Fraud Policy

Fraud Policy

Governance Policy

Policy Owner

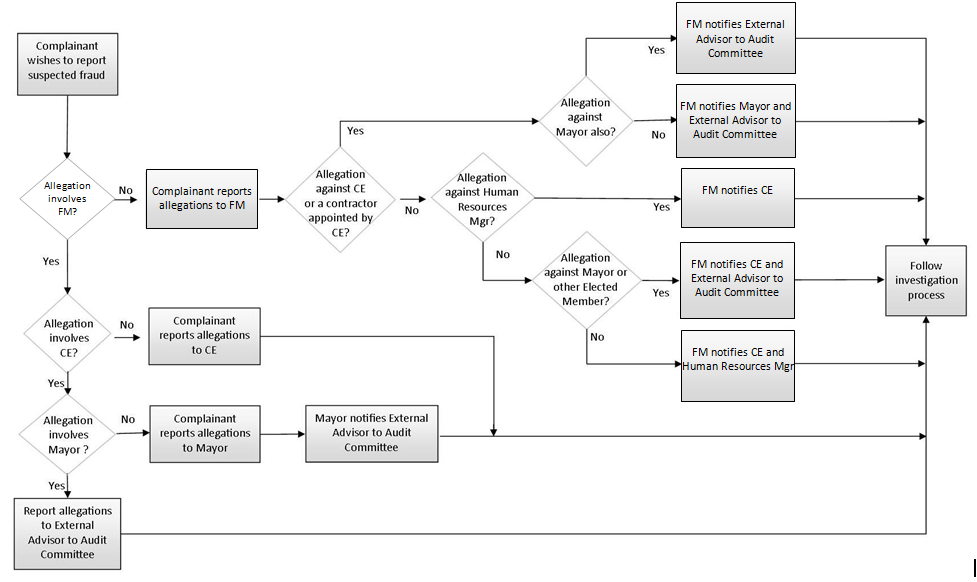

Legal Audit and Risk Group Manager

Adopted by

Thames-Coromandel District Council

Description of policy

States the Council's zero tolerance position on fraud against the

Council and sets out the guidelines and procedures for the prevention,

detection and investigation of suspected fraud or attempted fraud.

Keywords

Fraud, corruption, misconduct, crime, conduct, investigation, theft,

bribery, dishonesty.

ECM doc set number

Date policy first adopted

25 October 2006

Date this version adopted: 12 March 2019

This version effective from:

12 March 2019

Date of next review:

1 March 2022

Objectives

The objectives of the Fraud Policy are to:

•

Protect the integrity of the Thames-Coromandel District Council's financial systems,

assets and reputation from fraudulent and corrupt conduct;

•

Ensure an environment in which fraud or corruption are not tolerated and any

suspected incidents are reported on;

•

Ensure that adequate processes are in place to enable detection of such conduct;

•

Ensure that any instances of fraud or suspected fraud are properly investigated and

acted upon appropriately to mitigate any damage caused and avoid recurrence;

•

Ensure clear accountability by allocating responsibilities for fraud prevention and

response.

Background

This document supersedes the previous version adopted by the Thames-Coromandel District

Council on 7 August 2013.

Legal requirements

The Local Government Act 2002, s101(1) requires that a local authority must manage its

revenues, expenses, assets, liabilities, investments and general financial dealings prudently.

Section 111 also requires that:

“all information that is required by any provision of this Part or of Schedule 10 to be included

in any plan, report, or other documentation must be prepared in accordance with generally

accepted accounting practice if that information is of a form or nature for which generally

accepted accounting practice has developed standards.”

The auditing standard “The Auditor’s Responsibilities Relating to Fraud in an Annual Report"

(AG ISA (NZ) 240) falls within the definition of “generally accepted accounting practice”. This

standard state that the primary responsibility for the prevention and detection of fraud rests

with both those charged with governance of the entity and management. It also states that

Doc set:

1

every public entity is expected to have an appropriate policy in place to address fraud and

how to minimise it. This policy should include, as a minimum, the following key elements:

• a system for undertaking regular reviews of transactions, activities, or locations that may

be susceptible to fraud;

• specifications for fully documenting what happened in a fraud and how it is to be

managed;

• the means for ensuring that every individual suspected of committing fraud (whether they

are an employee or someone external to the entity) is dealt with consistently and fairly;

and

• the principle that recovery of the lost money or other property will be pursued wherever

practicable and appropriate.

Under the Local Government Act 2002, Council is also required to have various financial

statements and plans audited.

Policy framework

The Council has in place several other key policies that link to the fraud policy. These are:

Code of Conduct Policy

This policy is required under Schedule 7 of the Local Government Act 2002 and provides

standards of general behaviour for elected members and how breaches should be

addressed.

Misconduct and Disciplinary Policy

This policy deals with breaches to expected standards of conduct for staff and specifies

investigation procedures and disciplinary measures that may be taken where misconduct is

found to have occurred.

Protected Disclosures Policy

This policy is mandatory under the Protected Disclosures Act 2000. The policy provides

procedures to ensure protection for employees (including elected members, contractors,

former employees, volunteers and persons on secondment to the organisation) in disclosing

information about serious wrongdoing in or by the organisation.

Procurement Policy

Details the correct procedures for procurement and includes sections on conflicts of interest

and ethics prohibiting a number of activities meeting the definition of fraud under this policy.

Sensitive Expenditure Policy

Provides business processes to control sensitive expenditure. The policy does not cover

breaches with the exception of unauthorised use of a credit card and refers to the Fraud

Policy for such breaches.

Implementation

All staff and elected members will be notified of this revised policy and where to access a

copy.

All new staff and elected members will be provided with a copy of the policy upon

commencement of employment or term of office.

Implementation will include the development and maintenance of, and adherence to, a Fraud

Control Plan as per the Policy.

Recognising fraud and corruption risks

Council recognises that generally there are three particular conditions often associated with

fraud and corruption:

Doc set:

2

•

Incentives/pressures: Management, other employees or external parties have an incentive

or are under pressure, which motivates them to commit fraud, or act in a corrupt manner

(for example, personal financial trouble), or revert to bribery for preferential treatment by

council staff.

•

Opportunities: Circumstances exist that allow employees to commit fraud or act in a

corrupt manner, such as an organisation not having appropriate fraud and corruption

controls in place, or bribe council staff who are able to get around or override ineffective

controls (for example, managers being able to approve and authorise their own sensitive

expenditure, or health and safety inspectors issue compliance certificates instead of failing

the applicant).

•

Attitudes: Employees can rationalise committing fraud (for example, holding attitudes or

beliefs such as “everybody else is doing it nowadays” or “they made it so easy for me”) or

acting corruptly.

In performing its duties, the Council is responsible for the careful management of public

funds. Failure to have an effective fraud policy in place or to implement it may jeopardise

public money and assets.

Any adverse publicity surrounding an internal fraud places the Council’s reputation and

credibility at risk, which can negatively impact on relationships with regulators, business

partners and the general public. Without a clear policy and procedures for dealing with

suspected or confirmed fraud, there is a risk to the Council of a public perception of lack of

transparency and accountability. If serious action is not taken in instances of fraud, staff

confidence in managers is also likely to erode, and there is an increased risk of further fraud.

Factors that may impede the implementation of the Policy include lack of awareness of the

Policy by appropriate staff, elected members or other parties, non-compliance with Council's

systems, or inadequate procedures to anticipate and provide controls against deliberate

attempts to bypass the system (for instance, the ability of managers to override controls, lack

of independent checks/authorisations of transactions).

Policy statement

The Thames-Coromandel District Council requires all staff, elected members and parties

doing business with the Council to act honestly and with integrity and to safeguard any public

resources for which they are responsible. The Council will not tolerate any fraud or corruption

or any condoning or attempt to disguise such activities. All employees and elected members

are responsible for promptly reporting instances of suspected fraud using the procedures

outlined in this policy.

Implementation

1.

Application

This policy applies to any attempted, suspected or confirmed fraud or corruption involving

employees, elected members, consultants, vendors, contractors, members of the public and

outside agencies doing business with the Thames-Coromandel District Council.

2

Prevention

Responsibility

2.1

Written procedures and checks will be developed and maintained for

People &

the recruitment or promotion of employees to sensitive positions,

Capability

including thorough and independent checks of the potential employee’s

Manager

employment history to ensure the applicant is suitable for the position.

2.2

Due diligence checks will be carried out on all suppliers, contractors

Legal Audit and

and consultants prior to commencement of any business arrangement.

Risk Group

Manager

2.3

All staff will be provided with a copy of the Fraud Policy as part of their

People &

staff induction.

Capability

Manager

Doc set:

3

2.4

All elected members will be provided with a copy of the Fraud Policy on

Governance and

the commencement of their term in office.

Strategy Group

Manager

2.5

Accounting systems and procedures will be in accordance with

Corporate

generally accepted accounting principles.

Services group

Manager

2.6

A Fraud Control Plan including a register of fraud risk and internal

Chief Executive

controls for each area of the organisation will be developed within one

year of the adoption of this policy.

2.7

The Fraud Control Plan will include provisions to ensure an annual

Chief Executive

review of transactions, activities or locations that may be susceptible to

fraud is incorporated into the Audit and Risk Committee audit

programme.

2.8

For each fraud risk identified, the Fraud Risk Register will detail the

Chief Executive,

following:

All members of

Leadership Team

•

The area of business involved

•

Position responsible for managing the risk

•

General aims/policies relating to the issue

•

Preventive actions and controls

•

Any particular circumstances that would trigger an early review

•

Appropriate details to ensure the actions are implemented

effectively (such as roles responsible, timeframes)

•

Dates of last audit

2.9

The Fraud Risk Register will be reviewed for each area of the business

Chief Executive,

at least every two years.

All members of

Leadership Team

2.10

The appropriate manager will implement changes to procedures and

Relevant

systems as required by revisions of the Fraud Risk Register.

manager of

Leadership Team

2.11

Except for access to separate sections as required for the above

purposes by relevant managers, access to the Fraud Risk Register will

be restricted to the Chief Executive, Legal Audit and Risk Group

Manager and the Audit Director appointed by Audit New Zealand.

2.12

The Chief Executive will report to the Audit and Risk Committee

Chief Executive

annually on any updates to the Fraud Risk Register.

2.13

Subject to any legal constraints, staff and elected members will be

Chief Executive

notified of any cases of confirmed fraud and the actions taken in such

cases.

Doc set:

4

3

Detection

3

Detection

3.1

All staff and elected members will be encouraged to report any

Chief Executive

incidents of suspected fraud or corruption.

3.2

All staff and elected members in positions most likely to be able to

Line Managers,

detect fraud will receive training on warning signs and areas of risk.

Human Resource

Manager

3.3

The Council may implement covert mechanisms and/or surprise

Chief Executive

internal audits to detect fraud as appropriate with approval of the Chief

Executive.

3.4

A periodic review of expenditure approved by employees in sensitive

Chief Executive

positions will be carried out by the Internal Auditor.

4

Reporting and notification

4.1

Any person may report suspected or attempted fraud.

4.2

Disclosures may be made under the provisions of the Protected

Disclosures Act 2000 as applicable by following the procedures

contained in the Council’s Protected Disclosures Policy.

4.3

While complainants reporting incidents or suspicions will be

encouraged to identify themselves, anonymous reports will be

accepted.

4.4

A Fraud Complaint Manager will be appointed by the Chief Executive

to receive complaints and coordinate the response. The Legal Audit

and Risk Group Manager has been appointed Fraud Complaint

Manager from the date of this policy until such time as a new

appointment is made.

4.5

Any fraud that is detected or suspected must be reported immediately

to the Fraud Complaint Manager.

4.6

If it is believed that the Fraud Complaint Manager may be involved in

the suspected fraud, the fraud shall instead be reported to the Chief

Executive, who will take over the role of Fraud Complaint Manager

from that point.

4.7

If it is believed that the Chief Executive may also be involved in the

suspected fraud, the fraud shall instead be reported to the Mayor, who

will take over the role of Fraud Complaint Manager from that point.

4.8

If it is believed that the Mayor may also be involved in the suspected

fraud, the fraud shall instead be reported to the External Advisor. The

contact details of the External Advisor shall be provided on the

Council's Intranet site.

4.9

Any person wishing to report a suspected fraud is entitled to address

their concerns directly to the Police, the Office of the Auditor-General

or other appropriate agency if they believe it appropriate.

4.10

If there is any question as to whether an action constitutes fraud, the

Fraud Complaint Manager should be contacted for guidance.

4.11

On receiving information about a suspected fraud, the Fraud Complaint

Fraud Complaint

Manager will open a fraud investigation file which will contain a written

Manager

summary of the complaint, investigation findings and action/s taken.

Doc set:

5

4.12

In the case of an allegation against a staff member, the Fraud

Fraud Complaint

Complaint Manager will notify the Chief Executive and the People &

Manager

Capability Manager of the information received unless either is

believed to have been involved in the alleged fraud. If it is considered

the People & Capability Manager may be involved, the Fraud

Complaint Manager will notify only the Chief Executive.

4.13

If it is considered the Chief Executive may have been involved in the

alleged fraud, the Mayor and the External Advisor will be notified

instead.

4.14

In the case of an allegation against the Mayor or any other Elected

Member of Council or a Community Board, the Fraud Complaint

Manager will notify the Chief Executive and the External Advisor.

4.15

In the case of an allegation against a contractor appointed by the Chief

Executive, the Mayor and the External Advisor will be notified instead

of the Chief Executive.

4.16

The Fraud Complaint Manager will not disclose the identity of the

complainant unless requested or agreed to by the complainant.

4.17

Any attempt to deter or impede a suspected fraud being reported or

Fraud Complaint

investigated or any false or malicious allegation of fraud by any staff

Manager,

member will be treated as a serious misconduct under the Misconduct

People &

and Disciplinary Policy.

Capability

Manager

4.18

Any attempt to deter or impede a suspected fraud being reported or

Fraud Complaint

investigated or any false or malicious allegation of fraud by any elected

Manager,

member will be treated as a serious offence under the elected

Audit and Risk

members Code of Conduct.

Committee

4.19 Upon receiving information about a suspected fraud, the Fraud

Complaint Manager will as soon as possible notify the External Advisor

and Chairperson of the Audit and Risk Committee.

Doc set:

6

Reporting and notification process

5

Investigation

Reporting and notification process

5

Investigation

5.1

No complainant, member of staff or elected member shall attempt to

conduct an investigation, except as provided for in this policy.

5.2

No aspect of an investigation or allegation may be discussed by any

party with any other person except where necessary for the purposes

of carrying out the investigation or as otherwise provided for under

this policy.

5.3

In any case of an allegation involving the Chief Executive or a

contractor or consultant appointed by the Chief Executive, an

investigation will be coordinated by the Mayor and the External

Advisor following the procedures in this policy.

5.4

In any case of an allegation involving the Mayor or any other Elected

Member of Council or a Community Board, the investigation will be

coordinated by the Chief Executive and the External Advisor.

5.5

In any case of an allegation involving the Mayor and the Chief

Executive, the investigation will be coordinated by the Fraud

Complaint Manager and the External Advisor.

5.6

In any case of an allegation involving the Fraud Complaint Manager,

the investigation will be coordinated by the Chief Executive.

5.7

In all other cases, the investigation will be coordinated by the Fraud

Complaint Manager.

5.8

Where appropriate, the person undertaking the investigation will seek

Investigator

appropriate legal counsel or other professional advice before the

investigation begins.

5.9

Where appropriate and practicable, the person undertaking the

Investigator

investigation will make discreet enquiries to ascertain fundamental

Doc set:

7

facts to determine the seriousness and validity of the allegations.

5.10

If preliminary findings suggest further investigation is warranted the

Investigator

investigator may establish an Investigation Team including, as

appropriate the People & Capability Manager and/or an external

investigator. In the case of an allegation against a staff member, this

decision will be taken in consultation with the Chief Executive or

Mayor as appropriate.

The external investigator may be an external forensic investigator,

specialist fraud investigator and/or the External Advisor and/or other

specialist as needed.

The investigation team will investigate whether there is sufficient

evidence that a crime has been committed.

5.11

Members of the investigation team shall have free and unrestricted

access to all Council records and premises, and the authority to

examine, copy and/or remove all, or any portion of, the contents of

files, desks, cabinets, computers and other storage facilities on the

premises without prior knowledge or consent of any individual who

may use or have custody of any such items or facilities, when it is

within the scope of their investigation.

5.12

The investigation team shall be responsible for ensuring that all

Investigation team

relevant evidence is collected and secured in accordance with legal

requirements.

5.13

Where an external investigator is contracted, a letter of engagement

Fraud Complaint

shall be provided detailing the investigator’s powers and obligations.

Manager

5.14

If surveillance is proposed to be undertaken, advice shall be obtained

Fraud Complaint

from the Police or Council’s solicitors.

Manager

5.15

Legal advice will be sought where appropriate to determine the

Fraud Complaint

strength of the evidence obtained.

Manager

5.16

At any time during the investigation, the Chief Executive in

Chief Executive,

consultation with the People & Capability Manager may, when of the

People &

opinion that an employee may have been guilty of a serious

Capability Manager

misconduct, suspend an employee from work in accordance with

Council's Collective and Individual Employment Agreements.

Suspension is appropriate where there is a risk that evidence may be

tampered with or coercion of witnesses may occur.

5.17

When sufficient evidence of criminal activity has been obtained, a

Fraud Complaint

complaint against the individual/s involved will be laid before the

Manager

Police, Serious Fraud Office or other appropriate law enforcement

agency. The Council will continue to investigate any misconduct as

appropriate.

5.18

The fraud file notes must clearly state whether the information has

Fraud Complaint

been provided to a law enforcement agency and, if not, the reasons

Manager

for the decision.

5.19

At any stage of an investigation into a staff or elected member, if the

Human Resource

Fraud Complaint Manager or investigation team considers there may

Manager,

have been misconduct involved, the matter will be pursued under the

Chief Executive,

employee Misconduct and Disciplinary Policy or the Elected

Audit and Risk

Members Code of Conduct as appropriate. Information obtained from

Committee

the investigation into a possible criminal offence may be used for the

investigation into misconduct.

5.20

The Fraud Complaint Manager will advise the complainant of the

Fraud Complaint

Doc set:

8

outcome of the investigation, unless the complaint was anonymous.

Manager

5.21

The Mayor and Audit and Risk Committee will be advised of the

Chief Executive

outcome of any investigation.

5.22

Post-investigation assessments will be carried by the Fraud

Fraud Complaint

Complaint Manager in coordination with relevant managers to identify

Manager

and rectify any weaknesses of fraud controls and to update the Fraud

Control Plan as appropriate.

Investigation Process

Cost recovery

Evidence provided

Crime

to appropriate

enforcement agency

Yes

Investigation under

Preliminary

Misconduct and

Complaint

verification of facts

Investigation

Staff

Disciplinary Policy

received and

Investigation

Sufficient

and legal advice by

Team

relevant parties

Conducted

evidence?

Complainant

Investigation

Established

notified

Who?

advised of

Coordinator/s

Misconduct

outcome

Investigation under

Elected Members

No

Elected

Code of Conduct

Elected

Member

Policy

Member

6

Disciplinary and remedial actions

6.1

Where a criminal investigation has been carried out and information

provided to a law enforcement agency, any criminal action shall be

determined by that agency.

6.2

Where any misconduct or fraud has resulted in a loss of public funds

Chief Executive,

or resources, the Council will attempt to recover such loss from the

perpetrator whenever possible and practicable. Any penalty arising

from a law enforcement agency’s investigation will not preclude the

Council from seeking to recover any loss arising from the fraud from

the perpetrator.

6.3

Where recovery from the responsible party is not possible, recovery

Legal, Audit and

from Council’s insurers wil be sought.

Risk Manager

6.4

The Council shall cease doing business with and terminate any

Chief Executive,

contractual arrangement with any consultant, contractor, vendor or

Legal, Audit and

other party found to have attempted to defraud the Council unless

Risk Manager

there are compelling reasons not to do so. Any such reasons shall

be recorded in the Fraud Investigation File and reported to the Audit

and Risk Committee.

Doc set:

9

7

External Communications

7

External Communications

7.1

The Fraud Complaint Manager shall notify the fraud, or suspected

Fraud Complaint

fraud, to Council’s external auditors and insurers.

Manager

7.2

With the approval of the Fraud Complaint Manager and the Chief

Chief Executive

Executive, all statements to the media or public regarding fraud shall

be made by the Communications Manager or Chief Executive.

Measurement and review

Measurement of the effectiveness of this policy will be undertaken through analysis of fraud

complaints. This policy will be reviewed every three years.

Definitions

Corrupt practice

The intentional offering, giving or soliciting, directly or indirectly, of

anything of value to influence improperly the actions of another party.

The purpose of corruption is generally for personal gain (not always

financial) by the individual.

Due diligence

The undertaking of reasonable verifications and precautions to identify

or prevent foreseeable risks.

External Advisor

The independent member appointed to the Council's Audit and Risk

Committee.

Fraud

Fraud is an intentional act by one or more individuals among

management, those charged with governance, employees or third

parties, involving the use of caption to obtain an unjust or illegal

advantage for themselves or any other person, or to evade a liability to

the Council.

Fraud is not restricted to monetary or material benefits. It includes

intangibles such as status and information.

Examples of fraud covered by this policy include, but are not limited to,

the following:

• Theft, including cash, consumables and intangible assets;

• Forgery or alteration of a cheque, bank draft, financial or any other

document;

• Misappropriation of funds, securities, supplies, or other assets or

abuse of Council facilities for personal usage;

• Impropriety in handling the reporting of money or financial

transactions;

• Intentional misstatement of financial information or other reporting

of Council performance;

• Claiming pay or reimbursement of expenses not incurred for

legitimate Council purposes;

• Profiteering as a result of insider knowledge of Council activities;

• Disclosing confidential and proprietary information to outside

parties;

• Accepting or seeking anything of material value from contractors,

vendors or persons providing services, goods or materials to

Council;

Doc set:

10

• Using a false identity to obtain some benefit;

• Employing acts of bribery, corruption or coercion to benefit oneself;

• Unauthorised destruction, removal or inappropriate use of records,

information systems, furniture, fixtures, and equipment.

Corruption

means the lack of integrity or honesty (especially susceptibility to

bribery) or the use of a position of trust for dishonest gain. It includes

foreign and domestic bribery, coercion, destruction, removal or

inappropriate use or disclosure of records, data, materials, intellectual

property or assets, or any similar or related inappropriate conduct.

Within this definition, corrupt conduct includes but is not limited to:

• any person who has a business involvement with Council,

improperly using, or trying to improperly use, the knowledge,

power or resources of their position for personal gain or the

advantage of others, for example, fabrication of business travel

requirements to satisfy personal situations,

• knowingly providing, assisting or validating in providing false,

misleading, incomplete or fictitious information to circumvent

Council procurement processes and procedures to avoid further

scrutiny or reporting,

• disclosing private, confidential or proprietary information to outside

parties without implied or expressed consent, and

• accepting or seeking anything of material value from contractors,

vendors, or persons providing services or materials to Council (see

Council’s Sensitive Expenditure Policy).

Misconduct

Refers to any misconduct or serious misconduct as defined in the

Council's Misconduct and Disciplinary Policy.

Sensitive Positon

Position held involving handling of stock, assets, money, information,

financial or treasury functions and/or influence over significant

decisions.

Doc set:

11