link to page 2 link to page 2 link to page 12 link to page 17

Table of Contents

1.

REDACTED - 12.2 View Rd sale and purchase report - 17 June 2021, Public

1

Excluded Council Meeting Agenda, 20 May 2021

2.

REDACTED - 9.1 View Rd sale and purchase report - 17 June 2021

11

3.

REDACTED - Council 12 August 2020

16

OIA 21-094

Page 1 of 32

OIA 21-094

Page 2 of 32

OIA 21-094

Page 3 of 32

OIA 21-094

Page 4 of 32

OIA 21-094

Page 5 of 32

OIA 21-094

Page 6 of 32

OIA 21-094

Page 7 of 32

OIA 21-094

Page 8 of 32

OIA 21-094

Page 9 of 32

PUBLIC EXCLUDED EXTRAORDINARY COUNCIL MEETING

AGENDA

17 JUNE 2021

SUPPORTING INFORMATION

CONTRIBUTION TO COUNCIL’S STRATEGIC DIRECTION

The issues in this report contribute to the strategic priorities of a growing prosperous and regional y

connected city.

FINANCIAL CONSIDERATIONS

Cost

Financial considerations associated with the sale of the View Road units and the options open to

the Council are outlined throughout the body of this report.

Financial Implications

The GST Act contains specific rules in respect to the supply that whol y or partly consist of land.

This wil require that the sale of the properties wil be “zero rated” for the GST where Council sel s

the properties to:

A GST registered person who acquires the properties with the intention of using them to make

taxable supplies; and

The properties are not intended to be used as the principal place of residence of the purchaser

(or an associated person of the purchaser)

Where “Zero rating” applies, this effectively means that GST is charged by Council (but at 0%) and

no GST output tax is paid to Inland Revenue.

If the conditions of zero-rating cannot be met, for example if a government agency or developer

were to buy the properties with the intention of renting them as residential dwel ings (an exempt

supply rather than a taxable supply for GST purposes), then the sale would be subject to GST at

the standard rate of 15% and Council would have to pay GST output tax on the sale proceeds to

Inland Revenue.

It wil be important that the Sale and Purchase Agreement and the specific GST sections of the

Sale and Purchase agreement are completed correctly by both parties as this wil determine the

GST treatment for Council.

In order to protect Council from suffering GST impost on the sale price, the Sale and Purchase

Agreement should express the sale price as “plus GST (if any)”.

Costs of Sale

Council will be able to claim GST input tax on costs associated with the sale.

Income Tax

As Council is exempt from income tax (other than on income received from Council Control ed

Organisations), Council wil not be subject to income tax on the sale of the properties and nor wil it

be able to claim any deductions for income tax purposes.

STATUTORY REQUIREMENTS

Both parties have signed the Agreement for Sale and Purchase of real estate prepared by

Council’s Solicitors Simpson Grierson. The agreement contains extensive purchaser

acknowledgements regarding the weathertight nature of the property. The Purchaser waives any

right or claim it may have against the Vendor in respect of the condition of the property; and must

not make any claim in the future. The Vendor gives no representation or warranties in respect of

the property apart from minor workings relating to general terms of sale.

Item 12.2

Page 9

OIA 21-094

Page 10 of 32

PUBLIC EXCLUDED EXTRAORDINARY COUNCIL MEETING

AGENDA

17 JUNE 2021

The Vendor enters into the agreement in its non-regulatory capacity. When acting in its regulatory

capacity it is entitled to consider al applications to it in relation to this Property without regard to

this agreement.

Ful disclosure regarding the View Road units weathertight nature has occurred with both parties

interested in purchasing the units.

FOUR WELL-BEINGS

The matter discussed in the report (the sale of weathertight property acquisition and options open

to the Council) primarily relate to the Social and Economic wel beings.

TREATY CONSIDERATIONS

There are no particular Treaty obligations to note for this report. Ngati Toa/TRORT’s interest in

acquiring the View Road units is set out in the report. Elected members wil take into account the

overal working relationship with Ngati Toa when making a decision on this matter.

SIGNIFICANCE

An earlier report to Council on this matter has highlighted that it fal s at the lower end of the

financial significant threshold range.

ENGAGEMENT AND COMMUNICATIONS

Most matters to date relating to acquisition of the units have been conducted in public excluded. A

press release informed the public about the Council’s August 2020 decision to retain the units until

such time as they could be sold. On receipt of the substantive offer from TROTR in February 2021

the units have been advertised for sale. An information pack was provided to al potential

purchasers or similarly interested parties.

A press release wil be prepared fol owing this meeting to inform the public what has been decided.

ATTACHMENTS

Nil

Item 12.2

Page 10

OIA 21-094

Page 11 of 32

OIA 21-094

Page 12 of 32

OIA 21-094

Page 13 of 32

OIA 21-094

Page 14 of 32

OIA 21-094

Page 15 of 32

PUBLIC EXCLUDED EXTRAORDINARY COUNCIL MEETING

AGENDA

17 JUNE 2021

ATTACHMENTS

1.

View Road Sale and Purchase Report, Public Excluded Council Meeting Agenda, 20

May 2021

Item 9.1

Page 5

OIA 21-094

Page 16 of 32

PUBLIC EXCLUDED COUNCIL MEETING AGENDA

12 AUGUST 2020

12.2

OPTIONS FOR 26 VIEW ROAD

Author:

Andrew Dalziel, Chief Operating Officer / Deputy Chief Executive

Pouwhakahaere Mahinga Rangatōpū / Tumuaki Tuarua

Authoriser:

Wendy Walker, Chief Executive

Tumuaki

Section under the

The grounds on which part of the Council or Committee may be closed to

Act

the public are listed in s48(1)(a)(i) of the Local Government and Official

Information Meetings Act 1987.

Sub-clause and

s7(2)(g), s7(2)(h) and s7(2)(i) - the withholding of the information is

Reason:

necessary to maintain legal professional privilege, the withholding of the

information is necessary to enable Council to carry out, without prejudice

or disadvantage, commercial activities and the withholding of the

information is necessary to enable Council to carry on, without prejudice

or disadvantage, negotiations (including commercial and industrial

negotiations).

PURPOSE

The report backgrounds the acquisition of the 24 units with weathertight defects at 26 View Road.

It discusses a range of related matters and sets out the various options Council has in respect to

remediating, renting, leasing, selling or demolishing the units. The recommendations in the report

follow from a Council Options Workshop on 2 July 2020 and an elected members site visit to the

View Road units on 4 June 2020.

RECOMMENDATIONS

That the Council:

1.

Receive the report.

2.

Agree to retain the units until such time as they can be sold “as is” for a satisfactory price, or

some similar solution is found for the units.

3.

Agree to undertake necessary repairs, maintenance and upgrades to allow the units to be

tenanted, on the understanding that the rental income will be used to offset the holding cost

of keeping the units.

4.

Agree that should a substantive offer be received, before considering that offer, the units be

advertised for sale “as is” with full disclosure of their defects, in order to ensure any other

possible offers are taken into consideration before a decision is made.

Reports contain recommendations only. Refer to the meeting minutes for the final decision.

BACKGROUND

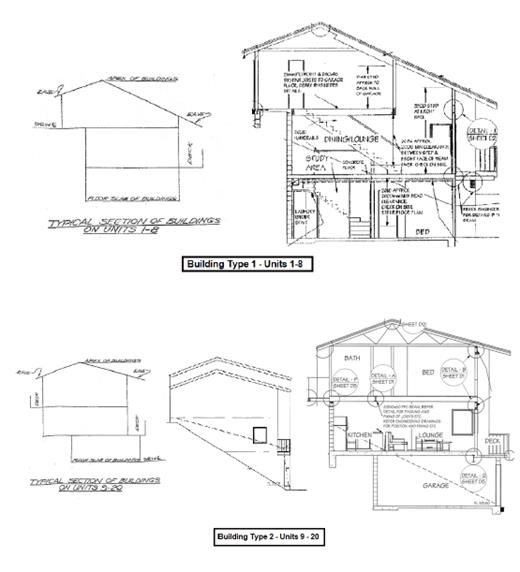

Description of the units

The 26 View Road site is comprised of 25 townhouses. There are 12 duplex units and a single unit

totalling 13 separate blocks in four different configurations. The building types and corresponding

units are outlined in the following table and diagram.

Item 12.2

Page 1

OIA 21-094

Page 17 of 32

PUBLIC EXCLUDED COUNCIL MEETING AGENDA

12 AUGUST 2020

Building Type

Relevant Units

Description

1

1-8

The garage effectively comprises the entire top

floor of the building.

The middle level is made up of a living area and

kitchen.

The lower level contains bedrooms and a

bathroom.

These units have three floors.

2

9-20

The garage effectively comprises the entire ground

floor of the building.

The middle level contains the living area, kitchen

and a toilet.

The top level contains the bedrooms a bathroom

and, in most cases, a closet laundry. These units

have three levels.

3

21-24

The top floor is made up of the garage, living area

and kitchen.

The lower floor contains bedrooms and a

bathroom.

These units have only two floors.

4

25

Unit 25 is the only unit onsite which is housed

entirely within its own building.

The top floor is made up of the garage, living area

and kitchen.

The ground floor contains the bedrooms and

bathroom.

Item 12.2

Page 2

OIA 21-094

Page 18 of 32

PUBLIC EXCLUDED COUNCIL MEETING AGENDA

12 AUGUST 2020

The units contain a mix of two and three bedroom; 13 of the units are three bedroom and 12 units

are two bedroom.

The units are located and cut into a steep hillside and are partially set above or below the access

road. They are set on concrete block retaining wall foundations which support up to two timber

framed upper levels. The cladding is a mix of painted fibre-cement weatherboard or textured fibre –

cement sheet and the roofs are painted steel. The decks are either concrete or cantilever timber

joists.

The units were all built by Hinds Builders Ltd under consent number 0564/06 and were completed

circa 2006. Code of Compliance certificates were issued by Porirua City Council in June 2007.

The location is close to the sea and is within a Zone D corrosion zone. The wind zone is likely to be

Specific Engineering Design.

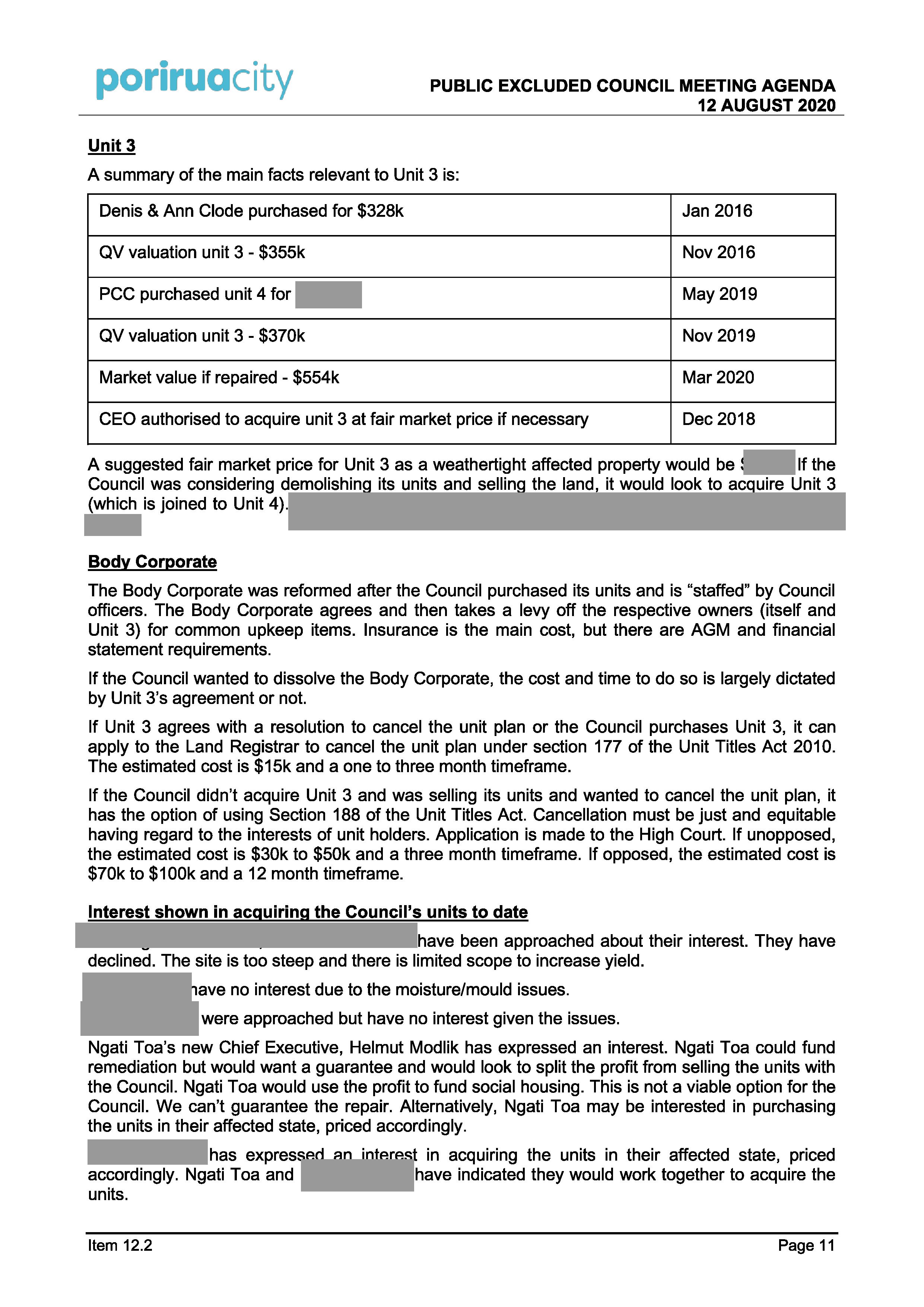

Claim

In February 2016, the Body Corporate applied for a Weathertight Homes Resolution Service

(WHRS) assessors report. A WHRS assessors eligibility report was then issued in May 2016. It

confirmed that the development met the criteria set out in the WHRS Act 2006.

A WHRS assessors follow up full report then meticulously detailed the unit’s weathertight defects.

These are in summary:

a) Inadequately detailed and terminated waterproofing membranes to reinforced concrete

retaining walls.

b) Inadequate weatherproofing to first floor concrete balconies throughout Units 9-20.

c) Poorly detailed and terminated saddle flashings to cantilevered balcony joist penetrations.

d) Inadequate step down from driveway surfaces to interior floor levels.

e) Inadequately weatherproofed joinery units to rear access doors.

In addition, the WHRS report identified a number of deficiencies that in the opinion of the Assessor

could lead to future water entry and damage.

f) Lack of drainage at the base of cavity wall construction.

g) Inadequate separation and clearance of cladding to party walls above exterior timber

decking.

h) Inadequate clearance of head flashings above ranch slider doors.

i) Inadequately weatherproofed horizontal plastered surfaces to party wall projections.

The Assessor set out a full “scope of works” to fix the units. The work in summary is:

a) Excavation and replacement of the waterproofing membranes to the below ground concrete

retaining walls (all units).

b) Uplifting existing tiles and balustrades to concrete balconies and installation of

waterproofing membranes (Units 9-20).

c) Modification of existing timber slatted decks, where installed to the rear elevation. This will

include some partial recladding of weatherboards and replacement of decay damaged

timber framing (Units 1-8 and 21-25).

d) Recladding of the fibre-cement weatherboards to the front elevations of Units 1-8 and

installation of walls either side of the garage doors (Units 1-8).

e) Temporary removal and reinstallation of the rear single access doors and installation of sill

tray flashings (Units 9-20 only).

Item 12.2

Page 3

OIA 21-094

Page 19 of 32

PUBLIC EXCLUDED COUNCIL MEETING AGENDA

12 AUGUST 2020

Future damage repairs – (optional work if considered to be needed):

f) Removal and replacement of the lowest fibre-cement weatherboard to all sections of fibre-

cement weatherboards (where not already affected due to other repair works), remove the

existing horizontal timber battens and the base of each elevations section and replace with

new timber battens to allow drainage /ventilation (all units).

g) In conjunction with removal of the existing timber decks to the rear elevations of Units 9-20

(due to excavation around retaining walls, ensure new decks are constructed with suitable

separation and clearance to existing clad party walls (Units 9-20).

h) Remove the weatherboard above the existing head flashings adjoining the ranch slider

doors (excluding on upper levels where under wide eaves), replace the current lapped

flashings with a continuous welded powder-coated metal head flashing and install new

weatherboards above each new flashing (all units).

i) Retrospective installation of metal capping to horizontal plastered surfaces above projecting

party walls. In localised areas (between Units 5 & 6 and 7 & 8).

The cost of repair was independently estimated by a QS during the WHRS assessment process,

as:

Current defects allowing water entry $4,094,235.00

inc GST and Professional fees

Future damage

$75,765.00

inc GST and Professional fees

Total estimated cost:

$4,170,000.00

N.B. – 85% ($3.5m) of this cost estimate is in regards to the cost of excavation and replacement of

the tanking membranes.

That cost will have since increased.

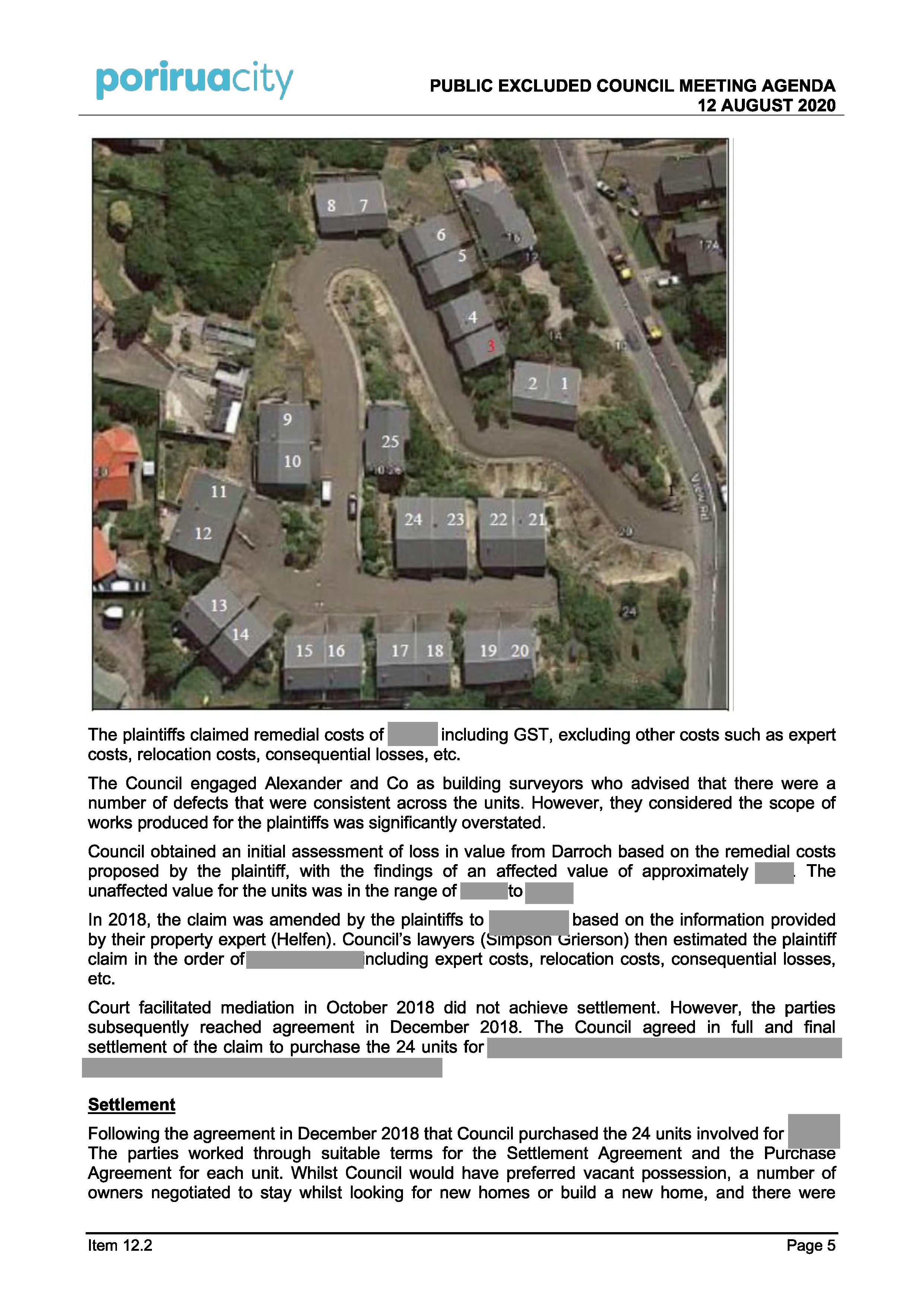

In June 2017, the Body Corporate and 24 of the 25 units issued proceedings against the Council

and Hinds Builders Ltd in the High Court, alleging that the development suffered defects and

damage. The owners of unit 3 did not participate in the proceedings. Unit 3 is identified in red on

the following aerial picture.

Item 12.2

Page 4

OIA 21-094

Page 20 of 32

OIA 21-094

Page 21 of 32

OIA 21-094

Page 22 of 32

OIA 21-094

Page 23 of 32

PUBLIC EXCLUDED COUNCIL MEETING AGENDA

12 AUGUST 2020

After the invasive testing work was carried out, Valuation Consultants Ltd were asked to provide

unaffected and affected valuations for the 24 units; a valuation for just the land (assuming

demolition of the buildings had occurred); and a rental assessment for the 24 units.

The respective April 2020 valuations are:

• 24 units assuming weathertightness remediation, deferred

$16m

maintenance and internal upgrade complete.

• 24 units assuming weathertightness remediation and deferred

$14.2m

maintenance complete (no upgrade)

• 24 units affected value – no remediation, maintenance or upgrade

$10.2m

undertaken

• Land value assuming demolition of 25 units with the purchase of

Unit 3

1. Sale to individual builders

$3.5m to $4m

2. Sale to one developer

$3m

3. Sale to one developer with slabs left in place

$3.5m

• Rental assessment for 24 units at 100% occupancy

$720k p.a.

The valuer noted that the $10.2m affected value would be difficult to achieve. Banks will not

finance weathertight building purchases. The Council would be a “price taker”.

While the current QV land value is $5.6m, the valuer stated that this figure does not represent the

underlying land value. It would not be feasible to sell duplex sites even if they were re-subdivided

down to individual fee simple sites. So instead of 25 lots, there are 13 lots for practical purposes.

Dual sites tend to sell for a premium of 30% to 40% above the selling price of a single site.

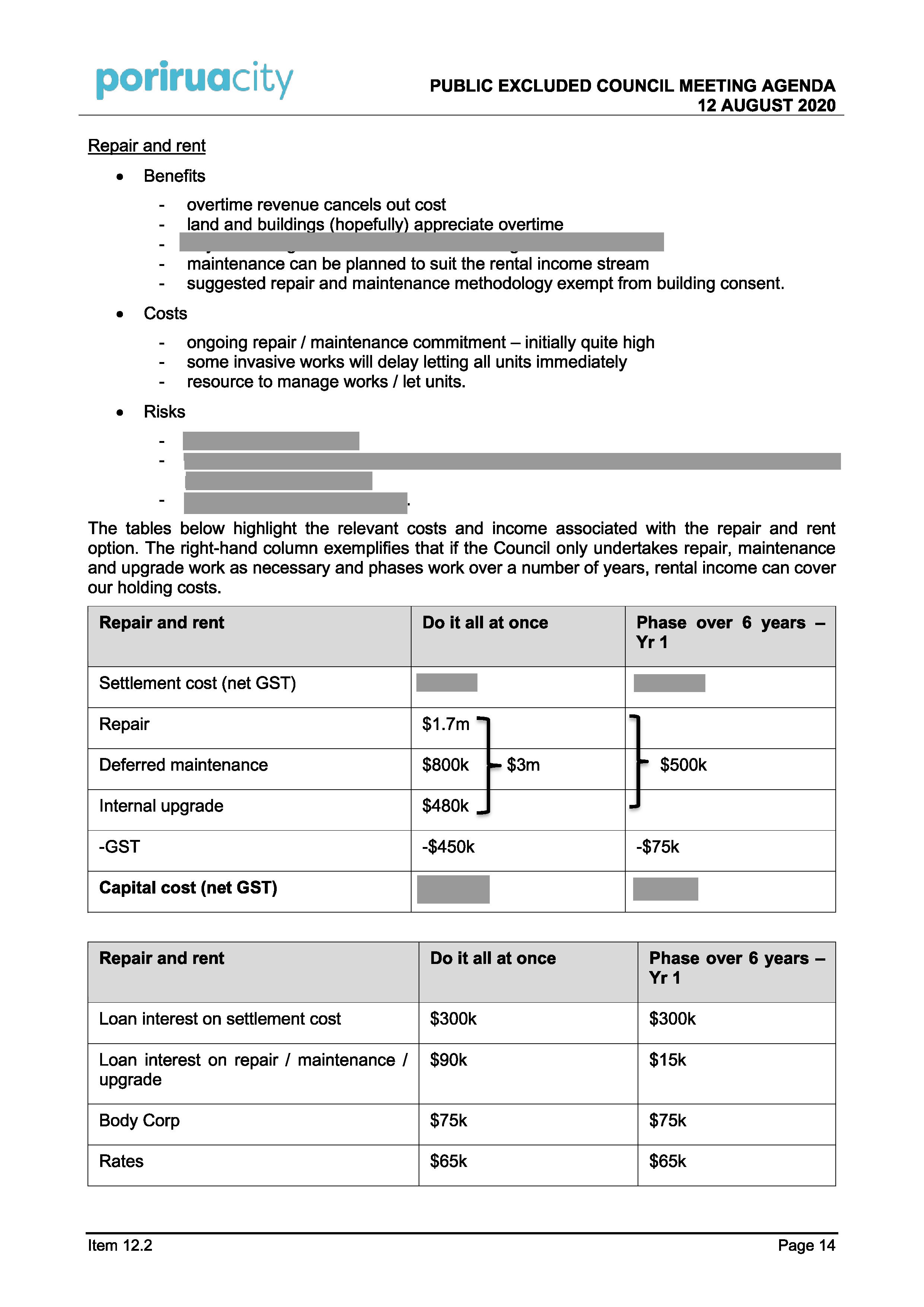

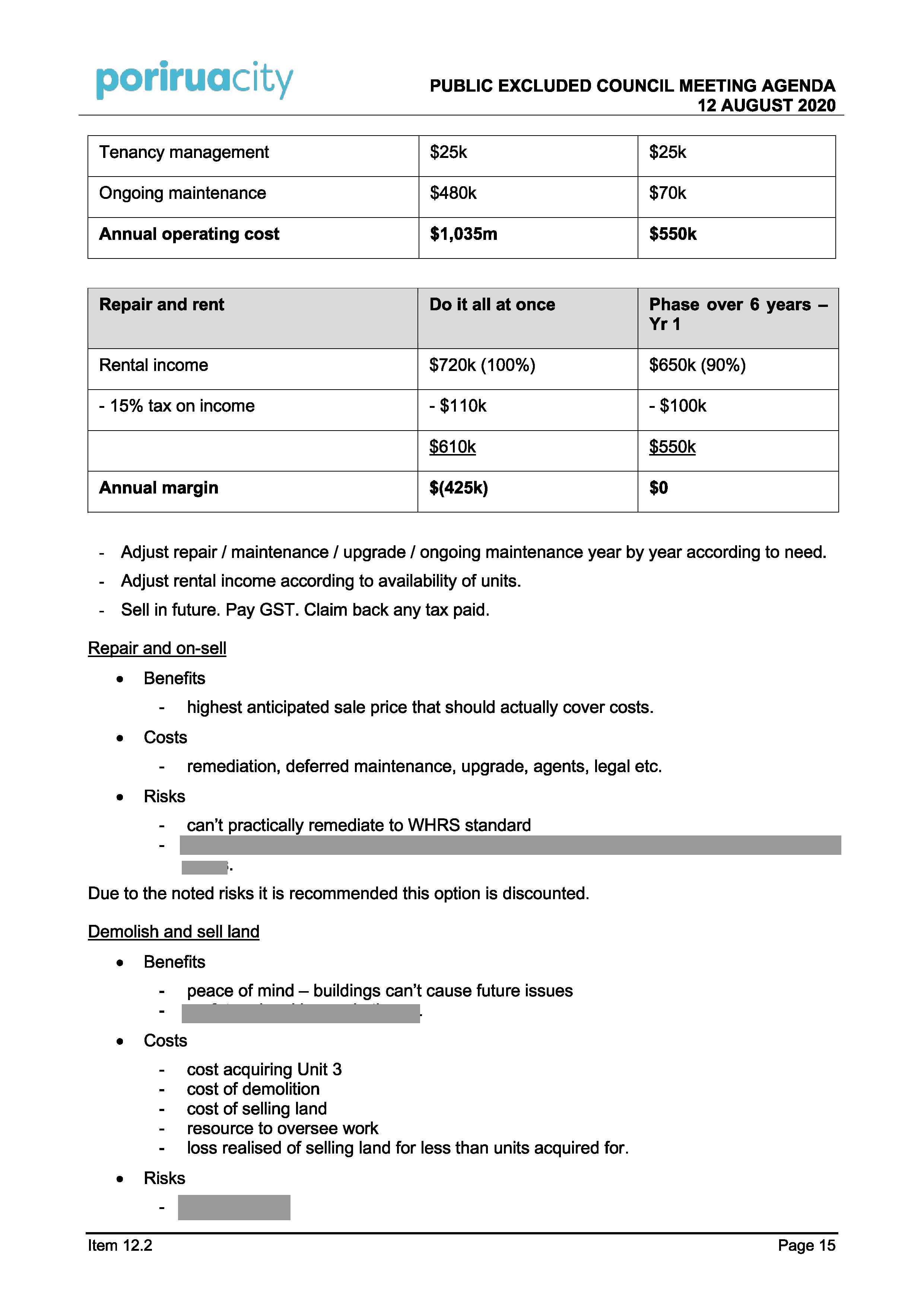

Alternative repair proposal

The Council now has three expert reports confirming weathertight defects with the units. However,

as was seen on the elected member site visit on 4 June, the damage actually appears relatively

minor. Despite the identified issues, the buildings have been largely fit for purpose since they were

built. The buildings look to be sound and appear well constructed.

The units cannot be fully remediated as per the ‘perfect’ solution set out by the WHRS. An

alternative repair proposal is to treat the dampness issues as best we can. The balconies can be

remediated. The top section of the weather proofing membrane of the basement walls can be

upgraded. A specialist negative pressure membrane can be applied to internal walls.

This is a methodology to use if the Council retains the units and rents them out. The work can be

staged over a number of years as needed. The Council would also need to address some deferred

maintenance items.

Item 12.2

Page 8

OIA 21-094

Page 24 of 32

PUBLIC EXCLUDED COUNCIL MEETING AGENDA

12 AUGUST 2020

The alternative repair work is summarised as:

Area

Work item

Upgrade balcony

• Remove and dispose of existing balustrades

membrane

• Remove and dispose of all tiles and prep slab

12 units

• Install new appropriate membrane on concrete balcony

$19k a unit / total cost if

(sealing cold joint)

applied to all 12 units

$230k

• Install new tiles on balcony

• Install new metal side mounted balustrades

• Strip away layers of gib encasing steel beam

• Grind back or wire brush off existing surface rust and paint

• Reinstate gib, plaster and paint

This would be priority one work. It would be carried out first to the units that obviously require it.

Area

Work item

Upgrade top termination

• Excavate around the top of the basement walls to expose

of retaining wall

membrane

membrane

• Prepare wall to take new membrane

24 units

• Lap new membrane strip over the top of the existing

$14k a unit / total cost if

membrane

applied to all 24 units

•

$340k

Terminate top of membrane with new pressure bar flashing

• Install protection and backfill

This would be priority two work. This would only be done as necessary where there is obvious

dampness and moisture issues.

Area

Work item

Treat rising damp with

• Remove interior lining trip and battens to expose block walls

negative pressure slurry

• Treat walls with specialist coating

11 units

• Reinstate linings & trim on new battens

$102k a unit / total costs if

•

applied to all 11 units

Paint and new floor coverings in effected rooms

$1.1m

• Electrical and plumbing disconnections and reconnections

• Make good affected joinery units

This is also priority two work, only undertaken to units as required.

Item 12.2

Page 9

OIA 21-094

Page 25 of 32

PUBLIC EXCLUDED COUNCIL MEETING AGENDA

12 AUGUST 2020

Area

Work item

Deferred maintenance

• Repaint exterior surfaces

$800k

• Rescrew roofing

• Replace Galvanise fixings with new S/Steel

• Upgrade existing barriers and fences and install new vehicle

barrier

This work is priority three. Some aspects like exterior painting can be pushed out quite a number of

years.

Building Consent

While a building consent would be required for the nature of the work required to undertake the

WHRS Assessor’s scope of works, a building consent would not be required for the alternative

repair work. The structure has not yet failed durability Clause B2 of the New Zealand Building

Code. The damage is quite minor. The repair work is about keeping water out, not remediating

damaged framing. Under Schedule One of the Building Act 2004 repairs can be undertake as part

of normal repair and maintenance. The work itself would need to be carried out in a way that is

compliant with the Act.

Residential Tenancies Act and Healthy Homes Standards

If the Council repairs and rents the units, it will be subject to obligations under the Residential

Tenancies Act, including the Healthy Homes Standards.

Under the Residential Tenancies Act 1986, landlords are generally responsible for:

• providing the premises in a responsible state of cleanliness;

• providing and maintaining the premises in a reasonable state of repair;

• complying with smoke alarm, healthy homes standards, and requirements under other

enactments;

• providing for the collection and storage of water where there a reticulated water supply

does not exist;

• compensating the tenant where the tenant has spent money on fixing something urgently in

circumstances where the tenant has made reasonable attempts to notify the landlord of the

problem; and

• taking reasonable steps to make sure that other tenants do not interfere with the

reasonable peace, comfort and privacy of the tenant.

There are five healthy homes standards:

Heating, insultation, ventilation, draught stopping and moisture ingress and drainage. The Council

would be required:

• to immediately comply with the insulation requirements in the Health Homes Standards

upon letting an apartment; and

• to comply with the remainder of the standards (relating to heating, draught stopping,

ventilation, moisture and drainage) by 1 July 2021.

Most standards (including the moisture tightness and drainage standard) are subject to the

“reasonably practicable” standard, which states that the standards do not apply where it is not

reasonably practicable for the landlord to fulfil them.

Our assessment is that if we undertake repairs we will be able to meet the legislative obligations.

Before tenanting we would also be wise to obtain an independent experts sign-off for acceptable

moisture levels.

Item 12.2

Page 10

OIA 21-094

Page 26 of 32

OIA 21-094

Page 27 of 32

OIA 21-094

Page 28 of 32

OIA 21-094

Page 29 of 32

OIA 21-094

Page 30 of 32

OIA 21-094

Page 31 of 32

OIA 21-094

Page 32 of 32

PUBLIC EXCLUDED COUNCIL MEETING AGENDA

12 AUGUST 2020

SUPPORTING INFORMATION

CONTRIBUTION TO COUNCIL’S STRATEGIC DIRECTION

The issues in this report contribute to the strategic priorities of a growing prosperous and regionally

connected city.

FINANCIAL CONSIDERATIONS

Financial considerations associated with the acquisition of the units and the various options open

to the Council are outlined throughout the body of this report.

STATUTORY REQUIREMENTS

A number of relevant statutory and legal obligations are outlined throughout the body of this report.

FOUR WELL-BEINGS

The matters discussed in this report (a weathertight property acquisition and options for its future)

primarily relate to the Social and Economic well beings.

TREATY CONSIDERATIONS

There are no particular Treaty obligations to note for this report. Ngati Toa’s possible interest in

acquiring the units is highlighted in the report.

SIGNIFICANCE

An earlier report to Council on this matter has highlighted that it falls at the lower end of the

financial significant threshold range.

ENGAGEMENT AND COMMUNICATIONS

Matters to date have been conducted in public excluded. However, once a formal decision is made

about the future of the units, a press release will be prepared to inform the public about what has

been decided. A pack of information wil also be assembled for “as is” purchasers or similarly

interested parties.

ATTACHMENTS

Nil

Item 12.2

Page 17

Document Outline