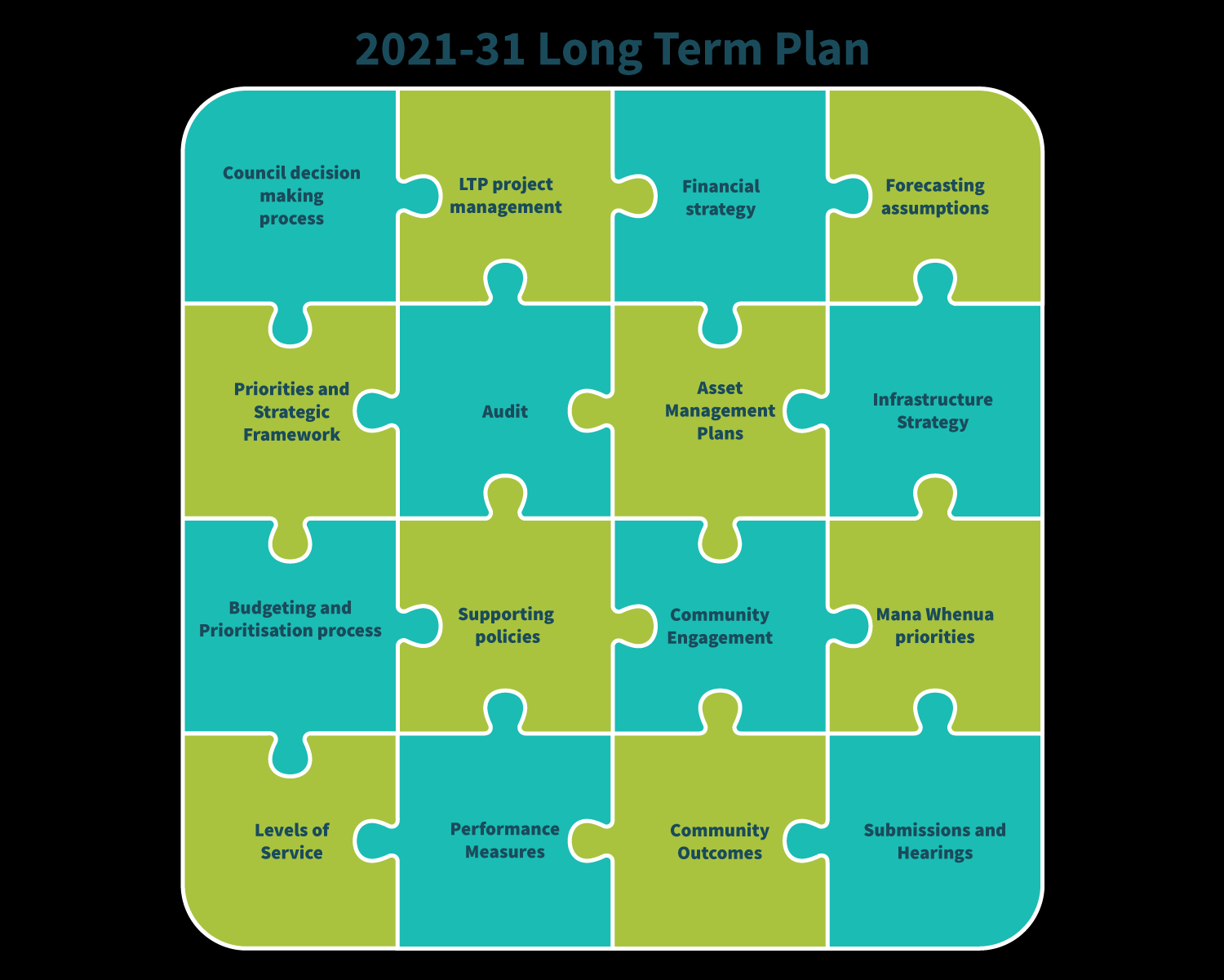

2021-31 Long Term Plan -

2021-31 Long Term Plan -

Economic and Financial Strategy Briefing

Workshop Outline

Purpose of workshop:

To provide information to Council to help inform decisions regarding the 2021-31 Long

Term Plan (LTP) Infrastructure and Financial Strategies and to discuss desired rating levels

for the coming years

Items to be discussed:

•

LTP overview and update – Tracy Plane (Manager Strategic and Corporate Planning)

•

Economic outlook and recovery – Jake Gilmer (Senior Strategic Advisor)

•

Asset Management and Infrastructure Strategy – Nicci Wood (Asset Management Advisor)

•

GW Financial Strategy and rates affordability – Tony Stallinger (interim CFO)

LTP overview – how it fits together

LTP overview – how it fits together

LTP Assumptions

Climate Change

Technology

Legislation and Governance

Partnerships with Mana Whenua and Māori

LTP Assumptions

Climate Change

Technology

Legislation and Governance

Partnerships with Mana Whenua and Māori

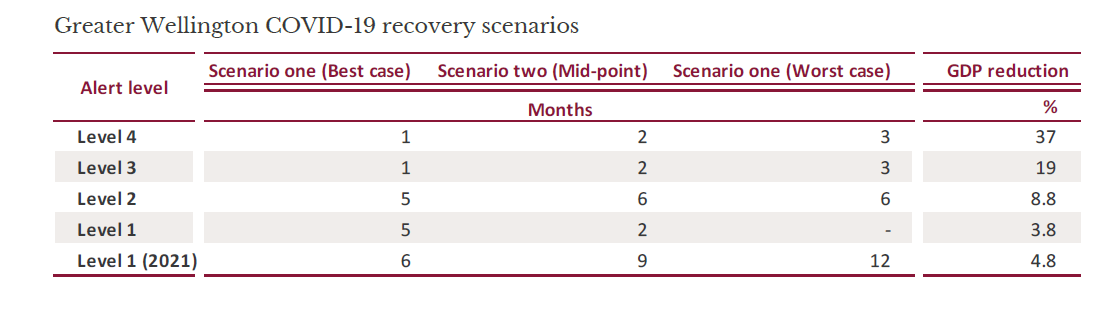

COVID-19 Recovery Scenarios

Alert level

Cumulative months as of 14 August 2020

COVID-19 Recovery Scenarios

Alert level

Cumulative months as of 14 August 2020

Level 4

1

Level 3

1

Level 2

1

Level 1

1

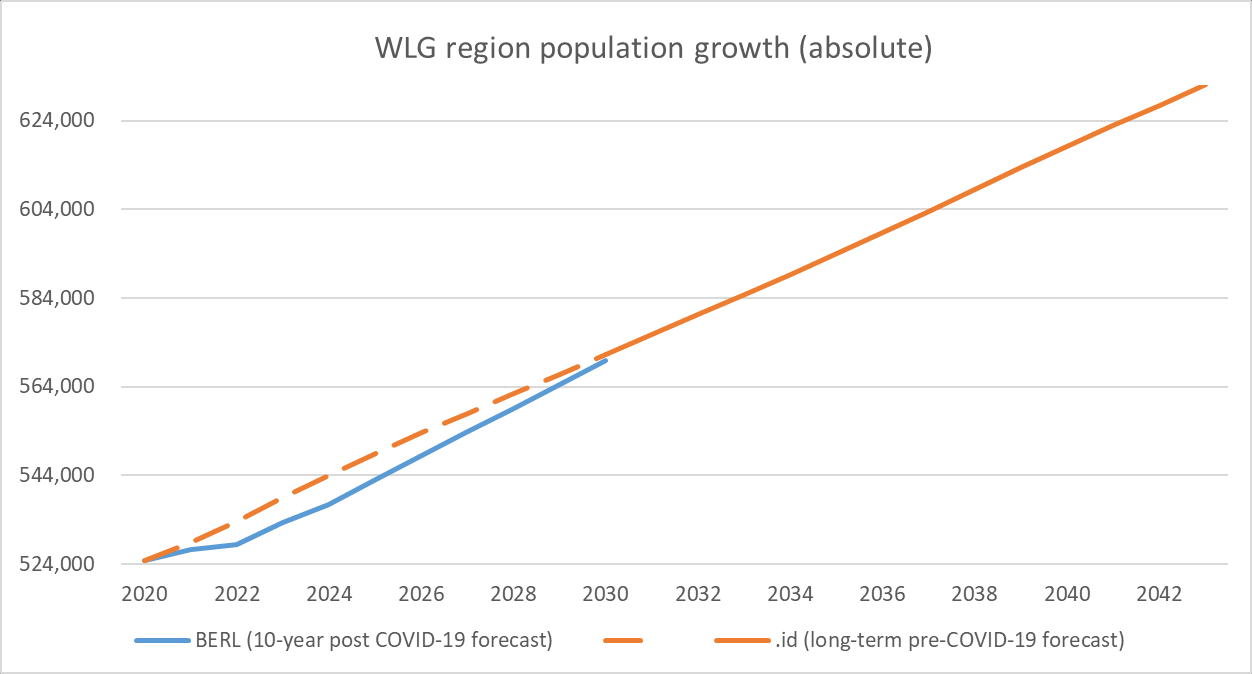

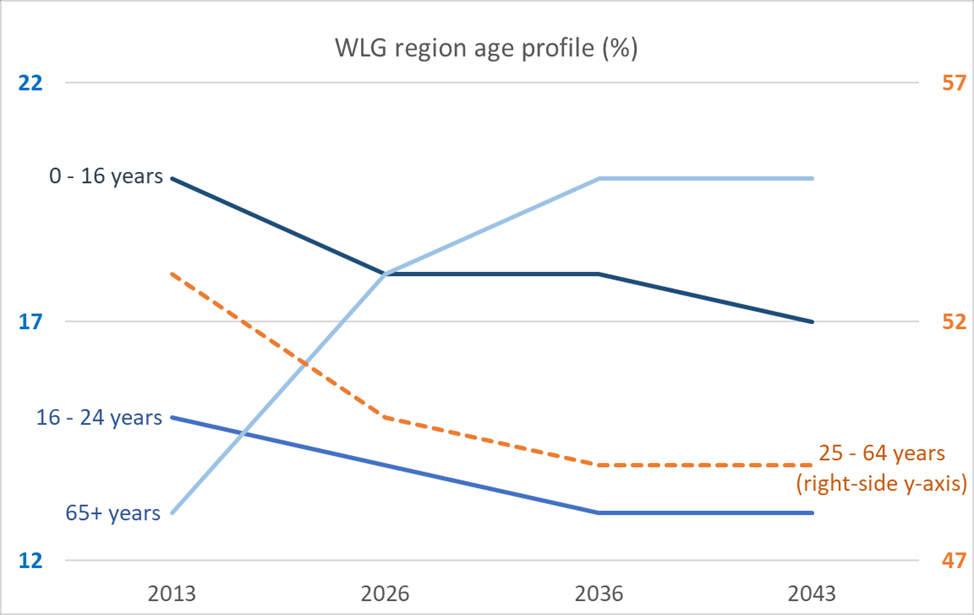

Population Trends

Population Trends

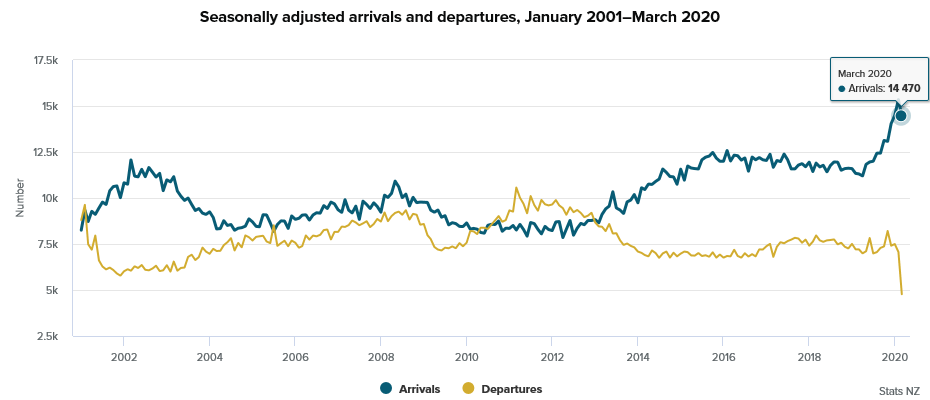

Population – COVID-19 Impact on Migration

Population – COVID-19 Impact on Migration

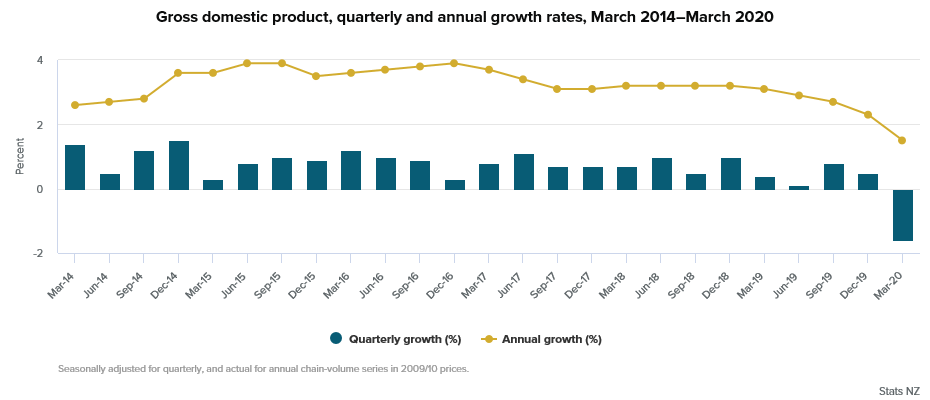

Economy – Gross Domestic Product

Economy – Gross Domestic Product

Economy – Unemployment

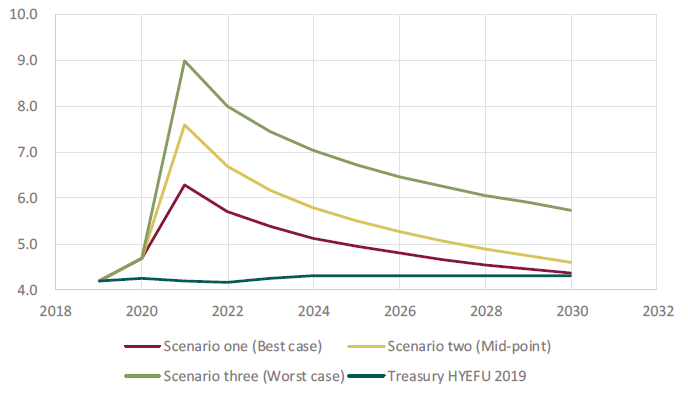

COVID-19 Unemployment Scenarios

Employment at a glance

June

Quarterly

Annual change

(seasonally adjusted)

2020 quarter

change

Economy – Unemployment

COVID-19 Unemployment Scenarios

Employment at a glance

June

Quarterly

Annual change

(seasonally adjusted)

2020 quarter

change

Percent

Percentage points

Unemployment rate

4.0

-0.2

0.0

Underutilisation rate

12.0

1.6

0.9

Employment rate

66.9

-0.6

-0.6

Labour force participation

69.7

-0.8

-0.6

rate

(000)

Percent

Unemployed

111

-5.1

2.1

Employed

2665

-0.4

1.2

Filled jobs

1989

-0.5

0.8

Working-age population

3984

0.5

2.0

Council Role in COVID-19 Response and Recovery

Council Role in COVID-19 Response and Recovery

Economic outlook summary

•

COVID-19 will impact population and economic growth over the next two years, even

under the best case scenario

•

Local and regional government spending can help keep people employed and stimulate

the economy

•

But that needs to be balanced with rates affordability and consideration of

unemployment levels

Any thoughts or comments before we move on to the next section?

Infrastructure Strategy

Infrastructure Strategy

Outline

•

Infrastructure Strategy: What, why, how

•

Audit NZ & SOLGM expectations

•

Significant issues and cross cutting theme

•

Options and decisions

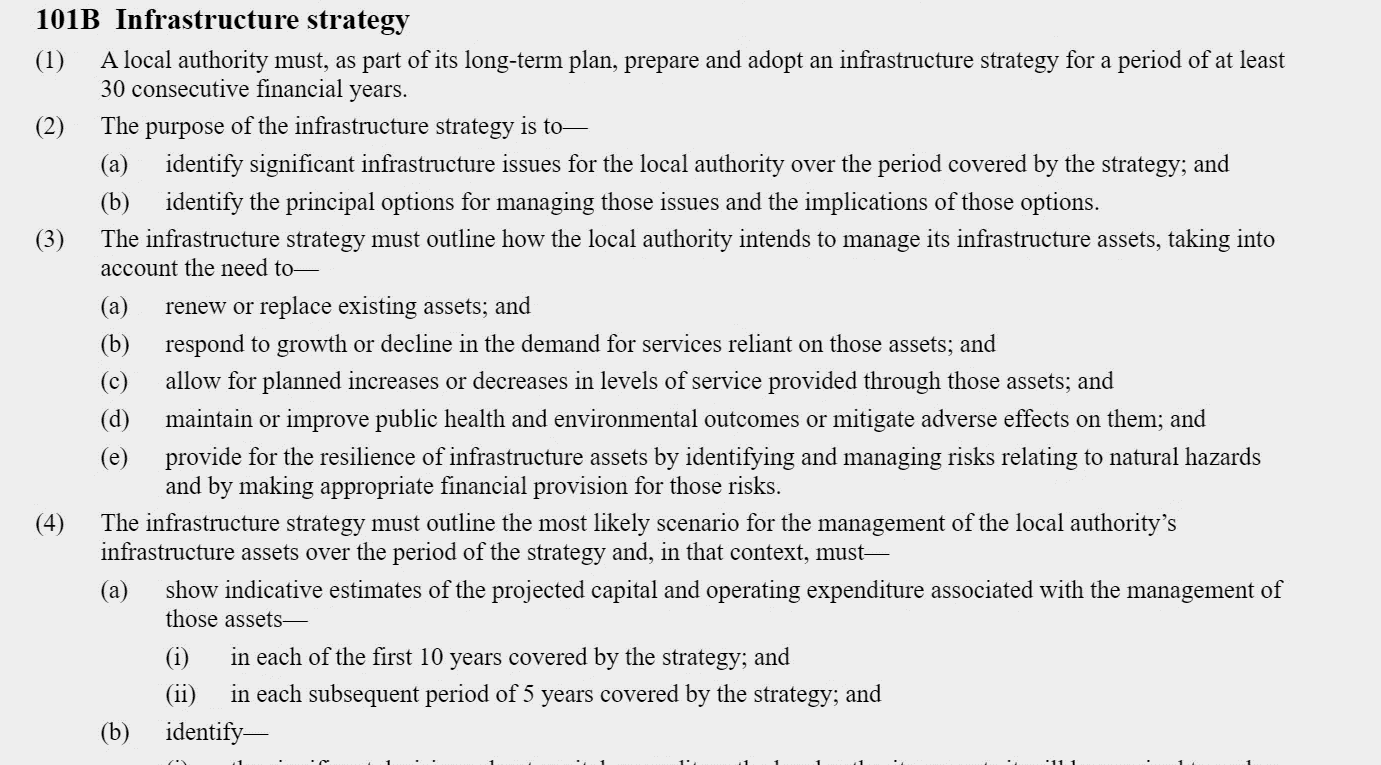

Section 101B of the Local Government Act

Section 101B of the Local Government Act

Principles Approach

• Forward looking

• Optimal

• Adaptive

• Coordinated

What when how.

Greater Wellington’s Infrastructure Strategy tells you

how we plan to manage our infrastructure over the next

30 years, to support the vision we have for the region.

It defines the nature of the challenges, our

approach and actions for dealing with the challenges;

and the implications of these actions

Audit NZ’S Key Disclosures

•

Clear approach to lifecycle asset management

•

Comprehensive discussion of climate change risks and our long

term responses.

•

Ratepayer affordability

GWRC infrastructure asset groups

•

Public Transport;

•

Water Supply;

•

Flood Protection;

•

Environmental Monitoring;

•

Parks; and

•

Harbour Management

Assumptions, Future Demand and Risk

Assumptions, Future Demand and Risk

The significant infrastructure issues for the region are:

•

Achieving zero carbon 2030

•

Improving resilience

•

Managing critical infrastructure

•

COVID-19 recovery

The cross cutting theme-

•

Affordability

Principle options for managing issues – carbon zero

Issues

Options

Most likely scenario

Policy changes (low carbon consideration policy,

Energy and low carbon first)

Eliminate operational carbon to meet carbon

Retire grazing land

EV bus fleet

zero 2030

Changes to levels of service.

Retire grazing leases

Grazing in Parks

Low carbon accelerator funding

Reforestation and offsetting

MetLink bus and train fleet.

Energy initiatives

New power supplier

Corporate machinery

New infrastructure, investment and policy

Low carbon Accelerator Fund

Energy treating and delivering water supply

Do nothing- submit to >2oC warming /accept

climate crisis

Policy changes (low carbon capital)

PFSI (Permanent Forest Sink) registration of area

Mitigating capital/ embodied carbon of assets review

Off site construction

lifecycle

Low carbon Accelerator Fund

Low carbon Accelerator Fund

Reduce carbon in newly-built assets and

materials, manufacturing, transportation, labour New ways of thinking and working

Drive development of new low carbon products

and end-of-life

– i.e. cement free concrete

Innovation in digital technologies, construction

techniques and development of standard

products.

Principle options for managing issues – resilience

Issues

Options

Most likely scenario

New investment – edge protection

Managed retreat.

Rail in region at risk sea level rise

Partnership investment for protection?

New ways of thinking and working

Accept risk

Rebuild as is

Parks assets at risk from undermining and sea level Retreat

Rebuild inland

rise

Retire activity - Policy changes

Innovation construction techniques

New investment for upgrades and renewal

Reprioritised Ngauranga reservoir strengthening

Innovation construction techniques and

Water supply at risk from seismic events

Ground strengthening Waterloo TP $2M

development of standard products.

Replacement of Kaitoke trunk main ($270mil)

Cross Harbour Pipeline

Vegetated ‘soft’ erosion edge protection

Hutt River erosion edge protection. Critical

Critical stopbank building and /or reconstruction

stopbank building.

Existing and potential land and development at

increasing flood risk

Retreat no new development in hazardous land – Ruamahanga River Scheme buffer land

new policies required

establishment and tree planting ($1m); stopbanks

reconstruction

Do nothing

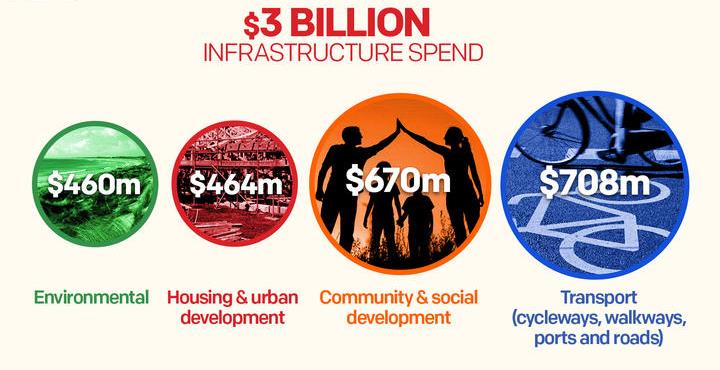

Principle options for managing issues – infrastructure

Issues

Options

Most likely scenario

$5M IN FUNDING FOR REGIONAL TRAINS

Greater public transport patronage requires

New infrastructure, investment and policy

$4M business case is being prepared

significant investment in infrastructure

Partnership to drive efficiencies

$6B for MRT under LGWM

$200M infra Commission funding for rail

New infrastructure, investment and policy

network upgrades – Improvements to rail line

Existing Metlink assets require ongoing

Partnerships

between Wellington, Wairarapa and Palmerston

investment to meet current LOS

North and Wellington Station safety

Decrease LOS

improvements

Upgrading and new assets

Optimisation of capacity at Te Marua upgrade

Integrated planning with WRGF

Future demand on water supply

$20M?

New source supply for growth

- Growth Porirua

Replacement of Kaitoke trunk main ($270mil)

Different technology

- Regional Growth Plan

Sustainable supply programme

Demand Management - Promoting water

Water meters

conservation

Key decisions

Significant Decision Required

Most Likely Scenario

Achieving Carbon Zero 2030

Capital Carbon options

Wetland restoration

Regional trains and EV bus fleet

Capital carbon lifecycle approach

Sustainable flood protection strategies

Ruamahanga River Scheme

Improving water supply resilience

Strengthening Ngauranga

Waterloo

Kaitoke bridge

Delivering a high quality, reliable public transport

network

Meeting future demands

Developing and committing to delivering Regional Growth

Framework

Lets Get Wellington Moving

RiverLink

Infrastructure Strategy Questions?

Infrastructure Strategy Questions?

Financial Strategy

Financial Strategy

Financial Strategy – guiding principles

We adopted a principle-based approach in developing our Financial Strategy centred on:

•

Fairness and intergenerational equity

•

Balanced budget

•

Borrowings funding

•

Distribution of benefits

•

Market neutrality

•

Willingness to pay

•

Value for money

•

Prudent

Financial Strategy – strategic direction

Our Financial Strategy focuses on these key elements:

•

Rates affordability

We balance demand for enhanced services with our communities’ ability to pay

•

Financial risk management

We have clear and effective risk management practices to protect core service delivery to our

communities

•

Investing in the right activities with appropriate funding and financing sources

We manage Infrastructure Strategy requirements within Financial Strategy limits. We select funding

sources in line with our Revenue and Financing Policy objectives

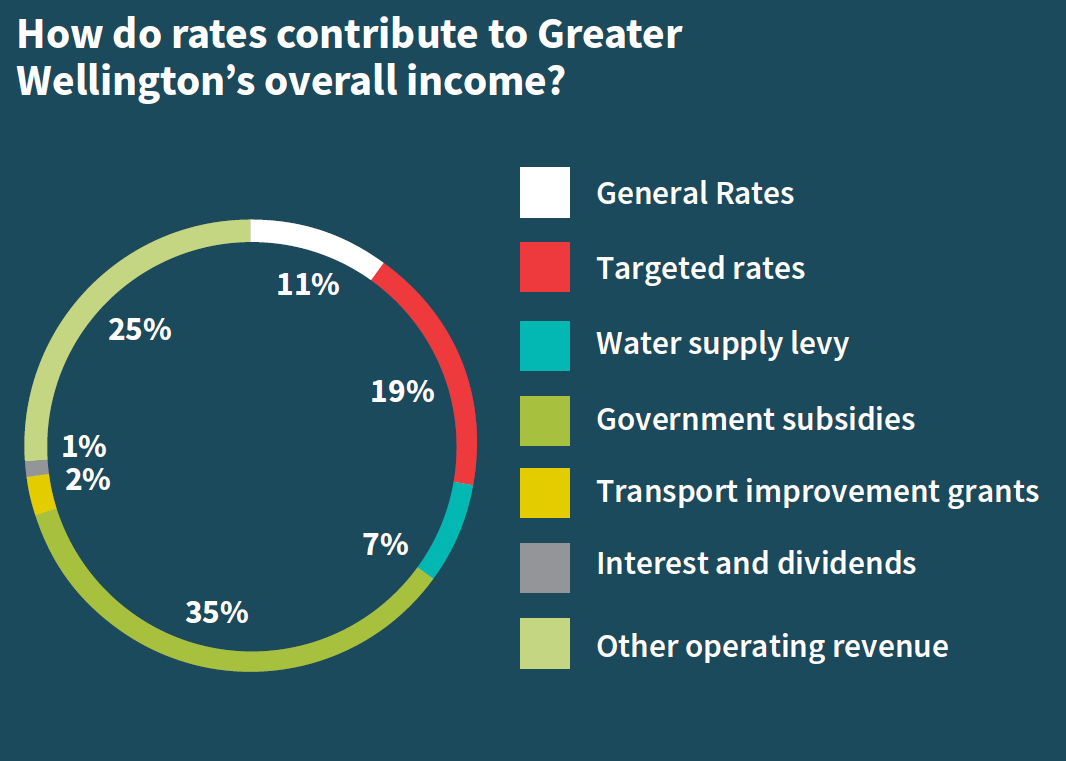

Revenue, rates and affordability

Revenue, rates and affordability

Composition of revenue

Composition of revenue

Rates and rates affordability

Rates and rates affordability

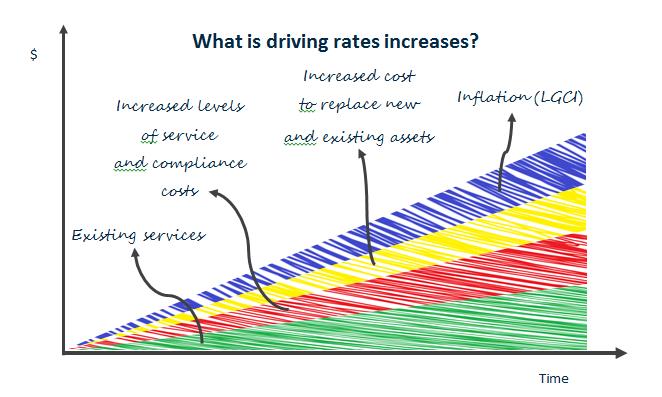

Rates and rates affordability cont….

Rates % increase vs inflation, household and consumer spending % change year on year

10.0%

5.0%

0.0%

2020/21

2021/22

2022/23

2023/24

2024/25

2025/26

2026/27

2027/28

2028/29

2029/30

2030/31

-5.0%

-10.0%

-15.0%

Limit on rates increase %: 2018 LTP

Inflation rate (LGCI)

Inflation rate CPI

Household incomes % increase

Consumer spending % increase

Rates and rates affordability cont….

Annual change in forecast rates revenue

12%

10%

8%

6%

4%

2%

0%

2014/15

2015/16

2016/17

2017/18

2018/19

2019/20

2020/21

2021/22

2022/23

2023/24

2024/25

2025/26

2026/27

2027/28

Rates increase %: LTP 2015

Rates increase %: LTP 2018

Actual rates increase %

What can our rates look like?

Options

Years 1-3

Years 4-10

Low

0% - 4%

3% - 8%

Main focus is on affordability and alleviation of economic hardship

Economic forecasts indicate rates increases maybe more affordable over this period

Less focus on supporting economic recovery and strategic priorities

Lower rates increases during years 1-3 will result in upward pressure on rates in subsequent years

Aligns with slower population growth and higher unemployment

Delayed projects and constrained service levels during years 1-3 will add to that pressure on rates

High priority on core services, keeping expenditure low and finding

as pressure mounts to catch up and enhance services

savings

Deferral of some significant projects and some service levels reduced

Minimal opportunity for new initiatives

Probable budget deficits in the short term

Medium

5% - 7%

3% - 10%

Balances focus on affordability and alleviation of economic hardship

Economic forecasts indicate rates increases maybe more affordable over this period

with delivering on strategic priorities

Continued pressure on service levels, project delivery and rates will continue, but at a lower level

High priority on core services

than the “low” option above

Emphasis on finding savings opportunities

Deferral of some projects and some service levels reduced to create

opportunity for new initiatives

Possibility of budget deficits in the short term

High

8% - 10%

3% - 12%

Main focus on continued investment to support economic recovery

Economic forecasts indicate rates increases maybe more affordable over this period

and our strategic priorities

Higher rates increases in years 1-3 will create more flexibility and ability to consider lower rates

Less focus on community affordability

increases in subsequent years

Projects deferred only if necessary due to delivery constraints

Demand for increased service levels and project delivery will be lower than other options, as

Savings identified to help fund new initiatives

investment levels were higher during years 1-3

Service levels maintained and increased in some areas

Higher likelihood of running a balanced budget