link to page 2 link to page 2 link to page 6 link to page 6

TOIA 20190500

Table of Contents

1.

Treasury Report - Options for regulatory responses to the growing obesity

1

problem

2.

Internship Research Project - Regulatory responses to address the growing obesity

5

problem in New Zealand - Final Report

20190500 TOIA Binder

Doc 1

Page 1 of 15

IN-CONFIDENCE

Treasury Report: Options for regulatory responses to the growing obesity

problem

Date:

17 November 2014

Report No:

T2014/1413

File Number:

SH-1-6-1

Action Sought

Action Sought

Deadline

Minister of Finance

Consider the attached report,

(Hon Bill English)

indicate if you would like to

discuss the report with the

Treasury, and

refer this Treasury Report and the

attached report to the Minister of

Health.

Contact for Telephone Discussion (if required)

Name

Position

Telephone

1st Contact

s9(2)(g)(i)

Analyst

s9(2)(k)

Ben McBride

Manager, Health

s9(2)(a)

Actions for the Minister’s Office Staff (if required)

Return the signed report to Treasury.

Refer a copy to the Minister of Health.

Enclosure:

Yes (attached)

Regulatory responses to address the growing obesity problem in New Zealand -

Final Report (Treasury:2986039v1) Add to worklist

Treasury:2991117v1

IN-CONFIDENCE

20190500 TOIA Binder

Doc 1

Page 2 of 15

IN-CONFIDENCE

Treasury Report: Options for regulatory responses to the growing

obesity problem

Executive Summary

This paper explores regulatory responses to the growing obesity problem. Regulatory

measures to combat obesity have been implemented internationally and there are often calls

for similar approaches to be implemented in New Zealand in the media and among

academics. The statistics on obesity in New Zealand have been worsening despite the

voluntary initiatives that have been implemented in recent years to combat the problem. This

has encouraged us to investigate potential regulatory responses that could be implemented

in New Zealand.

A third of New Zealand’s population is obese today and another third is overweight. Obesity

is expected to overtake tobacco use as the number one risk factor for health within the next

two years. An obese person incurs health care costs at least 25 percent higher than

someone of a normal weight. Therefore, with the increasing rates of obesity, health care

costs related to obesity are also expected to rise. Obesity is a key risk factor for a number of

chronic diseases and has links with diabetes, heart disease, stroke and coronary artery

disease. The rising rates of childhood obesity are of particular concern.

The environment we live in today has a huge impact on our lifestyles and is contributing to

the high rates of obesity. This environment, which facilitates and promotes weight gain, has

been named an ‘obesogenic’ environment. If this obesogenic environment is left

unaddressed, obesity rates, and subsequent health costs, are predicted to rise further.

The current approach to combat obesity involves a number of voluntary initiatives, which are

not underpinned by a coordinating strategy. Some regulatory and/or mandatory measures

may be required as an addition to the current initiatives to reverse the rising rates of obesity.

Based on international evidence and our engagement with academics in this field, we

consider that the most promising regulatory approaches to explore further are a sugar-

sweetened beverage tax, regulation of marketing to children and a mandatory front of pack

food labelling system. However, all options require trade-offs and further work would be

needed before making decisions about implementation.

Obesity is a complex problem and requires multiple initiatives to reverse the current trend.

Obesity has impacts on labour market participation, productivity and quality of life and

therefore cuts across several government sectors. A cross-government approach may be an

effective way to approach the obesity problem. We consider that an obesity target, perhaps

in the form of an additional BPS target, could help to encourage cross-government

collaboration and make this growing problem a priority area for cross-government action. A

target could also be used to focus on the connection between child obesity rates and

poverty.

Note: Pages 3-6 and 9 have been deleted as they are not

relevant to the request

T2014/1413 : Options for regulatory responses to the growing obesity problem

Page 2

IN-CONFIDENCE

20190500 TOIA Binder

Doc 1

Page 3 of 15

IN-CONFIDENCE

Some regulatory options show promise

12. The obesity epidemic is a growing problem internationally. There are international

examples of regulatory measures being implemented to combat the problem and

recently there have been calls for such measures to be implemented in New Zealand.

The Treasury Health Team has undertaken an initial review of a range of regulatory

measures that have been implemented internationally and identified in academic

research.

13. The attached report reflects international research and consultation with a number of

academics and identifies certain regulatory measures as promising options to target

obesity.

14. The options that show promise include a sugar-sweetened beverage tax, regulations

on marketing to children and a mandatory interpretive front of pack labelling system.

These regulatory initiatives could work well in combination with the voluntary measures

already in place. The reasons for suggesting these options as promising areas for

further investigation are summarised in the following section.

15. Some similar regulatory options are proposed in the recent New Zealand Medical

Association (NZMA) policy briefing,

Tackling Obesity, which recommends a sugar-

sweetened beverages tax, marketing regulation, front of pack labelling and licensing of

fast food premises.

Fiscal mechanism: Sugar-sweetened beverages tax

16. Sugar-sweetened beverages (SSB) deliver little to no nutrition, are heavily marketed to

children, contribute to poor diet and carry the risk of obesity, diabetes and other

diseases, as well as poor dental health.

17. Taxes on SSB have been introduced in a number of countries, including France,

Mexico, Finland, Hungary and a number of US states. Some international evidence has

shown these taxes to be effective in reducing consumption, for example, in France and

Hungary (National Heart Forum, 2012). A reduction in consumption of these beverages

in New Zealand is likely to have an impact on obesity rates as well as reducing

diabetes and poor dental health.

18. A SSB tax has the intended goal of changing the price of sugar-sweetened products

and ultimately changing consumer behaviour. A SSB tax may be a viable option for

New Zealand in principle, but further work would be required initially to ensure that a

SSB tax is the most appropriate and effective policy lever to help reduce obesity rates

and to determine that there is a strong rationale for targeting these products in

particular through taxation. There would then be policy trade-offs and design issues to

work through before a decision to proceed was made.

19. One concern about a SSB tax is that it may have negative distributional impacts

because the financial implications wil be more significant for lower socio-economic

groups. However, this might also have a progressive impact on health outcomes given

that there is a higher incidence of obesity-related disease within lower socio-economic

groups and they generally consume more unhealthy foods.

20. If additional work determined that there was a rationale for introducing a SSB tax,

design and implementation issues would then need to be considered. Further work and

analysis would be required on the level of the tax and inclusion criteria (e.g. powdered

drinks, juices, cordials, sports drinks, energy drinks, RTDs, etc.). There are likely to be

additional compliance costs for business and administration costs for government,

which would also need to be considered.

T2014/1413 : Options for regulatory responses to the growing obesity problem

Page 7

IN-CONFIDENCE

20190500 TOIA Binder

Doc 1

Page 4 of 15

IN-CONFIDENCE

21. Some opposition to a SSB tax could be expected from the beverage industry and we

have seen examples of this internationally. This is something to be considered as part

of further work on a SSB tax and this should involve working with and consulting

industry.

22. The attached report also covers other fiscal mechanisms to combat obesity, including a

saturated fat tax and removal of GST from fruit and vegetables. International evidence

has shown these regulatory measures to be less effective and more complex to

implement than a SSB tax.

Deleted - Not Relevant to Request

T2014/1413 : Options for regulatory responses to the growing obesity problem

Page 8

IN-CONFIDENCE

20190500 TOIA Binder

Doc 2

Page 5 of 15

y

ur

eas

Tr

Regulatory responses to address

Zealand

the growing obesity problem in New

Zealand

ew

N

s9(2)(g)(i)

February 2014

i

20190500 TOIA Binder

Doc 2

Page 6 of 15

I N T E R N S H I P R E S E A R C H

Regulatory responses to address the growing obesity problem in

P R O J E C T

New Zealand

M O N T H / Y E A R

February 2014

N Z T R E A S U R Y

New Zealand Treasury

PO Box 3724

Wellington 6015

NEW ZEALAND

Email

[email address]

Telephone

64-4-472-2733

Website

www.treasury.govt.nz

D I S C L A I M E R

The views, opinions, findings, and conclusions or

recommendations expressed in this Policy Perspectives Paper

are strictly those of the author(s). They do not necessarily reflect

the views of the New Zealand Treasury. The Treasury takes no

responsibility for any errors or omissions in, or for the correctness

of, the information contained in these Policy Perspectives

Papers. The paper is presented not as policy, but to inform and

stimulate wider debate.

Acknowledgements: Ministry of Health, Ministry of Primary

Industries, Boyd Swinburn, Elaine Rush, Geoff Simmons, Tony

Blakely, Jim Mann, and Louise Signal for their contributions to

the paper.

ii

Note: Pages i, iii and iv have been deleted as they

are not relevant to the request

20190500 TOIA Binder

Doc 2

Page 7 of 15

1

Executive Summary

This report assesses the regulatory responses appropriate for New Zealand to employ in

order to address the growing problem of obesity.

In 2013 the New Zealand adult obesity rate was 31 per cent, with a further 35 per cent

overweight (Ministry of Health, 2013). This rate has increased threefold since 1977

representing an escalating problem. Obesity has significant impacts upon health and

productivity costs, with the growing problem having serious implications for future economic

growth and sustainability. It is important to understand how improvements in health

outcomes can provide benefits to population wellbeing.

Obesity is a complex problem with a number of inter-related causes, which are stil not

completely understood. The current problem in New Zealand is generally seen to stem from

an obesogenic environment: an environment that facilitates and promotes weight gain.

The current policy approach to obesity in New Zealand focuses on initiatives that aim to

support and encourage individuals to lead healthier lifestyles and encourage the food

industry to provide healthier products and inform consumers.

The purpose of this paper is to investigate the role and effectiveness of a range of

regulatory measures that the government could implement in response to the growing

obesity crisis. The options considered are:

• An interpretive front of pack labelling system

• Regulation of marketing to children

• A sugar-sweetened beverage tax

• A saturated fat tax

• Removal of GST from fruit and vegetables.

The options focus on targeting the price and information aspects of the obesogenic

environment. The tax and GST options have been analysed from a health policy

perspective, rather than focusing on the precise mechanism (for example, excise tax vs.

sales tax). Each measure has been selected due to international application and substantive

evidence.

From analysis, it is evident that promising areas for further work include a sugar-sweetened

beverage tax, an interpretive front of pack labelling system, and regulation of marketing to

children.

A sugar-sweetened beverage tax would lead to a reduction in the consumption of sugar-

sweetened beverages. According to Briggs et al. (2013) a 20 per cent tax on sugar-

sweetened beverages could reduce consumption by 16 per cent. A UK study found a 20 per

1

20190500 TOIA Binder

Doc 2

Page 8 of 15

cent tax on sugar-sweetened beverages in the UK would have a 1.3 per cent reduction in

the prevalence of obesity (Briggs et al., 2013). It would also have a number of health

benefits, with a particular benefit on diabetes rates and dental health. There are concerns

that the tax would have greater financial implications for lower socio-economic groups.

However, some have suggested that this would be progressive in terms of health outcomes

as low socio-economic groups have a higher incidence of obesity. There are a number of

areas for further work, such as the mechanism by which the tax could be introduced, and a

number of policy formulation and implementation issues to consider.

Interpretive front of pack labelling is a policy that would provide the population with greater

information about food composition and would therefore drive behavioural change among

consumers to reduce consumption of products high in sugar, fat and salt. Evidence shows

there can also be an effect on producers in the space of product reformulation. The main

drawback of this policy is the impact on producers. A strong industry push back is to be

expected due to producer losses, product reputation and reduced sales of foods; however,

the gains in health impacts are seen to outweigh the costs. An area requiring further work in

this policy is defining the optimal interpretive system of front of pack labelling for New

Zealand, such as the ‘Health Star Rating’ or ‘Traffic Light’ systems. In addition, further work

into the possible implementation issues and costs to the producer would be required.

Finally, placing restrictions on marketing to children is a regulatory measure that would

reduce exposure to advertising for unhealthy foods, which could ultimately reduce demand

for these products and have benefits upon consumption. An issue of this approach is the

various media that are used by firms; regulations would have to consider an approach to

target a range of advertising media, which is likely to be complicated for some. There are

several issues that require further work namely policy formulation issues, such as the most

effective way to introduce the restrictions. It would be important to avoid unintended

consequences such as those that arose in Britain, where the policy increased children's

exposure to marketing as the restrictions were poorly targeted and implemented (elaborated

on p.18).

Whilst a sugar-sweetened beverage tax appears as a consideration for further work, a

saturated fat tax has not been considered due to a number of significant economic

implications, which have been seen from the Denmark experience. This is largely attributed

to implementation issues. In addition, the effect upon consumption is viewed as ambiguous;

this is mainly due to difficulties in specification and administration, the potential for increase

in other food consumption (e.g. salty foods) due to cross price elasticities, and push back

from powerful dairy and meat industries.

Another policy that has not been recommended is the removal of GST from fruit and

vegetables. This policy represents a loss of key government income, would compromise

GST efficiency, and has an unclear impact on obesity. Higher intakes of fruit and vegetabl

es

are likely to have a health benefit; however, there are issues regarding efficiency and equity

in using GST to achieve this increase (elaborated in section 5.5.3). Other mechanisms that

could be used to achieve an increase in fruit and vegetable consumption without

compromising the GST efficiency should be investigated.

2

Note: Pages 3-12 have been deleted

as they are not relevant to the request

20190500 TOIA Binder

Doc 2

Page 9 of 15

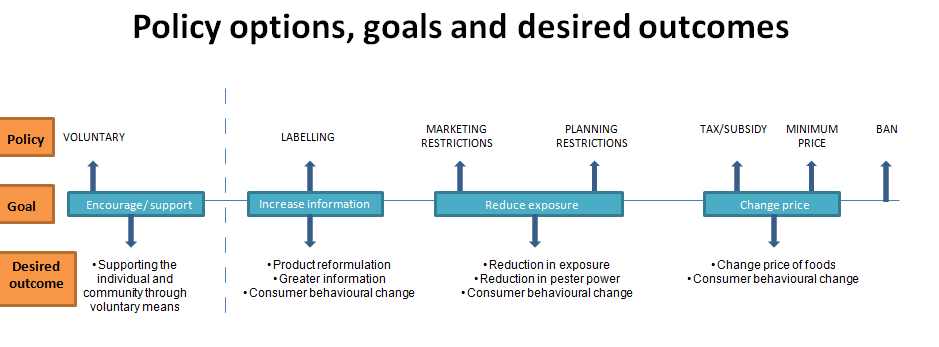

5 Regulatory measures

5.1 Regulatory options considered

Figure 5 shows a range of measures that could be adopted to address obesity. This paper

focuses on the following regulatory options:

• Interpretive front of pack labelling

• Regulation of marketing to children

• Pricing mechanisms:

o Sugar-sweetened beverage tax

o Saturated fat tax

o Removal of GST from fruit and vegetables

These options are the most widely considered and commonly implemented internationally.

However, due to the complexity of the problem there is scope for further research into other

regulatory measures including minimum pricing, planning restrictions and banning of goods.

These are shown on the continuum below, along with voluntary measures (see Figure 5).

Figure 5: Policy options, goals and desired outcomes

13

20190500 TOIA Binder

Doc 2

Page 10 of 15

5.2 Criteria for assessing regulatory measures

The following criteria wil be used to assess the regulatory options:

• Impact on consumption

• Efficiency and cost-effectiveness

• Acceptability: Stakeholder support

• Costs

• Feasibility

• Effects on equity

• Positive and negative impacts

The Treasury Living Standards framework has been considered where appropriate (as seen

from Figure 4):

• Economic Growth

• Sustainability for the Future

• Increasing Equity

• Social Infrastructure

• Reducing Risks.

The discussion of each regulatory option sets out the main issues to consider against the

options. A full analysis against all the criteria is in the Appendix (page 34).

5.3 Interpretive front of pack labelling

Deleted - Not Relevant to Request

14

Note: Pages 15-19 have been

deleted as they are not relevant to

the request

20190500 TOIA Binder

Doc 2

Page 11 of 15

Deleted - Not Relevant to Request

5.5.1 Sugar-sweetened beverage tax

A sugar-sweetened beverage tax would tax beverages containing added sugar. Sugar-

sweetened beverages include carbonated soft drinks, sports drinks, fruit drinks, flavoured

waters, sweetened teas, ready-to-drink coffees, and other non-alcoholic drinks containing

added sugars.

Rationale

There is evidence that taxes on foods with high sugar content can reduce consumption,

provided that the rate of tax is sufficiently high. Particular interest has been placed in sugar-

sweetened beverages because of their strong association with obesity, diabetes and dental

health.

20

20190500 TOIA Binder

Doc 2

Page 12 of 15

Sugar-sweetened beverages deliver little to no nutrition, are heavily marketed to children,

contribute to poor diet, and carry the risk of obesity, diabetes and other diseases (Brownell

& Friedman, 2012). The Global Burden of Disease panel estimates 0.6 per cent of deaths

worldwide per year can be attributed to diets high in sugar-sweetened beverages (Blakely et

al., 2014). By reducing consumption of these beverages through taxation, it is assumed

calorie intake will fall as people will be incentivised to reduce consumption. They may also

substitute these beverages for healthier alternatives, reducing sugar intake.

International application

Internationally a number of countries have introduced sugar-sweetened beverage taxes,

including France, Mexico, Finland and a number of US states (Landon & Graff, 2012). In

2011 Hungary introduced a sugar-sweetened beverage tax, and from evidence has proven

successful in reducing consumption.

Analysis of a sugar-sweetened beverage tax in New Zealand

Evidence of effectiveness

Sugar-sweetened beverage taxes have been associated with reductions in consumption.

Evidence from Hungary has reported consumption of sugar-sweetened beverages was

almost halved after the tax implemented in 2011 (Landon & Graff, 2012). Before the tax was

levied Hungary had an average soft drink intake of 290ml per day, with young people

obtaining 7 per cent of their daily energy from soft drinks (Landon & Graff, 2012). Following

the introduction of the tax, soft drink consumption in Hungary fell from 117 million litres to 69

million litres in the last quarter of 2011 (Landon & Graff, 2012). A New Zealand modelling

study found a decrease in consumption by 24 per cent when a 10 per cent tax was applied

to sugar-sweetened soft drinks (Eyles et al., 2012). In a recent study, Briggs et al. (2013)

found that a 20 per cent tax on sugar-sweetened beverages would reduce consumption by

up to 16 per cent. Evidence from other international taxes is still yet to be published.

Evidence from the Briggs et al. (2013) study suggested elasticity for sugar-sweetened

beverages was between 0.92 and -0.81, suggesting they are relatively elastic in nature. For

the lowest socio-economic group elasticity was estimated at -1.03 suggesting the reductions

would be proportionate to the increase in price (Briggs et al., 2013). This suggests a high

level of substitution with diet beverages or beverages containing no sugar content.

If the tax level was high enough there would be an impact on obesity in New Zealand. A

sugar-sweetened beverage tax is likely to have impacts on reduced consumption and

reductions on the rate of obesity. Modelling by Briggs et al. (2013) predicted that a 20 per

cent tax on sugar-sweetened beverages would reduce the prevalence of obesity in the UK

by 1.3 per cent, whilst a study in India by Basu et al. (2014) estimated that a 20 per cent

sugar-sweetened beverage tax would avert 4.2 per cent of the prevalence of obesi ty in

India. It is unclear if the obesity impacts would be to the same level in New Zealand;

however both represent promising indications in reductions of obesity (Blakely et al., 2014).

In addition to positive obesity outcomes there are reported benefits for diabetes, dental

cavities and a number of health conditions (Brownell & Friedman, 2012). Basu et al. (2014)

found that a 20 per cent sugar-sweetened beverage tax could reduce the incidence of

diabetes by 2.3 per cent from 2014 to 2023 (Blakely et al., 2014).

21

20190500 TOIA Binder

Doc 2

Page 13 of 15

Financial implications for low socio-economic groups

There are several concerns that a sugar-sweetened beverage tax would have greater

financial implications for lower socio-economic groups. However some have suggested that

this would be progressive in terms of health outcomes as poor people have a higher

incidence of disease, and consume less healthy food (Briggs et al., 2013). Consequently,

the greater absolute reduction in obesity would be assumed to be among poor people who

have a higher prevalence of obesity.

Industry push back

Opposition to a tax is to be expected from the beverage industry due to the high profitability

of sugar-sweetened beverage consumption and significant vested interests (Brownwel &

Frieden, 2009). From international experience, industry has opposed sugar-sweetened

beverage taxes and in many countries industry has spent large amounts of money to lobby

for the abolition of the tax (Lavin & Timpson, 2013).

Policy formulation issues

In the New Zealand context, an excise tax on these products is feasible whilst other designs

are likely to be complicated and ineffective. Issues with a sugar-sweetened beverage tax

raise a number of issues surrounding artificial sweeteners’ and the beverages subjected in

the tax. Internationally there is conflicting evidence surrounding artificial sweeteners, this

would have to be further considered in the policy design stage, with scope for artificial

sweeteners to be included in the tax (Fowler et al., 2008). However, it is important to

consider the switch from sugar-sweetened beverages to artificial y sweetened beverages as

a positive shift in reducing sugar intake, although it is not as healthy as a switch to water or

milk beverages. Some retailers may not pass on the tax to consumers and instead may

absorb the price increases as sugar-sweetened beverages are commonly used as a ‘loss

leader’ by a number of retailers.

Summary

Evidence suggests that a sugar-sweetened beverage tax would reduce consumption of

sugar-sweetened beverages and caries the prevalence of obesity. It would have a number

of health benefits, with a particular benefit in reducing diabetes and reducing poor dental

health. The benefit is highly likely to be progressive (this has been seen in tobacco taxation),

however there are concerns that the tax would have greater financial implications for lower

socio-economic groups. Some have suggested that this is progressive in terms of health

outcomes, and it is viewed as correctly targeting the groups with the highest prevalence of

obesity. There are a number of areas for further work, such as the mechanism by which the

tax could be introduced, and a number of policy formulation issues to consider.

5.5.2 Saturated fat tax

Deleted - Not Relevant to Request

22

Note: Pages 23-27 have been

deleted as they are not relevant to

the request

20190500 TOIA Binder

Doc 2

Page 14 of 15

6

Recommendations

6.1 Recommended approach

This paper suggests the most promising areas are:

• Sugar-sweetened beverage tax

• Regulations on marketing to children

• Interpretive front of pack labelling system

A sugar-sweetened beverage tax has been proposed as an area that could use further

work. This regulatory option has a number of benefits namely:

• A reduction in consumption of sugar-sweetened beverages, suggested up to 16 per

cent reduction in consumption from a 20 per cent tax.

• A number of health benefits, with a particular benefit on reducing diabetes, pre-

diabetes and a proven effect upon obesity.

• Increased revenue that could be used to support health promotion activities to

reduce obesity or prevent/treat diabetes.

Deleted - Not Relevant to Request

28

20190500 TOIA Binder

Doc 2

Page 15 of 15

Deleted - Not Relevant to Request

6.2 Areas for further work

6.2.1 Sugar-sweetened beverage tax

A sugar-sweetened beverage tax has the intended goal of changing the price of sugar-

sweetened products and ultimately changes in consumer behaviour. Further work would be

required on the level of the taxation, inclusion criteria (e.g. powdered drinks, juices, cordials,

sports drinks, energy drinks, RTDs etc) and the mechanism by which the tax is introduced.

There would have to be further work on the policy formulation issues, such as further

investigation into the harm of artificial sweeteners.

Deleted - Not Relevant to Request

29

Note: Pages 30-38 have been deleted

as they are not relevant to the request

Document Outline