AT Local (Devonport On-Demand Rideshare) Performance Report

The purposes of this paper are to:

review the performance of the AT Local on-demand rideshare operation in Devonport;

document the key learnings gained from the trial that could be applied to any future

on-demand operation; and

determine whether the existing Devonport AT Local trial should continue and if so,

whether changes are required.

1)

Background

Auckland Transport, like many public transport organisations globally, is being challenged to

deliver new, innovative and sustainable customer solutions to meet the demands of an ever-

increasing, multi-cultural and aging population in the digital age.

Public transport organisations face similar challenges through:

The requirement to serve an array of customer markets, ranging from high density

urban routes through to sparsely populated rural areas

Variable cost recovery across routes, with main corridors having higher service

frequency and quicker journey times (high cost recovery), whereas routes covering

outer suburbs attract fewer passengers (lower cost recovery)

Higher subsidies through reduced cost recovery, which can result in public and

media scrutiny of organisational priorities and demand for greater efficiencies.

The first and final leg of any journey can be the most difficult journey stage. Historically, it has

been difficult for public transport to provide effective services to bridge this gap and it remains

an on-going customer pain point. To fill this gap, commercial ride sharing and ride hailing

services have launched both globally and in New Zealand, where Uber, DriverHer, Ola and

Zoomy are now available. These services are focused on optimising (reducing) waiting and

travel times but only at an individual customer level.

Public transport organisations are now considering whether on-demand technologies could

be used to complement, supplement or substitute conventional public transport services and

assess whether these can deliver more customer-focused, flexible and cost-effective

outcomes. The focus is on optimising the journey for groups of customers (rather than

individuals) travelling to or from a public transport hub for a subsidised price.

Auckland Transport has partnered with Via Mobility, an international provider of innovative

rideshare solutions to create “AT Local”, a 12-month “test and learn” rideshare trial. It is a

publicly-subsidised, on-demand transport solution, designed to carry multiple (non-related)

passengers simultaneously from one location to another within a designated rideshare zone

i.e. customers share the vehicle with other passengers, not just the driver. The service is also

the first in the world to use an all-electric vehicle fleet.

Page

1 of

13

The rideshare trial has six key objectives:

1. Encourage modal shift away from the single occupant vehicle

2. Reduce congestion in the Lower Devonport Peninsula area, particularly on Lake Road

3. Deliver a new innovative way to meet customers ‘first’ and ‘final’ leg travel needs

4. Social responsibility including improved sustainability through use of electric vehicles

5. Measure customers adoption and perception of the rideshare concept

6. Take learnings and applicability of the service for other parts of Auckland

AT Local provides customers with an innovative, more

personalised public transport option, designed to better

meet their transport needs, allowing them to travel at their

time and location of choice, anywhere within the designated

rideshare zone. It is a flexible, cost-effective travel solution,

being responsive to the customer’s travel requirements,

thereby differing from conventional public transport, which

operates to a scheduled timetable along a designated

route. It offers an alternative option for the Lower

Devonport Peninsula community, in addition to providing

AT with valuable insights as to whether on-demand

rideshare is a viable first-and-last-leg option to address

future regional transport demand.

Customers download the AT Local app and following

registration, can immediately book and pay for rides, in addition to providing realtime feedback.

Customers can travel anywhere within the rideshare zone for a fixed fare per person, with

rides to or from the three local ferry terminals (transport hubs) being offered at a 50% discount

to assist in reducing congestion in streets up to one kilometre from the ferry terminals,

particularly during peak hours.

AT Local operates in a rideshare zone covering

the lower Devonport Peninsula, which has three

natural sea borders and one land boundary.

This significantly reduces the likelihood of “zone

creep” where customers living outside boundary

request the zone be expanded to include their

area.

Operating in the lower Devonport Peninsula

also provides an opportunity to reduce peak

hour congestion around the three local ferry

terminals, particularly Devonport. Customers

now have an alternative to leaving early,

spending time driving around searching for a car

park, then walking extended distances to (or

from) the ferry terminal - they can use the AT

Local and be dropped off at the ferry terminal in

good time to catch their ferry.

Page

2 of

13

2)

AT Local Performance

2)

AT Local Performance

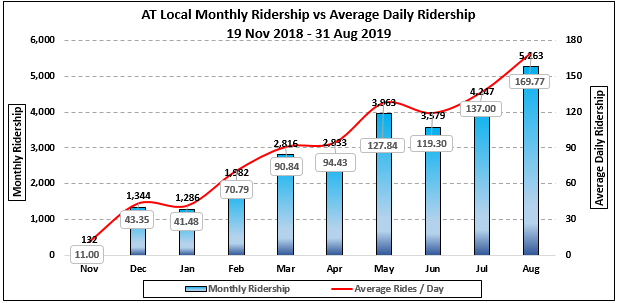

The trial commenced on 19 November 2018. The extended summer holiday period curtailed

customer acquisition and ridership growth but since February, there have been significant

month-on-month increases both. Between February and August 2019, customers increased

from 1,300 to 2,950 (+127%), whilst monthly ridership increased from 1,582 to 5,263 (+233%).

Selected Performance Metrics to 31 August 2019

i.

Customer Base: 2,950 (20.7% of target market)

ii.

Ridership to Date: 27,481

iii.

Regular Users: 890 (30.2% of customer base)

iv.

Modal Shift: 43% move from private motor vehicle

v.

39% of customers have taken three or more rides

vi.

49% rides aggregated during peak 07:00 - 08:00 (sharing vehicle with others)

vii.

Average Customer Rating: 4.88 out of 5.00

viii.

25.9% of customers now use AT Local more than once per day

ix.

23% of customers reported increased use of local ferries because AT Local has made

accessing these services easier.

x.

2% of customers have started using ferries because of AT Local

Both performance metrics and customer feedback indicate that AT Local is delivering modal

shift, with 43% of customers moving away from the private motor vehicle. This is supported

by unsolicited feedback, with customers proactively advising they now use AT Local, rather

than driving to the ferry terminals. Average daily ridership (including weekends) increased to

170 rides per day in August, whilst weekday-only ridership rose to 213 rides per day.

A)

Ridership Growth

AT Local has been operating for nine months. As AT Local has established itself as a viable

alternative for first and last leg travel with its target market. Growth is underpinned by in-

market promotions and more importantly, word of mouth referrals from satisfied customers,

resulting in both total rider numbers and regular riders increasing, as they use the service

more often.

Page

3 of

13

Monthly ridership has increased from 132 (Nov 2018) to 5,263 (Aug 2019), with average rides

per customer rising from 1.31 (Nov 2018) to 5.91 (Aug 2019).

B)

Impact on Local Bus Services

The implementation of New Network – North resulted in five bus routes servicing the lower

Devonport Peninsula. The new services are shown below:

There were initial concerns that the new AT

Local service could potentially cannibalise

the local bus routes by taking passengers

away. However, a recent customer survey

indicates there has been a limited impact

to date, with just 13% of AT Local

customers advising they had previously

used bus services. This is supported by a

more detailed analysis covering the period

1 February 2019 – 30 June 2019, shown

below:

Local Bus Services: Average Daily Passengers

AT Local

Time Period

801

802

806

807

814

01/02/19

–

487

341

49

63

1,552

86

30/04/10

01/05/19

–

488

355

46

60

1,475

124

30/06/19

Change

+1

+14

-3

-3

-77

+36

There is some anecdotal evidence suggesting that customers switch between the local 806

and 807 bus services (covering the Devonport Ferry Terminal) and AT Local but this depends

largely on whether a bus service is available when they want to travel. It is also possible that

some bus customers switch to AT Local services during bad weather conditions

It is worth noting that currently, the extent of switching between bus services and AT Local

may be restricted by the current App-only rideshare booking and payment operation. If any

subsequent service offered the traditional ride booking and payment options, this would

increase the rate of substitution between bus services and rideshare. Additionally, SuperGold

customers travel free of charge on public transport (subject to the SuperGold conditions of

travel), whereas all AT Local customers pay a fixed fare per rider.

C)

Cost (Subsidy) per Passenger

Other performance metrics have also improved significantly during the period since launch.

From a cost perspective, one-off set up costs totalled $103,400, so monthly operating

expenses have been adjusted to reflect this.

Page

4 of

13

The two largest monthly expenses (Go Bus contract fee and Via Mobility monthly service

charges) are fixed. Therefore, as ridership increases, revenue rises and passenger

operational performance metrics improve, thereby reducing the subsidy per ride and cost per

passenger kilometre. Should monthly ridership continue to rise, both the subsidy per ride and

cost per passenger kilometre will decrease correspondingly.

i.

Cost (Subsidy) per Passenger: $11.72 (Aug 2019)

This compares to overall PT performance for August of $2.97. In August, AT Local had a better

subsidy/passenger than 57 bus routes. The subsidy per passenger on contracted ferry

services is $11.18/pax

i.

Cost (Subsidy) per Passenger Kilometre: $4.82 (Aug 2019)

D) Farebox Recovery

Since 98.4% of monthly operating costs are fixed costs, are ridership and revenue increase,

farebox recovery also rises, reducing the net subsidy per rider.

i.

Farebox Recovery: 15.1% (Aug 2019)

E)

AT Local Performance Benchmarked Against Comparable Services

When comparing AT Local against eight other comparable services operated by Via Mobility,

it ranks highest for completion rate suggesting it is optimally resourced, whilst the third place

ranking for daily rides suggests improvements are possible. However, AT Local ranks second

for the second for peak hour rides, suggesting strong demand as a commuter service.

F)

Service Scalability

Implementation of the initial Devonport trial included one-off development and testing costs to

set up the App and Via Operating Console (VOC) framework, so new rideshare schemes can

leverage this to reduce the total expenditure associated with set-up.

However, it must be noted that when AT implemented AT Local, it did so using the existing

Via eco-system, which included operational, financial and reporting systems. This is a stand-

alone eco-system that operates outside of AT’s systems, so currently, all integration with AT

is manual. This includes (but is not limited to) customer feedback management, customer

communications, financial analysis, reporting and performance analytics.

In order to successfully implement additional rideshare schemes, consideration should be

given to integrating the Via / AT Local eco-system into the AT infrastructure.

3)

Performance Against the Six Key Objectives

A.

A Encourage modal shift away from private motor vehicle

Devonport, with a population of 23,000, has 30,000 car trips per day on Lake Road, with 50%

of trips being within the peninsula itself. Approximately 39% of customers use private motor

Page

5 of

13

vehicles, either as a driver or passenger, when travelling to or from the three local Devonport

Peninsula ferry terminals (public transport hubs).

Although local connector bus services are available, only 13% of ferry customers use them.

Five bus routes, covering all three ferry terminals, serve the Lower Devonport Peninsula but

there is a relatively low uptake of these options for a variety of reasons, including frequency,

reliability and the customer’s own proximity to the route(s).

Most ferry users live within three kilometres of the local ferry terminals and this, coupled with

the relatively flat geography, encourages both walkers and cyclists (combined 48%).

However, during wet weather, 13% of walkers and cyclists revert to the car, further

exacerbating local congestion.

AT Local provides customers with a reliable, low-cost alternative to the private motor vehicle,

effectively “mirroring” the journeys they take on an individual commuter basis e.g. from home

to the ferry terminal. However, importantly, because AT Local uses a smart algorithm to

maximise vehicle efficiency by aggregating rides, it reduces the total number of daily journeys

to and from the ferry terminals peak periods, whilst still transporting the same overall number

of customers.

AT Local Customer Survey: Main

Modal shift away from the private motor vehicle has been a

Mode of Travel to Ferry Terminal

significant contributory factor to AT Local’s on-going ridership

Pre-AT Local

increases. A recent in-market customer survey1 highlighted

Cycling

8%

that the AT Local customer profile broadly mirrors the travel

modes from the pre-AT Local survey. The survey showed 43%

Walking

31%

of car users had switched over to AT Local: 30% as car drivers

Bus

13%

and 13% as car passengers. This compares to 39%

identifying as car travel ers prior to AT Local’s introduction, so

Car passenger

13%

the service is delivering on this key objective. It should also

Car Driver

30%

be noted that only 13% of customers have switched from local

Other

5%

connector buses to AT Local, alleviating concerns that the new

service would “cannibalise” these routes

Translating this into monthly performance, in August, AT Local replaced a total 2,057 car

journeys and an average of 83 car journeys per weekday.

B.

Reduce congestion in the local Lower Devonport Peninsula area

The Devonport Peninsula is connected to the North Shore and beyond by Lake Road, the

main north – south arterial route, which can become extremely congested in both directions

during peak hours as ferry customers travel to and from the local ferry terminals, particularly

Devonport.

i.

Ride Aggregation1 by Week (12 Weeks from 27 May – 18 August)

1 Ride aggregation is where customer with individual bookings share one vehicle with other riders i.e. they have

each made individual bookings. This is distinct from where customers book for additional riders and also different

from other “rideshare” services, where individual customers “share” the ride with the driver, rather than with other

passengers.

Page

6 of

13

In the 12 weeks ended 01 September, ride aggregation averaged 31%. This rose to over 36%

during the four most recent weeks as ridership has increased to over 200 rides per week day,

showing that customers have embraced the concept of sharing the vehicles with others.

ii.

Ride Aggregation by Hour (12 Weeks from 27 May – 18 August)

A more granular analysis of operating hours provides greater insight into intra-day

aggregation, which rises to 49% between 07:00 – 08:00, corresponding to peak demand.

iii.

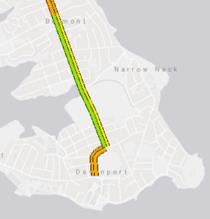

Congestion on Lake Road

Comparing peak inbound morning congestion between March 2019 and July 2019, there is

an improvement in the Albert Road / Victoria Road areas of Devonport. AT Local ridership

has increased by 151% between March 2019 (2,816) and July 2019 (4,247).

Inbound Lake Road Morning Peak Congestion

March 2019 July 2019

Page

7 of

13

C.

Social responsibility including improved sustainability through use of electric

vehicles

1)

Improve sustainability through the use of electric vehicles

AT Local delivered a world first in utilising an all-electric vehicle fleet for a rideshare scheme.

For period to 31 August, AT Local has delivered:

i.

27,481 rides

ii.

Average ride: 2.2km

iii.

10,652 motor vehicle trips replaced

iv.

65,538 passenger kilometres travelled

v.

8,651kg CO2 emissions saved (from active trips)

2)

Improve Travel Options for Accessible Customers

AT Local provides a safe, reliable, responsive and cost-effective transport option for

accessible customers, who can be more self-reliant when travelling locally. All three vans are

wheelchair accessible and customers can indicate they are an accessible customer using a

feature in the app. This ensures that an accessible vehicle will be automatically be assigned

to that ride request.

3)

Alignment with Vision Zero

AT Local uses professional drivers and offers customers safe and secure direct transport to

and from ferry terminals. It also reduces the incidence of distracted drivers travelling along

narrow side streets searching for parking spaces, assisting in creating a safer environment for

cyclists, pedestrians and other road users. Customers have a safer alternative if considering

driving when out socialising, with 21% of all rides on Fridays, compared to Mondays (15%).

D.

Deliver new innovative ways to meet customers ‘first’ and ‘final’ leg travel needs

Obtaining, analysing and translating customer feedback into prioritised actionable insights has

been crucial to delivering customer-focused improvements during the trial assisting in both

retaining existing customers and acquiring new ones throughout the trial.

Customers provide feedback using the “Rate My Ride” in-app feature at the conclusion of each

ride, or use the “Contact AT Local” in-app feature at any time. To date, 295 pieces of customer

feedback have been received, ranging from simple “one-liners”, to ride-specific issues,

through to detailed and constructive suggestions for improving the service.

Over 3,100 customers (13% of all bookings) have rated rides, with the average rating being

4.88 out of 5. The introduction of ‘friend-get-friend’ in-App referral offer during June has seen

over 100 customers acquired via this channel.

E.

Measure customers adoption and perception of the rideshare concept

Customer perception is measured by reliability, cost (fares) and ease of use (booking and

payment). Additional factors include driver attitude, other customers and ride comfort.

Customer adoption of AT Local demonstrates a strong demand, as performance to 31 August

shows:

i.

+2,950 customers have registered (20.7% of the target market)

Page

8 of

13

ii.

891 regular users (30.2% of customer base).

iii.

38% rides aggregated during peak hours (customers share the vehicle with others)

iv.

62% have taken at least one ride

v.

39% have taken three or more rides

vi.

4.88/5.00: Average customer rating

F.

Take learnings and applicability of the service for other parts of Auckland

The current AT Local trial has provided a considerable volume of transferrable knowledge and

insights that can be applied to any future rideshare operations. However, it is important to

note that in addition to these more generic aspects, each new rideshare area will include some

unique factors that must be taken into account in order that the operation is successful.

Below are some factors that should be considered when investigating new rideshare zones

and implementing new services. As each new rideshare operation is implemented, additional

learnings will result and these must be captured and considered as part of creating a living

framework for future schemes.

1)

Alternative Channels for Ride Requests:

i.

Provide alternative ride request options for customers, including:

a)

Telephone (e.g. via Contact Centre / Service Operator)

b)

Web-browser – online booking

c)

SMS services.

ii.

Extending channel options wil extend AT Local’s reach into both the senior citizen

community and also those market segments that are not digitally enabled.

Feedback from senior citizens and advocacy groups is that they would use AT

Local but they either do not have, or cannot use, smart phone technology.

2)

Alternative Payment Options:

i.

Provide alternative payment options, including:

a)

AT HOP cards,

b)

Cash on-board

Page

9 of

13

c)

Pre-paid voucher system.

ii.

Alternative payment options would allow other communities to use the service,

particularly senior citizens and those who do not have ready access to pay cards.

3)

Locations for New Services:

Should be supported by a detailed analysis of the local travel patterns, including both

current public transport and all other active and passive modes. These should include

(but not be limited to):

i.

Current public transport travel patterns by time of day and day of week

ii.

Current travel patterns using other modes by time of day and day of week e.g.

private motor vehicle, active modes etc.

iii. Analysis of local employers, numbers of employees, including shift patterns etc.

iv. Analysis of local amenities / facilities e.g. hospitals, schools, leisure activities

4)

Customer Segments:

Detailed analysis of the various customer segments within the target area is necessary

to ensure the service will meet their needs e.g. senior citizens require alternative ride

booking and payment options, rather than a solely App-based service.

5)

Promoting New Service Areas:

i.

Determine the channels preferred by the target market segments – these should

be the primary focus of customer promotional material

ii.

Encourage support from local businesses

iii. Commence the promotional campaign between two and four weeks prior to the

service launch to generate customer interest

iv. Promotional material must be clear in terms of the service offering:

a)

Whether the service is a rideshare service or a taxi

b)

How to book and pay for rides i.e. channel availability

c)

App Store Links to the Rideshare App (N.B.: It’s not an AT product)

d)

Links to support channels e.g. web page

e)

Rideshare zone and boundaries

f)

Fares – per person, not per trip

g)

Discounts e.g. Senior Citizens, Children

h)

Days and hours of operation

i)

Numbers and types of vehicles e.g. cars, minivans

j)

Security features: e.g. Paycard security, on-board CCTV

k)

If cash is not accepted, specify this as it also increases driver safety

v. Offer time-based incentives for pre-launch customer sign-ups to translate this into

early ridership e.g. Promotional Codes with expiry dates

vi. Pre-launch beta-testing with local residents to test the service and create

advocates who will promote the service in the post-go

Page

10 of

13

6)

Other Factors For Consideration:

i.

Geography and Proximity of Customers to Public Transport Hubs

Most customers using the local ferries live within three kilometres of the respective

terminals and since the current trial area is mainly flat, it is relatively easy for

people to walk or cycle to the ferry terminals. (39% of ferry users walk or cycle to

the ferry terminals).

Whilst there are some steeper sections within the rideshare zone that can present

challenges to customers with mobility impairment, overall, the relatively flat terrain

means easy walking and cycling routes. Consequently, many of these customers

switch to AT Local during adverse weather conditions, although the positive aspect

is that they do not revert to the private motor vehicle.

ii.

Weather Conditions

Auckland experienced an extended period of warm, dry weather from January

2019, with autumn and winter being the warmest and driest on record. These

factors have impacted demand for AT Local, which has shown a degree of

correlation with the prevailing weather conditions. AT Local ridership has risen

sharply on days with adverse weather conditions during the morning and afternoon

peaks.

The sharp contrast between July (4,247 rides) and August (5,263 rides) illustrated

the effect of rain. July’s rainfall was only 83% of the average, whereas August

experienced the highest number of days with rain on record (as opposed to total

rainfall, which was 89% of the average).

4)

Recommendations for Current AT Local Trial

A)

Continue the Current AT Local Service But with Service Changes

It is recommended that the current AT Local rideshare trial operating on the Lower

Devonport Peninsula should continue as a permanent first and last leg option for

customers. However, it is further recommended that the following changes are made to

improve the service offering and broaden its appeal to wider constituency groups.

1)

Change Operating Hours

i.

Mon – Fri Commuter Service Only)

Current weekend ridership is significantly below that of weekdays and there is a high

fixed cost component associated with providing weekend services. Therefore, it is

proposed that the current trial revert to a 5–day a week commuter-based service.

Page

11 of

13

Day

Current

Proposed

Annual Riders:

Annual Operating

Operating

Operating

+Increase / -

Cost Savings / (Extra

Hours

Hours

Decrease

Costs)

Mon - Thu

05:40am –

06:00am –

-750

21:20pm

21:00pm

Fri:

05:40am –

06:00am –

+500

21:20pm

22:00pm

Sat:

08:25am –

No Service

-2,324

18:50pm

Sun / Public

08:25am –

No Service

-2,063

Holiday:

18:20pm

Total

-4,637 Riders

Whilst there is a reduction in total annual ridership (4,637 riders), the associated revenue

loss is more than offset by the annualised cost savings.

2)

Provide Alternative Channels for Ride Requests

(Subject to additional trials commencing to defray the development and implementations

costs)

i.

Provide alternative ride request options for customers, including:

a)

Telephone (e.g. via Contact Centre / Service Operator)

b)

Web-browser – online booking

c)

SMS services.

ii.

Extending channel options wil extend AT Local’s reach into both the senior citizen

community and also those market segments that are not digitally enabled.

Feedback from senior citizens and advocacy groups is that they would use AT

Local but they either do not have, or cannot use, smart phone technology.

3)

Provide Alternative Payment Options

(Subject to additional trials starting to defray development and implementations costs).

i.

Provide alternative payment options, including:

a) AT HOP cards

b) EFTPOS on board

c) Cash on board

d) Pre-paid voucher system.

ii.

Providing alternative payment options would allow other communities to use the

service, particularly senior citizens and those who do not have ready access to

payment cards.

Page

12 of

13

4)

Expand Rideshare Zone

4)

Expand Rideshare Zone

i.

Off-Peak Hours

a) Expand the current rideshare zone boundary north to Hauraki Corner (shaded

in Yellow), using the

natural

boundary

line

created by Jutland Road

and Hauraki Road (runs

NE – SW).

b) Includes approx. 2,000

extra households

c) Determine impact on off-

peak

ridership

to

determine

if

genuine

demand

exists

and

vehicle optimisation.

ii.

Peak Hours

a) If

the

extension

of

services during off-peak

hours

is

successful,

consideration should be

given to running the same trial during peak hours.

Page

13 of

13