SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

southern rail tourism

passenger services

phase two: summary business

model analysis findings

confidential

june 2019

prepared for the canterbury mayoral forum

visitor solutions ltd and traction room ltd

IMAGE BY VEERASAK PIYAWATANAKUL

1

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

CONTENTS.

Executive Summary

4

1.0

Introduction

7

Project Brief and Methodology

2.0

Analysis

8

2.1

Model Assumptions

2.1a Operational Assumptions

2.1b Market Assumptions

2.2

Financial Model

2.2.1 Revenue

2.2.2 Costs - OPEX

2.2.3 Costs - CAPEX

2.2.4 Outputs

3.0

Risks and Mitigation

15

4.0

Opportunities

17

5.0

Conclusion and Recommendations

18

6.0

Appendix

19

Disclaimer:

Information, data and general assumptions used in the compilation of this report have been obtained from

sources believed to be reliable. Visitor Solutions Ltd and Traction Room Ltd have used this information in good

faith and makes no warranties or representations, express or implied, concerning the accuracy or completeness

of this information. Visitor Solutions Ltd and Traction Room Ltd are acting as independent consultants. In doing

so, the recommendations provided do not necessarily reflect the intentions of the Client. Interested parties

should perform their own investigations, analysis and projections on all issues prior to acting in any way with

regard to this project.

© Visitor Solutions 2018.

visitor solutions ltd and traction room ltd

2

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

IMAGE FROM SEETHESOUTHISLAND.COM

visitor solutions ltd and traction room ltd

3

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

EXECUTIVE

SUMMARY.

As part of the Canterbury Economic Development Strategy (CREDS) programme, the Canterbury

Mayoral Forum has requested a review of the potential for periodic rail passenger charter services,

or a regular service offering on the Main South Line [MSL] between Christchurch and Invercargill.

KiwiRail has indicated that they have no intention of running this service unless there is evidence

to support a commercial proposition. The purpose of this project is to complete an indicative

business justification case to determine whether there is potential and what the opportunity could

be. The project was staged in two phases, the first of which is now complete. The methodology

used to undertake the first phase of the project included a review of all available secondary data,

site visits, interviews and analysis.

Initial research led to the project brief being refined to focus on catering for tourism services

between Christchurch and Dunedin. Regular public passenger services were excluded on the

grounds of competitiveness against other transport modes, while the Dunedin to Invercargill

route was less desirable for operational and consumer demand reasons1. The first phase of the

study concluded:

1. The concept of a South Canterbury tourist rail experience looked promising from a technical,

operational and market demand perspective,

2. Dunedin Rail is a natural partner that brings significant benefits to the testing and potential

implementation of the concept. Dunedin Rail is likely to be central to the concept’s feasibility.

3. Timaru and Oamaru would potentially be the two main rail stops on route between

Christchurch and Dunedin (with Timaru being the simplest option),

4. The ‘loop’ approach to the concept potentially brings many other industry players into

consideration (which could assist higher visitation on the Christchurch to Dunedin rail leg).

5. Implementation is likely to be dependent on the use of a Silver Fern Railcar, either RM30 or

RM18 (both owned by KiwiRail). RM18 would need to be made operational.

6. Critically KiwiRail could facilitate or terminate the concept given its central role in any

development.

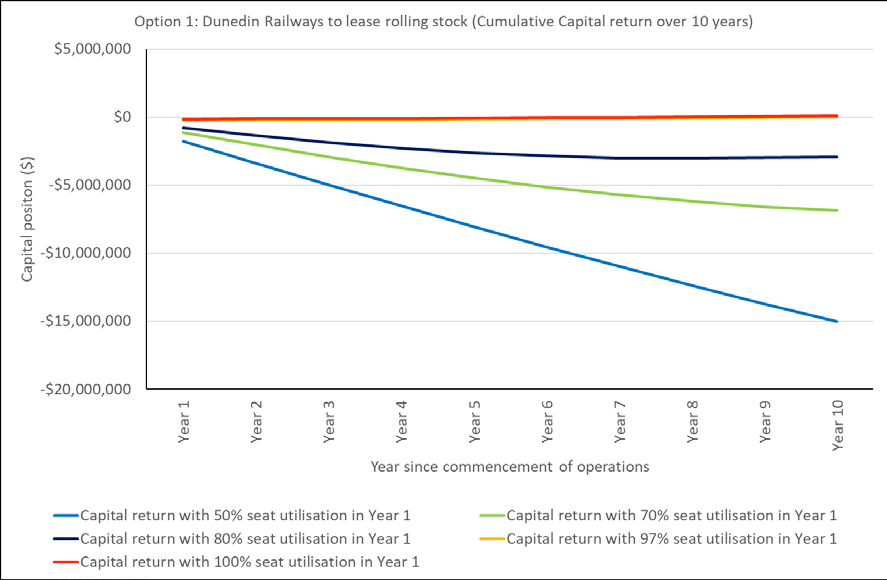

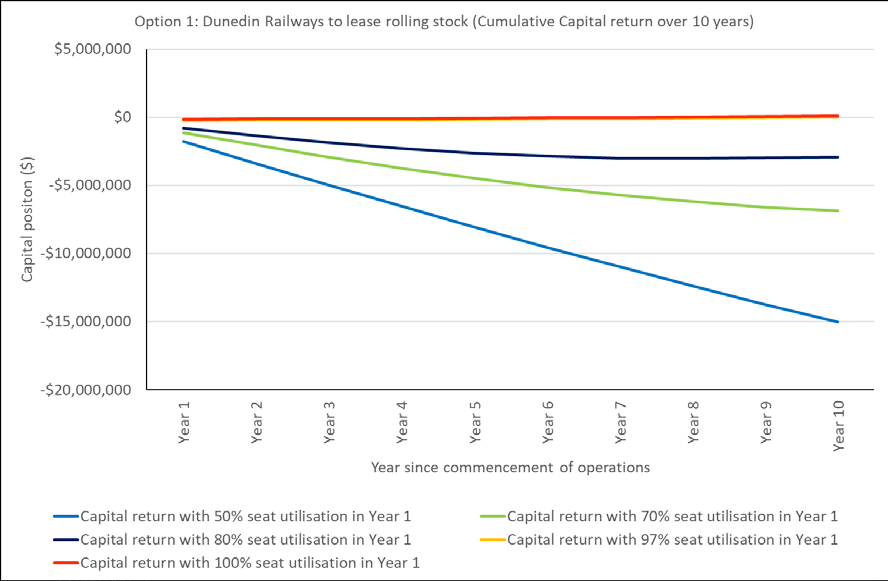

The second phase of the study, the preliminary financial analysis tested the proposition of using

the Silver Fern Rail car for the service. The modelling concluded that the operation of a Silver Fern

railcar service between Christchurch and Dunedin (with a stop in Timaru) was not operationally

viable. The financial model indicates that the rail car does not have enough capacity (at the

required ticket price) to be a viable proposition. In the unlikely scenario that 100% seat utilisation

is achieved, the cumulative capital return over a 10 year period is calculated to be $110k, however

based on the level of assumptions required for the development of the model it cannot be

considered to report to this level of accuracy. The cumulative capital return can therefore be

treated as zero. A more realistic 70% seat utilisation presents a cumulative capital return loss of

circa $7m over the same 10 year period. In summary, a nearly 100% seat utilisation is required for

the service offering to break even using the Silver Fern Rail Car.

IMAGE FROM GREAT JOURNEYS OF NZ WEBSITE

1. A Dunedin to Invercargill route could be explored at a later stage if required.

visitor solutions ltd and traction room ltd

4

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

During the study it also became apparent that Kiwirail had alternative plans (potentially in the

short term) for the railcar that it was leasing to Dunedin Railways. This highlights the difficulty of

establishing a service without Kiwirail being a core partner.

Should the potential service be able to utilise engines (and carriages) other than the Silver

fern rail car the financial model is likely to change for the better. Costs would be unlikely to

increase significantly while capacity could be improved substantially, thus improving profitability.

Achieving this would be dependant entirely on Kiwirail, given its control over so much of the

required infrastructure.

The potential benefit of such a route for Kiwirail would be in facilitating the tourist loops outlined

in the first phase of this study. These loops could assist patronage on Kiwirail’s existing services,

while also unlocking potential new revenue streams from partner organisations.

Dunedin Railways also has the potential to be a partner in some form in the future (even without

utilisation of the Silver Fern railcar).

Based on the findings of the financial analysis it is recommended that:

1. Advancing any further investigation into a Christchurch to Dunedin rail service using a Silver

Fern railcar should be ceased.

2. Dunedin Railways should be thanked for their assistance in the study and be informed of its

findings. An indication of Dunedin Railways future interest in any new partnering opportunities

should be tested.

3. Kiwirail should be approached and the information from this study shared to determine if

they are interested in exploring potential partnering opportunities for the rail route.

4. If Kiwirail is interested, focus should be placed on:

•

Options that increase service capacity above that of a Silver Fern rail car,

•

Options that enable the development of the South Island tourist loops outlined in Phase

One of the study.

5. Should the concept be advanced to the next stage with Kiwirail, a full market analysis and

business case should be completed.

visitor solutions ltd and traction room ltd

5

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

IMAGE BY PIXA BAY

visitor solutions ltd and traction room ltd

6

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

1. INTRODUCTION.

PROJECT BRIEF AND METHODOLOGY

As part of the Canterbury Economic Development Strategy (CREDS) programme, the Canterbury

Mayoral Forum has requested a review of the potential for periodic rail passenger charter services,

or a regular service offering on the Main South Line [MSL] between Christchurch and Invercargill.

KiwiRail has indicated that they have no intention of running this service unless there is evidence

to support a commercial proposition. The purpose of this project is to complete an indicative

business justification case to determine whether there is potential and what that opportunity

could be. The project was staged in two phases, the first of which is now complete. The

methodology used to undertake the first phase of the project included a review of all available

secondary data, site visits, interviews and analysis.

Initial research led to the project brief being refined to focus on catering for tourism services

between Christchurch and Dunedin. Regular public passenger services were excluded on the

grounds of competitiveness against other transport modes, while the Dunedin to Invercargill

route was less desirable for operational and consumer demand reasons2. The first phase of the

study concluded:

1. The concept of a South Canterbury tourist rail experience looked promising from a technical,

operational and market demand perspective,

2. Dunedin Rail is a natural partner that brings significant benefits to the testing and potential

implementation of the concept. Dunedin Rail is likely to be central to the concept’s feasibility.

3. Timaru and Oamaru would potentially be the two main rail stops on route between

Christchurch and Dunedin (with Timaru being the simplest option),

4. The ‘loop’ approach to the concept potentially brings many other industry players into

consideration (which could assist higher visitation on the Christchurch to Dunedin rail leg).

5. Implementation is likely to be dependent on the use of a Silver Fern Railcar, either RM30 or

RM18 (both owned by KiwiRail). RM18 would need to be made operational.

6. Critically KiwiRail could facilitate or terminate the concept given its central role in any

development.

The second phase of the study, the preliminary financial analysis is outlined in this section and

tests the proposition of using the Silver Fern Rail car for the service. The key findings from the

analysis are set out in summary form together with an Appendix containing additional detail.

IMAGE FROM GREAT JOURNEYS OF NZ WEBSITE

2. A Dunedin to Invercargill route could be explored at a later stage if required.

visitor solutions ltd and traction room ltd

7

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

2. ANALYSIS.

2.1 MODEL ASSUMPTIONS

a. Operational Assumptions

The cost model for the proposed service offering has been developed based on several high-level

assumptions regarding the operation of the service:

•

Dunedin Railways will operate the service using the Silver Fern rail car, currently on lease from

Kiwirail.

•

It is noted that Kiwirail have given notice to Dunedin Railways of their intention to take back

the rail car for purposes unknown. It is assumed that the rail car will again be made available

by Kiwirail to Dunedin Railways, either for purchase or for long term lease. The assumed costs

for lease of the rail car are $50,000 per year, whereas it is assumed that it would cost circa

$500,000 to purchase outright.

•

The service can be operated under Dunedin Railway’s existing Rail Safety Case.

•

Owing to constraints around journey times and availability of platform space at Christchurch

Station, the service would not be able to operate a same day return service. Therefore, the

return journey between Christchurch and Dunedin would have to incorporate an overnight

stop.

•

Any refurbishments to Timaru Station required to bring it up to a standard that is appropriate

will be borne by a combination of the local authority and the stations private owner, not

Dunedin Railways. These costs have therefore been excluded.

•

Where possible all other operational assumptions outlined in the model have been tested

using multiple data sources. However, these figures remain estimates.

b. Market Assumptions

For the purpose of developing the cost model for the proposed service, a range of assumptions

have been made regarding market conditions and levels of patronage for the service:

•

The service will operate three return journeys per week between Dunedin and Christchurch

and will operate for 52 weeks per year.

•

The maximum number of passengers that can be accommodated on the Silver Fern rail car

is 96.

•

The average one-way ticket price upon commencement of the service will be $100. This is

comparable with similar scenic services (Coastal Pacific and Tranz- Alpine), making allowance

for different fare types (starter, flexi etc).

•

Passengers’ on board spending in Year 1 is assumed to be an average of $10.

•

Activities would be offered to passengers when stopped in Timaru (estimated stop over is

between 1 – 2 hours). Concessions paid to Dunedin Rail from these activities have been

excluded from modelling at this preliminary stage.

•

Ticket prices and the value of on-board purchases will be subject to annual price inflation of

1.9% in line with recent market observations.

•

Annual demand growth of 3% will be observed.

2.2 FINANCIAL MODEL

The financial model for the proposed service offering has been developed based on a number

of revenue scenarios, dependent on seat utilisation, and estimated operational and capital

expenditure involved in delivering the service. The outputs of the model are, for each revenue

scenario:

•

Annual operating profit or loss for the first ten years of operation.

•

Annual “Farebox” for the first ten years of operation. The farebox model is used for transit

systems worldwide to measure the proportion of operating and capital expenditure that is

covered by revenue from ticket sales. A farebox of 100% is where the operation is cash neutral,

less than this would be an operating loss, greater than this would be an operating profit.

•

Overall capital return over a 10-year period i.e. the value of establishment costs recovered

from fare revenue.

The model has been developed for scenarios where Dunedin Railways would both lease and

purchase the rolling stock from Kiwirail. In interpreting the results, it became apparent that the

visitor solutions ltd and traction room ltd

8

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

lease model was more financially sustainable, both in terms of delivering improved returns to

Dunedin Railways, but also in terms of mitigating the risk of a large capital outlay on an ageing

asset (the railcars are approximately 50 years old). Furthermore, during informal discussions with

Dunedin Railways during the preparation of the model, they suggested that they did not have

much appetite for purchasing the rail car outright. For this reason, only the results for the option

of leasing the rail car are presented in the body of this report. The full analysis for both options is

however included in Appendix A.

2.2.1 Revenue

As discussed above, the revenue has been calculated based upon an average one-way ticket price

of $100 in the first year of operations, with an average on board spend of $10 per passenger. Ticket

prices and on-board revenue are assumed to be subject to market inflation of 1.9% per year. It is

assumed that patronage will grow by 3% per year, up to the maximum capacity of the rail car.

The revenue has been assessed for seat utilisation values of 50%, 70%, 80%, 97% and 100%. The

97% was analysed as it was found that that was the minimum level of patronage required to

break even after 10 years.

The revenue calculations for different seat utilisation values can be seen in Table 2.1 below:

Table 2.1: Estimated revenue for 10 years of operations.

Y 1

Y 2

Y 3

Y 4

Y 5

Y 6

Y 7

Y 8

Y 9

Y 10

Ticket price +

$100

$102

$104

$106

$108

$110

$113

$115

$117

$120

2% inflation

On board

$10

$10

$10

$11

$11

$11

$11

$11

$12

$12

spending per

person plus

2% inflation

Revenue with $1.65m $1.74m $1.83m $1.93m $2.02m $2.13m $2.23m $2.34m $2.46m $2.59m

50% seat

utilisation in

Year 1

Revenue with $2.31m $2.42m $2.54m $2.67m $2.81m $2.95m $3.10m $3.26m $3.43m $3.60m

70% seat

utilisation in

Year 1

Revenue with $2.64m $2.77m $2.91m $3.06m $3.21m $3.38m $3.54m $3.73m $3.86m $3.94m

80% seat

utilisation in

Year 1

Revenue with $3.20m $3.36m $3.43m $3.50m $3.57m $3.64m $3.71m $3.78m $3.86m $3.94m

97% seat

utilisation in

Year 1

Revenue with $3.29m $3.36m $3.43m $3.50m $3.57m $3.64m $3.71m $3.78m $3.86m $3.94m

100% seat

utilisation in

Year 1

visitor solutions ltd and traction room ltd

9

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

2.2.2 Costs - OPEX

The operating costs of the proposed service offering have been derived based upon ‘cost per trip’

figures obtained through informal liaisons with Dunedin Railways, regarding their existing charter

services between Dunedin and Rolleston. These figures have been increased on a pro rata basis

to allow for the final 20km (circa) leg between Rolleston and Christchurch. The figure used for the

model was $17,920 per return journey. This includes:

•

running rights,

•

on board staffing,

•

routine maintenance and refuelling, and

•

An additional $200 and $650 have been allowed for staffing of Christchurch Station and

overnight accommodation for train crews in Christchurch.

An annual cost of $50,000 has been allowed for lease of the rolling stock required to operate the

service. This value would have to be verified by further negotiations with Kiwirail for continued use

of the Silver Fern Rail Car, if these vehicles were offered back to Dunedin Railways in the future

and if the proposal was to be advanced.

Further operational expenditure allowed for includes:

•

travel agents’ commission,

•

marketing,

•

ticketing,

•

insurance,

•

industry memberships,

•

re-training of train drivers, and

•

loss of revenue due to service disruptions.

The operational expenditure allowed for is summarised in Table 2.2 below. It should be noted that

these are Year 1 figures and with the exception of the lease of rolling stock, are subject to 1.9%

annual inflation.

Table 2.2: Estimated Annual OPEX in Year 1

Lease of rolling stock

$50k

Running costs - based on Dunedin Charter Rates (per return

$18k ($2.8m per year)

journey)

Christchurch Station staffing costs (per return journey)

$200 ($31k per year)

Dunedin Railways overnight staff costs (per return journey)

$650 ($100k per year)

Travel agents commission (Assume 25/75 split between agents

$115k

and booking direct. Agent commission is 20%. Assume 5% of

ticket revenue)

Marketing Budget

$100k

Ticketing (use existing Dunedin Railways forum)

$20k

Insurance

$20k

Industry memberships

$10k

Loss of revenue due to service unavailability due to unplanned/

$45k

planned outage - allow 2 weeks per year

Re-training/replacement of train drivers

$7k every three years

total opeX in year 1

$3.29m

Note: * Assumes that the operation is leveraging off Dunedin Rails existing advertising / marketing

operations.

visitor solutions ltd and traction room ltd

10

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

2.2.3 Costs - CAPEX

The capital cost associated with establishment of the proposed service have been estimated

based on industry experience.

The largest capital outlay required, if the decision was taken to purchase rather than lease the

rail car(s), would be procurement of rolling stock. A value of circa $500,000 has been assumed for

this cost (which is only used in the models in the Appendix A). This would have to be verified by

further discussion and negotiation with Kiwirail, should the option be pursued further.

The remaining capital expenditure is summarised in Table 3 below:

Table 3: Estimated CAPEX to establish the service

Refurbishment of Timaru Station - to be funded by local

$0

council/private owner

Agreement of interface with other network operations

$50,000

Set up of access rights (from Kiwirail)

$10,000

Modifications to Dunedin Railways ticketing forums

$20,000

Advertising, PR campaigns, travel expos

$50,000

Training of existing train drivers to operate Rolleston to

$4,800

Christchurch

Training of additional train drivers, $6,900 each driver. Assume

$13,800

two additional drivers required.

Total Establishment Cost

$148,600

Note: * Assumes that the operation is leveraging off Dunedin Rails existing advertising / marketing

operations.

The model has been developed on the assumption that Dunedin Railways (and / or partners)

hold sufficient cash to fund the establishment costs detailed above without requiring financing

(Note: This is an area for further discussion regarding investment from other parties such as the

Southern Regional Mayoral forum and the Regional Growth Fund).

The option of purchasing rolling stock has been analysed on the assumption that it would be

financed at an interest rate of 10% over a 10-year term. This would equate to repayments of

$80,000 per year over the life of the term (this option is only shown in Appendix A).

IMAGE BY JAMES WHEELER

visitor solutions ltd and traction room ltd

11

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

Table 3: Estimated CAPEX to establish the service

Due to restricted capacity with the Silver Fern rail car, high seat utilisation is required almost

immediately for the service to be profitable in the long term.

Even with relatively high seat utilisation, the service will still operate at a loss every year. Over time,

the cumulative loss will increase, meaning that without significant financial subsidy, the service

will not be financially sustainable.

The full financial model is attached to this report as Appendix A.

IMAGE BY VEERASAK PIYAWATANAKUL

visitor solutions ltd and traction room ltd

12

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

2.2.4 Outputs

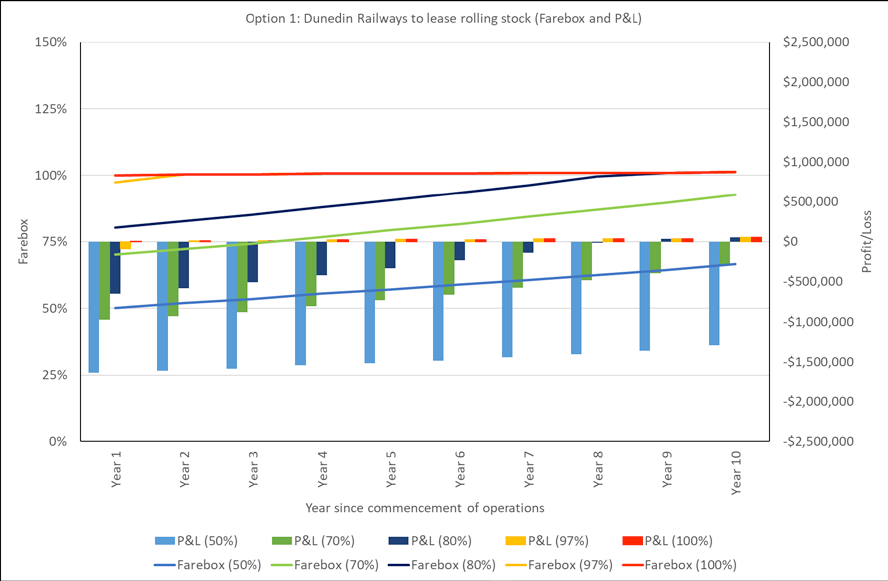

Figure 2.1, below, shows the annual operating profit and farebox for the revenue scenarios

analysed (the lease option):

Figure 2.1: Annual farebox and operating profit over 10 years

For the service to operate at a profit, seat utilisation needs to be almost 100% (the seat utilisation

at which break even occurs, considering the assumptions that have been made is 97%). The

profitability of the proposed service is constrained by the seat capacity of the Silver Fern rail car,

as can be seen by the fact that at 100% utilisation, the farebox is only just over 100%. (Note: this

would be an area for discussion with KiwiRail, as the provision of higher capacity carriages could

be considered at relatively little increase in assumed operating costs).

It is considered unlikely that 100% seat utilisation would be achievable, particularly at the

commencement of operations. Low seat utilisation would result in considerable operating losses

being incurred. For 50% seat utilisation, these losses would amount to approximately $1.2m per

year. This is a significant risk to the proposed operation.

Figure 2.2, below, shows the cumulative capital returns over 10 years of operations for the revenue

scenarios analysed:

visitor solutions ltd and traction room ltd

13

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

IMAGE BY RHONDA ALBOM

visitor solutions ltd and traction room ltd

14

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

3. RISKS AND

MITIGATION.

Given that there are a number of key assumptions behind the development of the cost model,

there are a series of risks that also apply, as outlined in Table 3.1 below:

Table 3.1: Risks associated with the proposed service offering

RISK

DESCRIPTION

MITIGATION OPTIONS

LIKELIHOOD & SEVERITY

Fare pricing

The one-way ticket

Benchmark against other

The proposed fare has been

price of $100 is not

tourist services operated in reviewed against similar tourist

compatible with market

New Zealand. Undertake

services and it is therefore

expectation and will result further market research

considered a low risk that it is

in significantly reduced

to determine predicted

over-priced. The consequences

patronage and therefore,

demand at that price.

of low patronage will be that

reduced revenue.

the operation would run at a

significant loss i.e. greater than

$1m per year.

Price inflation

Market inflation may

Secure long-term

The New Zealand economy has

exceed the assumed rate

contracts with suppliers

not experienced high levels of

of 1.9% which could make that limit levels of price

inflation in recent times and

it difficult to maintain

inflation per annum.

there is no reason to expect this

competitive ticket prices

to change. If the risk was to be

and recover operating

realised, either by keeping fares

costs.

low, or increasing fares and risking

low patronage, the service would

operate at a significant loss.

Over-estimated

Risk of patronage levels

Undertake further market The feasibility of the service

patronage levels

being over estimated.

research to determine

offering is dependent on

To break-even over a 10

predicted demand at that patronage levels – if only 50% seat

year period would require price.

utilisation was achieved in Year 1

29,100 one-way journeys

(15,000 one-way journeys), then

in Year 1, equating to a

after 10 years there would be a

high seat utilisation of

cash shortfall of $15m.

97% for the Silver Fern rail

car.

Seasonal variation It is expected that

Consider operating a

The analysis undertaken is based

in patronage levels patronage levels would be reduced timetable during on a year round service and

reduced during the low

the off season. Undertake

showed near full seat utilisation

season, however the cost

further market research

would be required for the service

of operation the service

to determine predicted

to be profitable. If the low season

would remain the same.

demand.

was to equate to 4 months, and

Hold sufficient levels of

patronage levels were to drop to

cash in reserve to operate 50%, this would equate to a drop

during the off season.

in revenue of circa $500k.

Directional

It is expected that

Offer reduced pricing for

If seat utilisation is dramatically

variation in

demand will be

the Dunedin commencing reduced for northbound services,

patronage levels

considerably greater

service to encourage

there would be a significant

for the Christchurch

return trips. Pump the

loss of revenue. If average seat

commencing service and northern leg (e.g. Offer

utilisation northbound was only

lower for the Dunedin

trips from Christchurch

50%, instead of 100%, this would

commencing service.

to fly to Dunedin and

equate to 25% shortfall (circa

Therefore, whilst it could

make the return journey

$800k per annum) from the

be forecast that demand

by train. Or promote a

revenue required for the service to

visitor solutions ltd and traction room ltd

15

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

will grow to achieve

Queenstown to Dunedin

be profitable.

seat utilisation for the

leg that returns to

southbound journey, this

Christchurch via rail).

may be more difficult to

achieve for both service

offerings.

On board

Levels of on-board

Benchmark against prices The level of on board spending

spending

spending per person is

offered on competing

of $10 per person is relatively

over estimated resulting in services. Consider

modest in light of the length of

reduced revenue.

including on board

the journey.

spending in ticket price.

At full capacity, the assumed

on board spending equates to

revenue of circa $300k per year.

This is approximately 10% of total

revenue, therefore would leave a

significant shortfall.

Maintenance

The Silver Fern rail car is

Lease more than one unit, The high levels of maintenance

requirements for

48 years old and is likely

providing redundancy in

could result in increased

rolling stock

to require a high level of

the service offering for

operational expenditure. It

ongoing maintenance.

maintenance activities.

should be noted that during

informal consultation with

Try to negotiate with

Dunedin Railways as part of

Kiwirail that leasing

this exercise, reservations were

charges are only paid for

expressed regarding the feasibility

day when the rail car is

of operating the service at the

operating.

proposed frequency using the

Silver Fern rail car (due to age of

the rail car).

Unforeseen service In the event of unforeseen Negotiate running rights

It is highly likely that at some

disruption

events that result in the

with Kiwirail that entitle

stage, there will be service

service not being able to

Dunedin Railways to

disruption.

operate, there would be

compensation should

lost revenue due to the

the rail network not be

The rail network is subject to

service not operating,

available.

operating restrictions in the event

in addition to the cost

Financial projections to

of extreme weather, which is

of providing alternative

allow for some loss of

inevitable in the region.

transport. This could be

revenue.

the result of unavailability Maintain the fleet of

For each trip that would be unable

of rolling stock or

rolling stock to a high

to operate, it would cost $9,600 in

unplanned maintenance

level.

lost fare revenue, based on Year

of the railway line. Such

1 ticket prices and 100% seat

an event could also be

utilization.

the result of events such

as extreme weather or

seismic activity.

Loss of the Silver

Kiwirail makes the Silver

Seek and alternative

The services would cease until an

fern rail car

fern rail car unavailable.

engine and carriages. This alternative engine and carriages

would require significant

were available. However, an

support from Kiwirail.

alternative configuration to the

Silver fern rail car is likely to be

more financially viable.

visitor solutions ltd and traction room ltd

16

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

4. OPPORTUNITIES.

The cost model only accounts for direct revenue from the sale of tickets and on-board purchases,

set against the operational and capital expenditure involved in establishing and operating the

service. It indicates that a high level of seat utilisation is required for the proposed service to be

financially sustainable as a standalone operation. However, the proposed service provides the

opportunity to open additional revenue streams that cannot be quantified by the cost model

alone. These opportunities include:

•

General increase in tourist numbers being delivered to destinations and stops in question.

•

Selling tickets as part of a wider rail package including Kiwirail tourist services, the Interislander

Ferry or Dunedin Railways other tourist services. There is the opportunity to partner with

Kiwirail in offering the route as part of the nationwide tourist services. This would offer

greater opportunities to cross sell the service with the other experiences operated by Kiwirail.

Furthermore, Kiwirail would be able to operate using modern rolling stock used elsewhere

on their tourist routes, specifically designed for tourist services. This would provide greater

capacity than the Silver Fern and potentially offer greater profitability.

•

Selling tickets as part of a rail/air combination in partnership with an airline, including airport

transfers. This may be of value as it would facilitate offering the service as a same day return.

Currently, only Air New Zealand operates flights between Christchurch and Dunedin, which

includes evening flights. This same approach could be expanded to bus, rental car, plane and

rail options that facilitate the South Island route loops outlined in phase one of this report.

•

Sell as part of a tourist loop, or selection of tourist loops, with set itineraries including car/

camper van hire and accommodation.

•

Selling tour packages including side trips destinations. Side trips offered may include:

•

Christchurch:

•

Banks Peninsula

•

Kaikoura

•

Hanmer Springs

•

Mt Hutt – during ski season

•

Timaru

•

Tekapo

•

Aoraki/Mt Cook

•

Pleasant Point Museum and Railway

•

Dunedin

•

Road transfer to Queenstown/Wanaka

•

Otago Peninsula

•

Catlins Coast

•

Moeraki Boulders

•

Offer trip packages including accommodation, meals etc in Christchurch or Dunedin (and

other destinations along the route loops outlined in phase one of the study).

The wider regional benefits that are likely to be realised as a result seeking to unlock some or all

of these opportunities have the potential to be considerable.

visitor solutions ltd and traction room ltd

17

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

CONCLUSION +

5. RECOMMENDATIONS.

5.1 Conclusion

The financial modelling undertaken in this second phase of the project has concluded that

the operation of a Silver Fern railcar service between Christchurch and Dunedin (with a stop in

Timaru) is not operationally viable. The financial model indicates that the rail car does not have

enough capacity (at the required ticket price) to be a viable proposition.

During the study it also became apparent that Kiwirail had alternative plans (potentially in the

short term) for the railcar that it was leasing to Dunedin Railways. This highlights the difficulty of

establishing a service without Kiwirail being a core partner.

Should the potential service be able to utilise engines (and carriages) other than the Silver

Fern rail car the financial model is likely to change for the better. Costs would be unlikely to

increase significantly, while capacity could be improved substantially, thus improving profitability.

Achieving this would be dependant entirely on Kiwirail, given its control over so much of the

required infrastructure.

The potential benefit of such a route for Kiwirail would be in facilitating the tourist loops outlined

in the first phase of this study. These loops could assist patronage on Kiwirail’s existing services

while also unlocking potential new revenue streams from partner organisations.

Dunedin Railways also has the potential to be a partner in some form in the future (even without

utilisation of the Silver Fern railcar).

5.2 Recommendations

Based on the findings of the financial analysis it is recommended that:

1. Advancing any further investigation into a Christchurch to Dunedin rail service using a Silver

Fern railcar should be ceased.

2. Dunedin Railways should be thanked for their assistance in the study and be informed

of its findings. An indication of Dunedin Railway’s future interest in any new partnering

opportunities should be tested.

3. Kiwirail should be approached and the information from this study shared to determine if

they are interested in exploring potential partnering opportunities for the rail route.

4. If Kiwirail is interested, focus should be placed on:

•

Options that increase service capacity above that of a Silver fern rail car,

•

Options that enable the development of the South Island tourist loops outlined in Phase

One of the study.

5. Should the concept be advanced to the next stage with Kiwirail, a full market analysis and

business case should be completed.

visitor solutions ltd and traction room ltd

18

SOUTHERN RAIL TOURISM PASSENGER SERVICES

PHASE 2 SUMMARY BUSINESS MODEL ANALYSIS FINDINGS

CONFIDENTIAL

6. APPENDIX.

visitor solutions ltd and traction room ltd

19

INCOME

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

Ticket price + 2% inflation

$100

$102

$104

$106

$108

$110

$113

$115

$117

$120

On board spending per person plus 2% inflation

$10

$10

$10

$11

$11

$11

$11

$11

$12

$12

Patronage with 50% seat utilisation in Year 1

15,000

15,500

16,000

16,500

17,000

17,500

18,000

18,500

19,100

19,700

Patronage with 70% seat utilisation in Year 1

21,000

21,600

22,200

22,900

23,600

24,300

25,000

25,800

26,600

27,400

Patronage with 80% seat utilisation in Year 1

24,000

24,700

25,400

26,200

27,000

27,800

28,600

29,500

29,952

29,952

Patronage with 97% seat utilisation in Year 1

29,100

29,952

29,952

29,952

29,952

29,952

29,952

29,952

29,952

29,952

Patronage with 100% seat utilisation in Year 1

29,952

29,952

29,952

29,952

29,952

29,952

29,952

29,952

29,952

29,952

Revenue*** with 50% seat utilisation in Year 1

$1,650,000

$1,740,000

$1,830,000

$1,930,000

$2,020,000

$2,130,000

$2,230,000

$2,340,000

$2,460,000

$2,590,000

Revenue*** with 70% seat utilisation in Year 1

$2,310,000

$2,420,000

$2,540,000

$2,670,000

$2,810,000

$2,950,000

$3,100,000

$3,260,000

$3,430,000

$3,600,000

Revenue*** with 80% seat utilisation in Year 1

$2,640,000

$2,770,000

$2,910,000

$3,060,000

$3,210,000

$3,380,000

$3,540,000

$3,730,000

$3,860,000

$3,940,000

Revenue*** with 97% seat utilisation in Year 1

$3,200,000

$3,360,000

$3,430,000

$3,500,000

$3,570,000

$3,640,000

$3,710,000

$3,780,000

$3,860,000

$3,940,000

Revenue*** with 100% seat utilisation in Year 1

$3,290,000

$3,360,000

$3,430,000

$3,500,000

$3,570,000

$3,640,000

$3,710,000

$3,780,000

$3,860,000

$3,940,000

Seats per train*

96

Maximum passengers per year**

2

9,952

Assumed demand growth

3%

Assumed price inflation

2%

* Capacity based on use of Silver Fern rol ing stock unit

** Maximum passengers based on 3 x return trips per week, 52 weeks per year

TOTAL EXPENDITURE

Upfront Cost Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

Total OPEX (Option 1 - Lease Rol ing Stock)

$3,288,620

$3,350,154

$3,419,757

$3,476,751

$3,541,859

$3,615,105

$3,675,810

$3,744,701

$3,821,800

$3,886,433

Total CAPEX (Option 1 - Lease Rol ing Stock)

$148,600

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

Total OPEX (Option 2 - Buy Rol ing Stock)

$3,238,620

$3,300,154

$3,362,857

$3,426,751

$3,491,859

$3,558,205

$3,625,810

$3,694,701

$3,764,900

$3,836,433

Total CAPEX (Option 2 - Buy Rol ing Stock)

$148,600

$80,000

$80,000

$80,000

$80,000

$80,000

$80,000

$80,000

$80,000

$80,000

$80,000

OPEX

Year 1 Cost

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

Running costs - based on Dunedin Charter Rates (per return journey)

$17,920

$2,795,520

$2,848,635

$2,902,759

$2,957,911

$3,014,112

$3,071,380

$3,129,736

$3,189,201

$3,249,796

$3,311,542

Christchurch Station staffing costs (per return journey)

$200

$31,200

$31,793

$32,397

$33,012

$33,640

$34,279

$34,930

$35,594

$36,270

$36,959

Dunedin Railways overnight staff costs (per return journey)

$650

$101,400

$103,327

$105,290

$107,290

$109,329

$111,406

$113,523

$115,680

$117,878

$120,117

Travel agents commission (Assume 50/50 split between agents and booking direct. Agent commission is 10%. Assume 5%

of ticket revenue)

$115,500

$115,500

$117,695

$119,931

$122,209

$124,531

$126,897

$129,309

$131,765

$134,269

$136,820

Marketing Budget

$100,000

$100,000

$101,900

$103,836

$105,809

$107,819

$109,868

$111,955

$114,083

$116,250

$118,459

Ticketing (use existing Dunedin Railways Platform)

$20,000

$20,000

$20,380

$20,767

$21,162

$21,564

$21,974

$22,391

$22,817

$23,250

$23,692

Insurance

$20,000

$20,000

$20,380

$20,767

$21,162

$21,564

$21,974

$22,391

$22,817

$23,250

$23,692

Industry memberships

$10,000

$10,000

$10,190

$10,384

$10,581

$10,782

$10,987

$11,196

$11,408

$11,625

$11,846

Loss of revenue due to service unavailability due to unplanned/planned outage - al ow 2 weeks per year

$45,000

$45,000

$45,855

$46,726

$47,614

$48,519

$49,441

$50,380

$51,337

$52,313

$53,307

Re-training/replacement of Locomotive Engineers

$6,900

$6,900

$6,900

$6,900

CAPEX

Upfront cost Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

Refurbishment of Timaru Station - to be funded by local council

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

Agreement of interface with other network operations

$50,000

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

Set up of access rights (from Kiwirail)

$10,000

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

Modifications to Dunedin Railways ticketing forums

$20,000

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

Advertising, PR campaigns, travel expos

$50,000

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

Training of existing Locomotive Engineers, Rol eston to Christchurch

$4,800

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

Training of additional Locomotive Engineers, $6,900 each LE. Assume two.

$13,800

$0

$0

$0

$0

$0

$0

$0

$0

$0

$0

Rol ing Stock Costs

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

Lease of rol ing stock (OPEX) - $50,000 per year

$50,000

$50,000

$50,000

$50,000

$50,000

$50,000

$50,000

$50,000

$50,000

$50,000

Purchase of rol ing stock (CAPEX)

$80,000

$80,000

$80,000

$80,000

$80,000

$80,000

$80,000

$80,000

$80,000

$80,000

Option 1: Dunedin Railways Lease Rolling Stock

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

Farebox with 50% seat utilisation in Year 1

50%

52%

54%

56%

57%

59%

61%

62%

64%

67%

Farebox with 70% seat utilisation in Year 1

70%

72%

74%

77%

79%

82%

84%

87%

90%

93%

Farebox with 80% seat utilisation in Year 1

80%

83%

85%

88%

91%

93%

96%

100%

101%

101%

Farebox with 97% seat utilisation in Year 1

97%

100%

100%

101%

101%

101%

101%

101%

101%

101%

Farebox with 100% seat utilisation in Year 1

100%

100%

100%

101%

101%

101%

101%

101%

101%

101%

Operating profit with 50% seat utilisation in Year 1

-$1,638,620 -$1,610,154 -$1,589,757 -$1,546,751 -$1,521,859 -$1,485,105 -$1,445,810 -$1,404,701 -$1,361,800 -$1,296,433

Operating profit with 70% seat utilisation in Year 1

-$978,620

-$930,154

-$879,757

-$806,751

-$731,859

-$665,105

-$575,810

-$484,701

-$391,800

-$286,433

Operating profit with 80% seat utilisation in Year 1

-$648,620

-$580,154

-$509,757

-$416,751

-$331,859

-$235,105

-$135,810

-$14,701

$38,200

$53,567

Operating profit with 97% seat utilisation in Year 1

-$88,620

$9,846

$10,243

$23,249

$28,141

$24,895

$34,190

$35,299

$38,200

$53,567

Operating profit with 100% seat utilisation in Year 1

$1,380

$9,846

$10,243

$23,249

$28,141

$24,895

$34,190

$35,299

$38,200

$53,567

Capital return with 50% seat utilisation in Year 1

-$1,787,220 -$3,397,374 -$4,987,130 -$6,533,881 -$8,055,741 -$9,540,845 -$10,986,656 -$12,391,357 -$13,753,157 -$15,049,590

Capital return with 70% seat utilisation in Year 1

-$1,127,220 -$2,057,374 -$2,937,130 -$3,743,881 -$4,475,741 -$5,140,845 -$5,716,656 -$6,201,357 -$6,593,157 -$6,879,590

Capital return with 80% seat utilisation in Year 1

-$797,220 -$1,377,374 -$1,887,130 -$2,303,881 -$2,635,741 -$2,870,845 -$3,006,656 -$3,021,357 -$2,983,157 -$2,929,590

Capital return with 97% seat utilisation in Year 1

-$237,220

-$227,374

-$217,130

-$193,881

-$165,741

-$140,845

-$106,656

-$71,357

-$33,157

$20,410

Capital return with 100% seat utilisation in Year 1

-$147,220

-$137,374

-$127,130

-$103,881

-$75,741

-$50,845

-$16,656

$18,643

$56,843

$110,410

Option 2: Dunedin Railways Purchase Rolling Stock

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

Farebox with 50% seat utilisation in Year 1

50%

51%

53%

55%

57%

59%

60%

62%

64%

66%

Farebox with 70% seat utilisation in Year 1

70%

72%

74%

76%

79%

81%

84%

86%

89%

92%

Farebox with 80% seat utilisation in Year 1

80%

82%

85%

87%

90%

93%

96%

99%

100%

101%

Farebox with 97% seat utilisation in Year 1

96%

99%

100%

100%

100%

100%

100%

100%

100%

101%

Farebox with 100% seat utilisation in Year 1

99%

99%

100%

100%

100%

100%

100%

100%

100%

101%

Operating profit with 50% seat utilisation in Year 1

-$1,668,620 -$1,640,154 -$1,612,857 -$1,576,751 -$1,551,859 -$1,508,205 -$1,475,810 -$1,434,701 -$1,384,900 -$1,326,433

Operating profit with 70% seat utilisation in Year 1

-$1,008,620

-$960,154

-$902,857

-$836,751

-$761,859

-$688,205

-$605,810

-$514,701

-$414,900

-$316,433

Operating profit with 80% seat utilisation in Year 1

-$678,620

-$610,154

-$532,857

-$446,751

-$361,859

-$258,205

-$165,810

-$44,701

$15,100

$23,567

Operating profit with 97% seat utilisation in Year 1

-$118,620

-$20,154

-$12,857

-$6,751

-$1,859

$1,795

$4,190

$5,299

$15,100

$23,567

Operating profit with 100% seat utilisation in Year 1

-$28,620

-$20,154

-$12,857

-$6,751

-$1,859

$1,795

$4,190

$5,299

$15,100

$23,567

Capital return with 50% seat utilisation in Year 1

-$1,817,220 -$3,457,374 -$5,070,230 -$6,646,981 -$8,198,841 -$9,707,045 -$11,182,856 -$12,617,557 -$14,002,457 -$15,328,890

Capital return with 70% seat utilisation in Year 1

-$1,157,220 -$2,117,374 -$3,020,230 -$3,856,981 -$4,618,841 -$5,307,045 -$5,912,856 -$6,427,557 -$6,842,457 -$7,158,890

Capital return with 80% seat utilisation in Year 1

-$827,220 -$1,437,374 -$1,970,230 -$2,416,981 -$2,778,841 -$3,037,045 -$3,202,856 -$3,247,557 -$3,232,457 -$3,208,890

Capital return with 97% seat utilisation in Year 1

-$267,220

-$287,374

-$300,230

-$306,981

-$308,841

-$307,045

-$302,856

-$297,557

-$282,457

-$258,890

Capital return with 100% seat utilisation in Year 1

-$177,220

-$197,374

-$210,230

-$216,981

-$218,841

-$217,045

-$212,856

-$207,557

-$192,457

-$168,890

Option 1: Dunedin Railways to lease rol ing stock (Farebox and P&L)

150%

$2,500,000

$2,000,000

125%

$1,500,000

$1,000,000

100%

$500,000

75%

$0

-$500,000

Profit/Loss

Farebox

50%

-$1,000,000

-$1,500,000

25%

-$2,000,000

0%

-$2,500,000

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

Year since commencement of operations

P&L (50%)

P&L (70%)

P&L (80%)

P&L (97%)

P&L (100%)

Farebox (50%)

Farebox (70%)

Farebox (80%)

Farebox (97%)

Farebox (100%)

Option 2: Dunedin Railways to purchase rol ing stock (Farebox and P&L)

150%

$2,500,000

$2,000,000

125%

$1,500,000

$1,000,000

100%

$500,000

75%

$0

Profit/Loss

Farebox

-$500,000

50%

-$1,000,000

-$1,500,000

25%

-$2,000,000

0%

-$2,500,000

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

Year since commencement of operations

P&L (50%)

P&L (70%)

P&L (80%)

P&L (97%)

P&L (100%)

Farebox (50%)

Farebox (70%)

Farebox (80%)

Farebox (97%)

Farebox (100%)

Option 1: Dunedin Railways to lease rol ing stock (Cumulative Capital return over 10 years)

$5,000,000

$0

-$5,000,000

-$10,000,000

Capital positon ($)

-$15,000,000

-$20,000,000

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

Year since commencement of operations

Capital return with 50% seat utilisation in Year 1

Capital return with 70% seat utilisation in Year 1

Capital return with 80% seat utilisation in Year 1

Capital return with 97% seat utilisation in Year 1

Capital return with 100% seat utilisation in Year 1

Option 2: Dunedin Railways to purchase rol ing stock (Cumulative Capital return over 10 years)

$5,000,000

$0

-$5,000,000

Capital positon ($) -$10,000,000

-$15,000,000

-$20,000,000

Year 1

Year 2

Year 3

Year 4

Year 5

Year 6

Year 7

Year 8

Year 9

Year 10

Year since commencement of operations

Capital return with 50% seat utilisation in Year 1

Capital return with 70% seat utilisation in Year 1

Capital return with 80% seat utilisation in Year 1

Capital return with 100% seat utilisation in Year 1

Capital return with 97% seat utilisation in Year 1