Board Meeting | 28 April 2014

Agenda item no. Entered by board secretary

Closed Session

Integrated Fares

(Note, yellow highlights are changes to the previously uploaded paper resulting from feedback

from the 20 April CFC meeting.)

Recommendation(s)

That the board:

i.

Receives the report

ii.

Notes that additional external AT Metro funding to minimise HOP fare increases from

the transition to integrated fares has not been forthcoming, resulting in a feasible

pricing Scenario 1 ‘revenue neutral’ (previous scenario A from October 2014 Board)

with two additional pricing scenarios under consideration to achieve a Scenario 2

‘minority HOP fare increases’ and Scenario 3 ‘minimal HOP fare increases’. Final

approval of the preferred pricing scenario and fare prices will be sought from the

Board later in 2015, considering feedback from public consultation, and confirmed

three year LTP/NLTF AT Metro funding plus identification of other opex reductions,

including potential reduction in low patronised PT services, to cover unbudgeted

revenue reductions and increased passenger capacity costs under the alternative

scenarios.

iii.

Approves the product development roadmap including:

a. Stored Value from single leg/trip single fare (with 50c transfer discount) stage

based to single journey concept comprising 2-hour travel across up to 3 legs

b. Simplified Day and Monthly passes with single all-zone month pass for

bus/train and three consistent inner, mid and outer harbour ferry passes

c. Simplified day pass with single all-zone day pass (includes inner harbour

ferries)

d. Review a transition from Day and Monthly passes to fare caps after

stabilisation of integrated fares

iv.

Approves targeted public consultation on indicative fares and structure in May via the

RPTP variation process including:

a. Proposed geographic zones and boundaries

b. Indicative range of pricing levels to accommodate pricing scenarios 1 to 3.

c. Product transition roadmap

v.

Notes proposed go-live of integrated fares to April 2016

vi.

Notes an increase in the integrated fares budget from $6.85M to $8M.

Executive summary

Further to the Board approval in October 2014 of the business case and fare structure concept

for AT Metro integrated fares, further work has been completed to:

(a) identify indicative pricing scenarios

(b) confirm the proposal for the AT Metro ticket product roadmap

Page 1

Board Meeting | 28 April 2014

Agenda item no. Entered by board secretary

Closed Session

(c) confirm project timeline and budget with confirmed Thales development activities

(d) with an improved technical development solution by Thales.

Attachment 1 provides an update to the Customer Focus Committee presentation of 20 April

2015 to accommodate feedback provided at that meeting.

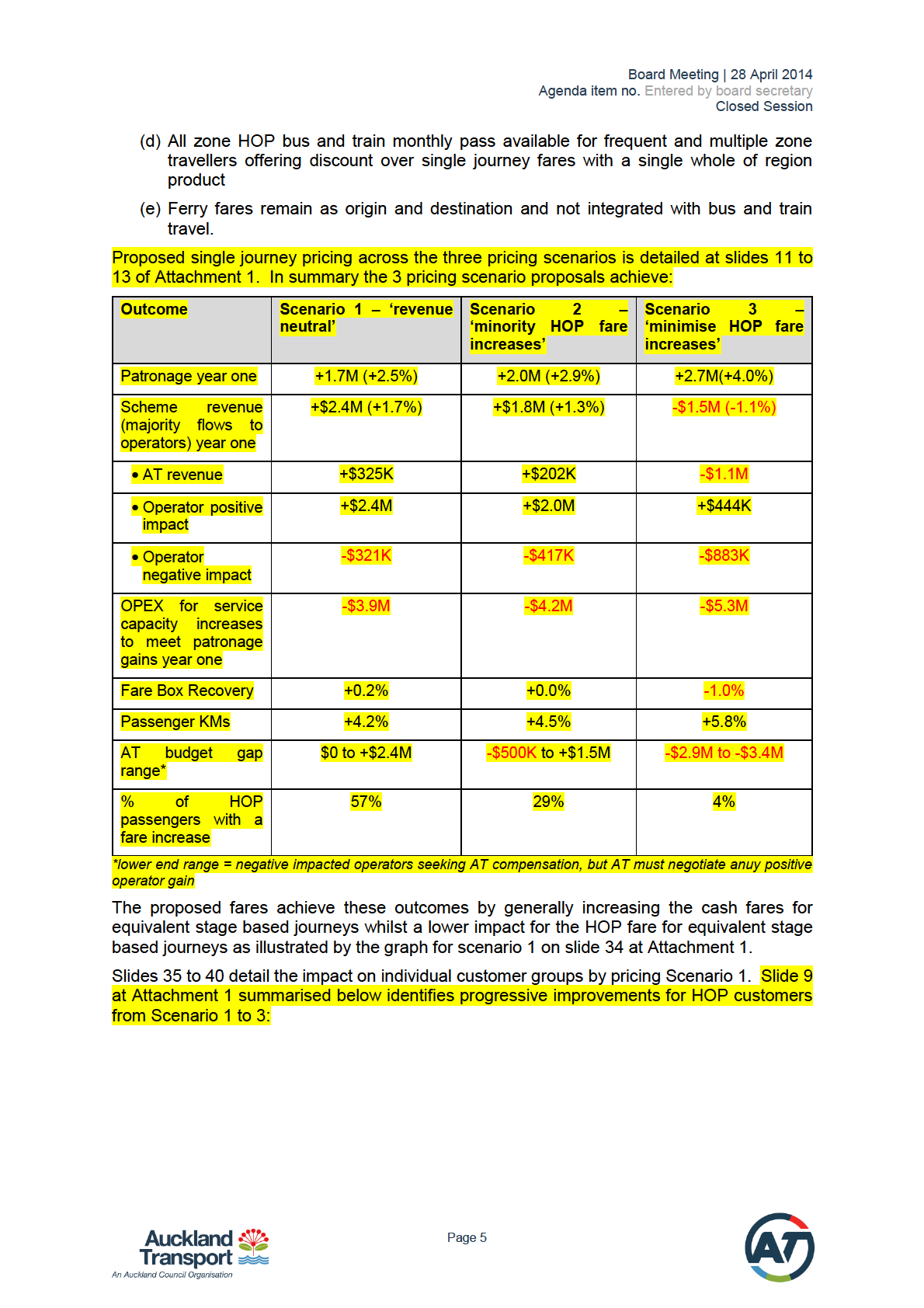

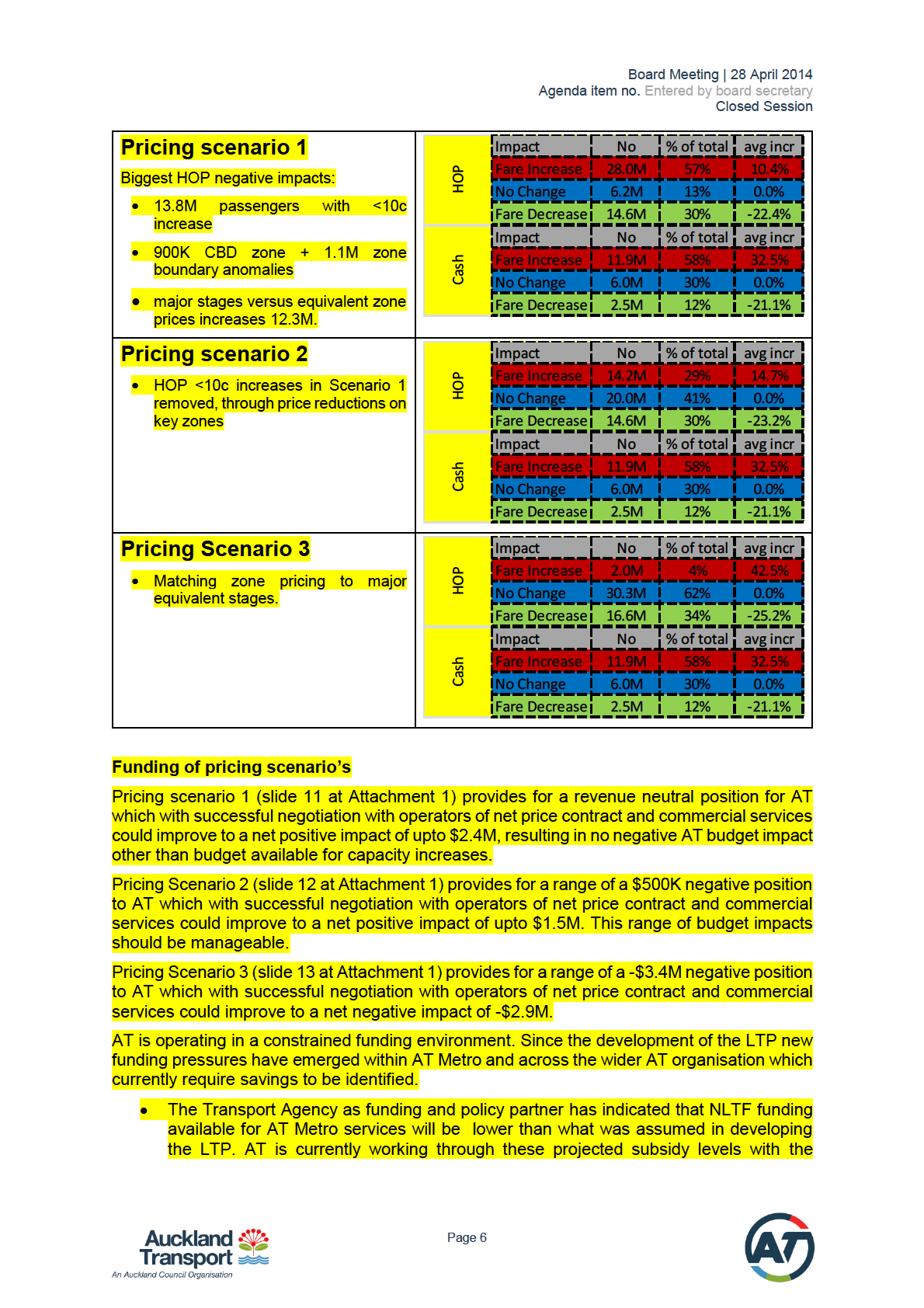

There are three indicative price scenario’s in this paper detailed on slides 9 to 13 at Attachment

1 which achieve improving fare outcomes for customers:

Scenario 1 ‘revenue neutral’ based on no additional specific external funding beig

forthcoming: 43% HOP fare user price reduction or no change; +$2.4M per annum

scheme revenue increase; $3.9M per annum capacity increase (budgeted) for +1.7M

passenger boardings per annum; zero unbudgeted impact on AT; +0.2% farebox

recovery

Scenario 2 ‘minority HOP fare increases’: 71% HOP fare user price reduction or no

change; +$1.8M per annum scheme revenue increase; $4.2M per annum capacity

increase ($4.0M budgeted) for +2M passenger boardings per annum; -$0.5M

(unbudgeted) to +$1.5M (favourable) per annum AT budget impact; 0% farebox

recovery impact

Scenario 3 ‘minimising HOP fare increases’: 96% HOP fare user price reduction or no

change; -$1.5M per annum scheme revenue decrease; $5.3M per annum capacity

increase ($4.0M budgeted) for +2.7M passenger boardings per annum; -$2.9M

(unbudgeted) to +$3.4M (unbudgeted) per annum AT budget impact; -1% farebox

recovery impact

All the above scenarios see significant cash fare increases and increasing the HOP to cash

differential from at least 20% to at least 33%. All scenarios see the residual 4% of HOP

passengers with a fare increase as a result of the removal of micro-zone fares (CBD and

airport), removal of anomalies between bus and train fare stages (eg Orakei station) and some

zone boundaries differing from current stage boundaries.

AT is still confirming with Council and Transport Agency partners the three year AT Metro

funding through the LTP and NLTF. Other opex funding will also need to be identified to fill

funding gaps for Scenarios 2 and 3. With consideration of public consultation feedback, the

final pricing scenario and pricing levels for integrated fares will be confirmed to the Board later

in 2015, with a view to progressing as far as possible towards Scenario 3. In parallel,

confirmation of Scenario 3 BCR above 1.0 will be required to complete the application to the

Transport Agency for funding.

As part of the introduction of integrated fares, it is proposed to rationalise products, removing

those that lack uptake and replacing them with simplified day and monthly pass zone options.

A transition path is proposed to review the revenue and customer demand of integrated fares

and period passes after introduction of integrated fares when the AT Metro customer and

revenue base beds-in to assess the benefits and impacts of a transition from period passes to

fare caps. This substantially de-risks the revenue exposure to AT after the go-live of integrated

fares during the next two years.

The proposal is to implement a substantially simplified HOP product suite alongside the revised

HOP stored value 2-hour 3-leg journey single fare and cash single trip offering:

(a) Single all-zone day pass that includes inner harbour ferries

Page 2

Board Meeting | 28 April 2014

Agenda item no. Entered by board secretary

Closed Session

(b) Single all-zone monthly pass

(c) 3 ferry monthly passes - inner harbour, mid harbour and outer harbour, subject to

confirmation of technical solution and commercial negotiation with ferry operators.

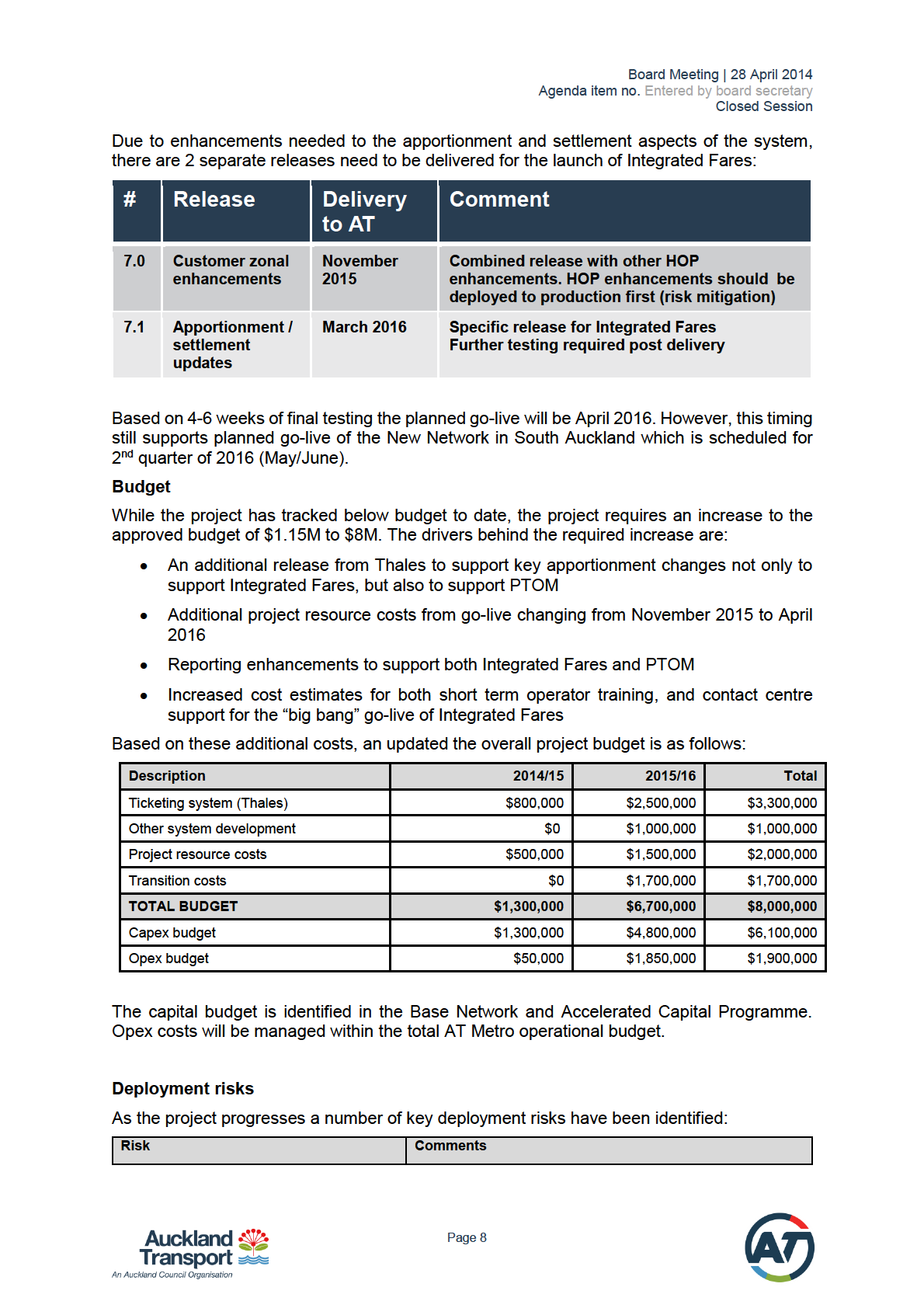

Based on the Thales confirmed development schedule of the ticketing solution, the planned

go-live date is April 2016. Following confirmation of Thales development costs for the back-

office apportionment solution and higher planned public communications costs the project

budget will need to increase by $1.15M to $8M.

It is proposed that targeted public consultation occur in May 2015 based on the current

modelled zone pricing ranges and products outlined in this paper via the RPTP variation

consultation proposed for May.

Strategic context

The Regional Public Transport Plan (RPTP) is in the process of being varied to reflect amongst

other updates, the move to integrated fares. It will set out key fares policy, the 2-hour 3-leg

journey concept for AT HOP single fares and product offering, and the proposed zone map.

There will be consultation for the RPTP and targeted integrated fares consultation will be

aligned.

Integrated Fares remains a key element for successful implementation of the AT Metro New

Network to allow passengers to transfer without financial penalty and to provide a simpler,

more intuitive fare structure to support aggressive patronage growth targets for Auckland.

Introduction of a zonal fare structure will bring Auckland in line with many leading international

cities and provide a platform for future growth of public transport.

The proposal is aligned to the AT strategic themes to prioritise rapid, high frequency public

transport and transform and elevate customer focus and resilience through offering a more

intuitive and simpler fare structure.

Pricing scenarios requiring additional opex cannot be confirmed until three year LTP/NLTF AT

Metro funding is confirmed over the coming two months and other potential opex and service

reductions are identified to cover unbudgeted revenue reductions and service capacity cost

increases.

Background

In October 2014 the Board resolved:

Adoption of the business case.

Approved a 2-hour single journey HOP fare (up to 3 individual trips) across bus and rail

with daily caps, weekly caps or passes and introduction of neighbourhood fare zones

Approved a preferred pricing strategy of ‘limit HOP fare increases’ subject to

identification of the additional opex funding required

Noted acceptance of two alternate pricing scenarios (‘patronage retention’ and

‘revenue neutral’) based on the level of additional opex funding availability.

Approved release of integrated fares information for public consultation

Noted that detailed pricing will be brought back to the Board prior to implementation

Approved commencement of development of integrated fares to achieve

implementation by November 2015.

Page 3

Board Meeting | 28 April 2014

Agenda item no. Entered by board secretary

Closed Session

Progress since the October 2014 Board meeting is detailed in the updated (following feedback

from the 20 April 2015 meeting) Customer Focus Committee presentation provided at

Attachment 1, with the key points of change or confirmation highlighted below.

Issues and Options

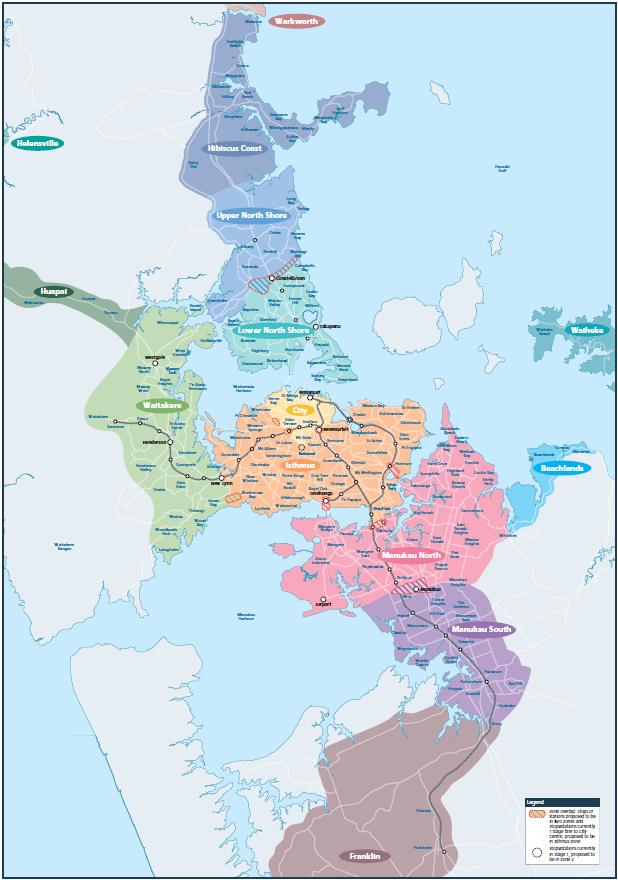

Fare zones

The fare zone map previously presented has been refined with Auckland divided into

geographic zones radiating out from the central city which are separately labelled and

coloured (Attachment 2). This includes refinements which reflect feedback from focus

groups held in mid-2014. The map will be core in helping Aucklanders understand the

zonal fare structure and will be a key focus during the planned public consultation.

Product suite: bus and train

The bus/train ticket product suite is illustrated at slide 6 in Attachment 1. In summary:

(a) A 2-hour journey of up to 3-legs for AT HOP single fare paying for zones passed

through (only once per zone) as illustrated at slides 7 and 8 at Attachment 1

(b) Cash fares limited to single leg journeys as illustrated at slide 8 at Attachment 1

(c) A preferred option of a family weekender pass (2 kids free with a fare paying adult)

(d) A whole region single bus/train/inner harbour ferry day pass of $18

(e) A whole region single bus/tain monthly pass of $205

(f) Potential migration from above day and monthly passes to fare caps based on

modelling post implementation of integrated fares when revenue and customer

behaviour change can be accurately modelled following bedding in of the integrated

fares proposal.

Slides 14 and 15 at Attachment 1 provide further rationale for the simplification of existing day

and monthly passes and the future transition potential from period passes to fares caps when

revenue and customer behaviour change risk can be accurately assessed after the broader

change to integrated fares.

Fares pricing

The integrated fares model has been updated quarterly (currently to December 2014) with the

latest HOP data to ensure modelled outcomes closely match passenger behaviour. In

development of the indicative fares the following three key principles have been followed:

(a) Minimise impacted passengers - minimise the number of passengers with fare

increases (particularly HOP passengers)

(b) Minimise extent - where there are increases, minimise extent of increase

(c) Promote longer distance PT use - ensure longer distance travel is cheaper as this

delivers the highest economic benefit (increased passenger kms)

The following fare rules have been applied which will form part of key public messages:

(a) Adult HOP single fare customers receive at least 33% discount off cash journeys with

a single leg and more on multi-leg journeys

(b) Child and accessible fares are at least 40% cheaper than the equivalent adult fare

(c) Tertiary HOP fares are at least 20% cheaper than Adult HOP fares

Page 4

Board Meeting | 28 April 2014

Agenda item no. Entered by board secretary

Closed Session

Agency. However, initial additional opex reductions may need to be identified and will

be known by June.

Other AT projects have signalled a requirement for more opex budget in the 2015/16

financial year than was allocated in the LTP. This will be finalised by June.

Currently, any possible opex reductions that may be identified will need to be utilised to help

close the LTP funding gap before considering integrated fares pricing scenarios.

If a decision is made to proceed with an Integrated Fares scenario that is not revenue neutral

(pricing Scenarios 2 or 3) then the only feasible way this could be funded is through:

Reducing some existing low patronised PT services

Negotiating a revenue clawback on net price contracted and commercial services with

operators

Identify other opex and service reductions.

Since sufficient opex funds internally for pricing Scenario 3 have not yet been identified final

confirmation of pricing levels will be confirmed to the Board later in 2015.

Scenario 3 results in a worsening of the fare box recovery ratio by 1% which would require

above CPI increases in fares and or an extension of the timeframe to meet NZTA fare box

recovery targets.

Another factor is the need to meet criteria for Transport Agency co-investment. At present

this initiative has a benefit-cost ratio (BCR) of 1.9, making it High, High, Low using the

Transport Agency’s assessment criteria. At this level they will still co-invest but will not do so

if the BCR falls below 1.0. The current ratio is based on a capital cost of approx. $7 million

and a revenue-neutral option for on-going cost. The changes proposed in Scenario 3 are

likely to still keep the project above a cut-off BCR of 1.0. Modelling required to complete the

application to the Transport Agency will confirm this. Should the project look likely to drop

below a BCR of 1.0 we will need to reconsider fare revenue and this will also be considered

in the subsequent report-back.

Ferry products

The zonal fare structure outlined above will not apply to ferries, at least in the initial stages.

Including ferries in the full zonal system would be expensive, as current ferry fares are higher

than comparable bus and train fares. Furthermore, the integration of ferries is further

complicated by exempt services – Devonport, Waiheke and Stanley Bay, which are outside of

AT’s contractual control. The existing point-to-point fares for ferry services will therefore

continue to apply, pending further work on integrating them into the zonal structure.

However, investigations are underway to examine whether ferries could in part be

incorporated into a zonal solution and journey concept, at least in part. The concept is:

Ferry HOP fare is land based equivalent fare plus one zone, incorporating origin and

destination land based PT travel.

Grouped radiating distance based monthly passes (slide 20 at Attachment 1)

Grouped radiating distance based cash prices

This approach requires further technical validation with Thales, and would require commercial

negotiation with operators.

The product migration path for ferries is detailed on slide 19 of Attachment 1

Project schedule, budget and deployment risks

Page 7

Board Meeting | 28 April 2014

Agenda item no. Entered by board secretary

Closed Session

Attachment 2: Proposed zonal map

Page 11