LTP Financial Tools-

interest rates swap and reserves strategy

17 November 2020

LTP Financial Tools-

interest rates swap and reserves strategy

17 November 2020

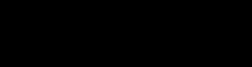

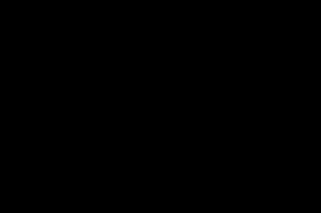

Baseline without financial tools

Increase of $21.6m (10.9%) in 2025/26

Increase of $24.7m (17.6%) on 20/21

Baseline without financial tools

Increase of $21.6m (10.9%) in 2025/26

Increase of $24.7m (17.6%) on 20/21

1. Waterloo Railway Stn roof renewal $5.6m

Reduction of $12.9m (-5.8%) in 2029/30

1. Mvt in reserves $11m

2. Rail station upgrades $12.6m

1.

Rail station upgrades completion in 27/28, -

2. PT revenue gap $8m rail and bus

3. Wairarapa carriage replacement $1.8m

$14.7m

4. Rail contract – Wairarapa Service Improvement $1.2m

20%

2.

Rail fare revenue -$0.9m

3.

Rail timetable changes +$1.7m

4.

Additional fleet capacity +$0.5m

Reduction of $2.2m (6.8%) in 2030/31

15%

1.

Rail fare revenue -$0.9m

2.

Investment Mngt swaps expenditure -$1.3m

10%

ase

erc

In

5%

s %

ate

R

0%

2021/22

2022/23

2023/24

2024/25

2025/26

2026/27

2027/28

2028/29

2029/30

2030/31

-5%

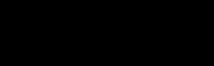

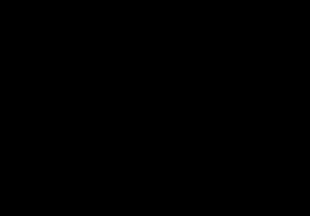

Increase of $12.5m (7.6%) in 22/23

1. Improvements to Regional Stations $1.3m

Increase of $12.7m (7.2%) in 23/24

Reduction of $2.8m (-1.3%) in 2026/27

2. Matangi Heavy Maint/Overhauls $0.7m

1. Rail Contract - RS1 Implementation Fee $1m

1.

Waterloo Railway Stn roof renewal project completion in

3. Snapper Profes -

si 10%

onal services $0.5m

2. Capex GWRC Ticketing Solution $2.5m

25/26, not rated in 26/27, -$5.6m

4. Committed $1.4m

3. Wairarapa - Carriage Replacement $1.3m

2.

Improvements to regional stations project completion in

5. EV Programme Capex GWRC Ticketing Solution $1.4m

4. GWRC Ticketing operations $3.1m

25/26, not rated in 26/27, -$1.3m

6. Wairarapa - Carriage $0.6m

Environment & Catchment:

3.

Early locomotive termination fee -$2.4m

7. Replacement RTDIS $0.8m

5. Movement in debt servicing $1.3m

4.

Rail fare revenue -$0.8m

8. Replacement Development Rail Contract - RS1 New

6. Movement in reserves $0.4m

Offset with:

Timetable $1.3m

7. Reduced Crown funded project revenue $0.5m

1.

Wairarapa carriage replacement $4.6m

Environment & Catchment:

2.

Additional fleet capacity $0.8m

9. Movement in debt servicing $1.9m

3.

Timetable changes operation $0.8m

10. Reduced Crown funded project revenue $1.2m

4.

Wairarapa Service Contract Improvement $1.2m

Baseline

Council Low

Council High

Rates % increase without use of PT Reserve

Rates % increase without use of PT Reserve

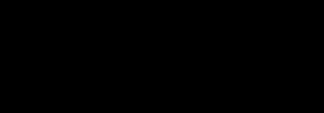

Environment – Regulatory Change Impact

2021/22

2022/23

2023/24

2024/25

2025/26

2026/27

2027/28

2028/29

2029/30

2030/31

Regulatory Initiatives:

Yr1

Yr2

Yr3

Yr4

Yr5

Yr6

Yr7

Yr8

Yr9

Yr10

Regional planning - implementing and responding to national direction

1,500,000

2,000,000

2,350,000

2,250,000

2,250,000

1,300,000

1,000,000

1,000,000

500,000

-

Fit for the Future

1,250,000

1,250,000

1,250,000

1,250,000

1,250,000

1,250,000

1,250,000

1,250,000

1,250,000 1,250,000

Wetland mapping and monitoring

-

-

-

140,000

140,000

140,000

80,000

80,000

80,000

80,000

Freshwater Science and monitoring

-

-

300,000

300,000

300,000

300,000

300,000

300,000

300,000

300,000

Facilitating local climate change adaptation processes

-

-

-

-

-

200,000

200,000

200,000

200,000

200,000

Completing whaitua development in a more integrated way

-

250,000

250,000

250,000

250,000

250,000

-

-

-

-

Total

2,750,000

3,500,000

4,150,000

4,190,000

4,190,000

3,440,000

2,830,000

2,830,000

2,330,000 1,830,000

Indicative Rates Increase

1.9%

2.5%

2.9%

2.9%

2.9%

2.4%

2.0%

2.0%

1.6%

1.3%

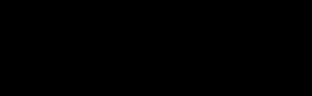

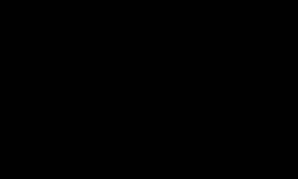

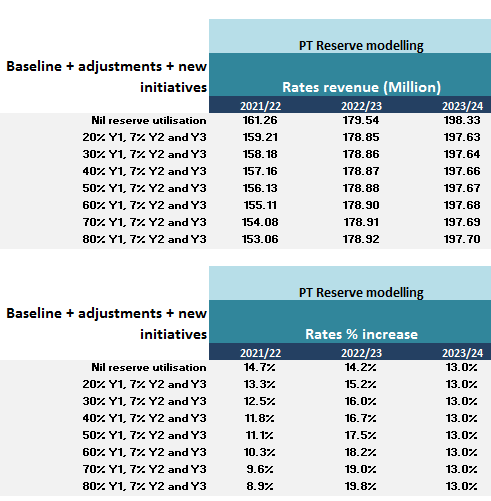

Rates revenue and % increase: PT Reserve modelling

Rates revenue and % increase: PT Reserve modelling

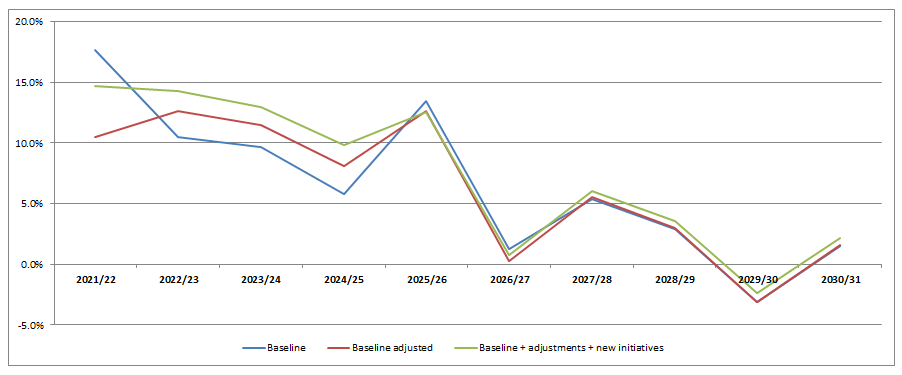

PT Reserve utilisation option: 20% Y1, 20% Y2, 15% Y3

PT Reserve utilisation option: 20% Y1, 20% Y2, 15% Y3

This option keeps the rates increase % below 15% throughout the LTP

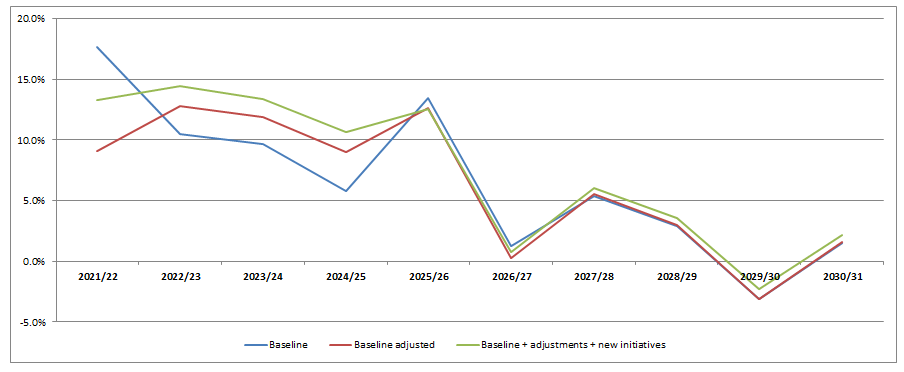

Rates % increase with adjustments and initiatives

Adjustments included:

16%

Rates % increase with adjustments and initiatives

Adjustments included:

16%

Rates % increase below 15% over LTP

Includes:

1. PT Reserve: 20% Y1, 20% Y2, 15% Y3 with

1. Baseline

reduction in interest revenue earned

14%

2. Adjustments

2. Removal of Nga Petone Cycleway

3. New initiatives

3. Environment additional revenue

12%

4. RiverLink loan life extension of 5 years

5. Debt funding PT revenue gap: Y1: $8m,

10%

Y2: $6m and Y3: $4m

6. PT KiwiRail maintenance programme debt

8%

funded

7. PT adjustments to FAR 51% to 90% in baseline

6%

and initiatives

4%

2%

0%

2021/22

2022/23

2023/24

2024/25

2025/26

2026/27

2027/28

2028/29

2029/30

2030/31

-2%

-4%

Baseline + adjustments + new initiatives

Managing Interest rate risk via Hedging

Managing Interest rate risk via Hedging

What is Hedging ?

• Hedging is designed to provide certainty

• It’s a risk mitigation strategy against fluctuating interest rates,

commodities, or foreign exchange movements

• Our discussion will focus on

interest rate hedging

• What is the risk we are trying to avoid?

• There is a cost to have certainty via hedging, but there could be a

even bigger one with taking a risk – i.e. uncertainty

• Finance Strategy – LTP – Financial Prudence (not taking undue risks)

Fixed or Floating rate interest cost ?

Fixed or Floating rate interest cost ?

• There are two types of interest bearing debt

•

Fixed rate - the interest rate remains constant over life of the debt

•

Floating rate - the interest rate on the debt is re-priced generally every 90

days

•

Floating rate is generally cheaper

than

Fixed rate

Fixed Rates

• but interest rates change over

time

Floating Rate

3 months

• 90 days is 0.25%, 10 years is 3.5%

How Council manages its Debt

How Council manages its Debt

• All Council debt is borrowed at a floating interest rate i.e. re-priced every 90

days

• Funds are borrowed for various terms, overnight, 90 days to up to 17 years

• Interest rates risk on Councils debt is managed separately

Note

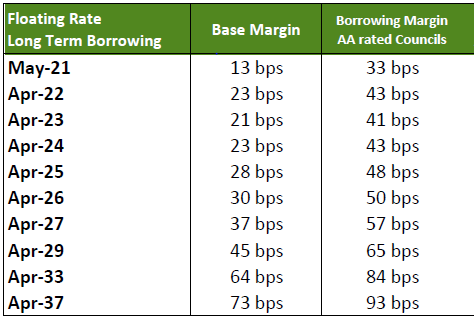

LGFA

• Our cost to borrow to April 2025 is the

90 day rate plus a fixed margin of 0.48%

• 90 day rate is 0.28% now

• i.e 0.76% for the next 90 days

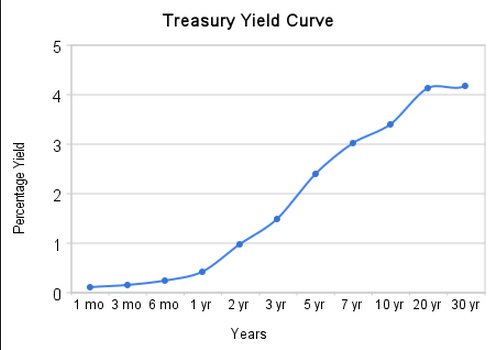

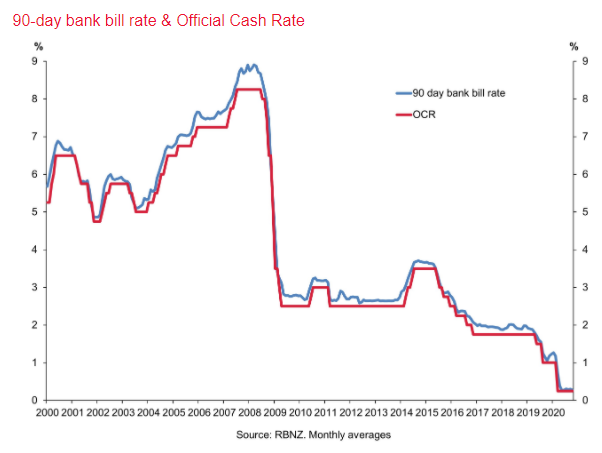

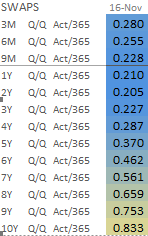

Graph of 90 day Floating rate over time Current Fixed rate SWAPS 16 Nov

Cost to fix via swap for 5 years to

Graph of 90 day Floating rate over time Current Fixed rate SWAPS 16 Nov

Cost to fix via swap for 5 years to

2025 is 0.37%

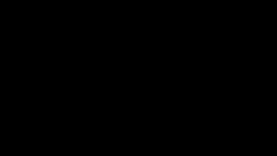

Showing our Borrowing portfolio spread

30-Jun-20

Greater Wellington Regional Council

Funding Maturity Chart

0 - 3 years

3 - 6 years

6 years plus

15%-60%

15%-60%

10%-60%

39%

34%

27%

150.0

125.0

100.0

75.0

m

D

Z

N

50.0

25.0

0.0

2023

2026

2033

-25.0

1-

2

3

4

5

6

7

8

9

0

1

2

3

4

5

-

-

-

-

-

-

-

-

1

1

1

1

1

1

0

1

2

3

4

5

6

7

8

-

-

-

-

-

-

9

0

1

2

3

4

1

1

1

1

1

Maturity Date Bucket

Drawn Loans

CP

Available

Linked Deposits

How is the councils interest rate risk managed ?

• The floating interest rate can be switched into fixed rate with an interest rate swap

• An interest rate swap can be for a short time i.e. 6 months or a long time i.e. 17 years +

• We have a portfolio of floating rate interest cost - some overlaid with fixed rate swaps

•

Interest rate swaps are flexible they can be cancelled, they can be extended or shortened

.. Banks are happy to do this …. More on this later

• Operation of Swaps governed by our Treasury Risk Management Policy

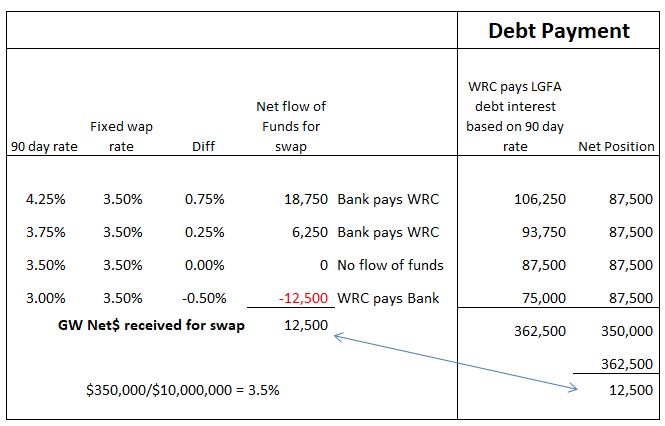

Example of a how a SWAP works

• WRC borrow funds at a floating interest rate (each 90 days the rate is re-

priced) and rates determined by the market were:

4.25%, 3.75%, 3.50%, 3.00% on Drawdown, March, June, September,

Borrowed $10 million from LGFA on floating rate note for 1 year

• WRC enters into a swap to ensure a

fixed interest rate for 1 year at 3.50%

Example of a SWAP

Example of a SWAP

=C

Example of a SWAP

Swap fixed rate v Floating rate showing payoff

Example of a SWAP

Swap fixed rate v Floating rate showing payoff

4.50%

4.00%

$18,750 &

$6,250 bank

pays us

Floating rate

Fixed rate

3.50%

$12,500 pay to bank

3.00%

Mar

Jun

Sep

Dec

Treasury Risk Management Policy

• Policy sets out the parameters under which we manage our interest rate

risk

• Reviewed every 3 years, any changes are advocated/supported by our

Treasury Advisors –PwC and approved by ELT, FRAC, Council

• Policy provides latitude to take some view on interest rates - reviewed

at least quarterly by PwC

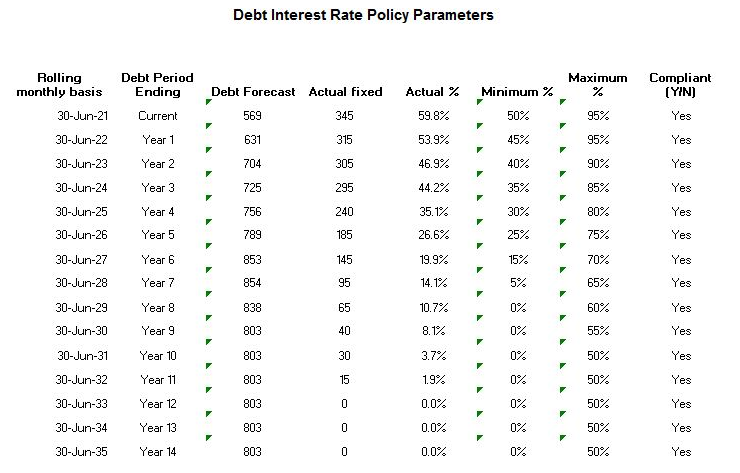

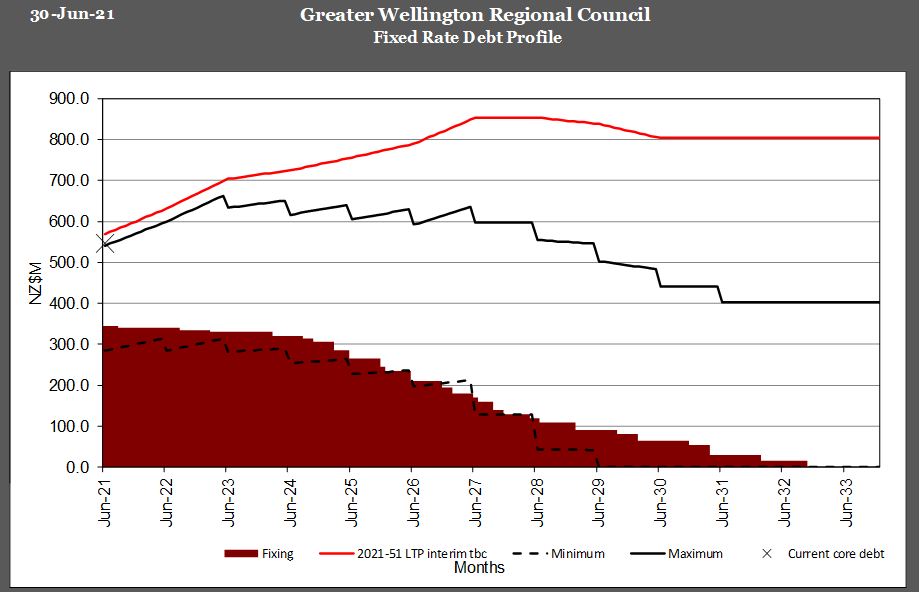

Interest rate Hedging Policy parameters – Fixed rate

Interest rate Hedging Policy parameters – Fixed rate

Hedging/Fixed interest rate graphically

Hedging/Fixed interest rate graphically

SWAP valuations

• Swaps valued regularly, reported quarterly via our management reporting to Council

• Is an Accounting requirement, impact are:

•

Balance sheet valuation reflect the current position if swaps cancelled today

•

Profit and Loss account amounts represent the

changes between years

• Valuations vary as interest rate move up and down and as the swaps are used-

up/extinguished

Interest rate SWAPS are flexible

• Currently we have pressure with our LTP .. Can we use swaps to help us out ?

• Yes, anything is possible

• Its like your home mortgage you can easily change the rate … but there is often a cost

• An

opportunity cost and a

costs of the bank to pay

• We can reduce interest costs in the next few years by extending out our swaps

• Simplistically we pay fixed rate 5% for 2 years we can extend and pay 2.5% for 4 years

• But after 2 years if we paid 5% we could pay 0.25% for the next two years instead

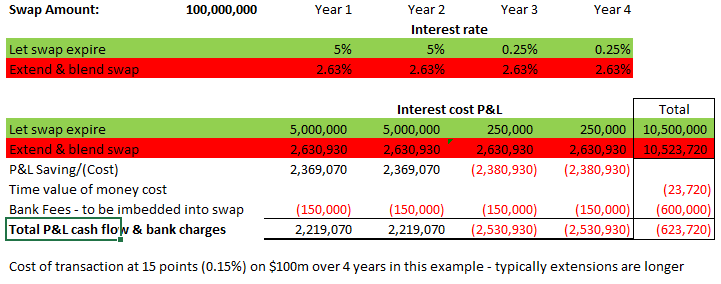

Interest rate swaps – Swap extensions – Simple scenario

Interest rate swaps – Swap extensions – Simple scenario

• $100m of Debt and a swap on this to pay 5% for 2 years and want to extend 2 years

• Current 90 day floating rate is 0.25% and same for the next 4 years

What an extension looks like

What an extension looks like

Proposed extension

Completed extension

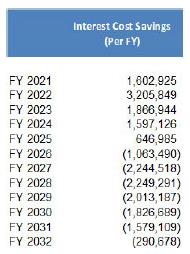

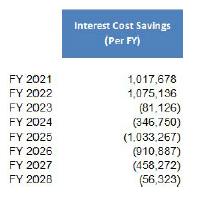

Extension scenario 1 – Target $2m per year over next 3 years

Extension scenario 1 – Target $2m per year over next 3 years

• Asked PwC to provide scenario of

targeting saving of $2m over first 3

years of LTP.

• Includes bank charges amounting to

$2,200,000

• Amends $160 million of swaps

• Average extension 9 years

• Terminal interest rates 2.6%

Extension scenario 2 – Optimise Blend & Extend – rate reduction

Extension scenario 2 – Optimise Blend & Extend – rate reduction

• Asked PwC to provide scenario to

optimise best value saving on

extending high interest rate

swaps

• Includes bank charges of

$650,000

• Amends $60 million of swaps

• Average extension 7 years

• Terminal interest rates 2.5%

Advantages of blend and extending swaps

• Can provide immediate interest cost savings

• Lowers average interest rate in early years

• Regret factor on execution is presently low, rates can go lower but limited

Disadvantages of blend and extending swaps

• While initial saving, costs are increased in later years

• There is a cost to complete transaction – can be expensive

• There is no competitive pricing, have to take banks charges, or abandon

• Changes can range from 0.05% per annum to 0.20% depends on bank and

market conditions

• Can create problems in latter years as cost reverse

Recommendation

• There is no right or wrong answer

• Economically it does not stack up because of the bank costs, these are spread.. nevertheless

are to be paid

• Would not do this in the ordinary course of business unless there is an imperative

• What are our advisers recommending .. As above.