22

$20k

5 years

$42,000

25.2%

5

HVAC

rtu

Baseline + Demand Control Ventilation (DCV)

258

20

312,000

$ 14,000

71

$15k

2 years

$174,000

96.8%

o

6

d

p

Baseline + Movie Museum Gallery HVAC Off Overnight

250

27

429,000

$ 42,000

78

$0k

0 years

$561,000

NA

e

c

p

n

O

a

Combined HVAC Control Opportunities (Baseline +

7

h

233

44

700,000

$ 60,000

134

$61k

2 years

$742,000

101.0%

En

Scenarios 2, 3, 4, 5 and 6)

8

n

Scenario 7 + Condensing Loop Heat Pump

232

1

13,000

$ 500

3

$40k

80 years

-$34,000

-9.0%

ig

9

s

Scenario 7 + Magnetic Bearing Water Cooled Chiller

231

2

38,000

$ 4,000

7

$118k

30 years

-$67,000

-1.7%

De

t

Scenario 7 + Low Specific Fan Power (SFP) Central Air

10

n

225

9

136,000

$ 15,000

23

$17k

1 years

$284,000

134.9%

ie

Handling

c

s

11

fi

e

iti

Scenario 7 + Variable Speed Cooling Tower

216

18

278,000

$ 28,000

50

$10k

1 years

$361,000

280.1%

12

Ef

n

y

Scenario 7 + Air Sourced Heat Pump

216

18

278,000

$ 5,000

44

$39k

7 years

$31,000

14.4%

rtu

13

rg

o

e

Scenario 7 + Waste Water Heat Pump

215

19

293,000

$ 7,000

47

$264k

38 years

-$174,000

-3.5%

p

n

p

14

Scenario 7 + Variable Volume Condensing Water Loop

211

22

351,000

$ 35,000

62

$50k

2 years

$419,000

72.6%

E

O

15

d

e

Scenario 7 + Energy Piles

203

30

475,000

$ 47,000

85

$303k

6 years

$338,000

17.2%

c

n

Combined Efficient Design Opportunities (Scenario 7 +

16

a

165

69

1,079,000

$ 86,000

188

$419k

6 years

$495,000

17.8%

h

Scenarios 10, 11, 12, 13, and 15)

En

17

Scenario 16 + Roof Mounted Photovoltaics

149

16

250,000

$ 25,000

45

$344k

12 years

-$10,000

6.2%

The findings are as follows:

The combined savings of implementing Daylight Harvesting, Economiser, DCV, Exhaust Air Heat Recovery, and switching the Movie Museum Galleries HVAC Off overnight is indicated as a substantial reduction of 44kWh/m2 per

year and 134 tonnes of associated Greenhouse Gas (GHG) emissions per year. The opportunities indicate a payback period of 2 years, with a NPV of approximately $740K and an IRR of 101% across a 20 year period.

Further energy reductions can be achieved by installing Variable Speed Cooling Tower Fans, a Variable Volume Condensing Water Loop, an Air Sourced Heat Pump, Energy Piles and designing for a Low SFP central air

handling (includes efficient motors). The combination of the these opportunities is indicated to reduce energy consumption by 69kWh/m2 per year, $86K of cost savings per year, and a reduction of 188 tonnes of associated GHG

emissions per year. They are indicated to have a short payback period of 6 years, even with the low energy rates WCC are currently paying. The 20 year NPV is indicated to be just under $500K with an IRR of 17.8%, which

suggests these options would result in a favourable return on investment.

Incorporating the combined envelope measures outlined in the EECA 2A report, the combined HVAC controls and combined HVAC design opportunities is indicated to reduce energy consumption by approximately 40%

(125kWh/m2 per year, $150k of cost savings per year, and a reduction of 365 tonnes of associated GHG emissions per year). The 40% reduction in energy consumption is indicated to have a short payback period of under 5

years and an indicative 20 year NPV of over $1 million dollars with an IRR of over 20%. All suggesting that the combination of the building envelope and system options would result in a favourable return on investment. These

figures exclude roof mounted PV which should be considered given the visual statement and marketing opportunity a PV installation would represent.

High efficiency motors will be specified during the selection process. For example, selections with EC motors will be undertaken as EC motors have mid-high 90% efficiencies. Note: the 60-70% efficiency displayed on the AHU

fan data sheets provided by suppliers represent the total efficiency of the entire fan assembly, which takes into account the EC motor efficiency, the fan scroll efficiency and any losses.

1

Based on indicative increased capital cost over baseline option. Order of capital costs TBC by Cost Consultant. Excluding GST, contractor P+G and margins, contingency allowance, and professional fees. These estimates are for comparison purposes

only, and not to establish construction budget or estimate operating expenses. 2

Based on WCC electricity rate of 10ȼ/kWh and gas rate of 5ȼ/kWh with a 2.5% annual inflation rate assumed

3

Assumes a 6.5% discount rate

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // i

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

Contents

1 Introduction

3

2 Project Description

3

2.1

MACC

3

3 Energy Efficiency Overview

4

3.1

Efficiency Optimises Lifetime Costs

4

3.2

Energy Efficiency Adds Value

4

4 Computer Simulation Models

4

4.1

Weather File

4

4.2

Baseline Model

4

5 Energy Efficiency Opportunities

6

5.1

Control Opportunities

6

5.2

Design Opportunities

6

6 Findings

7

7 Financial Analysis

9

8 Comments & Recommendations

10

9 Energy Management

11

10 Next Steps

11

Appendices

Appendix A – Computer Simulation Model Inputs

Appendix B – Financial Performance Analysis

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // ii

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

1

Introduction

2

Project Description

This energy efficiency advisory service has been requested by Wellington City Council (WCC) to review selected

2.1

MACC

energy efficiency opportunities available to the proposed Museum and Convention Centre (MACC). The scope of

services provided aligns with the objectives of the Energy Efficiency & Conservation Authority (EECA)

WCC is planning to construct a new MACC with an approximate useable floor area of 15,751m2. MACC is a 5

Programme 2B Advisory service requirements.

storey building. The lower four floors consist of two 10m high floor to ceiling mezzanine split levels that house the

museum exhibits. The top floor houses the convention centre. MACC is comprised of:

As summarised by EECA:

11 large exhibition pieces

The objective of Programme 2B is to ensure that energy efficiency features [Building Services]

are incorporated

1,100 person convention centre,

into the more detailed design and construction of the Building. Where the Building has been part of a Programme

Kitchen,

2A Project, it will be important that the recommendations from the Programme 2A report are included in the

detailed design and construction (if possible).

Offices, and

Lobby area.

The EECA Programme 2A report has been carried out in parallel with this report and is focussed on an energy

efficient building envelope.

Figure 1 shows that MACC is located across the street from Te Papa and situated between three existing

buildings.

The energy efficiency review uses computer simulation modelling to benchmark the energy performance benefit

of selected energy efficiency opportunities against a theoretical baseline model and the proposed design.

Project summary details are as follows:

Each opportunity has been considered purely from an energy, Greenhouse Gas (GHG) emissions and energy

Location: Cable Street, Wellington

cost perspective only. Other criteria including internal environmental quality (e.g. occupancy thermal comfort, air

Client: Wellington City Council

quality, daylight availability, access to external views etc), architectural, construction, cost, emissions, cleaning,

Design Stage: Preliminary Design

safety in design and all other aspects which inform to the performance and aesthetic requirements of the building

design should be considered separately by the project team.

N

Limitations

This study has been prepared for the purposes of helping to inform the development of the building design. The

computer simulation models are only intended to help inform the building design and the predicted values may

overestimate or underestimate the actual building performance in use. Note that the energy benchmark

calculations use standard benchmarking criteria for occupancy, lighting, power and plant usage and benchmark

weather data. Actual operating variables will differ in reality (e.g. weather, fitout and usage patterns, blinds

control etc.). We point out that the weather files used for the computer simulations represent a typical weather

year only and does not account for periods of unseasonably high (or low) temperature or humidity.

The energy benchmarks are not an estimate of predicted energy use and as such cannot be guaranteed that the

actual building energy use will be within the target limits as this will be determined by many variables, including

those listed above.

All costs are high level estimates only based on suppliers quotes and may not reflect the actual costs. These will

need to be confirmed by further design and the project quantity surveyor.

Figure 1 – Proposed site location on the existing Cable Street site

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 3

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

3

Energy Efficiency Overview

4

Computer Simulation Models

Commercial and industrial buildings account for around 8% of New Zealand’s total energy consumption a year,

A 3D computer simulation model was created for the building using IES Virtual Environment software. IES

and 5% of total CO2 emissions.

simulation software is of the dynamic thermal simulation type that is capable of predicting building thermal

performance and estimating annual energy consumption in a building.

Studies have shown there can be as much as a ten-fold difference in actual energy consumption between similar

buildings with design and construction-related issues and operational issues the main contributors to the

The program is based upon finite difference methods as recommended by CIBSE Part A for energy and

differences.

environmental modelling to model the transmission and storage of heat in the building fabric.

3.1

Efficiency Optimises Lifetime Costs

The thermal model was created using IES Virtual Environment Version 2015. This has been independently

verified to meet ANSI/ASHRAE Standard 140-2004 (Building Thermal Envelope and Fabric Test Loads)

Designing energy-efficient buildings makes sense on a number of levels – not the least of which is the overall

performance criteria. The

Apache HVAC module has been used to accurately simulate Heating, Ventilation, and

economics.

Air-Conditioning (HVAC) energy.

Typical costs relative to initial construction costs over the life of a typical building are:

Environmental consultant fees

0.01 to 0.03

4.1

Weather File

Professional fees

0.10 to 0.15

Each model has been simulated using the NIWA Wellington TMY2 weather file (Data Source - TMY2 NIWA

Construction costs

1.00

18234 D14482 WMO Station 934360). This represents a historical average year of Wellington weather data as

Energy, operating and maintenance costs 3.00

recorded at the Kelburn weather station. It must be noted that the weather data does not account for any

Business costs (salaries, rental/space)

200.00

unseasonable weather conditions and does not account for any localised micro climate effects at the site

Even taken together the design fees and costs of construction are a small portion of total lifetime costs of a

location.

building. Focusing on these initial construction costs alone will almost certainly result in a project that does not

optimise its lifetime costs.

4.2

Baseline Model

The thermal envelope has been modelled to represent the combined EECA 2A proposed building thermal

The extra initial cost of letting the architects and engineers evaluate the design thoroughly and determine an

envelope performance:

energy-efficient outcome is an investment that should repay itself many times over the life of the building.

External walls: R 2 m2.K/W (including thermal bridging effects)

Business costs are by far the most significant lifetime cost of a project, and to influence them, the potential effect

Roof: Total R-value: R 3 m2.K/W (including thermal bridging effects)

of a building on the productivity and health of its users must be taken into account.

R 1.3 ground floor

Vision Glazing:

Energy-efficient design can also play a significant role in providing healthier, more productive environments. For

– Uwindow: U 3.0 W/m2.K (including frame effect)

example:

– Shading Coefficient: 0.40

–

Increased levels of thermal insulation results in improved winter thermal comfort

G value: 0.35

External shading to control summer cooling loads also reduces direct solar gain which may cause discomfort

for building occupants. Well-designed shading also means users do not need to use their blinds as much,

The baseline model includes the external solar shading surrounding the building and the adjacent buildings.

allowing more access to daylight and exterior views.

The baseline model has full air conditioning to all occupied areas with a combination of centralised Variable Air

Energy-efficient high frequency lighting may reduce headache producing flicker

Volume (VAV) Air Handling Units (AHU) with zone reheat and a 4 pipe fan coil unit system providing heating and

3.2

Energy Efficiency Adds Value

cooling via a water cooled chiller plant and gas boiler plant (condensing type). Mechanical ventilation is provided

as per the current design provision. Internal lighting is assumed to be predominantly provided by LED lighting

All stakeholders in the building stand to gain from more energy-efficient design.

technology. HVAC plant and equipment efficiencies align with the Department of Building and Housing’s

Guidelines for Energy Efficient HVAC plant (MEPS).

Owners/occupiers and building users enjoy lower operating costs, and potentially greater operational flexibility

and an environment that encourages greater productivity. The benefits also contribute to the long-term value of

The operating and occupancy profile used in the model has been set to align with the forecast average 10 year

the asset for owners and portfolio holders.

projection for movie museum usage from “Wellington City Council - Indicative business case for a new movie

museum” document from November 2015 and projected year 5 convention centre usage from “Wellington City

The benefits of energy efficiency wil become more obvious and more valuable as energy costs rise, employees’

Council - Indicative business case for a new convention centre” document from December 2015.

pressure for healthier environments increases, regulation becomes a more distinct possibility and overall

environmental awareness improves.

Further details of the baseline computer model inputs are described in Appendix A.

Sample images of the 3D computer model can be seen in the following figures:

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 4

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

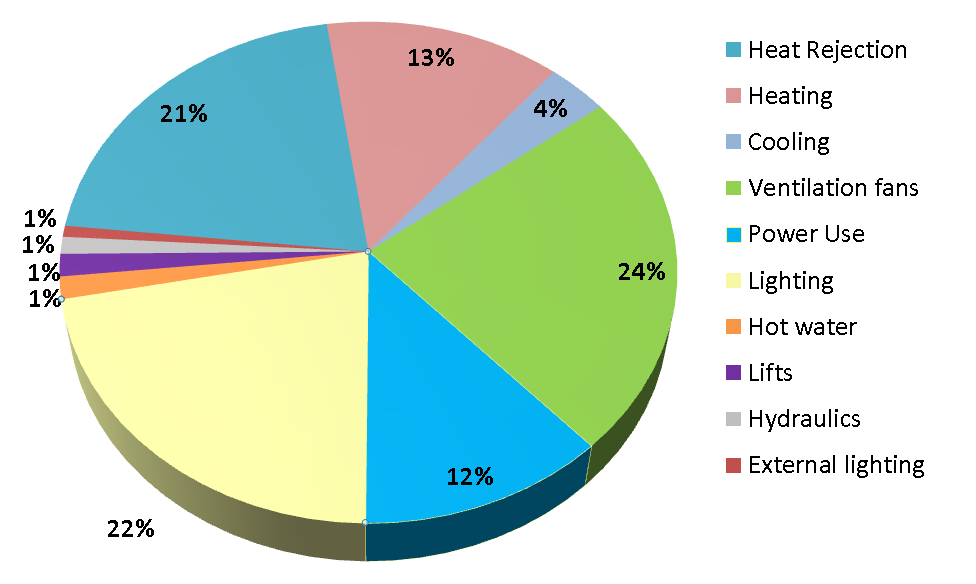

Benchmark Energy End Use Breakdown

Adjacent Buildings

The benchmark annual energy end-use breakdown for the theoretical baseline model can be seen in the

following figure:

Solar Shading

Figure 2 - Computer simulation model showing proposed façade design, view from north.

Figure 4 - Baseline Model, Benchmark Energy End Use Breakdown

It can be seen that heating, cooling, ventilation fans, and heat rejection energy makes up 62% of the annual

energy use for the baseline model. Ventilation fans energy is the highest HVAC end use at 24% and is

comprised of AHUs, supply air fans, fan coil units, and miscellaneous extract fans (e.g. toilets, kitchen exhaust,

back of house etc). Heat rejection energy is the second largest energy user at 21% of overall energy and is

comprised of the cooling tower fans and the condensing circuit’s pumps. In the baseline model, the heat rejection

operates at a constant speed, regardless of the cooling load. Heating energy is 13% and is comprised of outdoor

air heating and space heating. Cooling energy accounts for only 4% due to the efficiency of the Baseline water

cooled chiller.

The lighting and power (for computers, kitchen equipment and other equipment) makes up a further 34% of the

annual energy usage. The baseline model assumes LED lighting and typical use of lighting and power with a low

level of energy management being employed by building users. The energy use attributed to computers and

other appliances can be a large variable and should be benchmarked as the design and Furniture, Fixtures and

Equipment (FFE) stage progresses. The simulations have assumed equipment efficiency is not overly energy

efficient at this stage but we recommend that an energy efficient equipment specification is targeted.

The remaining 4% of energy usage is for hydraulics, lifts, and external lighting.

Figure 3 - Computer simulation model showing proposed façade design, view from south

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 5

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

5

Energy Efficiency Opportunities

Variable speed cooling tower fans: Cooling tower fans which run constantly can over cool the condenser

water. A variable speed drive is installed and varies the cooling tower fan speed to only cool the condensing

water to the temperature the chiller is requesting. This in turn reduces the cooling tower fan energy

The following Programme 2B energy efficiency opportunities were identified by WCC and Beca.

consumption.

Variable volume condenser water loop: Condensing water loop pumps which run constantly can over cool

5.1

Control Opportunities

the condenser water. A variable speed drive is installed and varies the Condensing water loop pumps to only

cool the condensing water to the temperature the chiller is requesting. This in turn reduces the condensing

The potential energy saving performance of a number of energy efficient HVAC controls opportunities were

water loop pump energy consumption.

initially assessed against the baseline model as follows:

Low Specific fan power central air handling: Specific fan power is a measurement of the electric power

Demand Controlled Ventilation (DCV): Outside air supply is delivered only as required to achieve the

that is needed to drive a fan, relative to the air volume that is circulated through the fan. SFP is measured in

required level of air quality (as opposed to 100% of design capacity during all occupied hours). Air quality

Watts per litre per second (W/l.s). Fan energy consumption will reduce by designing the ventilation system

sensors monitor air quality levels to determine the level of outdoor air rate required.

which has lower static pressure. The design takes advantage of larger duct sizes to reduce friction. As an

Economiser: The Economiser is used if the HVAC system zone is requesting cooling and the outdoor air

example, the table below displays the impact having a lower static pressure has on fan power.

temperature is cool enough to directly provide the zone cooling requirements.

HVAC Off Overnight: Switch the HVAC off overnight in the Movie Museum Galleries and let the temperature

Fan Static

Power Input

drift outside of the heating and cooling temperature set points. The Convention Centre already switches off

800 Pa

3.7 kW

overnight.

900 Pa

4.2 kW

1000 Pa

4.6 kW

Exhaust Air Heat Recovery: Install a run around coil to recover heat from exhausted air to preheat incoming

outdoor air which is supplied to the Fan Coil Unit system (Lobby areas). Additional pipework connected from

the exhaust duct to the supply air duct

before the Air Handling Units heating coil is required.

High efficiency motors will be specified during the selection process. For example, selections with EC motors

will be undertaken as EC motors have mid-high 90% efficiencies. Note: the 60-70% efficiency displayed on

Daylight harvesting to FOH areas: Install electric light dimming in perimeter lobby and convention centre

exhibition areas. Lighting energy use has been reduced to account for daylight levels in FOH perimeter areas

the AHU fan data sheets provided by suppliers represent the total efficiency of the entire fan assembly, which

to simulate automated light dimming controls

takes into account the EC motor efficiency, the fan scroll efficiency and any losses. This is for a total system,

not just the motor only.

Combined HVAC Control Opportunities: All of the five opportunities above were simulated together.

Combined Opportunities: The following selected opportunities were simulated together:

– Air Sourced Heat Pump

5.2

Design Opportunities

– Energy Piles

–

The above Combined Control Opportunities form a new scenario which the potential energy saving performance

Variable Speed Cooling Towers

of a number of additional enhanced building services design opportunities were separately assessed against, as

– Variable Volume Condensing Water Loop

follows:

– Low Specific Fan Power Central Air Handling

Magnetic Bearing Water Cooled High Efficiency Chillers: The efficiency gains in a magnetic bearing

Roof Mounted Photovoltaic Array: Photovoltaics are a renewable energy generation source which converts

chiller are attained from a

reduction in the energy losses associated with friction. The reduced energy losses

solar radiation into electricity. It is proposed to install a 160kW array over 50% of the MACC roof area.

increase the heat transfer efficiency of the chiller. This is because no oil is used in the chiller. Also, a variable

speed drive on the motor allows the compressor to operate much more efficiently at partial loads than

standard compressors.

Waste Water Sourced Heat Pump: A Waste Water Sourced Heat Pump absorbs heat from waste water

(sewage) and transfers the heat to the building through the refrigerant cycle in a heat pump. The Waste

Water Heat Pump scenario has a Sewage SHARC to remove solid waste and makes the waste water usable

as a heat source.

Condenser loop water sourced Heat Pump: Similar to the Waste Water Sourced Heat Pump, the

condensing loop water is used to absorb heat and transfer the heat to the building through the refrigerant

cycle in a heat pump. A condensing loop Heat Pump can only be used when there is a coincident cooling load

equal to or greater than the heating load.

Air Sourced Heat Pump: Similar to the waste water sourced heat pump, the outside air is used to extract

heat and transfer the heat to the building through the refrigerant cycle in a heat pump.

Energy Piles (Ground sourced heat rejection through piles): Energy Piles use the ground as an energy

transfer medium, in this case as a medium to reject heat. Energy Piles reduce the cooling energy

consumption because it uses the ground as a means to cool the condensing water for free without requiring

cooling tower fans (pumps for water circulation through piles are still required). If the ground cannot cool the

condensing water entirely, the cooling tower would be used. The assessment has assumed that 2 loops of

piping were run through the 37 piles that are 1m or larger in diameter with an estimate heat rejection capacity

of 110kW.

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 6

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

6

Findings

Each computer model scenario has been simulated over a typical Wellington weather year and the annual energy benefit of each energy efficiency opportunity is separately compared to either the baseline model or the proposed

Combined Load and Controls Opportunities scenario which forms a new baseline to measure the energy efficient design opportunities against. The findings are as follows:

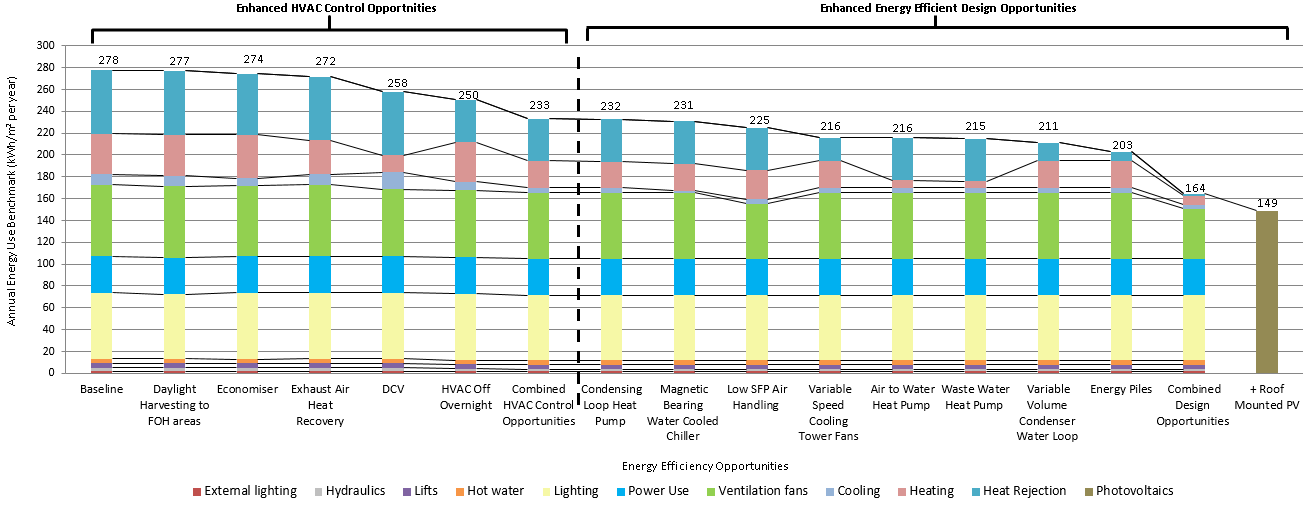

Figure 5 – Annual Energy Use Benchmark Comparison

DCV and Switching the Movie Museum Gallery HVAC Off overnight are indicated to produce the largest

It is indicated that large energy savings are offered by designing the heat rejection system to be more energy

energy savings from a controls perspective. DCV is indicated to save 20kWh/m2 a year, and switching the

efficient:

HVAC Off overnight 27kWh/m2 a year.

– Variable speed cooling towers is suggested to reduce energy consumption by 18kWh/m2 a year and GHG

Combining the HVAC control opportunities is indicated to reduce energy consumption by 44kWh/m2 a year,

emissions by 50 tonnes per year.

lower GHG emissions by 134 tonnes per year, and reduce energy costs by approximately $60K per year.

– A Variable volume condensing water loop is indicated to reduce energy consumption by 19kWh/m2 a year

The various heat pump options all reduce energy consumption, with the Air Sourced (18kWh/m2.yr) and Waste

and GHG emissions by 62 tonnes per year.

Water (19kWh/m2.yr) Heat Pumps being indicated to provide a large amount of annual energy savings. Both

It is indicated that installing Energy Piles would be the single largest energy saver. Energy piles reduce energy

the air sourced and waste water heat pumps have the potential to reduce GHG emissions by over 40 tonnes

consumption by 30kWh/m2 a year and GHG emissions by 80 tonnes per year.

per year.

Combining the design options which provide a favourable return on investment (Low SFP, Variable Speed

Upgrading the water cooled chiller to a magnetic bearing option may reduce energy by only 2kWh/m2 per year

Cooling Tower Fans, Variable Volume Condensing Water Loop, Air Sourced Heat Pump, and Energy Piles) is

largely due to the already high efficiency of standard water cooled chillers.

indicated to reduce energy consumption by 69kWh/m2 per year and GHG emissions by 188 tonnes per year.

By designing the central ventilation systems to minimise pressure loss can lead to 9kWh/m2 per year worth of

A roof mounted PV system covering 50% of the MACC roof area can generate 16kWh/m2 per year and

energy savings. This equates to 23 tonnes of GHG emissions.

equates to approximately 45 tonnes of GHG emissions. Installing PV presents a visual statement that WCC

and the MACC development is sustainability and environmentally focussed.

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 7

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

Table 2 – Annual Energy Savings Benchmark Summary

Enhanced HVAC Control Opportunities

Enhanced Energy Efficient Design Opportunities

Magnetic

Variable

Variable

Annual Energy and

Daylight

Exhaust

Combined

Condensing

Bearing

Low SFP

Speed

Air to

Waste

Volume

Combined

Roof

Emissions Savings

HVAC Off

Energy

Harvesting

Economiser

Air Heat

DCV

HVAC Control

Loop Heat

Water

Air

Cooling

Water Heat

Water Heat

Condenser

Design

Mounted

Benchmark

Overnight

Piles

to FOH

Recovery

Opportunities

Pump

Cooled

Handling

Tower

Pump

Pump

Water

Opportunities

PV

areas

Chiller

Fans

Loop

kWh/m2 per year

1

3

6

20

27

44

1

2

9

18

18

19

22

30

69

16

kWh per year

12,000

51,000

96,000

312,000

429,000

700,000

13,000

38,000

136,000

278,000

278,000

293,000

351,000

475,000

1,079,000

250,000

$ per year

$1,600

$7,000

$5,000

$14,000

$42,000

$60,000

$500

$4,000

$15,000

$28,000

$5,000

$7,000

$35,000

$47,000

$86,000

$25,000

Tonnes CO2-e/ year

2

7

22

71

78

134

3

7

23

50

44

47

62

85

188

45

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 8

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

7

Financial Analysis

Air Sourced Heat Pump ($39K): Based on additional costs of purchasing a 150kW air sourced heat pump @

$40K, minus the cost of the 150kW boiler it is replacing @$11K, and an additional hot water circuit for

Domestic Hot Water @$10K.

This section compares the financial performance of each energy efficiency opportunity. Please refer to Appendix

Waste Water Heat Pump ($264K): Based on additional costs of purchasing a 150kW water sourced heat

B for detailed financial analysis of each enhanced energy efficiency opportunity identified over the baseline.

pump @ $42K, minus the cost of the 150kW boiler it is replacing @$11K, an additional hot water circuit for

Domestic Hot Water @$10K, and the additional cost of the Sewage SHARC component @$223K.

The following indicative capital costs have been estimated by Beca energy modelling team generally based on

Energy Piles ($303K): Based on additional costs of piping, pumps, pile detailing, and additional non-steel

previous project experience and supplier costs, however we recommend these are each confirmed by the project

casing concrete pile construction costs for the 39 proposed piles greater than 1m in diameter @ $303K

cost consultant:

(contractor’s estimate of an additional 20% to pile construction costs).

Daylight Harvesting to FOH Areas ($21K): This allows for the installation of daylight sensors, wiring,

Combined Design Opportunities ($419K): The combined capital cost increase of the selected

controllers and associated controls programming

opportunities: Low SFP, Variable Speed Cooling Tower Fans, Variable Volume Condensing Water Loop, Air

Economisers ($5K): This allows for the inclusion of wiring and associated BMS programming to the VAV

Sourced Heat Pump, and Energy Piles.

AHUs.

Roof Mounted PV ($344K): Based on installation costs of purchasing a 160kW PV system @ $2,150 per

Exhaust Air Heat Recovery ($20K): Additional costs of run around coils, piping and extra pumps of

kW.

additional circuit, and larger fans to compensate for higher pressure drop across the additional heat recovery

coils.

The current WCC energy rates have been used as follows:

Demand Controlled Ventilation (DCV) ($15K): This allows for the installation of air quality sensors, wiring

Electricity: $0.10 per kWh

and associated BMS programming

Natural gas: $0.05 per kWh

HVAC Off overnight ($0): No additional cost for switching off HVAC overnight as it is a Building

Management System (BMS) schedule change.

The payback periods have been compared based on the following calculation while taking account of typical

Combined HVAC Control Opportunities ($61K): The combined capital cost increase of the selected

rates of inflation:

opportunities: Daylight Harvesting, DCV, Exhaust Air Heat Recovery, Economiser, and HVAC Off Overnight.

Condensing Loop Heat Pump ($40K): Based on additional costs of purchasing 62kW Water Sourced Heat

Payback Period (in years) = Initial Investment Cost / Annual Operating Savings

Pump @ $30K and associated pipework and controls @$10k.

Magnetic Bearing Water Cooled Chillers ($118): Based on additional costs of purchasing two 1200kW

Note that the following considerations have been allowed for in these calculations:

magnetic bearing water cooled chillers @ $277K each compared to two typical York centrifugal 1200kW

Any reduction in heating or cooling plant or equipment costs as a result of each energy efficiency opportunity

water cooled chillers @$218K each. No maintenance cost savings have been incorporated.

has not been considered

Low SFP ($16K): Based on additional costs of purchasing larger duct sizes @ $426K to reduce static

An annual 2.5% inflation increase has been used as instructed by WCC

pressure by 20% to achieve a SFP of 2W/l.s compared to smaller duct sizes @$410K which have 20% higher

A 6.5% discount rate has been used as instructed by WCC

static pressure and have a SFP of 2.5W/l.s.

Maintenance costs have been excluded

Variable Speed Cooling Tower Fans ($10K): This allows for the installation of VSDs, to include wiring and

Potential to send any excess power generated by PVs back to the electrical grid

associated BMS programming.

Variable Volume Condenser Water loop ($50K): This allows for the installation of VSDs to Condensing

A summary of the financial analysis can be seen in the following table:

Water pumps and includes wiring, associated BMS programming, and additional cost of indirect cooling

towers versus direct cooling tower.

Table 3 – Financial Analysis Summary

Enhanced HVAC Control Opportunities

Enhanced Energy Efficient Design Opportunities

Financial

Daylight

Variable

Air to

Waste

Variable

Exhaust

Combined

Condensing

Magnetic

Low SFP

Combined

Roof

Performance

Harvesting

HVAC Off

Speed

Water

Water

Volume

Energy

Indicator

Economiser

Air Heat

DCV

HVAC Control

Loop Heat

Bearing Water

Air

Design

Mounted

to FOH

Overnight

Cooling

Heat

Heat

Condenser

Piles

areas

Recovery

Opportunities

Pump

Cooled Chiller

Handling

Opportunities

PV

Tower Fans

Pump

Pump

Water Loop

Indicative

$21k

$5k

$20k

$15k

$0k

$61k

$40k

$118k

$17k

$10k

$39k

$264k

$50k

$303k

$419k

$344k

Capital Cost4

Payback

12 years

1 years

5 years

2 years

0 years

2 years

80 years

31 years

1 years

1 years

7 years

39 years

2 years

6 years

6 years

12 years

Period5

20 year NPV6

$800

$89,000

$42,000

$174,000

$561,000

$742,000

-$34,000

-$67,000

$284,000

$361,000

$31,000

-$174,000

$419,000

$338,000

$495,000

-$10,000

20 year IRR

7.0%

1

42.5%

25.2%

96.8%

NA

101.0%

-9.0%

-1.7%

134.9%

280.1%

14.4%

-3.5%

72.6%

17.2%

17.8%

6.2%

4

Based on indicative increased capital cost over baseline option. Order of capital costs TBC by Cost Consultant. Excluding

GST, contractor P+G and margins, contingency allowance, and professional fees. These estimates are for comparison

purposes only, and not to establish construction budget or estimate operating expenses. 5

Based on WCC electricity rate of 10ȼ/kWh and gas rate of 5ȼ/kWh with a 2.5% annual inflation rate assumed

6

Assumes a 6.5% discount rate

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 9

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

8

Comments & Recommendations

8.2.3

Heat rejection

The largest single energy saving option, and also the largest capital cost investment, is indicated to be the

installation of Energy Piles. Energy Piles use the ground as an energy transfer medium, in this case as a

We recommend that WCC considers including the HVAC controls and design opportunities subject to meeting

medium to reject heat. Energy Piles reduce the cooling energy consumption because it uses the ground as a

their investment criteria and the project budget. Consideration should be given to the visual statement and

means to cool the condensing water. Energy Piles would initially cost approximately $300K and offer an annual

marketing opportunity a PV installation would represent

energy cost reduction over $40K per year. Energy Piles are indicated to have a payback period of 6 years, a 20

year NPV of over $337K and an IRR of 17.2%. This suggests Energy Piles would offer a good return on

8.1

Controls Opportunities

investment. If this option is to be pursued, it is recommended to undertake a detailed feasibility study which

determines the make-up of the ground conditions and potentially use a test pile as a means to assess the

Implementing energy efficient HVAC control opportunities in the building services design are indicated to offer

performance of a potential Energy Pile system

significant energy savings when compared to the baseline. The combined savings of implementing Daylight

Harvesting, Economiser, DCV, Exhaust Air Heat Recovery, and switching the Movie Museum Galleries HVAC

Off is indicated to offer 44kWh/m2 per year with a reduction of 134 tonnes of associated Greenhouse Gas (GHG)

8.3

Photovoltaics

emissions. This represents good practice and improves on the baseline (which represents a minimal level of

Installing a roof mounted PV system would represent a visual statement that WCC and MACC development are

energy performance). The HVAC controls opportunities have a payback period of 2 years, an NPV of $740K

sustainability and environmentally focussed. The potential energy generation from the system is indicated to

across a 20 year period and an IRR of 101%. It suggests the options would result in a favourable return on

reduce energy and GHG emissions substantially at 16kWh/m2 and 45 tonnes of GHG per year respectively. The

investment.

payback for installing a PV system is 12 years. The large reduction in emissions and the visual aspect of the

solar collectors on the roof provides a great marketing statement. It is assumed all energy generated is used

8.1.1

HVAC scheduling

onsite.

A high energy saving opportunity is indicated to be offered by switching off HVAC in the Movie Museum

galleries. The payback period for the option is 0 years because it does not require any additional costs.

8.2

Design opportunities

Further energy reductions can be achieved by installing Variable Speed Cooling Tower Fans, Variable Volume

Condensing Water Loop, Air Sourced Heat Pump, Energy Piles and designing for central air handling to have a

Low SFP. The combination of the these energy efficient design opportunities is indicated to provide a further

energy reduction of 69kWh/m2 per year, $86K of cost savings per year, and a reduction of 188 tonnes of

associated GHG emissions. The combined opportunities have a short payback period of 6 years, even with the

low energy rates WCC are currently paying. The 20 year NPV of the combined design opportunities is indicated

to be over $500K with an IRR of 19.8%, which suggests the options would again result in a favourable return on

investment.

8.2.1

Heating source

Of the three different heat pump options (Condensing Water Loop, Air Sourced and Waste Water), the Air

sourced heat pump is the only option that provides a positive NPV over a 20 year period. The Air Sourced Heat

Pump is indicated to have a 7 year payback, a 20 year NPV of approximately $31K and an IRR of 14.6%. The

reason the condensing loop Heat Pump does not financially stack up, with a payback of 64 years, is due to the

limited energy savings it could provide as there is a minimal occurrence of coincident heating and cooling load.

Conversely, the Waste Water Heat Pump offers high energy savings, but the payback is indicated to be 39 years

and is due to the very high capital cost investment required of approximately $263.5K (primarily due to the

Sewage SHARC cost of approximately $223K).

8.2.2

Cooling source

The magnetic bearing water cooled chiller does not provide a favourable return on investment with a payback of

31 years. This is largely due to the low cooling energy load and the low WCC energy costs. The financial

assessment of the magnetic bearing water cooled chiller does not include any cost savings from lower

maintenance costs.

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 10

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

9

Next Steps

10 Energy Management

We propose the following next steps:

While the energy efficiency opportunities identified may offer significant energy savings, it is the operational

stage of a building where energy savings are realised. Implementing an energy management system and

1) Client team to review report & discuss with Beca

organisational plan that meets/exceeds ISO 50-001 (Energy Management) standards will aid in targeting a

reduced energy consumption, carbon emissions and energy costs.

2) Project QS to review energy efficiency opportunities and confirm implementation cost

3) Project team to incorporate energy efficiency opportunities into building design subject to meeting WCC

An energy management system enables an organisation to follow a systematic approach in achieving continual

improvement of energy performance.

investment criteria and project budget

4) Project team to ensure energy efficient plant and equipment selection is retained throughout the design

Having an effective energy management system offers several important opportunities:

and construction phase on the project

Lower operating costs

Improved environmental performance

5) WCC and MACC to consider implementing a comprehensive 2 year building tuning programme (in

Longer equipment life

conjunction with the main contractor and design team) to ensure the building is operating as per the

Better risk management

design intent

More effective, lower cost maintenance (Proactive)

Improved thermal comfort and indoor air quality, and

We recommend WCC and MACC apply for EECA Programme 2C (Commissioning) and 2D (Assessing

Enhance public image

energy performance after occupation) to provide funding assistance with this.

Energy

Energy Management system initiatives include:

Management

Creating a Plan

Cycle

– Energy Policy

– Objectives and Targets

Reviewing the current systems

Identifying improvements

Implementing improvements

Measuring and Verifying improvements

Reviewing the energy management system

The Energy Efficiency and Conservation Authority (EECA) have various funding schemes which help to

implement an effective energy management system:

Energy Management Plan: EECA can potentially fund up to 40% of costs (up to $100,000) for this work

– Setting up a system to manage your energy, including development of an energy policy

– Identifying your main areas of energy use

– Setting an energy-savings target

– Creating plans to prioritise energy-saving opportunities.

Systems Optimisation: EECA can potentially fund up to 40% of costs (up to $100,000) for this work

– Identifying areas for improved energy efficiency

– Tuning and recalibrating existing equipment

Monitoring & Targeting: EECA can potentially fund up to 40% of costs (up to $100,000) for this work

– Implementing a monitoring & targeting system

– Analysing, comparing and benchmarking energy use

– Target setting

– Reporting

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 11

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

Appendix A

Computer Simulation Model

Inputs

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 12

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

Table 4 - Baseline Model Building Services inputs

Model Item

Baseline Energy Model Input

Model Input

Comment

Model Item

Baseline Energy Model Input

Model Input

Comment

Reference

Reference

Design space

Convention Centre Space Plenary,

Project

Building

Based upon SPA architectural

temperature and

Documentation

humidity conditions

Pre-Function, General Office, Meeting

Mechanical

documents: dated 12 April 2016.

Rooms and Movie Museum Galleries:

engineer

23°C Cooling

Beca draft building services

preliminary design as at 6 May

20°C Heating

2016.

Convention Centre BOH Circulation

Thermal simulation

IES Virtual Environment version

CIBSE

18°C Heating

software

2015

Movie Museum BOH Circulation

Weather file for

NIWA Wellington TMY2

Assumed

IWEC files have shown to

18°C Heating

thermal simulation

contain errors in

Kitchen

temperature data

16°C Heating

Outdoor Design

Summer:

NIWA

2.5% design day criteria

conditions

23.6oC DB

Humidity:

18.9oC WB

Not controlled

#hrs exceeded is 45

Winter

Lighting power

Convention Centre:

Project Electrical

LED lighting design

5.2oC

density

Exhibition: 8 W/m2

Engineer.

lighting power density

#hrs exceeded is 110

Plenary: 12 W/m2

Pre-Function: 12 W/m2

Ground solar

0.20

(CIBSE) Assumed

reflectance

General Office Areas: 6 W/m2

Asphalt

Meeting Rooms: 12 W/m2

Modelled spaces

Circulation – Area FOH : 8 W/m2

All conditioned and unconditioned

Architectural

spaces in the building

drawings

Circulation – Area BOH : 5 W/m2

Movie Museum:

Areas for each space taken from

Project

Galleries: 8 W/m2

architectural drawings – 04/05/2016

mechanical

Circulation – Area BOH : 4 W/m2

engineer

Assessed spaces

Conditioned spaces

Project

Energy consumption of

the retail areas is not

Lighting schedule

Mechanical

Office and Museum: NABERS

NABERS

engineer

considered.

Convention Centre: Adapted

Thermal zoning

NABERS for 9am to 10pm operation

Spaces zoned to align with

Project

Peak equipment

Convention Centre:

mechanical system design

Mechanical

CIBSE Guide A

gains

Exhibition: 5 W/m2

engineer

Table 6.2

Plenary: 15 W/m2

Assumptions

Manually controlled

Not modelled

Project

external shading

Pre-Function: 15 W/m2

NABERS

device e.g. solar

Mechanical

General Office Areas: 11 W/m2

control blinds,

engineer

Meeting Rooms: 11 W/m2

external louvres etc

Circulation – Area FOH : 5 W/m2

Automatically

Circulation – Area BOH : 5 W/m2

Not modelled

Project

controlled shading

Movie Museum:

device e.g. solar

Mechanical

Galleries: 5 W/m2

control blinds,

engineer

Circulation – Area BOH : 5 W/m2

external louvres

Equipment

NABERS schedule for equipment is

NABERS

schedule

adapted similar to the lighting

schedule

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 13

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

Model Item

Baseline Energy Model Input

Model Input

Comment

Model Item

Baseline Energy Model Input

Model Input

Comment

Reference

Reference

Process load

Not modelled

Project

Covered under

Outside air

Convention Centre:

Beca design

density

Mechanical

equipment gains

ventilation rate

Exhibition: 8l/s.person

features report

engineer

Plenary: 8l/s.person

Occupancy density

Meeting Rooms: 10l/s.person

Convention Centre

Project business

Represent typical

General Offices: 10l/s.person

Kitchen/Cafe: 5m2 / person

case

diversified density

Circulation – FOH and BOH:

Circulation – FOH and BOH: 5m2/

1l/s.person

person

Kitchen: 8l/s.person

Exhibition: 12m2 / person

Cafe: 10l/s.person

Plenary: 12 m2 / person

Movie Museum:

Meeting Rooms: 12 m2 / person

Museum Gallery spaces:

Office: 15m2 / person

8l/s.person

Lobby: 5m2 / person

Lobby/Circulation: 10l/s.person

Movie Museum:

Gallery: 29m2 / person

Outside air control

Project

No heat recovery or

Museum:

Lobby: 5m2 / person

mechanical

demand controlled

9am to 7pm, 365 Days a year

Occupancy gains

engineer

ventilation

Exhibition, BOH, and Lobby : 75W

CIBSE Guide A

Convention Centre:

sensible, 55W latent

9am to 10pm, 7 days per week

Kitchen:80W sensible 80W latent

Boiler SEER

Outdoor air preheat and

Plenary, Meeting, and Offices:70W

90% (condensing gas fired boiler)

Assumed

4pipe FCU unit heating

sensible 35W latent

NZBC Clause H1

Chiller SEER

Full Load: 5.5 (water source chiller)

New water cooled

Typical water cooled

Occupancy

NABERS schedule for occupancy is

NABERS

chiller plant

chiller efficiency

schedule

Part load: 6.1

adapted similar to the lighting

schedule

Heating Hot Water

HHW design flow temp: 60oC -70oC

Project

Infiltration rate

0.15 ACH all of the time ( 24hour

Project

Loop

HHW design delta T: 10oC

Mechanical

occupancy)

mechanical

HHW pump configuration: Constant

Engineer

engineer

Primary, Variable Secondary

Night purge

Not modelled

Project

ventilation

Chilled Water Loop

CHW design flow temp:6oC -12oC

Project

mechanical

CHW design delta T: 6oC

Mechanical

engineer

CHW pump configuration: Constant

Engineer

Pressurisation

None

Project

Primary, Variable Secondary

requirements

mechanical

engineer

Condensing Water

CDW design flow temp:29oC -35oC

Project

HVAC operating

Museum exhibition: 24/7 all year

Loop

CDW design delta T: 6oC

Mechanical

Project

schedule

round

CDW pump configuration: Constant

Engineer

mechanical

Convention: 8am to 10pm, 7 days

Flow

engineer

per week

1.5 hour optimum start period

Pipe/duct heat

5% allowance

Assumed

Mechanical

loss/gains

Design room temperatures achieved Project

services control

during occupancy hours

mechanical

Pumps

Based on design flow rates

Assumption

strategy

engineer

AHU Fans

16°C preheat temperature

Project

Typical fan efficiency

Heating coil via HHW gas boiler

mechanical

circuit

engineer

10 no. AHU Variable Volume Fans:

– Flow rates sized using IES

ApacheHVAC

– 2.5W/l.s

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 14

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

Table 5 - Baseline Model Architectural inputs

Model Item

Baseline Energy Model Input

Model Input

Comment

Reference

Model Item

Baseline Energy Model Input

Model Input

Comment

Supply Air Fans

18°C preheat temperature

Project

Typical fan efficiency

Reference

Heating coil via HHW gas boiler

mechanical

Site location

As site location

Assumed

circuit

engineer

2 no. fans:

Longitude = 174.80 E

– SAF-01-01: 2,000l/s

Latitude = 37.02 S

– SAF-05-01: 6,000l/s

Site Orientation

As site location

Architectural

2.5W/l.s

plan drawings

Building

Adjacent buildings modelled

Architectural

FCU fans

1 per FCU Zone

Project

Typical AC type FCU fan

Overshadowing

drawings

2.5W/l.s

mechanical

performance

Building Geometry

engineer

As shown on architectural drawings

Architectural

Exhaust Air fans

7 no. fans:

drawings

Project

Typical fan type

–

Building thermal

EAF-01-01: 2,000 l/s

mechanical

performance

External walls: R 2 m2.K/W (including

H1 minimum

Refer to EECA 2A

envelope

– EAF-05-01: 4,000 l/s

engineer

thermal bridging effects)

values

report

– EAF-05-02: 3,500 l/s

Roof: Total R-value: R 3 m2.K/W (including

– EAF-05-03: 2,500 l/s

thermal bridging effects)

– EAF-05-04: 2,500 l/s

R 1.3 ground floor

– EAF-06-01: 2,000 l/s

Vision Glazing:

– EAF-06-02: 6,000 l/s

– Uwindow: U 3.0 W/m2.K (including frame

2.5W/l.s

effect)

Glazing shading

Vision glazing:

NZS4218

Refer to EECA 2A

coefficient

Lifts

– Shading Coefficient: 0.40

report

4 kWh/m2 per year

GreenStar Office

–

Design & Built

G value: 0.35

Internal walls

2009

13mm plasterboard lining, 90mm timber

Architectural

framing, 13mm plasterboard lining

DHW

drawings

4 kWh/m2 per year

GreenStar Office

Intermediate floors

Design & Built

Carpet +underlay, 150mm concrete slab,

Architectural

2009

1000mm ceiling cavity, 13mm plasterboard

drawings

External surface

0.5 (medium coloured) to be assigned to all

Assumed

solar reflectance

external surfaces

External lighting

2 kWh/m2 per year

Assumed

Area of glazing

As per proposed design

Architectural

drawings

Area of frame

10% glazing area

Assumed

Area of skylight/

None

Architectural

clerestory

drawings

Fixed external solar

Fixed Solar Shading modelled as per the

Architectural

Basecase

shading device

proposed design.

drawings

allowance

Manually controlled

Blinds are not operated

Assumed

curtains/blinds

Manually controlled

Not proposed

Assumed

natural ventilation

opening

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 15

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

Table 6 – NABERS lighting schedule

Convention Centre areas:

Museum and Office areas:

12am-

7am-

8am-

9am-

10pm-

11pm-

7am

8am

9am

10pm

11pm

12pm

12am-

7am-

8am-

9am-

5pm-

6pm-

8pm-

9pm-

7am

8am

9am

5pm

6pm

8pm

9pm

12am

Week

0%

15%

60%

100%

50%

15%

Saturday

0%

15%

60%

100%

50%

15%

Week

15%

40%

90%

100%

80%

60%

50%

15%

Sunday

0%

15%

60%

100%

50%

15%

Saturday

15%

40%

90%

100%

80%

60%

50%

15%

Sunday

15%

40%

90%

100%

80%

60%

50%

15%

Table 9 – Energy Efficiency Opportunities

Convention Centre areas:

Model Item

Energy Model Input

Model Input Reference

Switch Movie Museum

HVAC only operates from 8am to 7pm.

Project mechanical engineer

12am-

7am-

8am-

9am-

10pm-

11pm-

7am

8am

9am

10pm

11pm

12pm

HVAC Off overnight

A 1.5 hour optimum start period

Week

15%

40%

90%

100%

80%

50%

Exhaust air heat recovery

Run around coil

Project mechanical engineer

Saturday

15%

40%

90%

100%

80%

50%

50% heat recovery effectiveness

Sunday

15%

40%

90%

100%

80%

50%

Demand Control

Outside air supply reduces to as a percentage

Estimated based on

Ventilation

based on diversified design occupant density

Table 7 – NABERS equipment schedule

European studies. Actual

requirement will be

Museum and Office areas:

dependent on the project and

building occupancy rates

12am-

7am-

8am-

9am-

5pm-

6pm-

7pm-

9pm-

Economiser cycles (free

Up to 20oC outdoor air temperature: when outside

7am

8am

9am

5pm

6pm

7pm

9pm

12am

cooling)

air temperature is lower than indoor air

Week

25%

65%

80%

100%

80%

65%

25%

25%

temperature, the economiser cycle is used.

Saturday

25%

65%

80%

100%

80%

65%

25%

25%

Daylight harvesting to

Sunday

25%

65%

80%

100%

80%

65%

25%

25%

Reduced NABERS office lighting schedule by

NABERS

FOH areas

20% in FOF perimeters areas

Combined HVAC Control

Convention Centre areas:

All of the above

Opportunities

12am-

7am-

8am-

9am-

10pm-

11pm-

7am

8am

9am

10pm

11pm

12pm

Waste Water Sourced

3.73 (Water sourced heat pump)

Based on York water sourced

Heat Pump SEER

150kW

heat pump selection with

Week

25%

65%

80%

100%

80%

25%

Evaporator water in

Saturday

25%

65%

80%

100%

80%

25%

temperature of 15oC and

Sunday

25%

65%

80%

100%

80%

25%

supplying 50oC/45oC hot

water

Table 8 – NABERS occupancy schedule

Air sourced Heat Pump

3.0 (Air cooled heat pump)

Based on typical air sourced

Museum and Office areas:

SEER

150kW – equates to 90th percentile heat load.

heat pump selection

12am-

7am-

8am-

9am-

5pm-

6pm-

7pm-

9pm-

Condensing circuit water

3.86 (water cooled heat pump)

Based on York water sourced

7am

8am

9am

5pm

6pm

7pm

9pm

12am

sourced Heat Pump

62kW – is maximum coincident heating and

heat pump selection with

SEER

cooling load.

Evaporator water in

Week

0%

15%

60%

100%

50%

15%

5%

0%

temperature of 22oC and

Saturday

0%

15%

60%

100%

50%

15%

5%

0%

supplying 50oC/45oC hot

Sunday

0%

15%

60%

100%

50%

15%

5%

0%

water

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 16

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

Model Item

Energy Model Input

Model Input Reference

Model Item

Energy Model Input

Model Input Reference

(Energy Piles) Ground

25W/m of heat rejection through water loop

Combined Energy

Ground sourced cooling and

Current Design proposal with the following

As above

Sourced heat coupling

Efficient Design

circulating through buildings piles.

opportunities combined:

through piles

energy pile literature.

Opportunities

2 loops of piping per pile

– Air Sourced Heat Pump

Pile details:

– Energy Piles

– 15 piles at 29m

– Variable Speed Cooling Towers

– 17 piles at 29.5m

– Variable Volume Condensing Water Loop

– 7 piles at 24.5m

– Low Specific Fan Power Central Air Handling

Equates to approximately 100kW of heat rejection

Roof-mounted

10m2 per kW of install PV: 160kW

Based on NIWA Sunshine

capacity

photovoltaic array

26% efficiency drop due to inclination and

hours for Wellington and

Increased Pump energy was included

orientation and system losses.

SolarKing PV 260W (per

Magnetic Bearing Water

50% of roof area available for PV to be installed:

panel) selection.

1200kW chiller

Based on a Powerpax

Cooled High Efficiency

– Roof area: 1600m2

Magnetic Bearing

Magnetic Bearing

1200kW water cooling chiller

Chiller

– Effective PV panel area: 955m2

water cooled chiller

water cooled chiller

selection supplying 6oC/12oC.

NIWA Mean monthly total sunshine (hours)

10 point part load

10 point part load

for Wellington

COPs:

COPs:

–

1150kW: 5.81 COP

– 1150kW: 5. 5 COP

– 1035 kW: 6.63

– 1035 kW: 6.1 COP

COP

– 115kW: 6.1 COP

– 920kW: 7.56 COP

– 805kW: 8.66 COP

– 690kW: 10.07 COP

– 575kW: 11.96 COP

– 460kW: 12.33 COP

– 345kW: 12.47 COP

– 230kW: 13.23 COP

115kW: 13.86 COP

Variable speed cooling

Fans vary speed based on outdoor air

tower fans

temperature:

– 100% fan speed at 24.8oC outdoor air

temperature

Does not account for reduced fan speed

requirements due to low cooling load.

Variable volume

Pumps vary speed proportionally to cooling load:

condenser water loop

– 10% to 40% cooling load: 6% pump speed

(Open versus closed

towers)

– 50% cooling load: 13% pump power

– 60% cooling load: 22% pump power

– 70% cooling load: 34% pump power

– 80% cooling load: 51% pump power

– 90% cooling load: 73% pump power

– 100% cooling load: 100% pump power

Low specific fan power

A 20% improvement on baseline SFP:

Typical fan efficiency

Central Air Handling

– 2.0W/l.s

– Supply and return air fans

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 17

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

Appendix B

Financial Performance

Analysis

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 18

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

Daylight Harvesting to FOH areas

Years

Annual

Cummulative

Payback

Capital

Annual Cash

Present Value of

Net Present Value of

Savings

Savings

Investment

Flow

Saving

Savings

Client Input Values

0

$0

$0

-$21,000

$21,000

-$21,000

-$21,000

-$21,000

Inflation Rate

2.5%

1

$1,633

$1,633

-$19,367

$0

$1,633

$1,533

-$19,467

Discount Rate

6.5%

2

$1,674

$3,307

-$17,693

$0

$1,674

$1,476

-$17,991

3

$1,716

$5,022

-$15,978

$0

$1,716

$1,420

-$16,571

4

$1,759

$6,781

-$14,219

$0

$1,759

$1,367

-$15,204

Assessment Inputs

5

$1,803

$8,584

-$12,416

$0

$1,803

$1,316

-$13,888

Capital Cost

$ 2

1,000

6

$1,848

$10,431

-$10,569

$0

$1,848

$1,266

-$12,622

Secondary Capital Cost

$ -

7

$1,894

$12,325

-$8,675

$0

$1,894

$1,219

-$11,403

Time of Secondary Capital Cost (Years)

0

8

$1,941

$14,266

-$6,734

$0

$1,941

$1,173

-$10,230

Annual Savings

$1,633

9

$1,990

$16,256

-$4,744

$0

$1,990

$1,129

-$9,101

Assessment Length (Years)

20

10

$2,039

$18,295

-$2,705

$0

$2,039

$1,086

-$8,015

11

$2,090

$20,386

-$614

$0

$2,090

$1,046

-$6,969

12

$2,143

$22,528

$1,528

$0

$2,143

$1,006

-$5,963

Assessment Results

13

$2,196

$24,724

$0

$2,196

$969

-$4,994

Payback Period (years)

12.0

14

$2,251

$26,975

$0

$2,251

$932

-$4,062

Total NPV

$840

15

$2,307

$29,283

$0

$2,307

$897

-$3,165

IRR

7.0%

16

$2,365

$31,648

$0

$2,365

$863

-$2,302

ROI

99%

17

$2,424

$34,072

$0

$2,424

$831

-$1,471

18

$2,485

$36,557

$0

$2,485

$800

-$671

25

19

$2,547

$39,104

$0

$2,547

$770

$99

20

$2,611

$41,714

$0

$2,611

$741

$840

Total

$41,714

$840

Inflation Rate

Glossary of Terms

Discount Rate

The discount rate is the rate at which cash

depreciates with time, hence the value of annual

savings decreases.

Capital Cost

Capital costs are fixed one time expenses,

typically the purchase of plant.

Present Value (PV)

PV is the present day value of the future returns

from the investment.

Internal Rate Of Return (IRR)

IRR is the discount rate that make the NPV = 0

at the end of the assessment period. i.e. The

Internal Rate of Return is the rate where if you

discount all of the future cash flows, the present

value of the flows is equal to the cost.

Net Present Value (NPV)

NPV is the sum of all previous PV's.

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 19

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

Economiser

Years

Annual

Cummulative

Payback

Capital

Annual Cash

Present Value of

Net Present Value of

Savings

Savings

Investment

Flow

Saving

Savings

Client Input Values

0

$ -

$ -

$ ( 5,000) $ 5

,000

$ ( 5,000) $ ( 5,000) $ ( 5,000)

Inflation Rate

2.5%

1

$ 7

,001

$ 7

,001

$ 2

,001

$ -

$ 7

,001

$ 6

,574

$ 1

,574

Discount Rate

6.5%

2

$ 7

,176

$ 1

4,177

$ -

$ 7

,176

$ 6

,327

$ 7

,901

3

$ 7

,355

$ 2

1,532

$ -

$ 7

,355

$ 6

,089

$ 1

3,990

4

$ 7

,539

$ 2

9,072

$ -

$ 7

,539

$ 5

,860

$ 1

9,850

Assessment Inputs

5

$ 7

,728

$ 3

6,800

$ -

$ 7

,728

$ 5

,640

$ 2

5,491

Capital Cost

$ 5

,000

6

$ 7

,921

$ 4

4,721

$ -

$ 7

,921

$ 5

,429

$ 3

0,919

Secondary Capital Cost

$ -

7

$ 8

,119

$ 5

2,840

$ -

$ 8

,119

$ 5

,225

$ 3

6,144

Time of Secondary Capital Cost (Years)

0

8

$ 8

,322

$ 6

1,162

$ -

$ 8

,322

$ 5

,028

$ 4

1,172

Annual Savings

$ 7

,001

9

$ 8

,530

$ 6

9,692

$ -

$ 8

,530

$ 4

,840

$ 4

6,012

Assessment Length (Years)

20

10

$ 8

,743

$ 7

8,435

$ -

$ 8

,743

$ 4

,658

$ 5

0,669

11

$ 8

,962

$ 8

7,397

$ -

$ 8

,962

$ 4

,483

$ 5

5,152

12

$ 9

,186

$ 9

6,583

$ -

$ 9

,186

$ 4

,314

$ 5

9,467

Assessment Results

13

$ 9

,416

$ 1

05,998

$ -

$ 9

,416

$ 4

,152

$ 6

3,619

Payback Period (years)

1.0

14

$ 9

,651

$ 1

15,649

$ -

$ 9

,651

$ 3

,996

$ 6

7,616

Total NPV

$ 8

8,632

15

$ 9

,892

$ 1

25,541

$ -

$ 9

,892

$ 3

,846

$ 7

1,462

IRR

142.5%

16

$ 1

0,140

$ 1

35,681

$ -

$ 1

0,140

$ 3

,702

$ 7

5,164

ROI

3477%

17

$ 1

0,393

$ 1

46,074

$ -

$ 1

0,393

$ 3

,563

$ 7

8,727

18

$ 1

0,653

$ 1

56,727

$ -

$ 1

0,653

$ 3

,429

$ 8

2,156

25

19

$ 1

0,919

$ 1

67,646

$ -

$ 1

0,919

$ 3

,300

$ 8

5,456

20

$ 1

1,192

$ 1

78,838

$ -

$ 1

1,192

$ 3

,176

$ 8

8,632

Total

$ 1

78,838

$ 8

8,632

Inflation Rate

Glossary of Terms

Discount Rate

The discount rate is the rate at which cash

depreciates with time, hence the value of annual

savings decreases.

Capital Cost

Capital costs are fixed one time expenses,

typically the purchase of plant.

Present Value (PV)

PV is the present day value of the future returns

from the investment.

Internal Rate Of Return (IRR)

IRR is the discount rate that make the NPV = 0

at the end of the assessment period. i.e. The

Internal Rate of Return is the rate where if you

discount all of the future cash flows, the present

value of the flows is equal to the cost.

Net Present Value (NPV)

NPV is the sum of all previous PV's.

Beca // 3 June 2016

5138221 // NZ1-12429047-20 0.20 // page 20

MACC - EECA Programme 2B Energy Efficiency Review (Building Services)

Exhaust Air Heat Recovery (FCU system only)

Years

Annual

Cummulative

Payback

Capital

Annual Cash

Present Value of

Net Present Value of

Savings

Savings

Investment

Flow

Saving

Savings

Client Input Values

0

$ -

$ -

$ ( 20,000) $ 2

0,000

$ ( 20,000) $ ( 20,000) $ ( 20,000)

Inflation Rate

2.5%

1

$ 4

,634

$ 4

,634

$ ( 15,366) $ -

$ 4

,634

$ 4

,351

$ ( 15,649)

Discount Rate

6.5%

2

$ 4

,750

$ 9

,384

$ ( 10,616) $ -

$ 4

,750

$ 4

,188

$ ( 11,461)

3

$ 4

,869

$ 1

4,252

$ ( 5,748) $ -

$ 4

,869

$ 4

,030

$ ( 7,431)

4

$ 4

,990

$ 1

9,243

$ ( 757) $ -

$ 4

,990

$ 3

,879

$ ( 3,552)

Assessment Inputs

5

$ 5

,115

$ 2

4,358

$ 4

,358

$ -

$ 5

,115

$ 3

,733

$ 182

Capital Cost